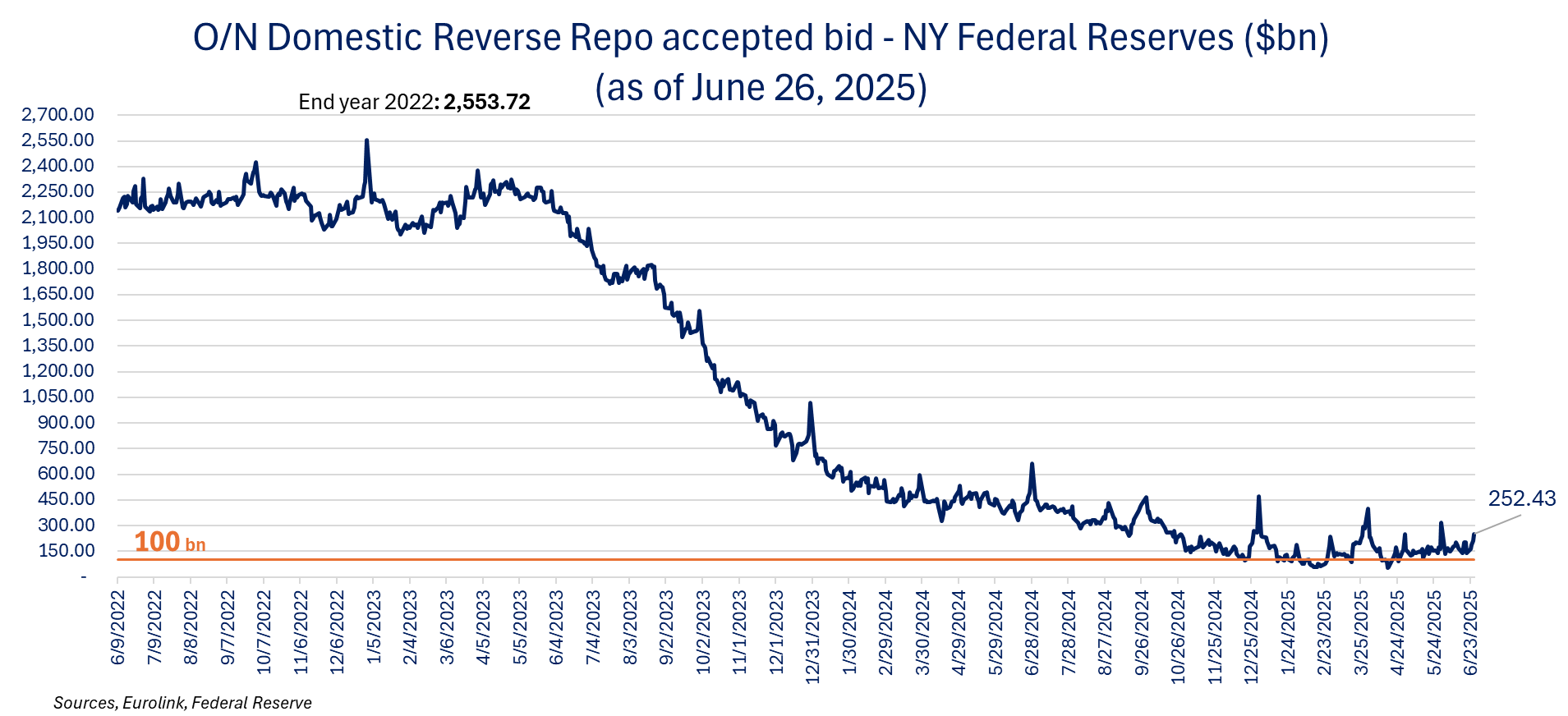

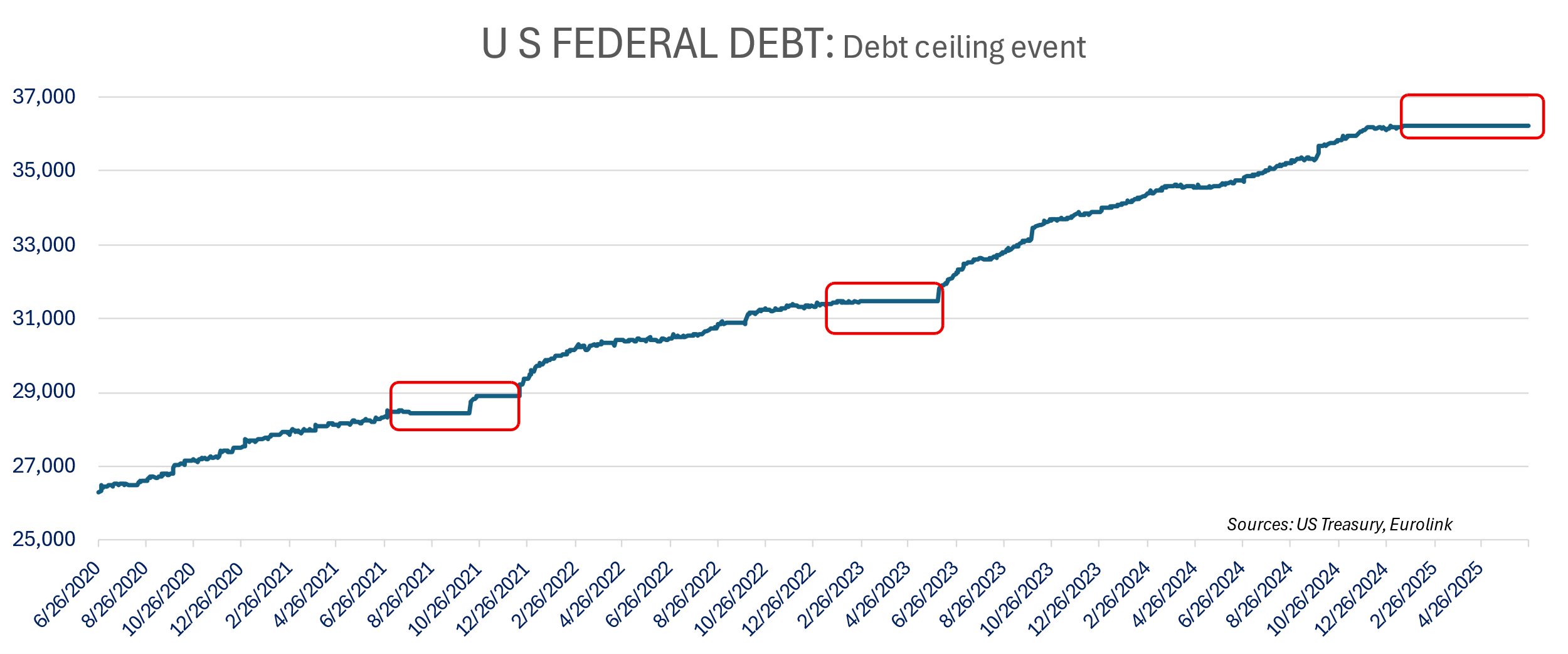

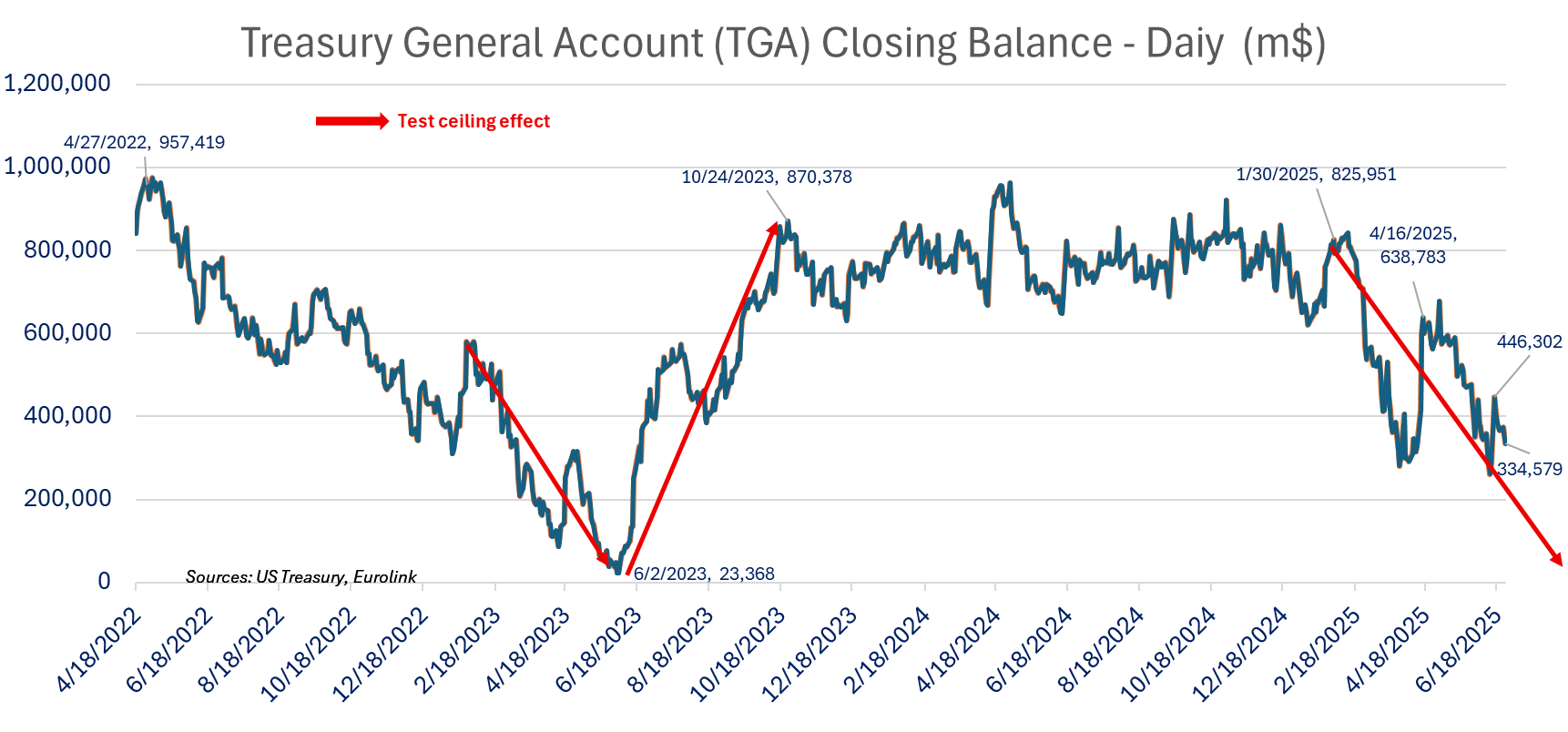

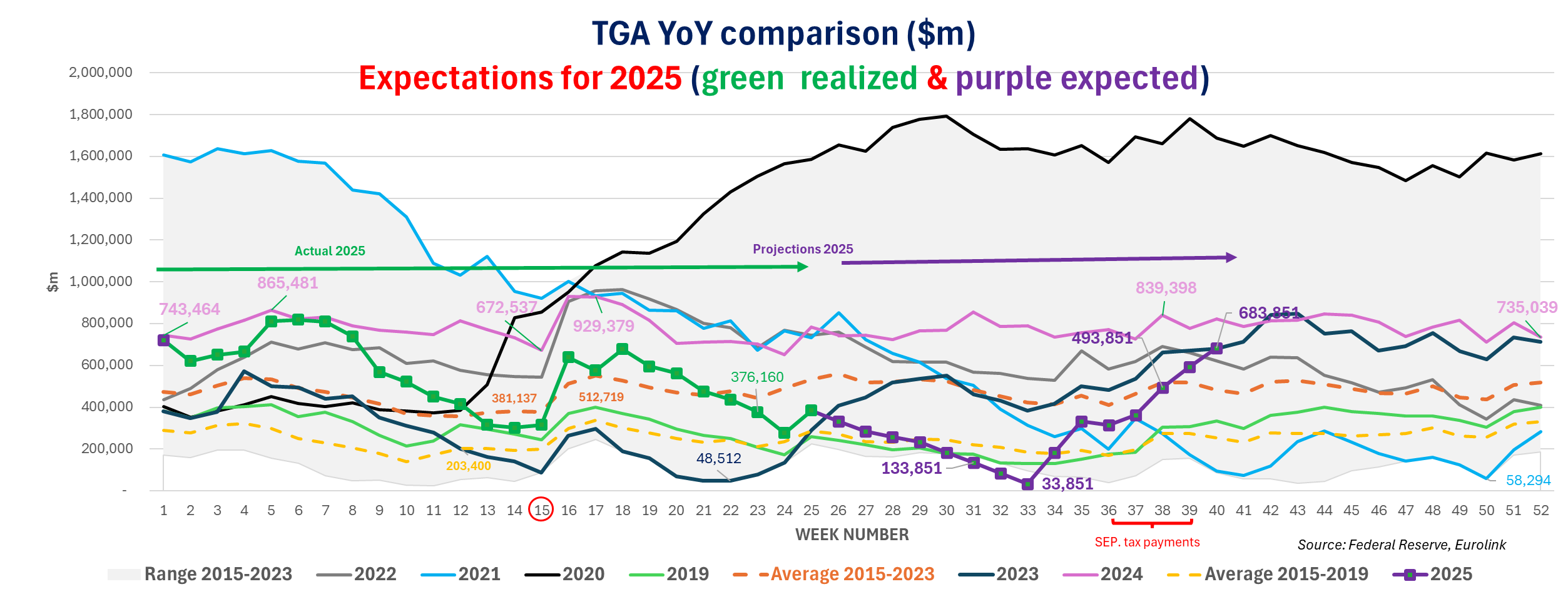

Stocks continue to move higher with hope for a smoother July 9 Tariff decision after the administration talks about ~ 10 “agreements” expected to be reached in the coming days. The framework agreement with China is signed but we still speak about the broad framework agreed in Geneva in May, refine in London this month, but not implying any new breakthrough. Uncertainty remains about the timing (and content) of the “beautiful bill passage” with as highlighted by the latest Fed balance sheet and the daily TGA and RR Data, time is of the essence as we will reach the end of the special measures by mid-August if the increase in the debt ceiling is not approved before that. The RR increases at month/quarter end, taking away some liquidity provided by the decline in the TGA. With RR exhausted we still brace for a sharp liquidity withdrawal post Debt ceiling agreement as the treasury rebuild the TGA.

The withdrawal of the “revenge tax” is a clear positive for investment in the US and bonds, along the SLR changes, but we still face larger deficits and larger issuance in the coming months. Bond yields are higher in the last session of the week and stocks close on records.

