Sharp increase in UK Yields as Starmer backtracks on welfare reforms, not supporting Reeves, ending up with none of the savings expected and a loss of credibility. UK 10-year yields are up by more than 17bp 4.63%! Bond yields are up across the board, including in the US (+5bp, 4.3% after dipping briefly below 4.20% yesterday), Germany (+4bp at 2.61%) for 10yr.

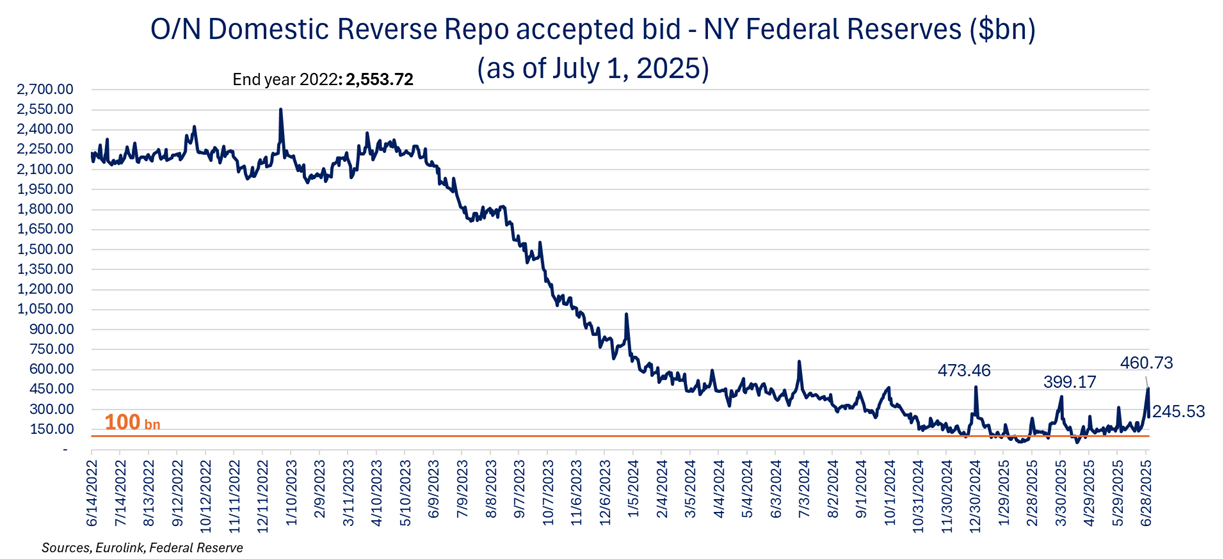

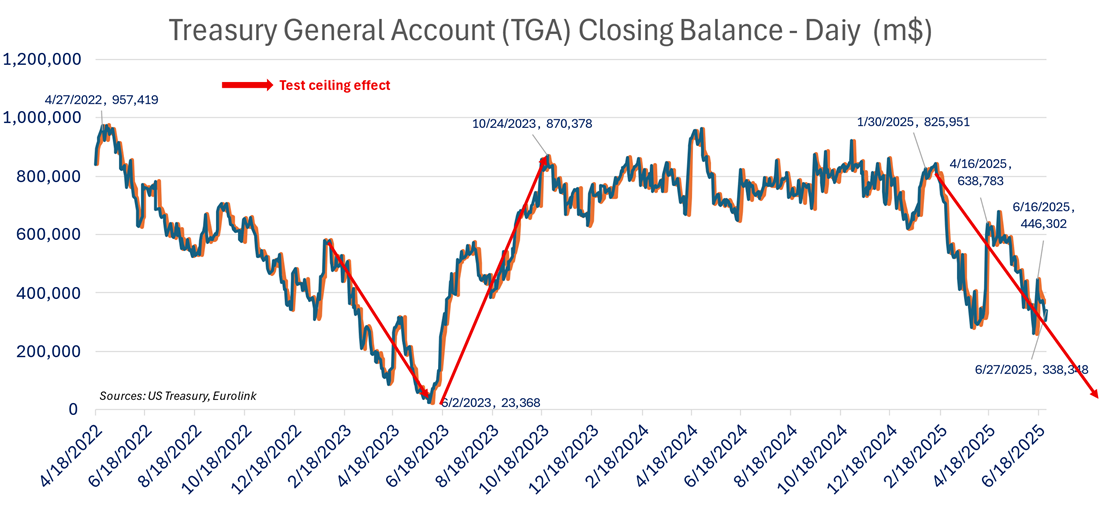

The UK episode is a good reminder that the global fiscal push will take a toll on yields. Bond markets are complacent going into the OBBB debate and the increase of the debt ceiling. We saw higher tension than usual for the mid-year end, with both SOFR and RR at the highest since year end. The debt ceiling removal associated with the bill will lead to higher issuance and tighter liquidity.

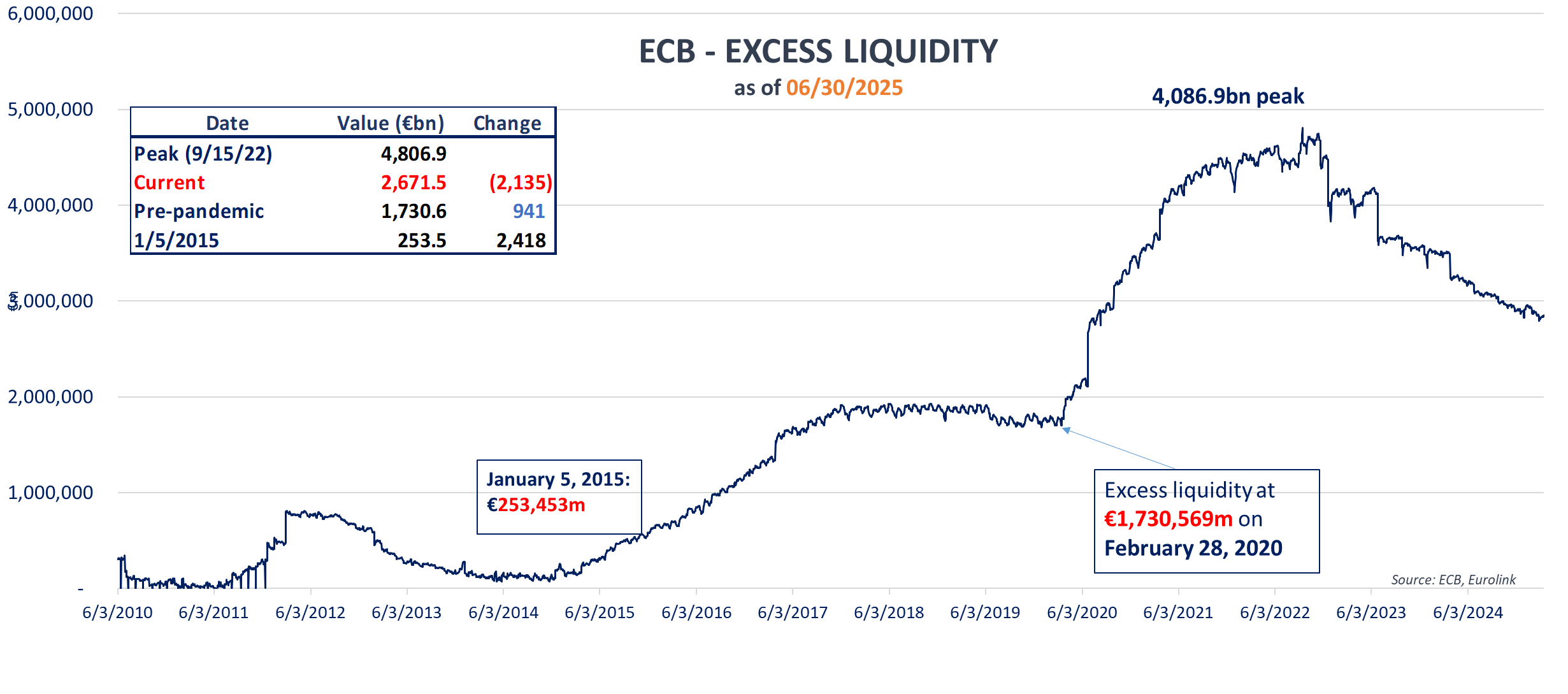

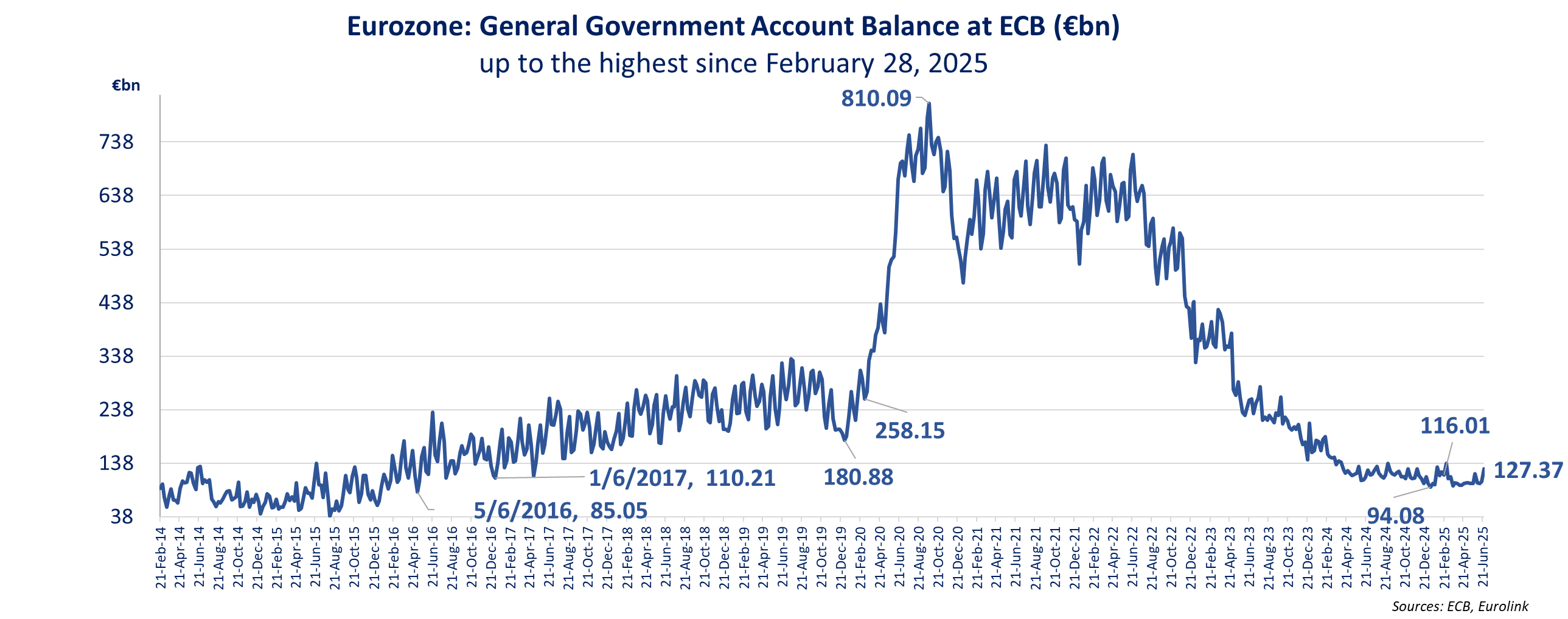

Liquidity tightened last week in the Eurozone (excess liquidity sown -37bn w/w) as the government account increased the most since end of February as reported by the ECB balance sheet update.

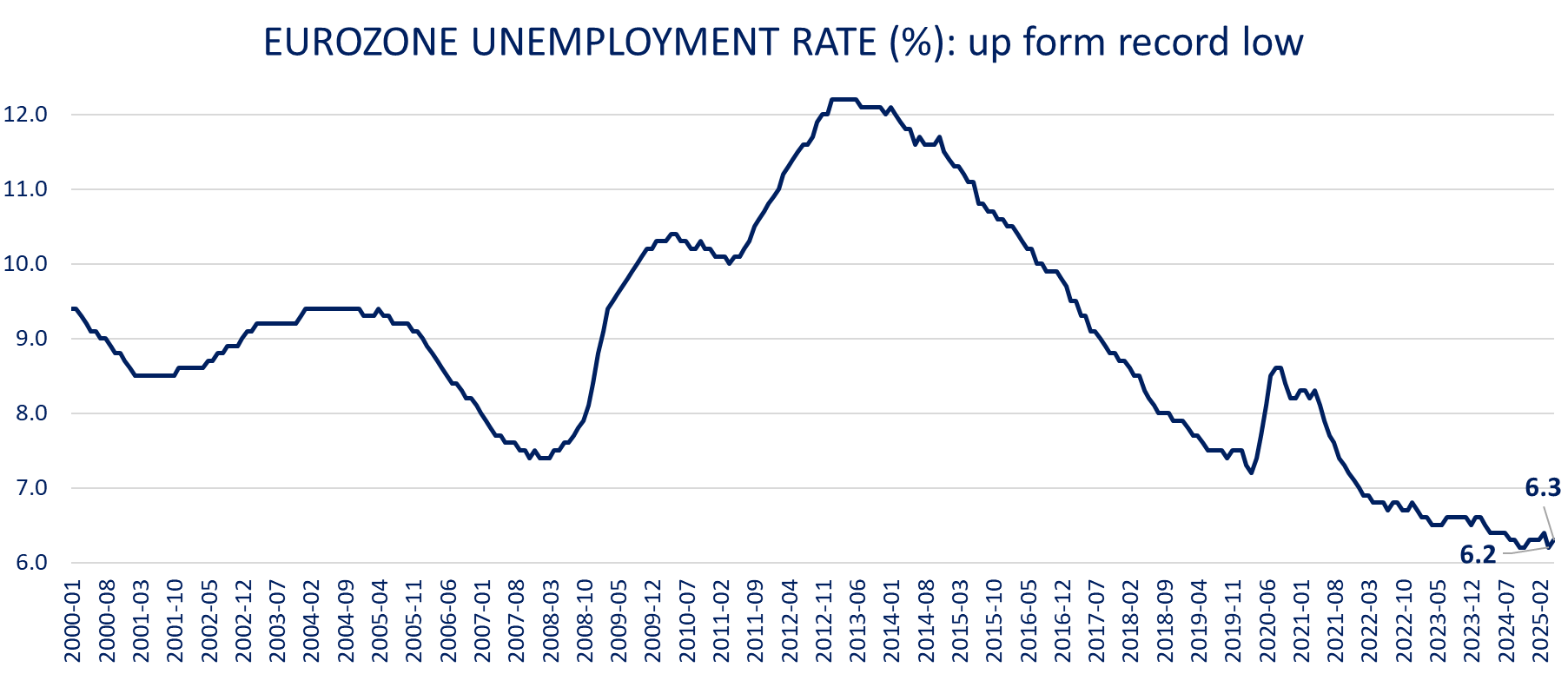

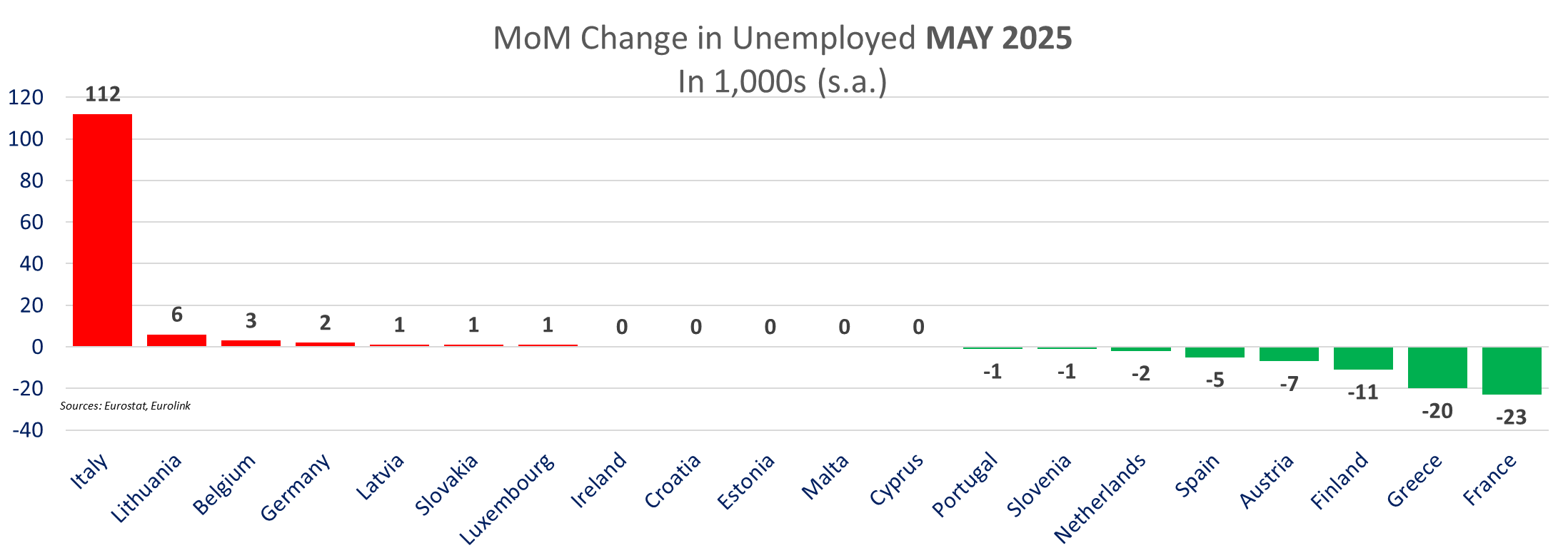

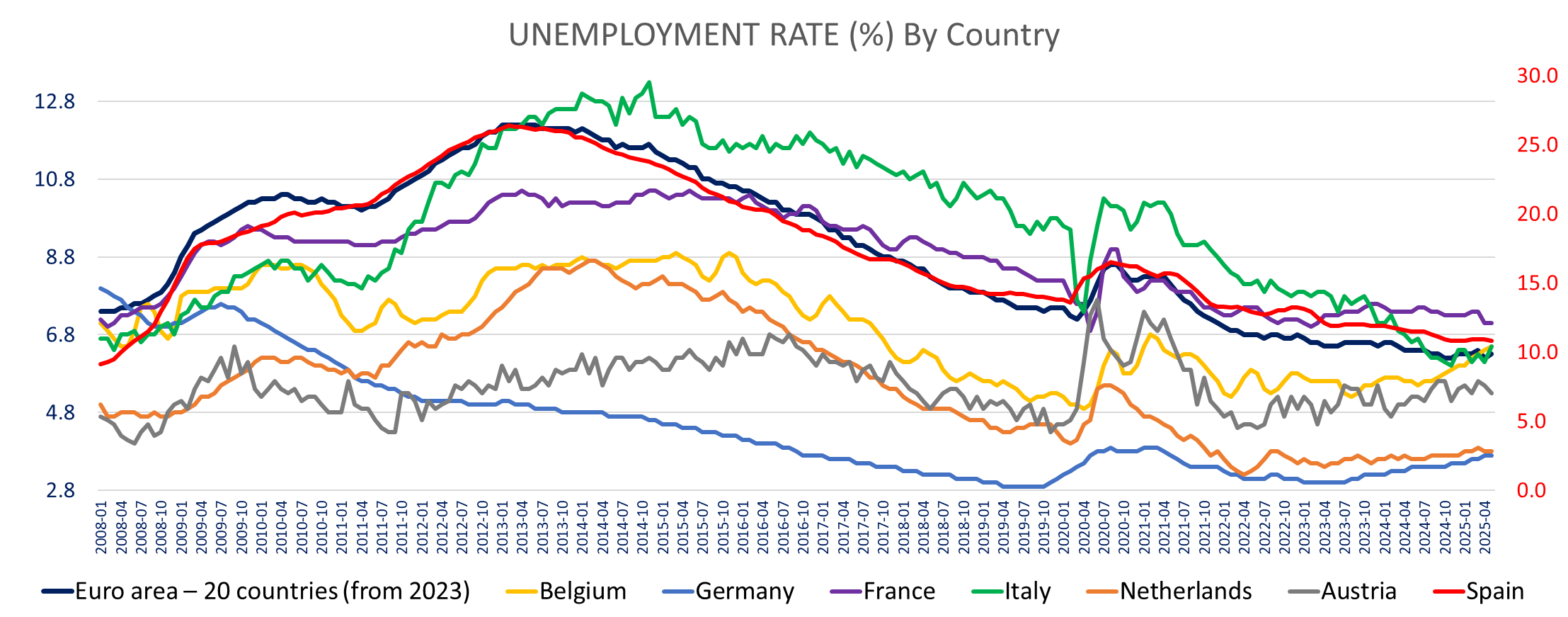

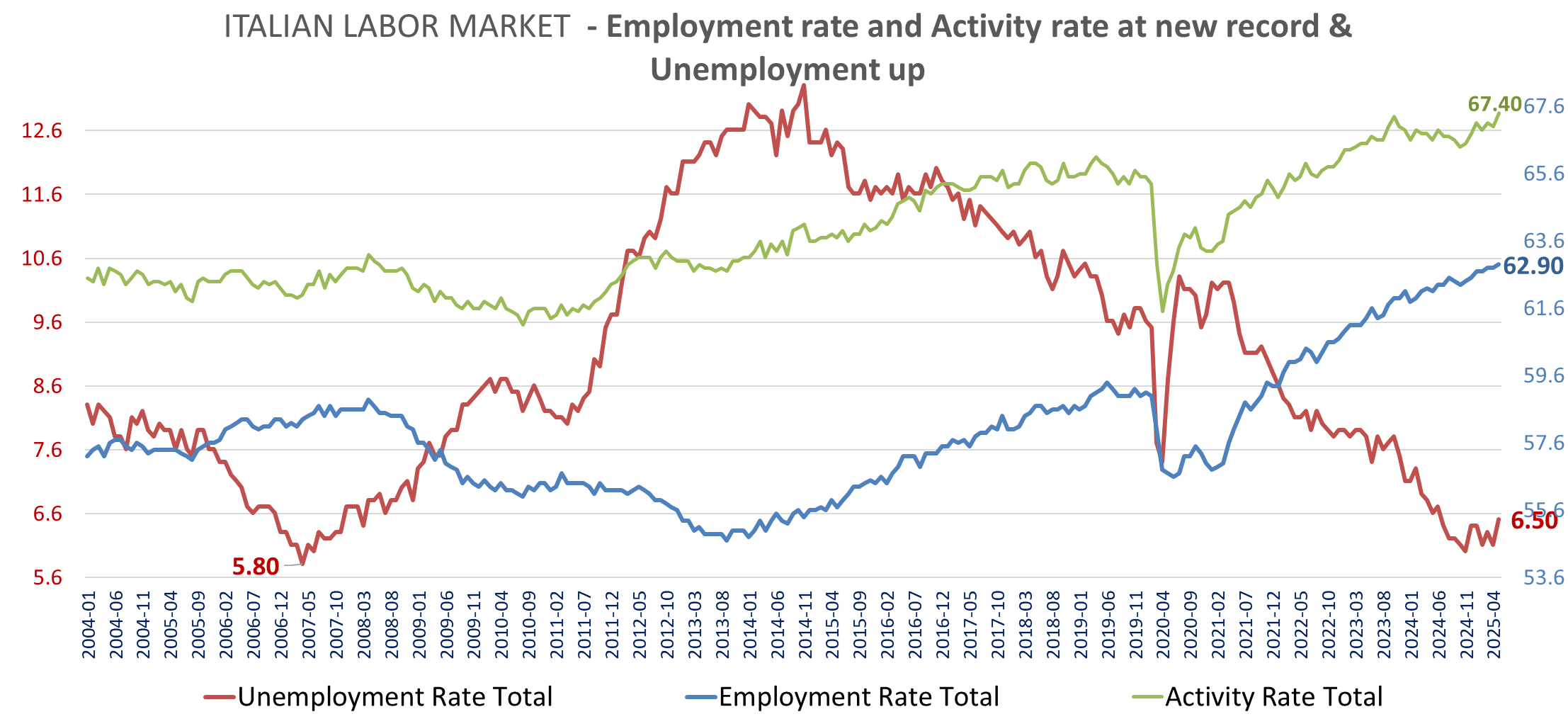

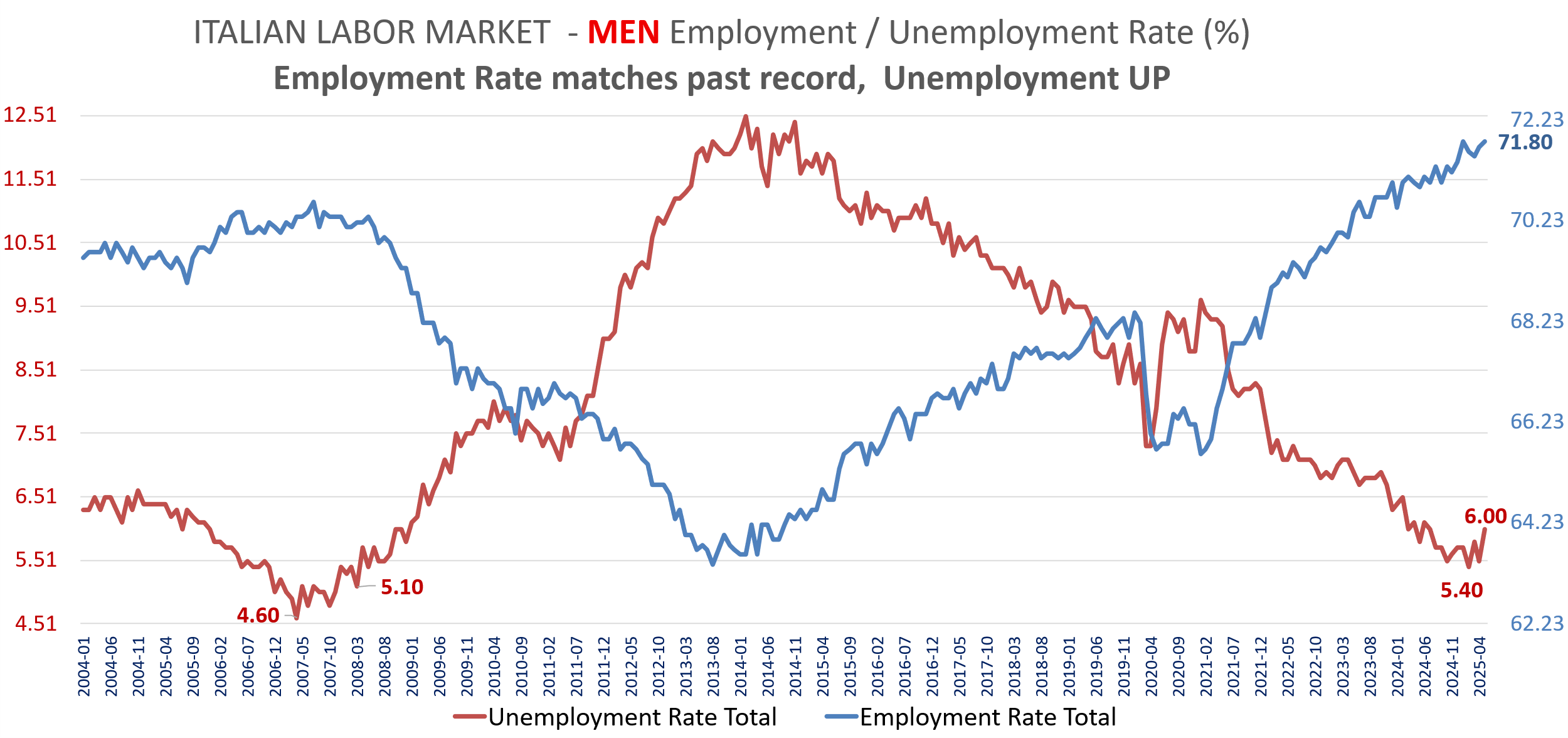

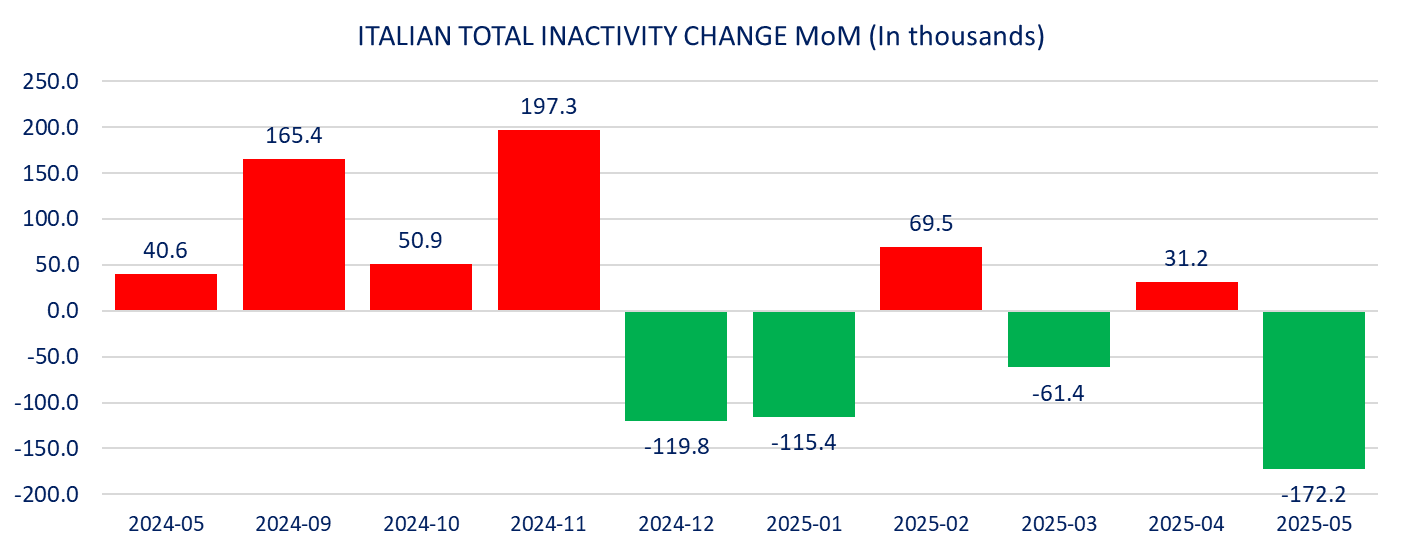

At first glance, the Eurozone labor market weakened in May with unemployment increasing 54k and the unemployment rate of the lows at 6.3% above expectations of 6.2%. The sharp increase in Italian unemployment (+112.6k m/m, 6.5% rate up from 6.1%) was the main factor behind the increase. As described in the Italian labor comments, the increase in unemployment in Italy coincides with a sharp increase in active population (+192k), record high activity rate and employment rate (notably older population).