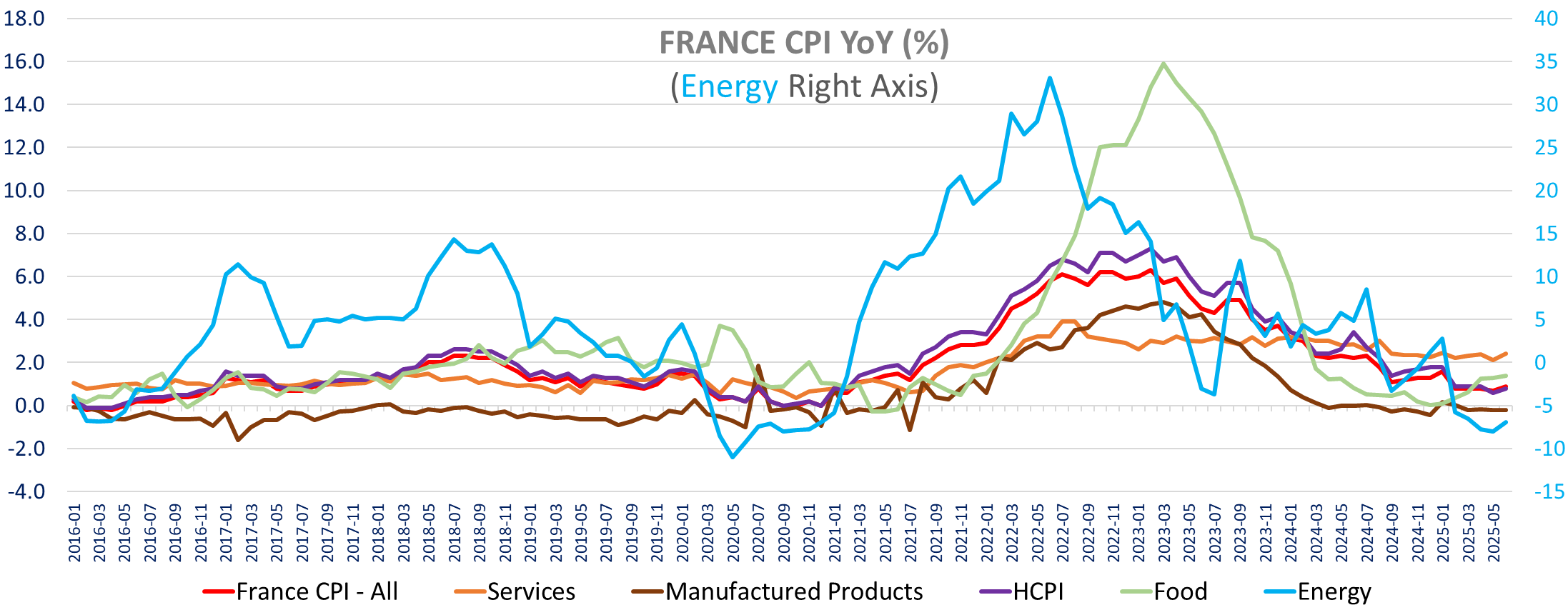

The May US PCE and core PCE are up with the later more than expectations and the first inflation data for June inflation in the Eurozone (France and Spain) also came higher than expected.

The French CPI is above expectations of 0.7% yoy at 0.9% yoy up from 0.7% yoy in May. Prices increased 0.3% m/m rather than 0.2% anticipated. The HICP is also higher than consensus forecasts at 0.8% yoy (0.4% m/m) up from 0.7% yoy in May when 0.7% yoy / 0.2% m/m was expected. The increase is partially due to higher energy inflation (-6.9% vs -8%) on higher liquid fuel prices, but higher services inflation was the main driver up to 2.4% from 2.1% with INSEE flagging higher accommodation, transport and communication services inflation.