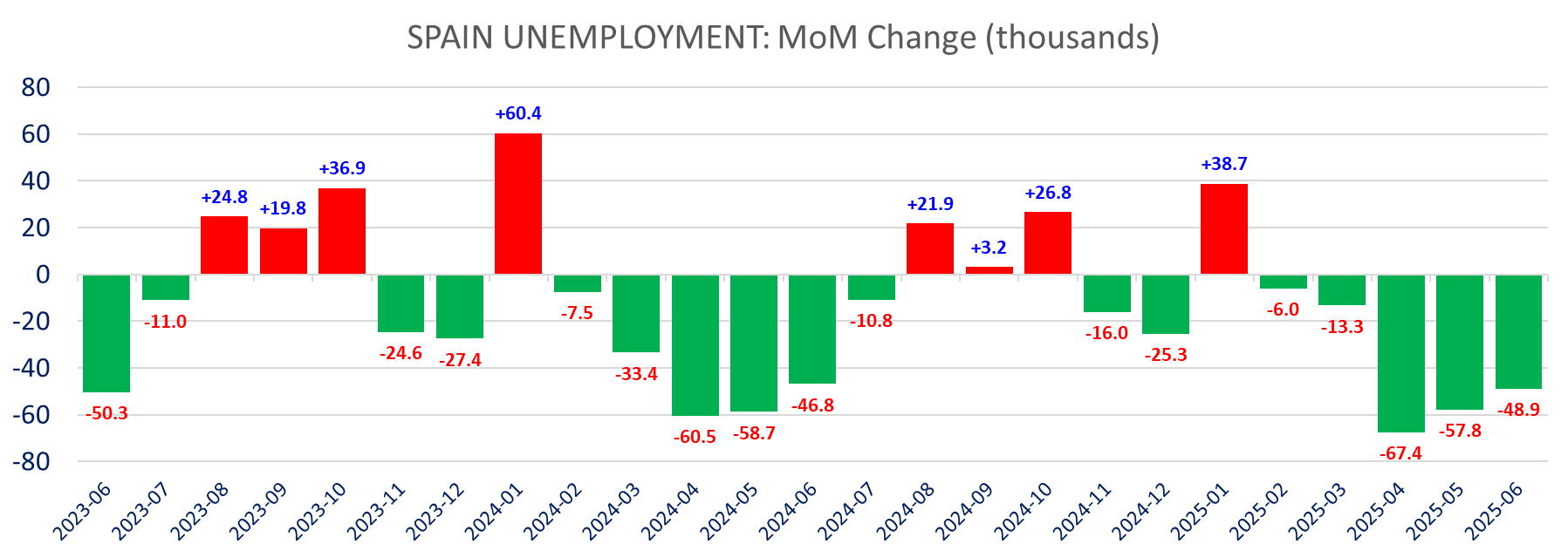

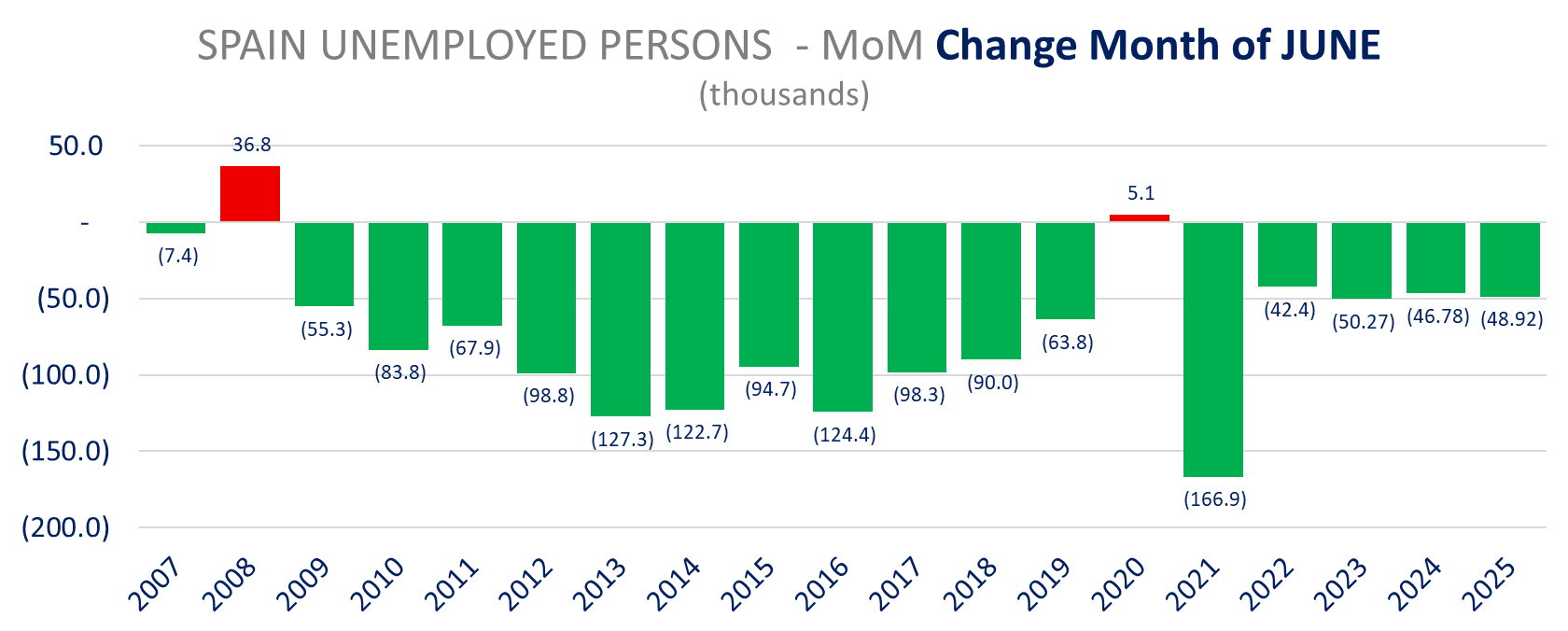

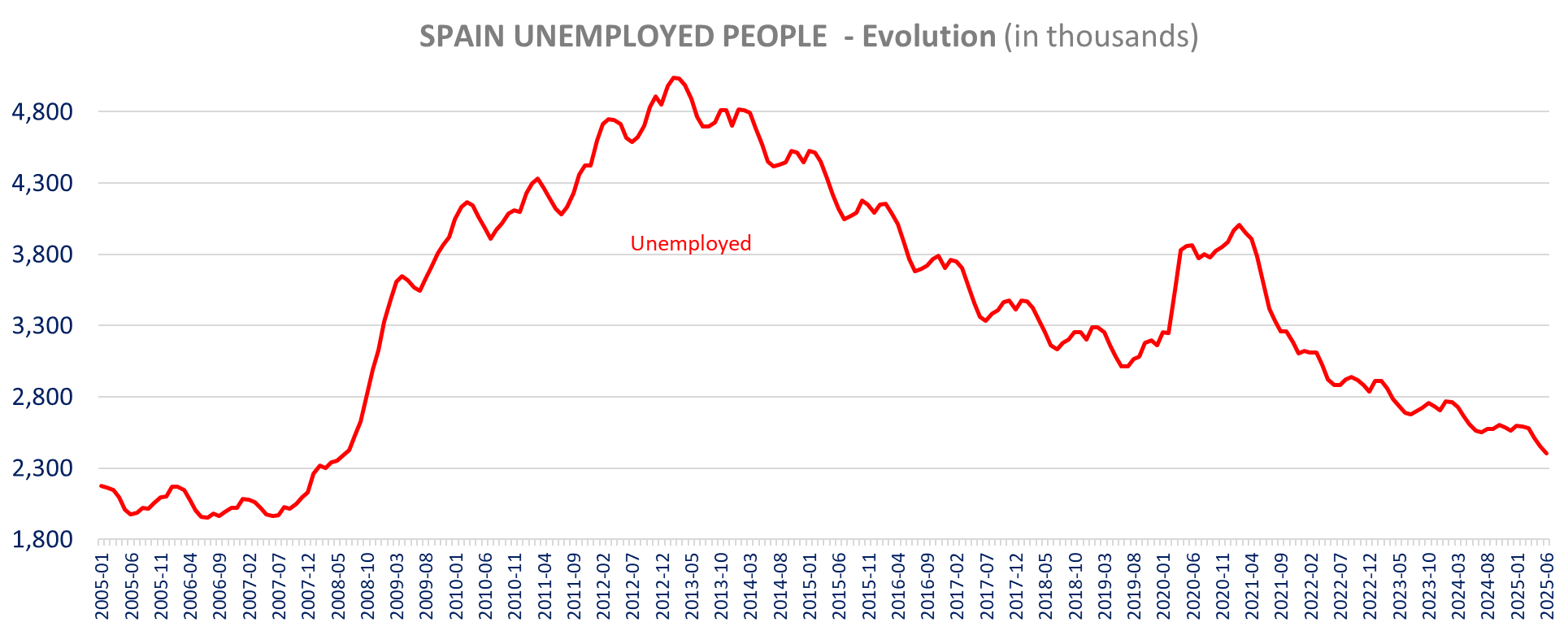

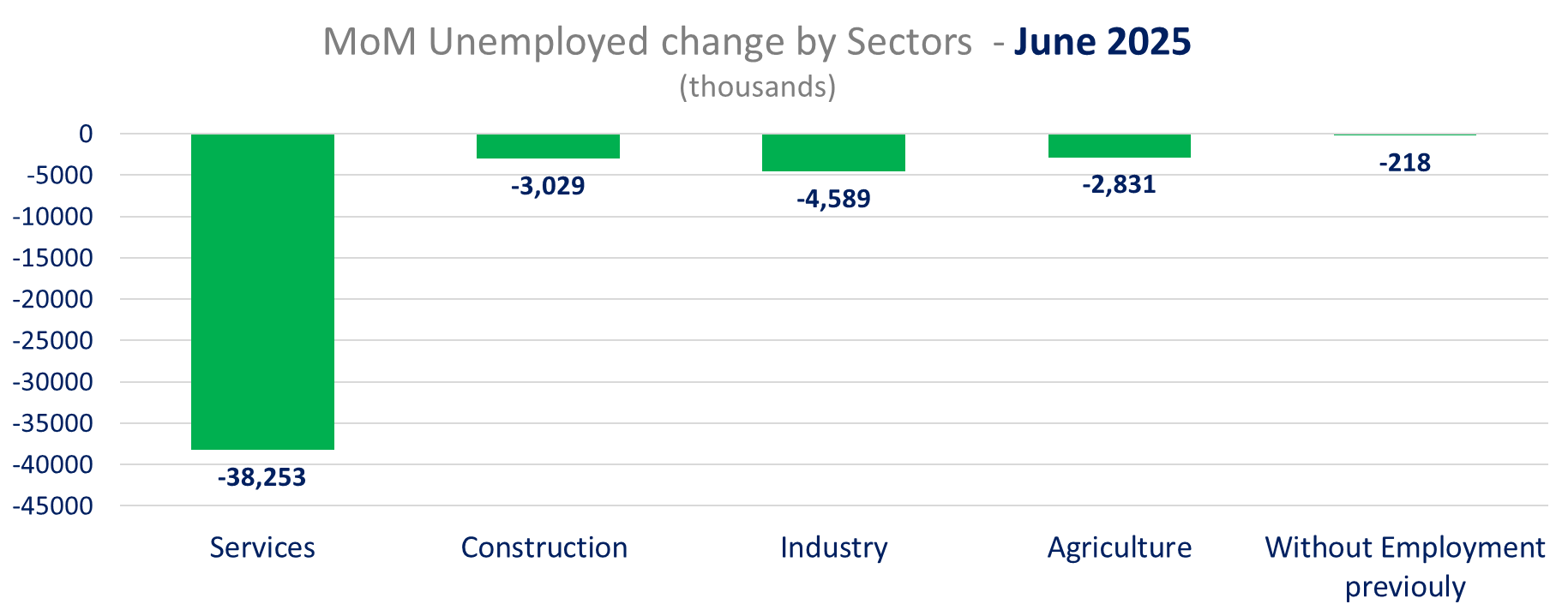

The latest Unemployment data in Spain, shows another decrease in unemployment in June. June is down month seasonally and June 2025 decline is in line with the decline in the past 3 years for that month June (range 42.4k-50.3k). Spain unemployment falling by another -48.92km/m in June to 2,405,963, declining for the 5th month in a row and down 7 months out of the last 8. Unemployment has declined by -193.5k in the last 5 months and is down -115.1k yoy. The decline in June is once again driven by services (-38.25k) with the summer season start.