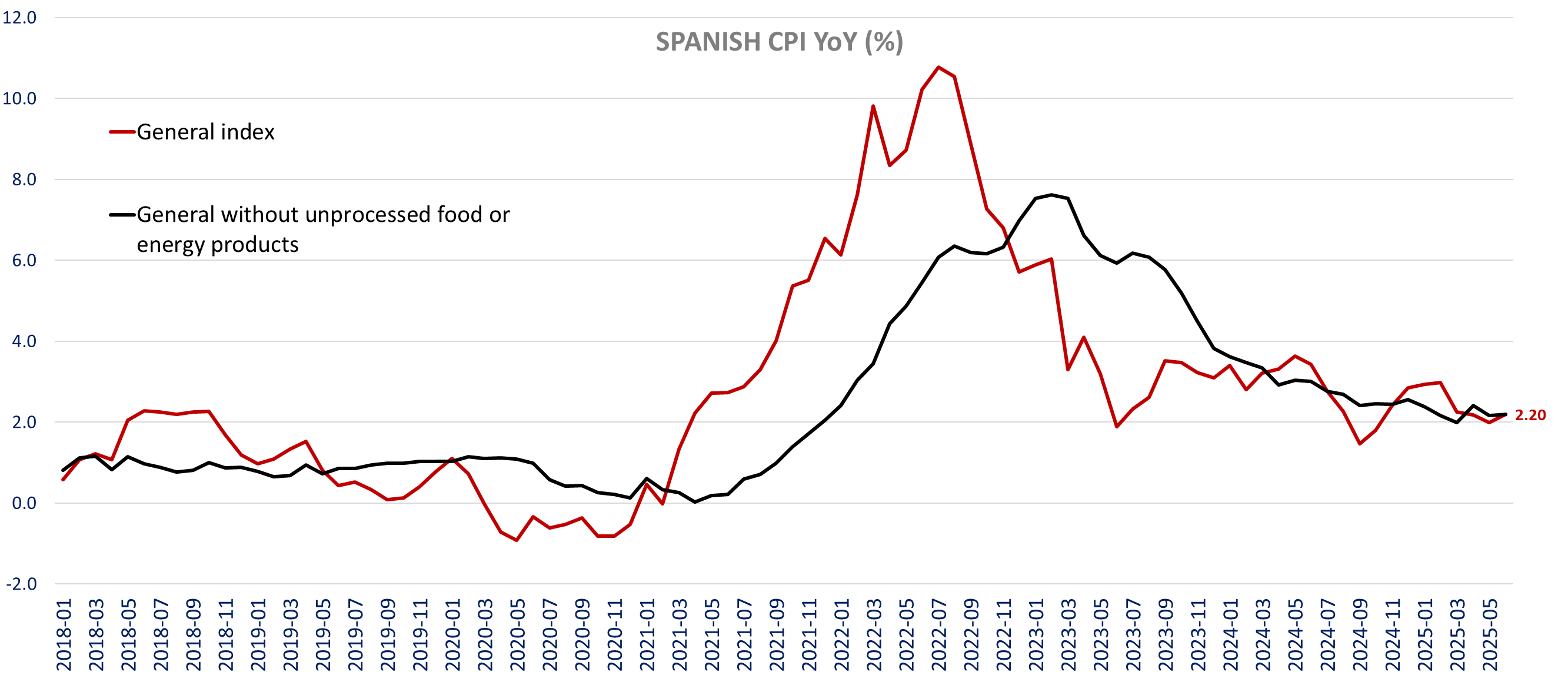

The Spanish CPI is also higher than anticipated in June as the INE post preliminary estimate of an increase in the CPI to 2.2% yoy from 2% in May (0.6% m/m) when expectations were for an unchanged CPI at 2%. It is the first increase in 3 months and the highest since March, The Core CPI is unchanged at 2.2% yoy (0.4% m/m) in line with expectations. The HICP is also up to 2.2% yoy from 2% yoy (also +0.6% m/m) in May also beating expectations for an unchanged rate of inflation. INE also mentioned higher fuel prices, but also higher Food & non-alcoholic beverages inflation.