Consumer confidence, the ECB CES survey and the ESI (as well as domestic data) show resilience in employment and lower consumer unemployment fear.

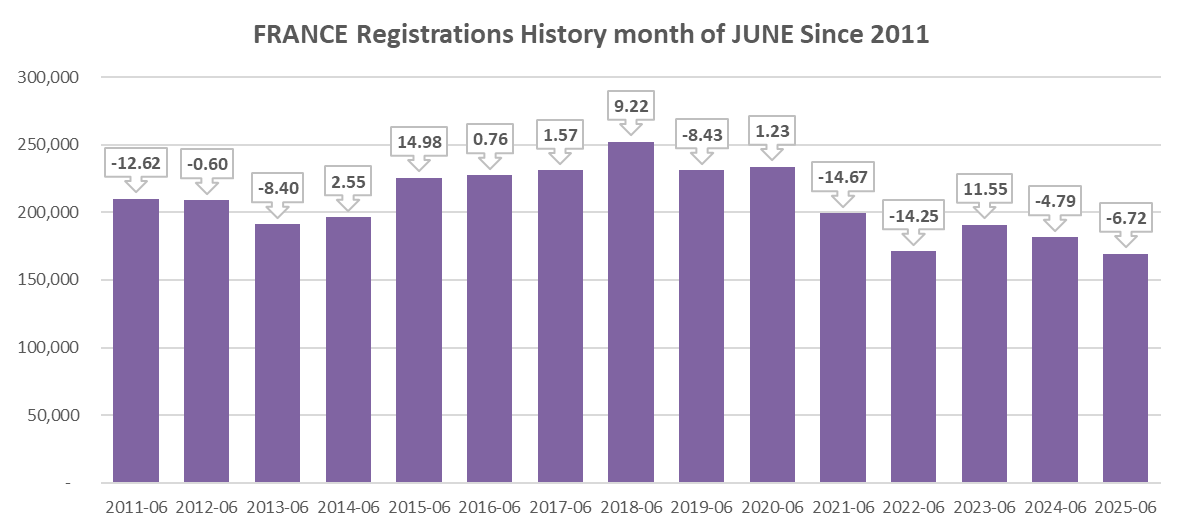

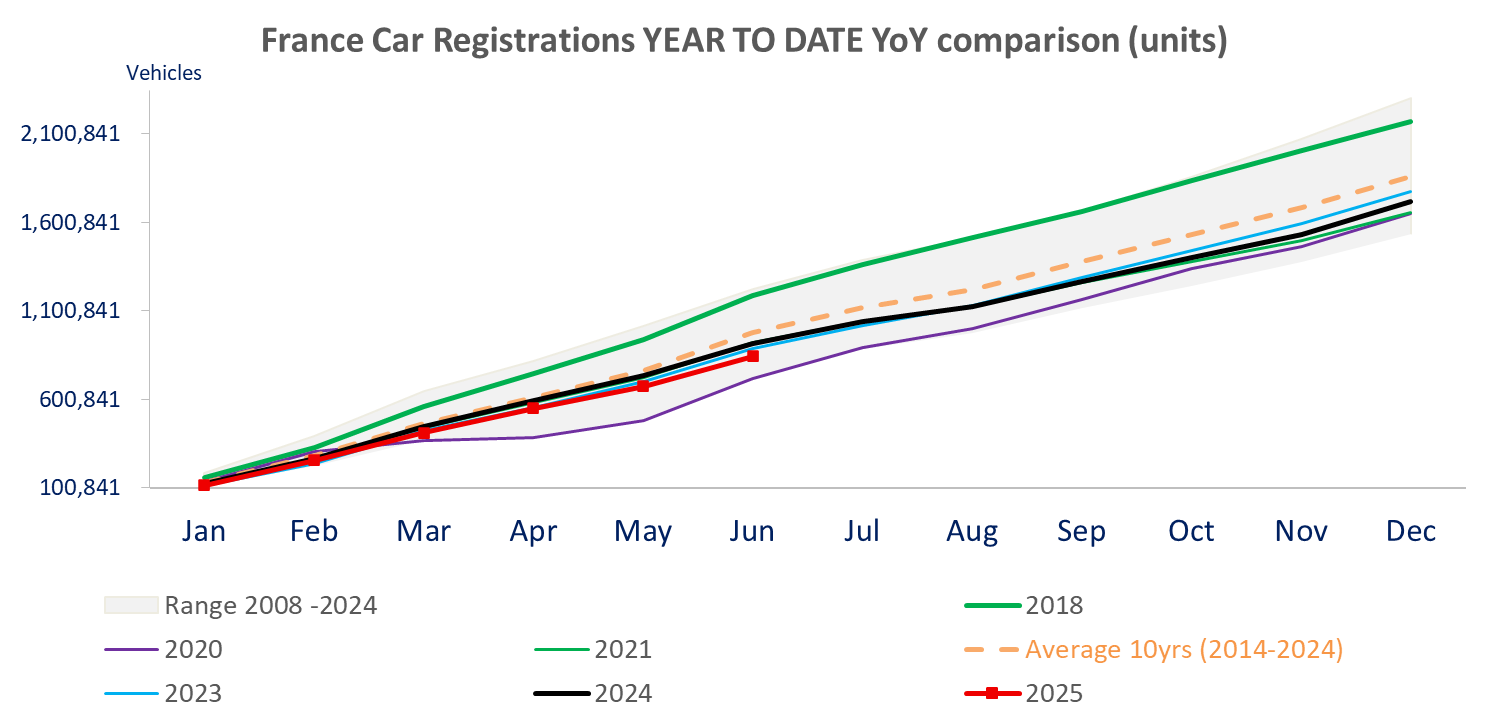

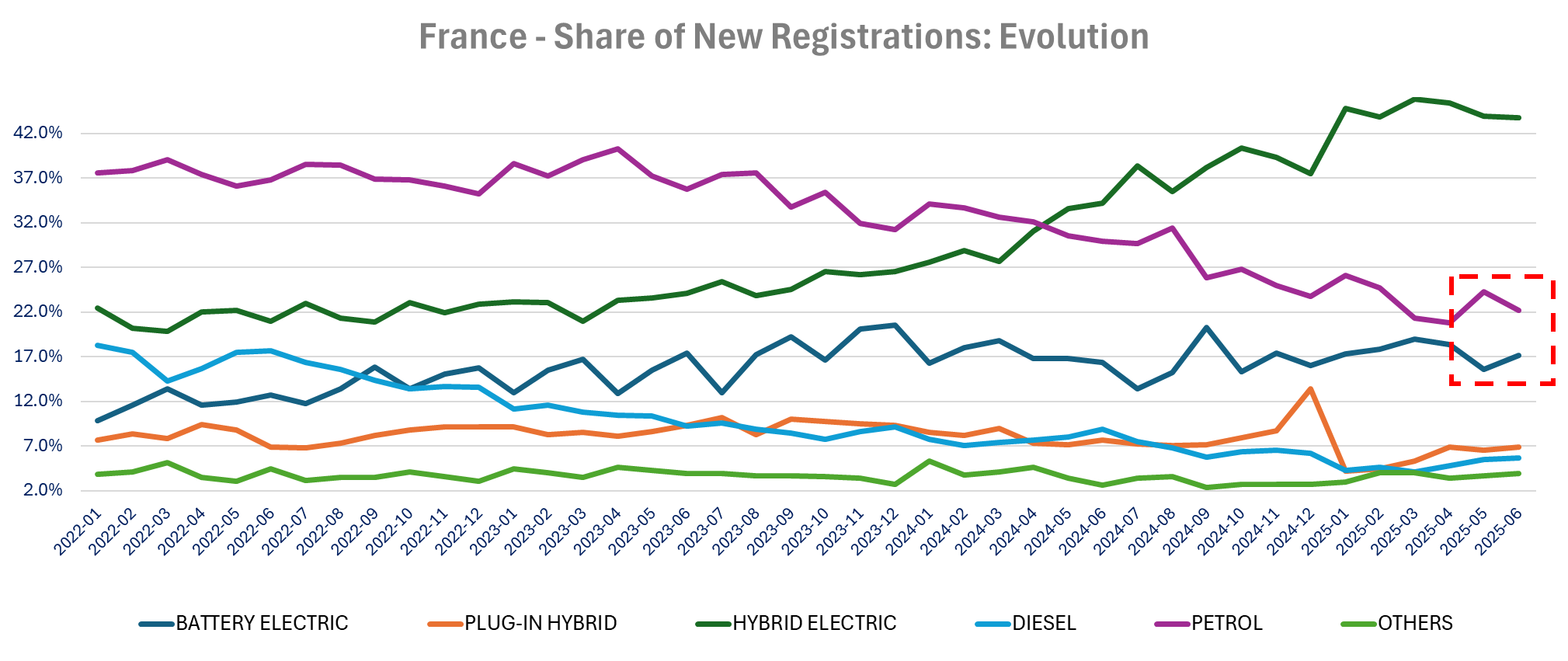

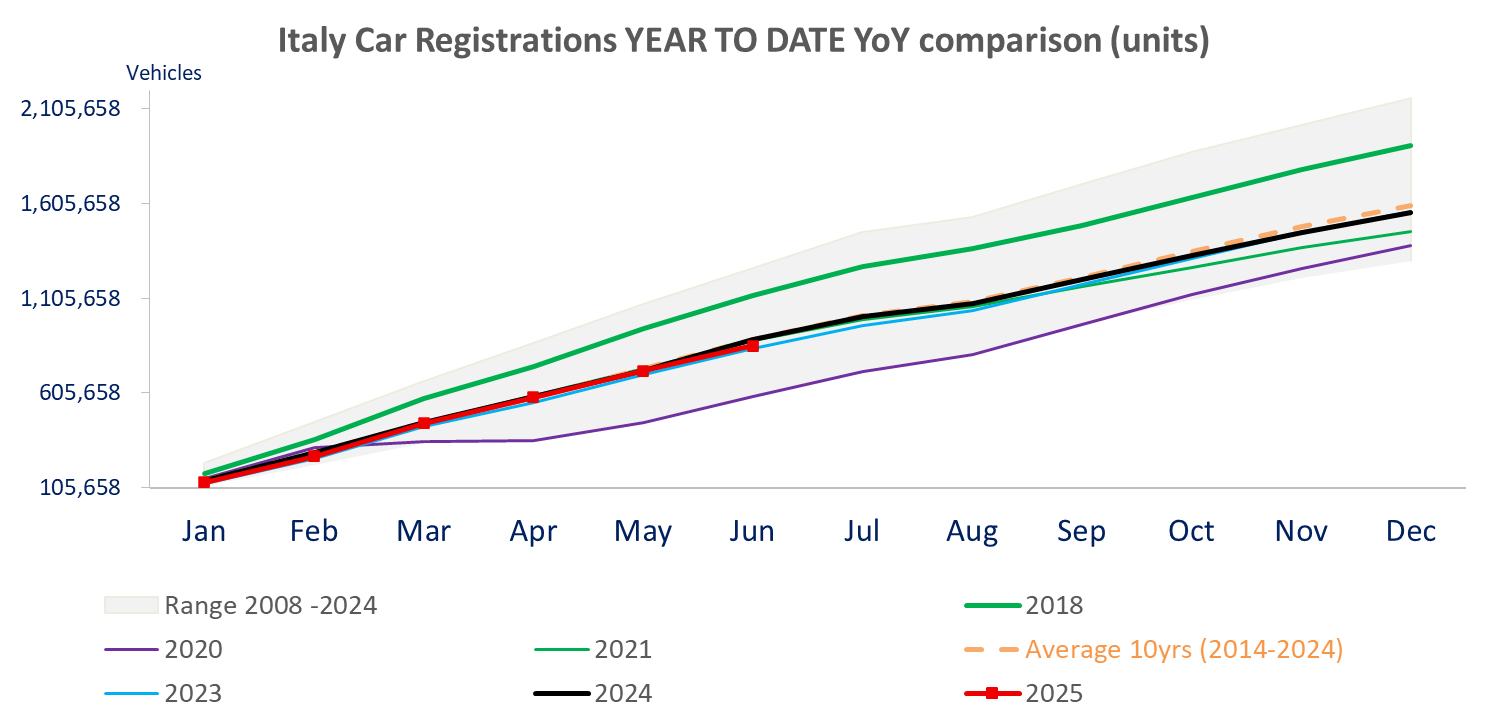

We have the first data for June car registrations, in France, Italy and Spain. Registrations continue to show a weak market in France in June with 169,504 vehicles -6.7 % yoy and -7.9% yoy the worst June since 1999. On the other hand,

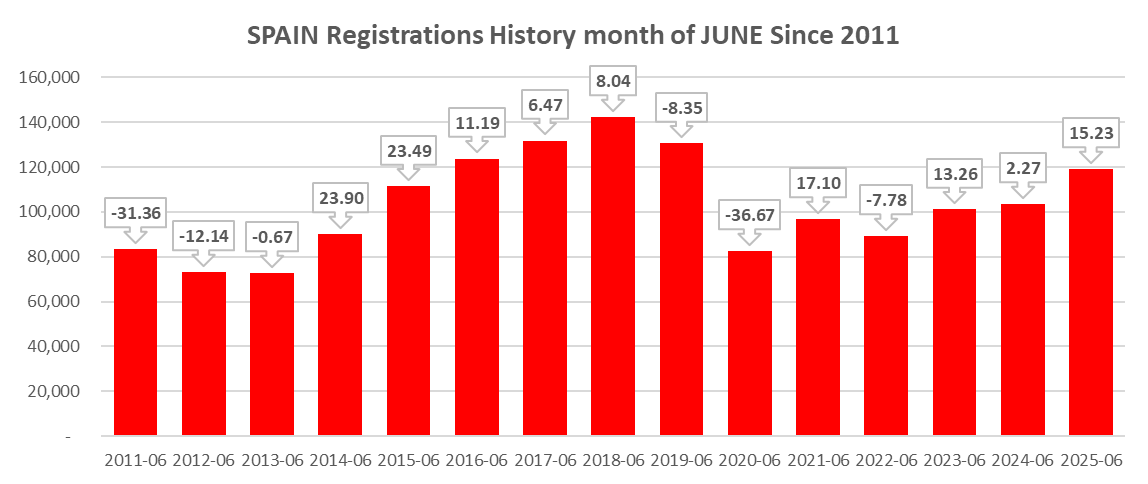

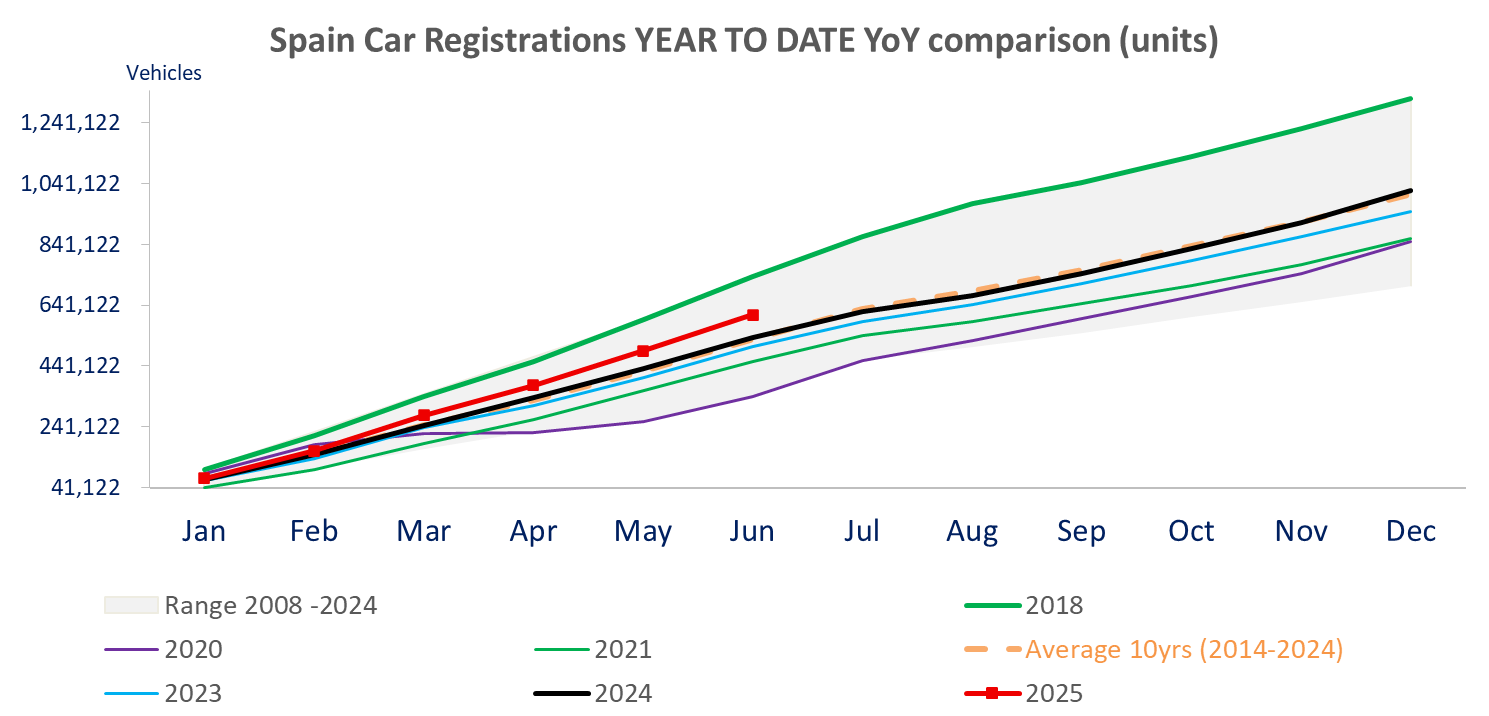

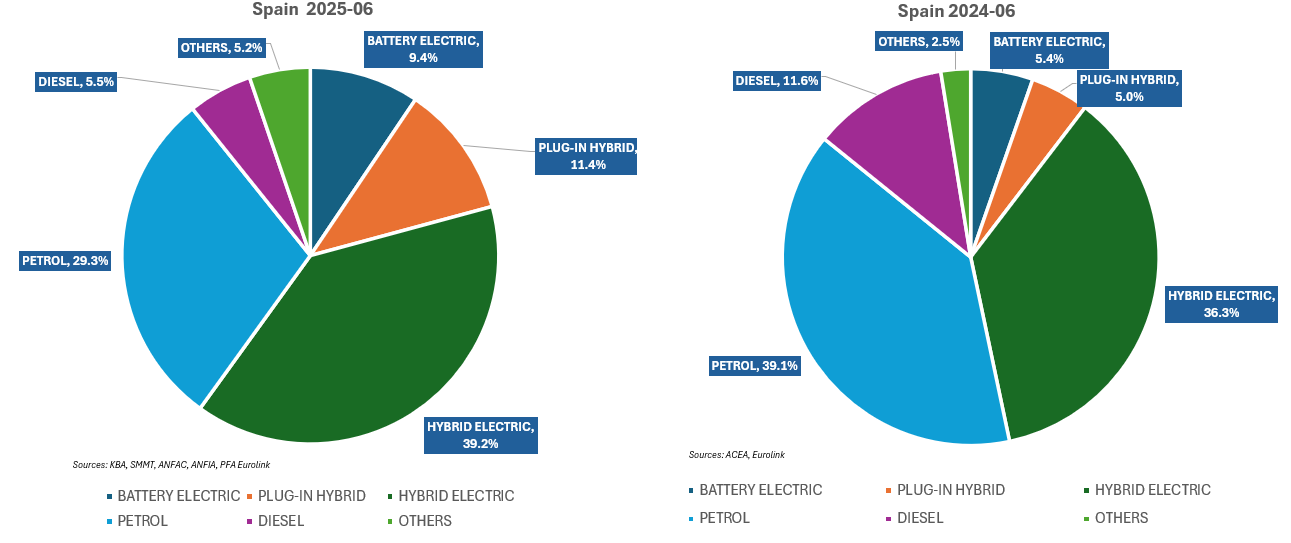

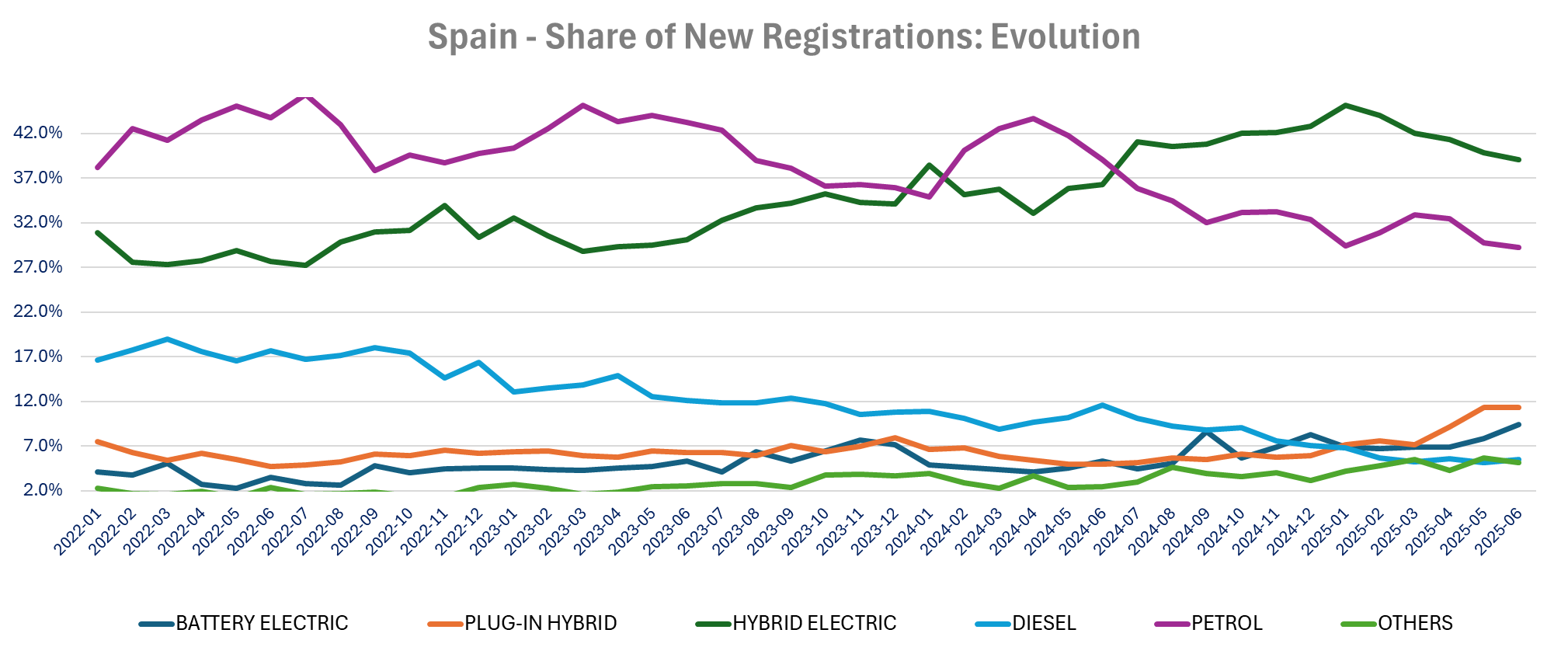

we have continuation of strong sales in Spain (incentives and post flood) with sales up 15.2% yoy and up 13.9% yoy ytd up from 13.6% yoy ytd in May. The best June since 2019.

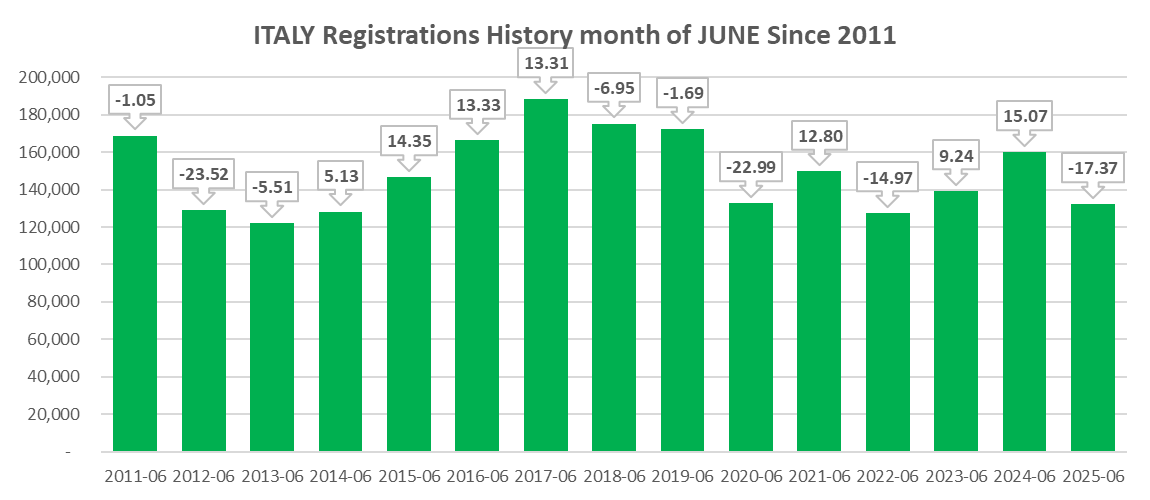

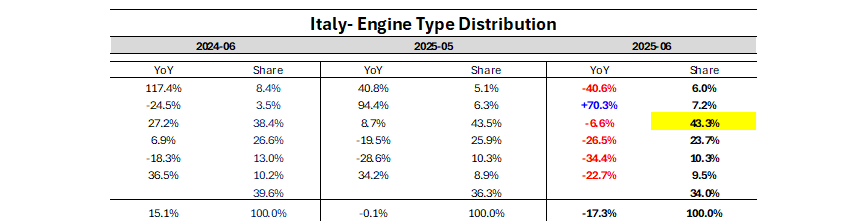

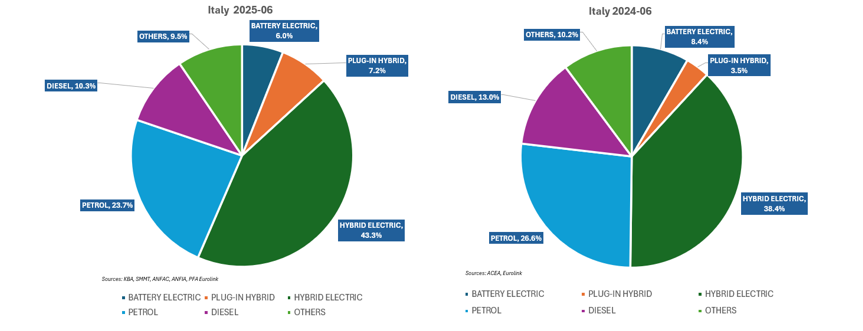

Registrations fell -17.4% yoy in Italy, but on high comparison basis, as June 2024 sales were up 15.1% yoy on incentives with Italian EV sales up 117.3% yoy in June 2024. On a year-to-date basis Italian sales are down –3.6% yoy down from -0.5% yoy in May. June 2025 is still above June 2022.