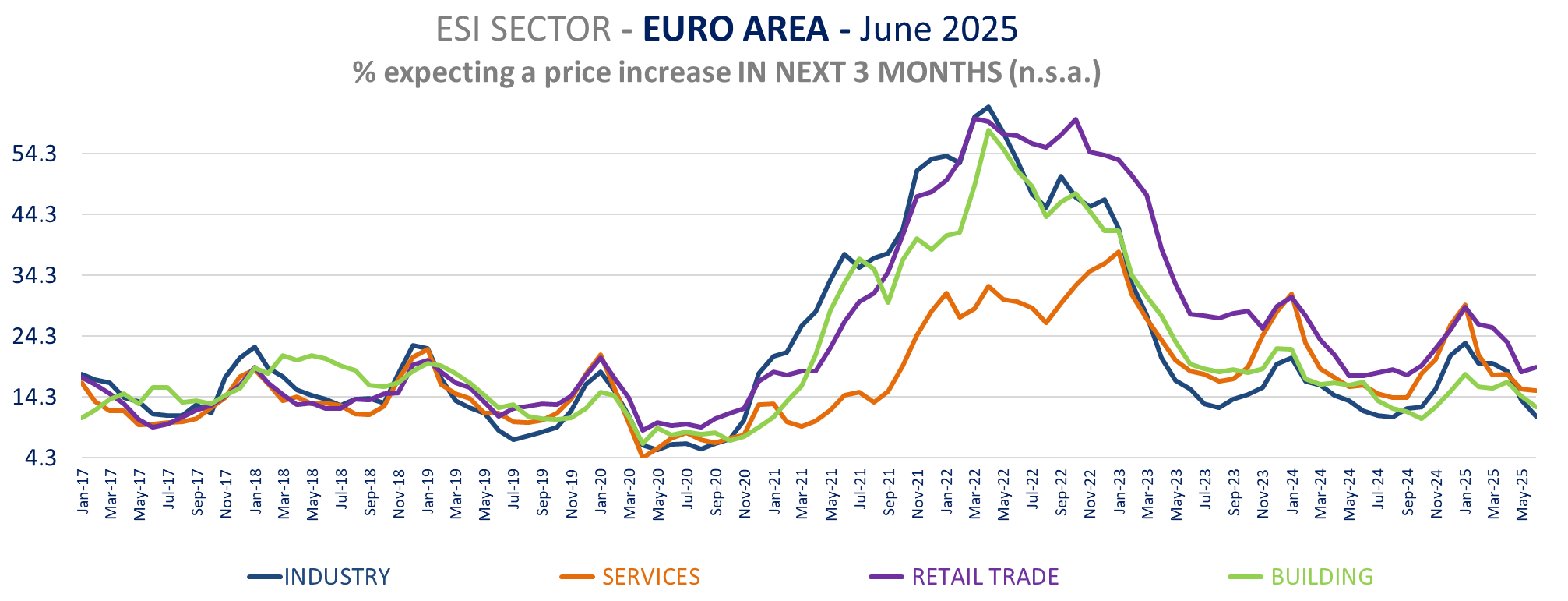

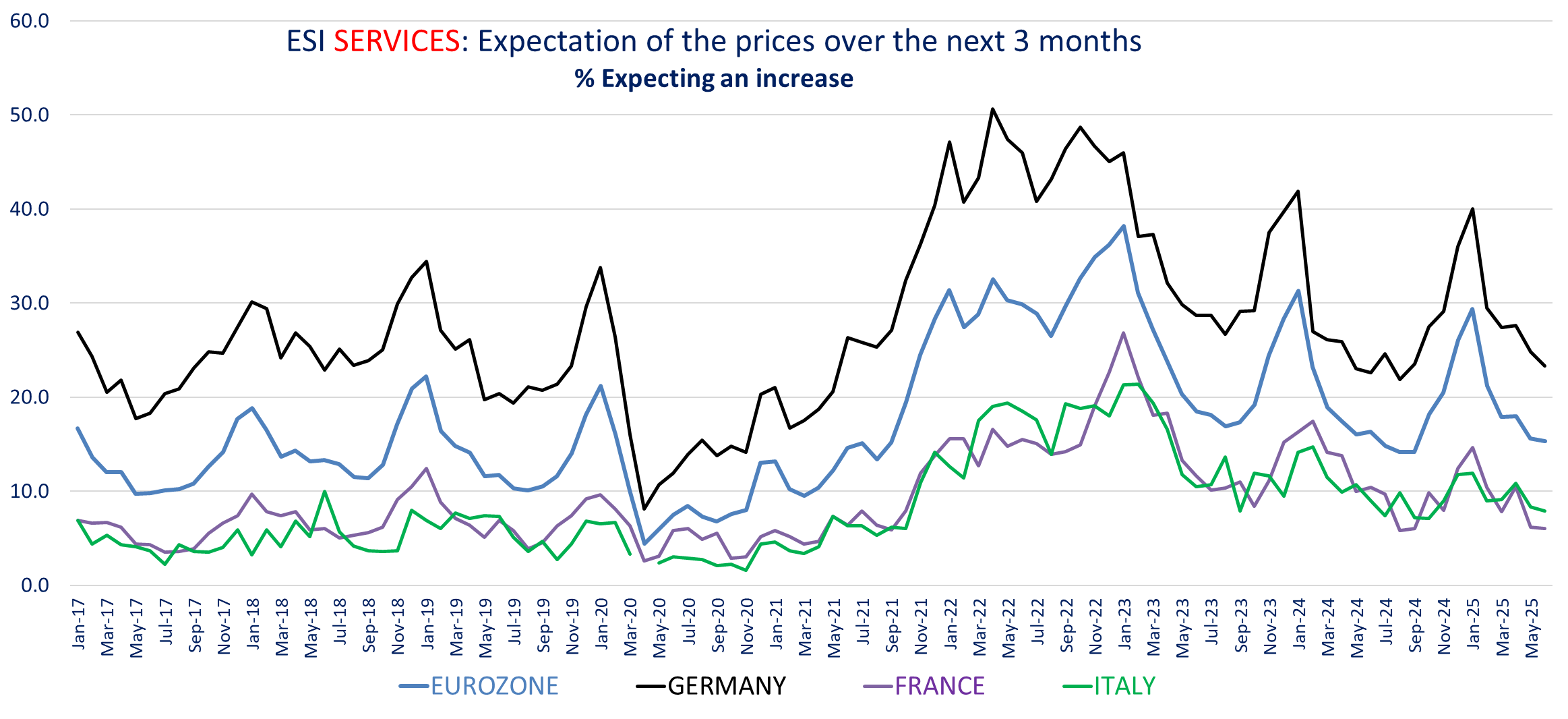