Tesla continues to underperform the EV market in Italy and Spain and did slightly better than the market in France (-0.1% vs -2.3% for the market). Details show that the Model Y outperformed the EV market, and Model 3 underperformed massively

On the companies’ front: Santander announces that it has reached an agreement to acquire 100% of TSB Banking Group plc from Banco de Sabadell, S.A., with a valuation of £2.65 billion in an all-cash transaction. The acquisition further strengthens Santander’s position in one of its core markets. Following the sale of TSB to Santander for €3.1bn, Sabadell will hold a General Shareholders’ Meeting on 6 August to approve both the sale and the payment of an extraordinary dividend of €0.50 per share. SGS announces that it has signed a definitive agreement to acquire the entire issued share capital of Applied Technical Services, a provider of specialized Testing, Inspection, Calibration and Forensics solutions in North America for an enterprise value of $1,325m corresponding to a multiple of 11.2 times 2026 EBITDA including run rate synergies. Vestas Wind Systems shares are up sharply this morning, following positive sector-wide momentum after a revised U.S. Senate bill less negative than initially feared was announced. Some of the most punitive measures—such as a proposed excise tax on wind and solar projects using foreign components—were removed at the last minute. Greggs says that LFL sales in June were impacted as very high temperatures affected the UK, increasing demand for cold drinks but reducing the overall footfall. Whilst acknowledging that comparative LFL sales are less demanding in the second half of the year, in light of the current trading conditions the Board now anticipates that the full year operating profit could be modestly below that achieved in 2024More details on equities here

Warning from the UK: 10yr Gilt yield up 17bp.

Beware of the OBBB…

According to the release of PFA (France), ANFAC (Spain) and ANFIA (Italy), Tesla continues to underperform the EV market in Italy and Spain and did slightly better than the market in France (-0.1% vs -2.3% for the market).

Details show that the Model Y outperformed the EV market, and Model 3 underperformed massively. For example, in France the Model Y is up 49.9% year-over-year and the Model 3 -77.7% (only 406 cars in June)

In Spain, the Model Y is up 127.2% yoy (only 1,179 vehicles though) and the Model 3 up 31.1% (1451 vehicles) versus an EV market up 103%,

The Italian market is skewed with a sharp increase in June 2024 due to incentives (EV market was up 117%.3 yoy in June 2024 and now down -40.6% yoy in June 2025). Tesla I still down -66% yoy, underperforming.

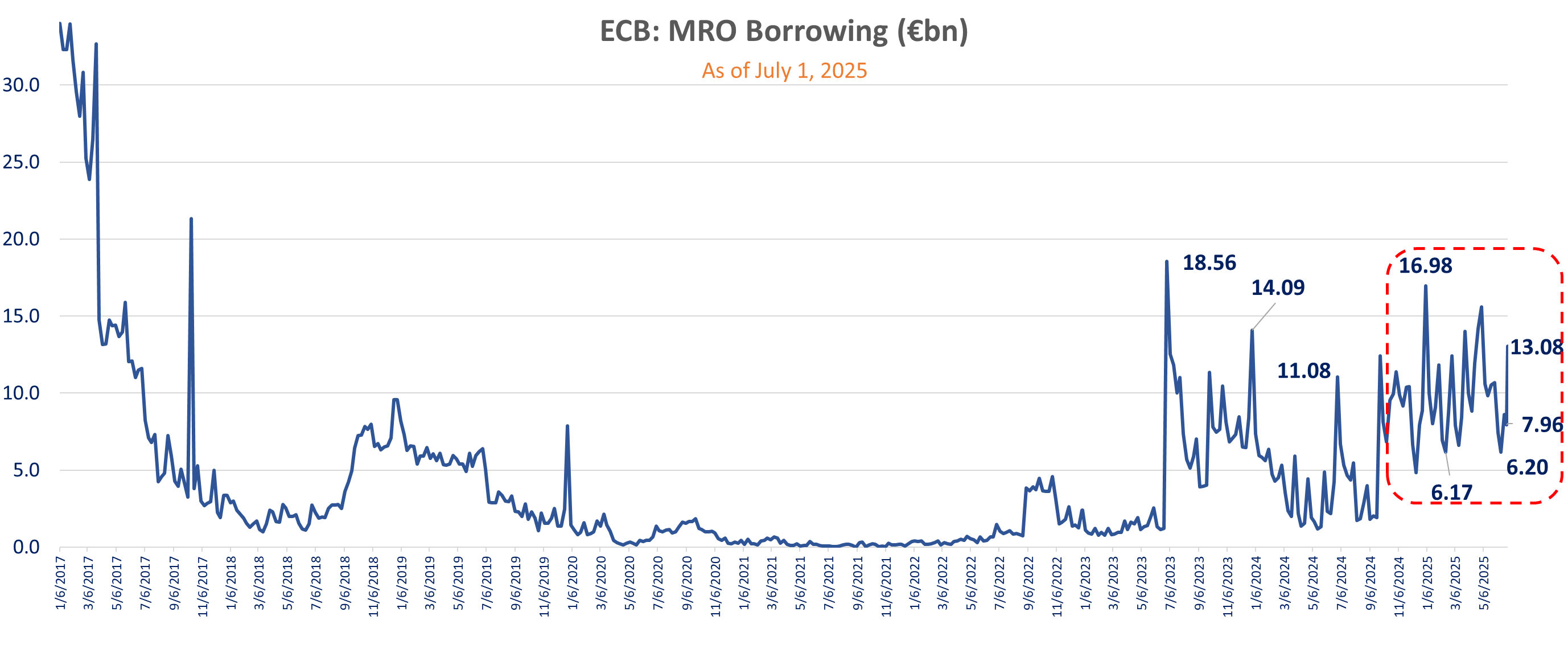

The ECB Balance sheet’s total assets declined by -€9.4bn week over week as of Friday June 27. The decline is the result of -12.65bn in securities held for monetary policy purposes partially compensated for by the increase in loans to bank we flagged last week of €3.38bn. ECB consolidated financial statement

Last week’s open market operations showed an increase in MRO borrowing of +€4.447bn to €13.075bn and a slight decrease (-€0.839bn) in 3-month LTRO borrowing during the monthly rollover. The March LTRO matured on 06/25/2025 with a total €7.23bn due and was replaced by €6.39bn 3month LTRO ending January 10, 2026.

This current week, the MRO borrowing declined to 7.96bn (down -€5.12bn w/w) as reported by the open market operations (OMO)

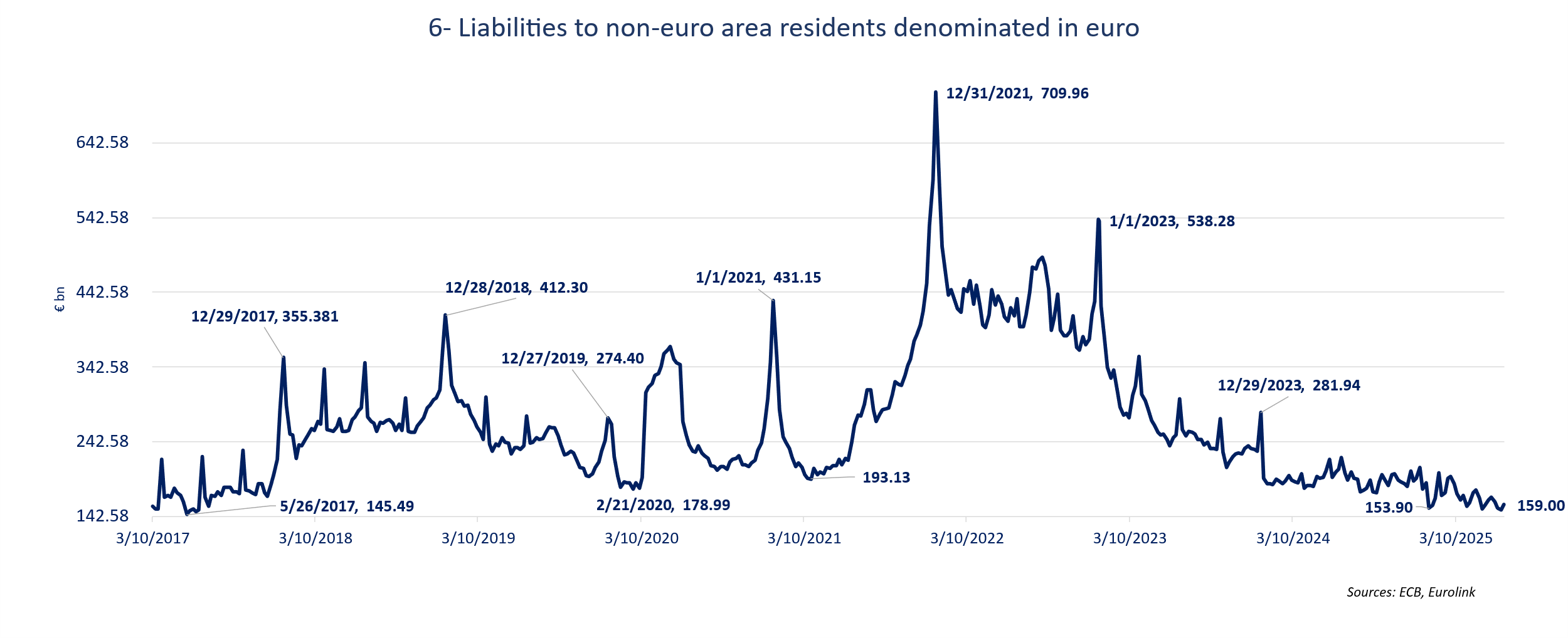

Excess liquidity fell by more than that, down -€37.16bn w/w as the liabilities side shows a larger increase in the General Government Account, up +€23.92 bn w/w to €127.37bn (Highest level since February 28) and a +€7.8bn increase in liabilities in € to non-euro area resident (item 6 on the liabilities side) to a still low level of €159bn.

Base money declined by -€34.8bn (+€2.21bn in banknotes in circulation)

Another strong month for Spain, with unemployment falling by another -48.92k m/m in June to 2,405,963, declining for the 5th month in a row and down 7 months out of the last 8. Unemployment has declined by -193.5k in the last 5 months and is down -115.1k yoy.

The fall in June is once again driven by services (-38.25k) but it fell in the other sectors as well (-3,029 in construction and -4,589 in manufacturing)

June sees declines seasonally with the summer season. June 2023 in in line with the last 3 months of June (range 42.4k-50.3k). Labor Ministry Release

The Eurozone unemployment increased by 54k m/m in May, pushing the unemployment rate up to 6.3% from April’s record low of 6.2%.

The sharp increase in Italian unemployment (+112.6k m/m, 6.5% rate up from 6.1%) was the main factor behind the increase. As describe in the Italian labor comments, the increase in unemployment coincides with a sharp increase in active population (+192k), record high activity rate and employment rate (notably older population).

The number of unemployed decreased in France, Greece, Finland, Austria and Spain. Besides for Italy, the unemployment rate is up in Belgium (6.5% vs 6.4%), Lithuania (6.5% vs 6.3%), Malta (2.7% vs 2.6%). It is unchanged in Germany, France, The Netherlands, Portugal, Latvia, Slovakia and Luxembourg. It is down in Spain (10.8% vs. 10.9%, Ireland (4% vs 4.1), Croatia (4.5% vs 4.6%), Slovenia (3.9% vs 4%), Greece (7.9% vs 8.3%) and Cyprus (3.6% vs 3.7%).

Unemployment declined -14k m/m for women and increased +68k m/m for men. On a year over year basis, unemployment is down -168k (was -257k in April) in the Eurozone (-166k for women and -3k for men!)

The unemployment rate increased to 6.5% from 6.1% while economists expected an improvement to 6%, but it rose amid stronger activity rate and employment rate, both reaching new record high. Employment increased exclusively for the older population (50+)

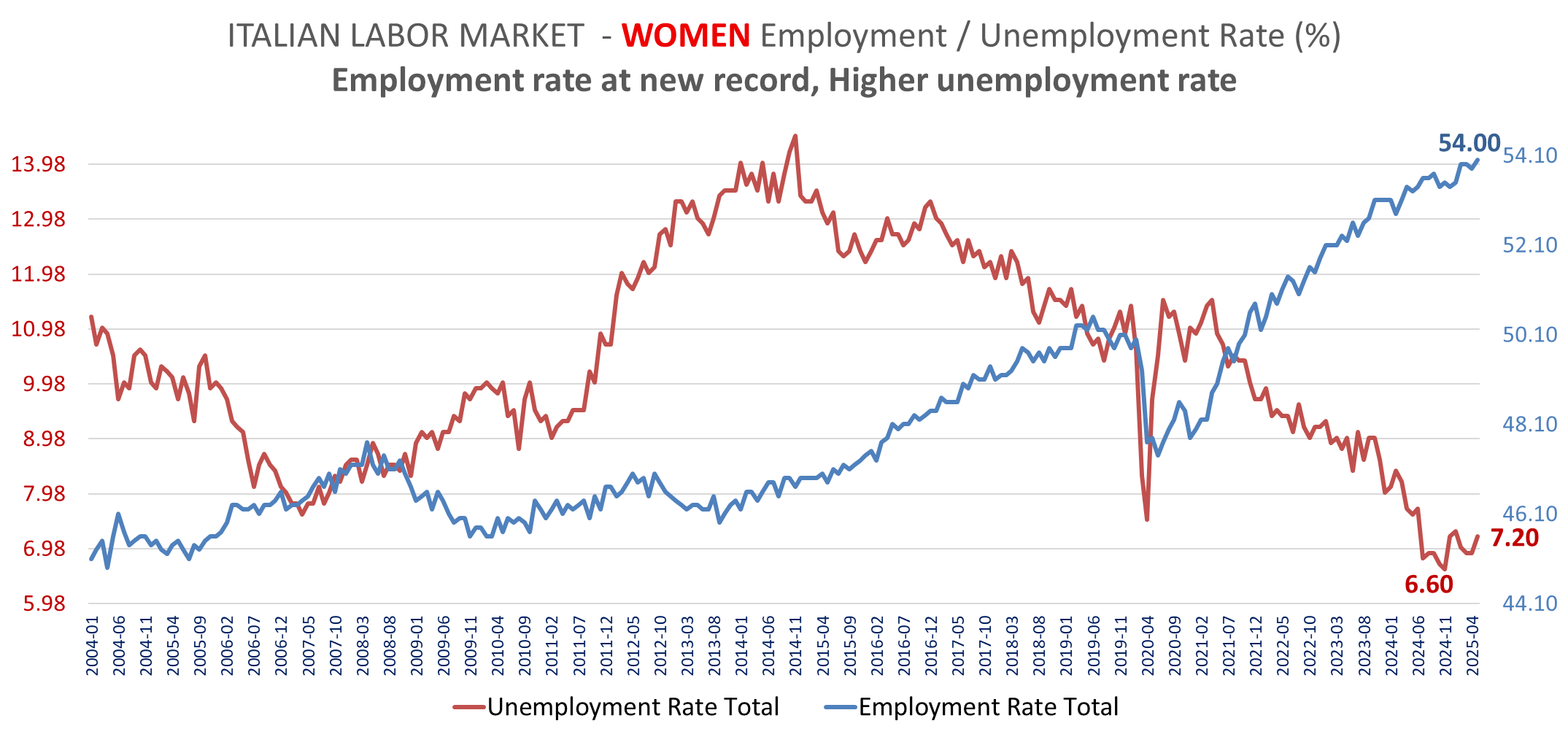

The unemployment rate increased to 6% from 5.5% for men and to 7.2% from 6.9% for women. Unemployment increased by 112.6k m/m (79.3k for men, 33.3k for women) but active persons increased by 192.6k (112.9 for men, 79.7 for women). Employment increased by 80k (33.6k for men and 46.4k for women).

The inactivity rate declined to 32.6% from 33% and the activity rate increased to 67.4% from 67%, a new record. The employment rate reached a new record at 62.9%, back to the January high for men at 71.8% but at a new high for women of 54% (53.9% in February- March was the previous record)

Employment increased the 50+ (124k) out of which +106.4k for the 50-64 age group but declined for the other age brackets (-6.5k for 15-24, -29.3k for 25-34 and -8.2 for the 34-49 groups). The number of unemployed increased for all age groups, with the larger increase for the 25-34 (+42k, rate at 10.3% up from 9.5%), and the 34-49 group (+32.5k rate at 5.7% up from 5.4%). The unemployment rate surged to 21.6% from 19.9% for the 15-24 age group with +27.7 unemployed m/m. The unemployment rate increased marginally for the 50+ (3.5% vs 3.4%, +10.2k)

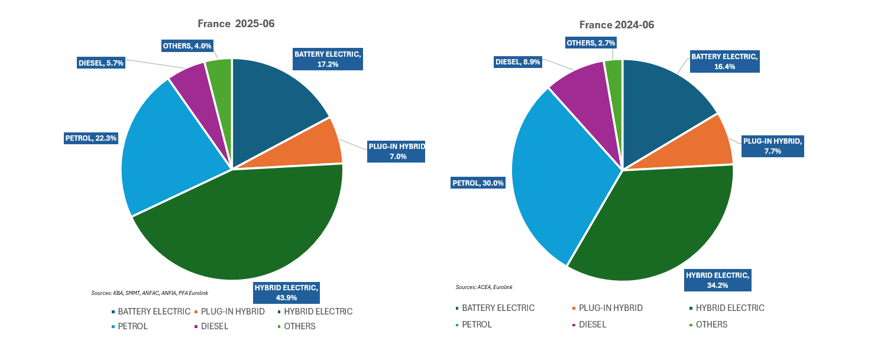

The first batch of European registrations continues to show weak market in France in June (169,504 vehicles -6.7 % yoy and -7.9% yoy ytd in June vs -8.2% yoy ytd in May) the worst June since 1999. PFA release

We have continuation of strong sales in Spain (incentives and post flood) with sales up 15.2% yoy and up 13.9% yoy ytd up from 13.6% yoy ytd in May. The best June since 2019. ANFAC Release, ANFAC electric

Registrations fell -17.4% yoy in Italy, but on the back of high comparison basis, as June 2024 sales were up 15.1% yoy on incentives with Italian EV sales up 117.3% yoy in June 2024. On a year-to-date basis Italian sales are down –3.6% yoy down from -0.5% yoy in May. June 2025 is still above June 2022. ANFIA Release

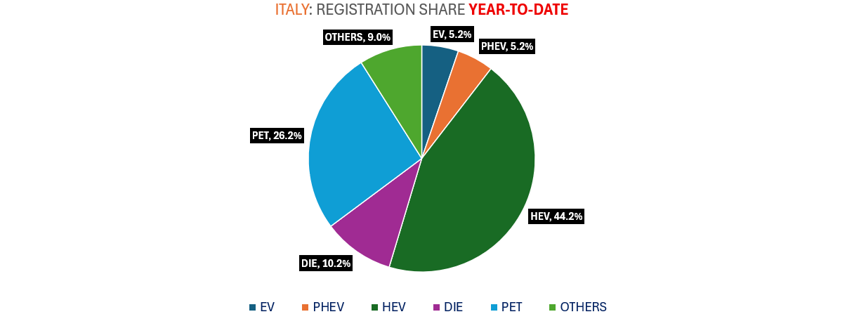

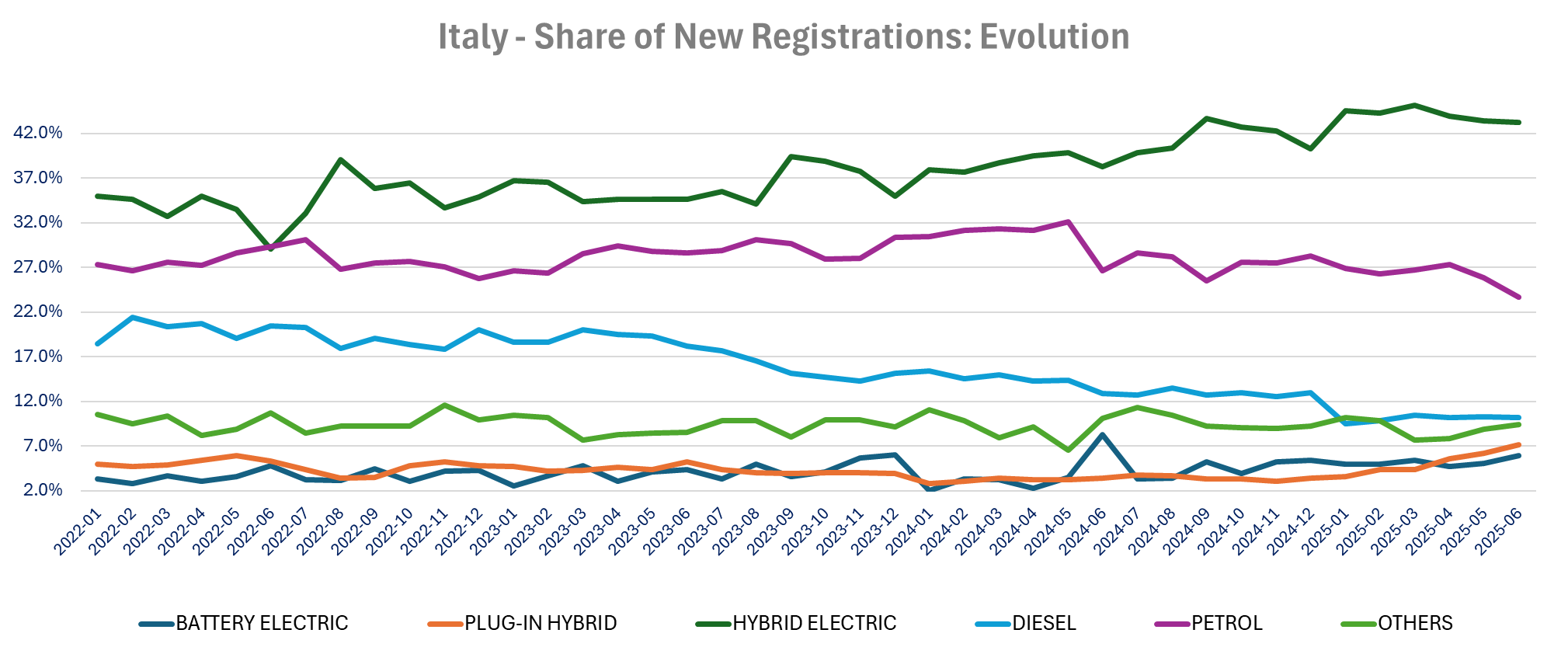

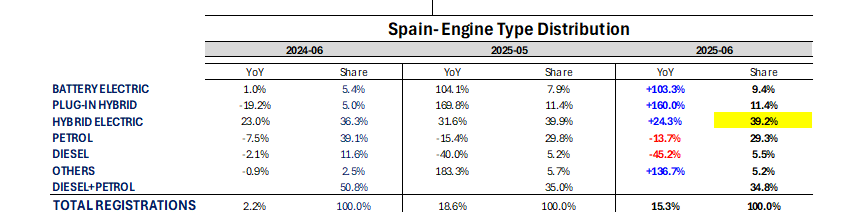

EV Sales down -40.6% yoy in Italy (due to high comps) but still up 27.9% yoy year to date. In Spain EV sales are up 84% ytd and Plug-in up 82.4%, HEV +32.8%.

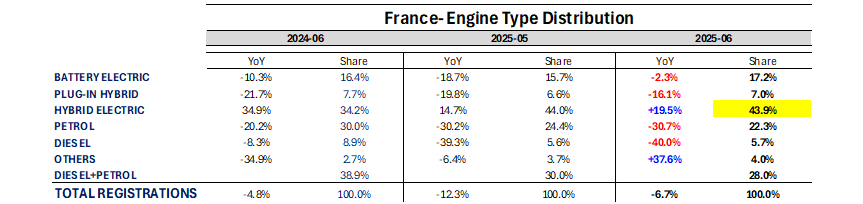

In France EV are down -2.3% (i.e. better than market gaining 0.8pt in share yoy) and HEV are up+19.5% yoy in June. Year to date, France EV sales are down -6.2% yoy, HEV +34.1% but plug-in are down -33.3%

.

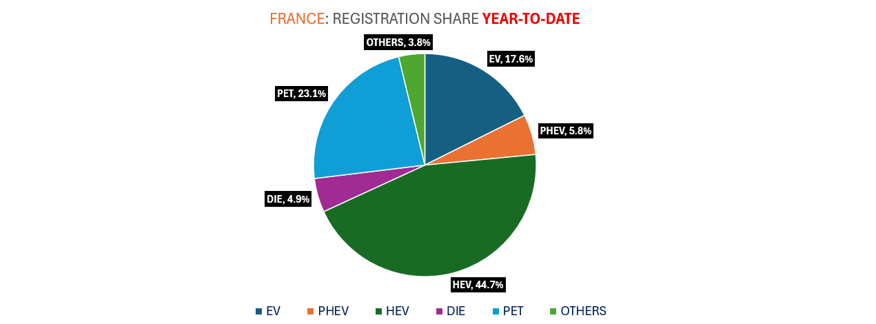

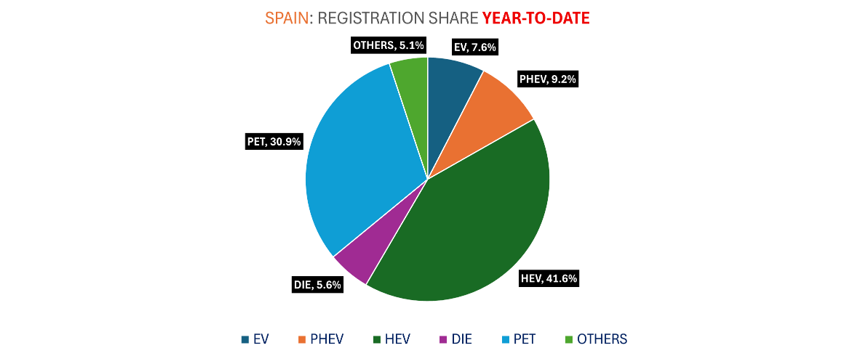

Diesel and Gasoline engine continue to decline. Year to date, Diesel share is down to 4.9% in France, 5.8% in Spain and 9% in Italy. For gasoline, Ytd share is down to 23.1% in France (22.3% in June), 26.2% in Italy (23.7% in June), 30.9%in Spain (29.3% in June). Year over year, in the first 6 months of the year, Diesel and Petrol engines combined lost -14.4 points in share of registrations in Spain, -11.9 points in France and -8.5 points in Italy.

Year-to-date HEV gained 14ppt share in France, 5.9 points in Spain and 5.5 points in Italy.