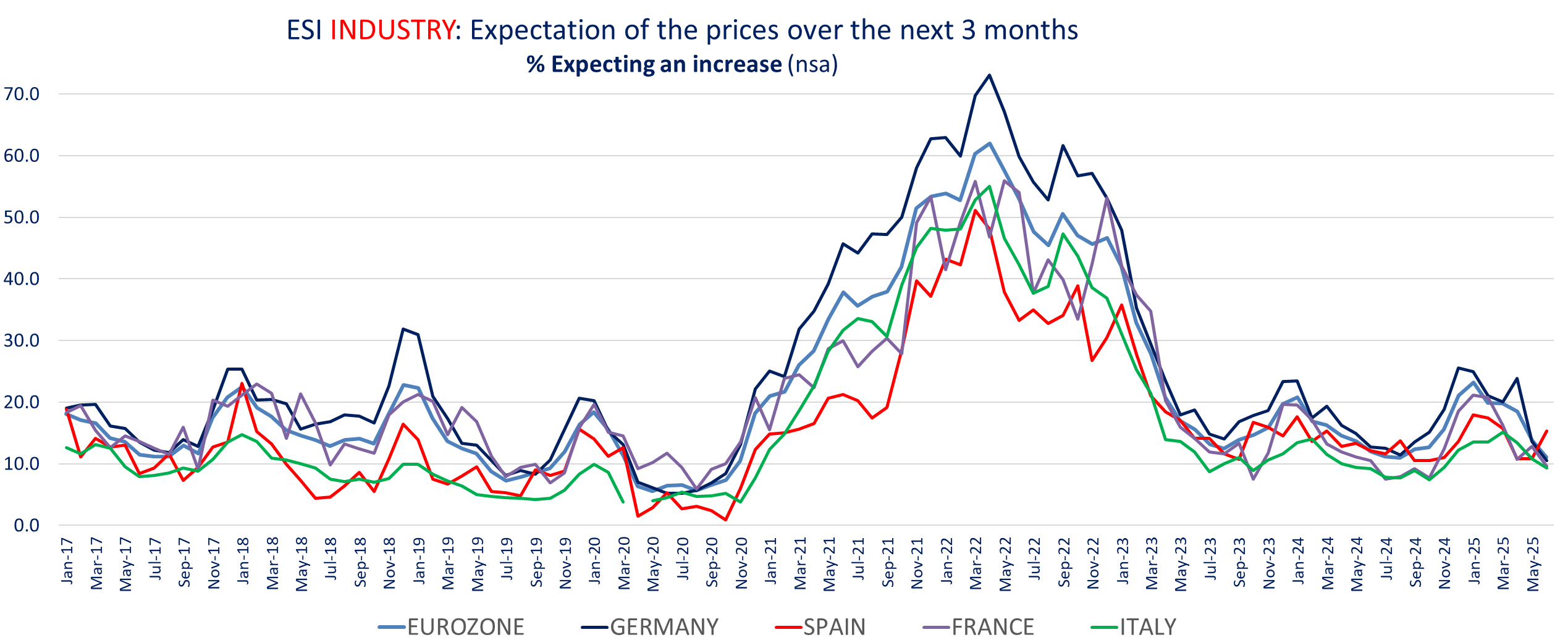

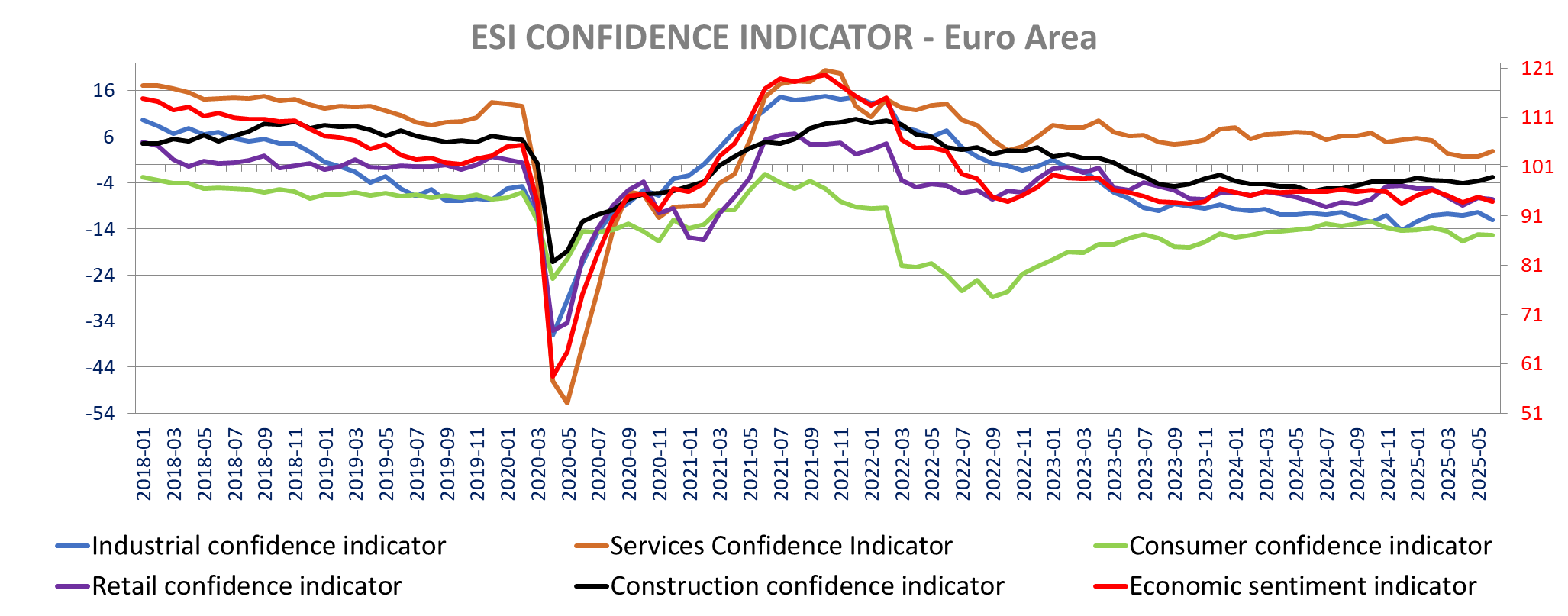