Tesla improved slightly still underperforming the EV market in Spain and Italy, thanks to better performance of the Model Y. (see comments above)

FRANCE, ITALY, SPAIN

|

|

Wednesday, July 2, 2025 | ||

|

VWS | |||

|

DKK |

104.65 |

+9.58% | |

|

VWS |

Vestas Wind Systems shares are up sharply this morning, following positive sector-wide momentum after a revised U.S. Senate bill less negative than initially feared was announced. Some of the most punitive measures—such as a proposed excise tax on wind and solar projects using foreign components—were removed at the last minute. Additionally, Vestas announced its largest-ever order for its V172-7.2 MW turbines—a 115 MW order in Germany from ENERTRAG. | ||

|

|

|

|

|

|

SAB | |||

|

EUR |

2.84 |

+5.26% | |

|

SAB |

Following the sale of TSB to Santander for €3.1bn, Sabadell will hold a General Shareholders’ Meeting on 6 August to approve both the sale and the payment of an extraordinary dividend of €0.50 per share. | ||

|

|

|

|

|

|

VOLCAR B |

Volvo Car AB | ||

|

SEK |

18.21 |

+5.05% | |

|

VOLCAR B |

Volvo Cars reported global sales of 62,858 cars in June, down 12 per cent compared to the same period last year. The total sales for the period of January through June amounted to 353,780 cars globally, a decrease of 9 per cent compared to the same period 2024. | ||

|

|

|

|

|

|

SAN | |||

|

EUR |

7.18 |

+3.12% | |

|

SAN |

Santander announces that it has reached an agreement to acquire 100% of TSB Banking Group plc from Banco de Sabadell, S.A., with a valuation of £2.65 billion (approximately €3.1bn) in an all-cash transaction. The acquisition further strengthens Santander’s position in one of its core markets, expanding its customer base and lending capacity across the UK. Santander UK would become the third largest bank in the country by personal current account balances and number four in mortgages. The transaction is expected to generate cost synergies of 13% of the combined business’s cost base, equivalent to at least £400million pre-tax. To deliver these synergies, Santander expects to incur £520 million of pre-tax restructuring costs during 2026 and 2027. | ||

|

|

|

|

|

|

SGSN | |||

|

CHF |

82.76 |

+2.65% | |

|

SGSN |

SGS, announces that it has signed a definitive agreement to acquire the entire issued share capital of Applied Technical Services, a provider of specialized Testing, Inspection, Calibration and Forensics solutions in North America for an enterprise value of $1,325m corresponding to a multiple of 11.2 times 2026 EBITDA including run rate synergies. ATS is expected to bring $460 million of sales and $95 million of EBITDA before synergies in 2026. | ||

|

|

|

|

|

|

GRG | |||

|

GBp |

1700.00 |

-13.92% | |

|

GRG |

Greggs says that LFL sales in June were impacted as very high temperatures affected the UK, increasing demand for cold drinks but reducing the overall footfall. Whilst acknowledging that comparative LFL sales are less demanding in the second half of the year, in light of the current trading conditions the Board now anticipates that the full year operating profit could be modestly below that achieved in 2024. Greggs’ previous guidance for 2025 was for operating profit to be at least in line with, or slightly above, the £195.3 million achieved in 2024. | ||

Versus early hours:

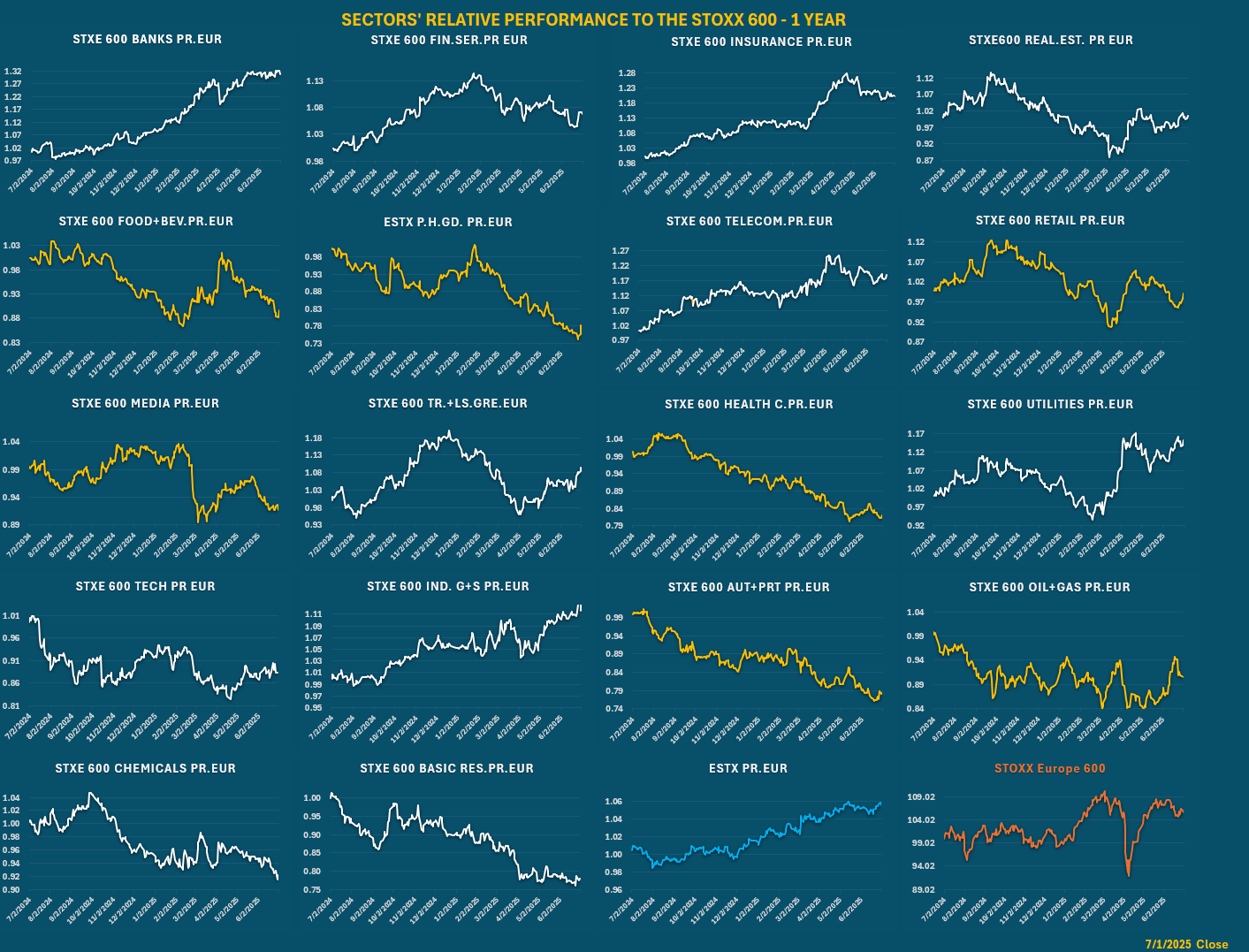

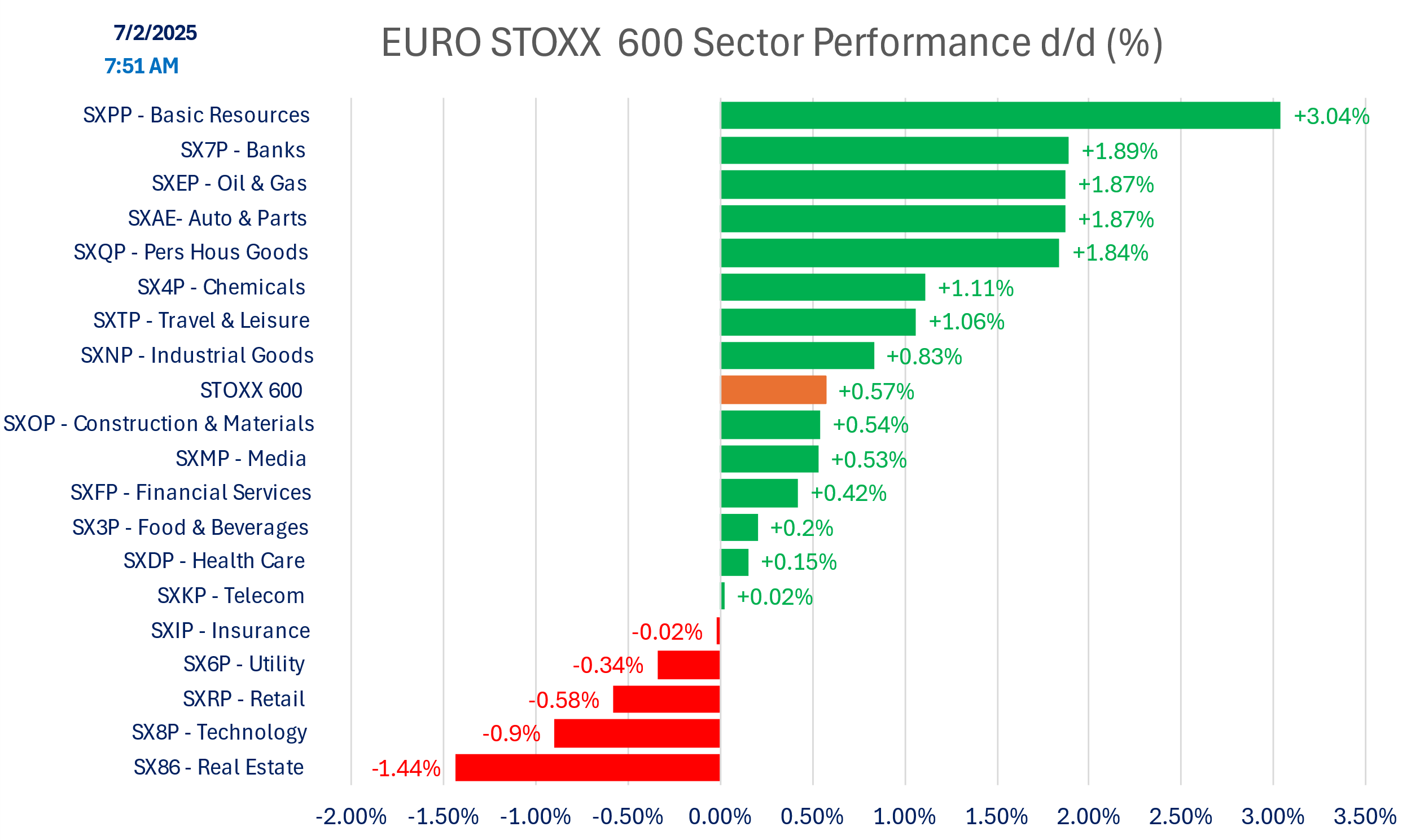

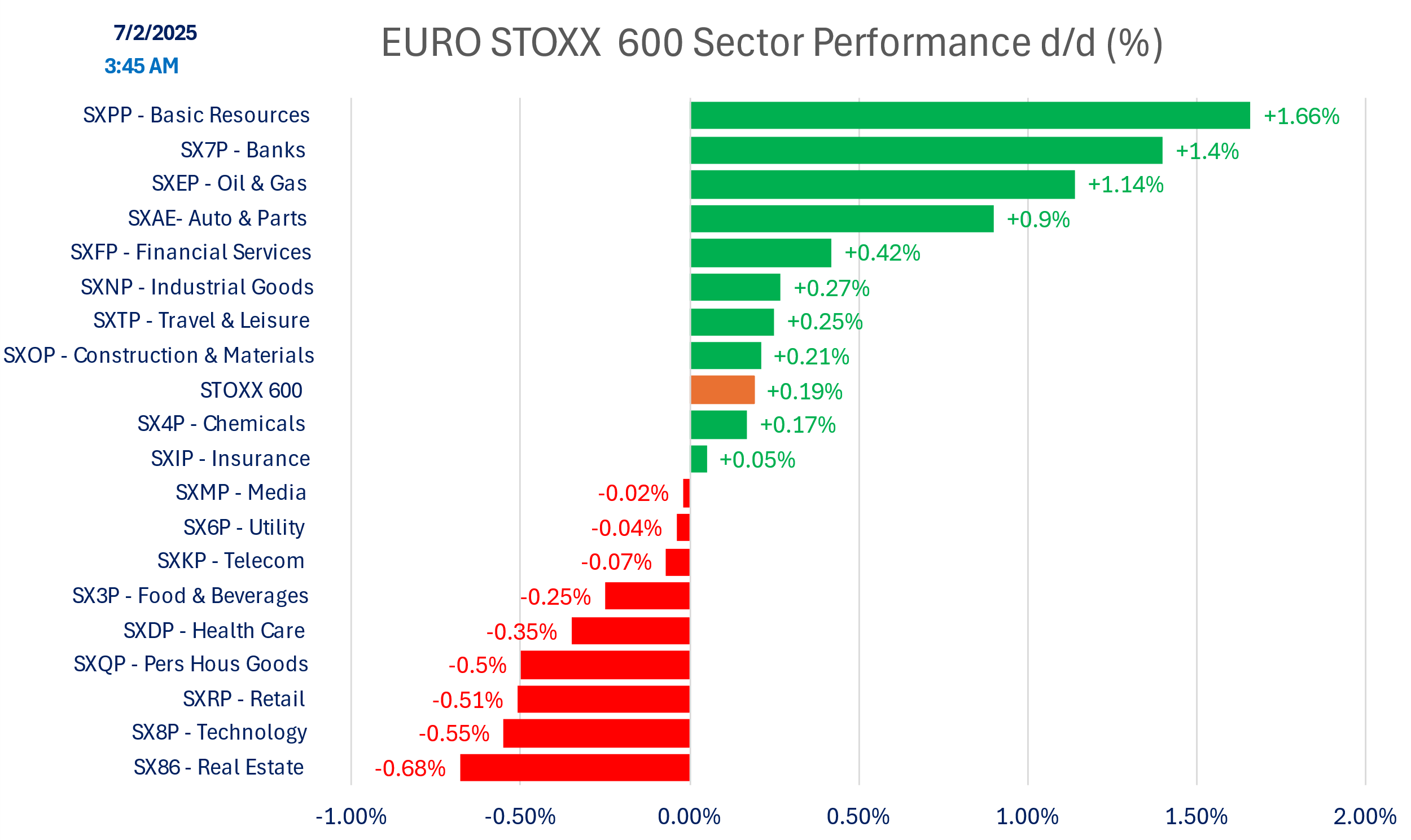

SECTOR PERFORMANCE

Relative performance to STOXX 600

Today’s Performance

Versus early hours:

Indices

Versus early hours

Commodities

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.