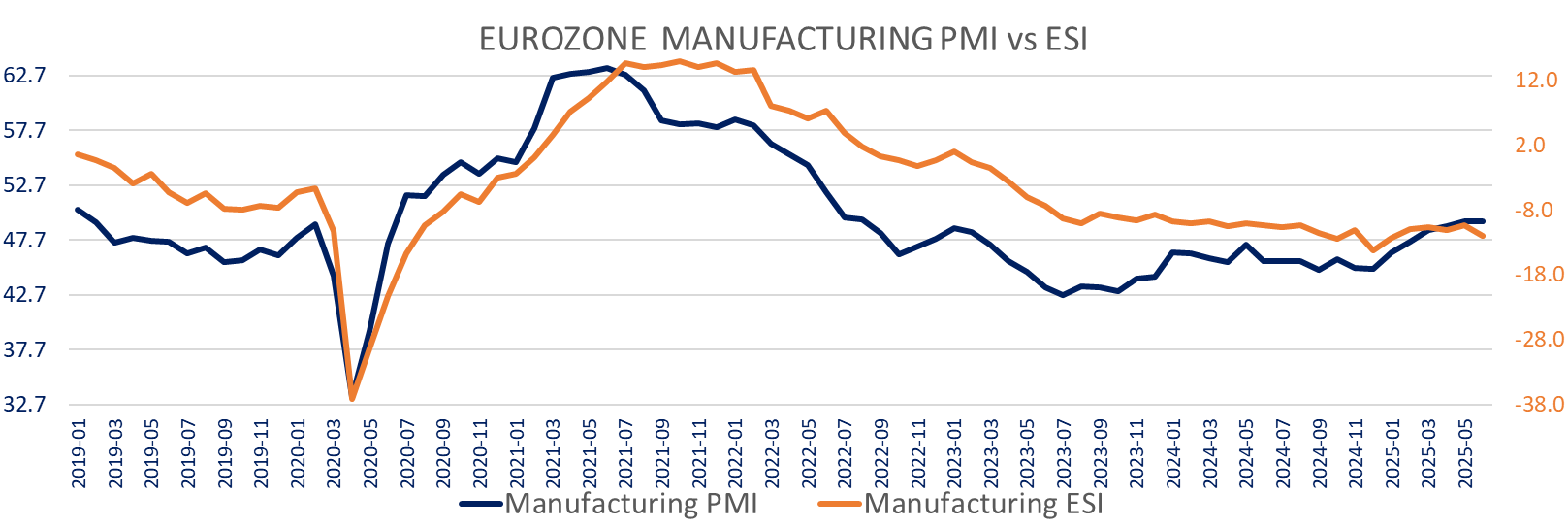

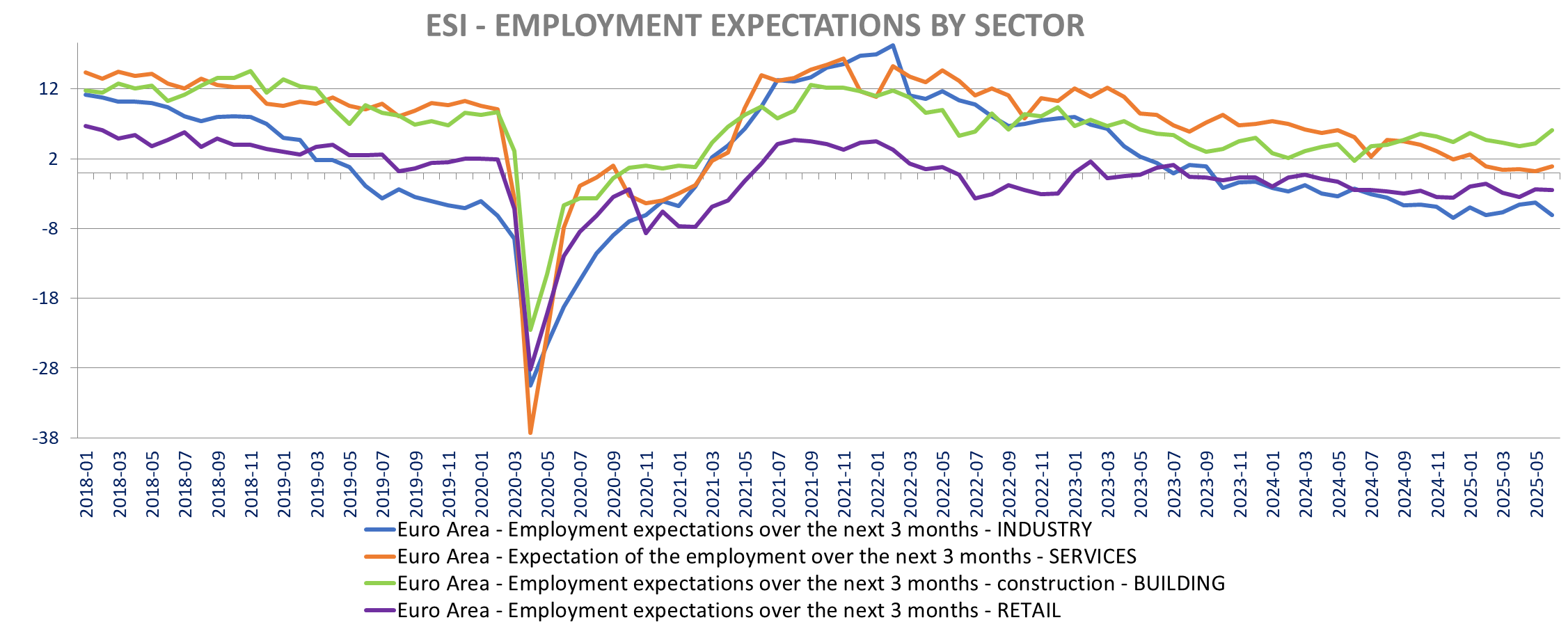

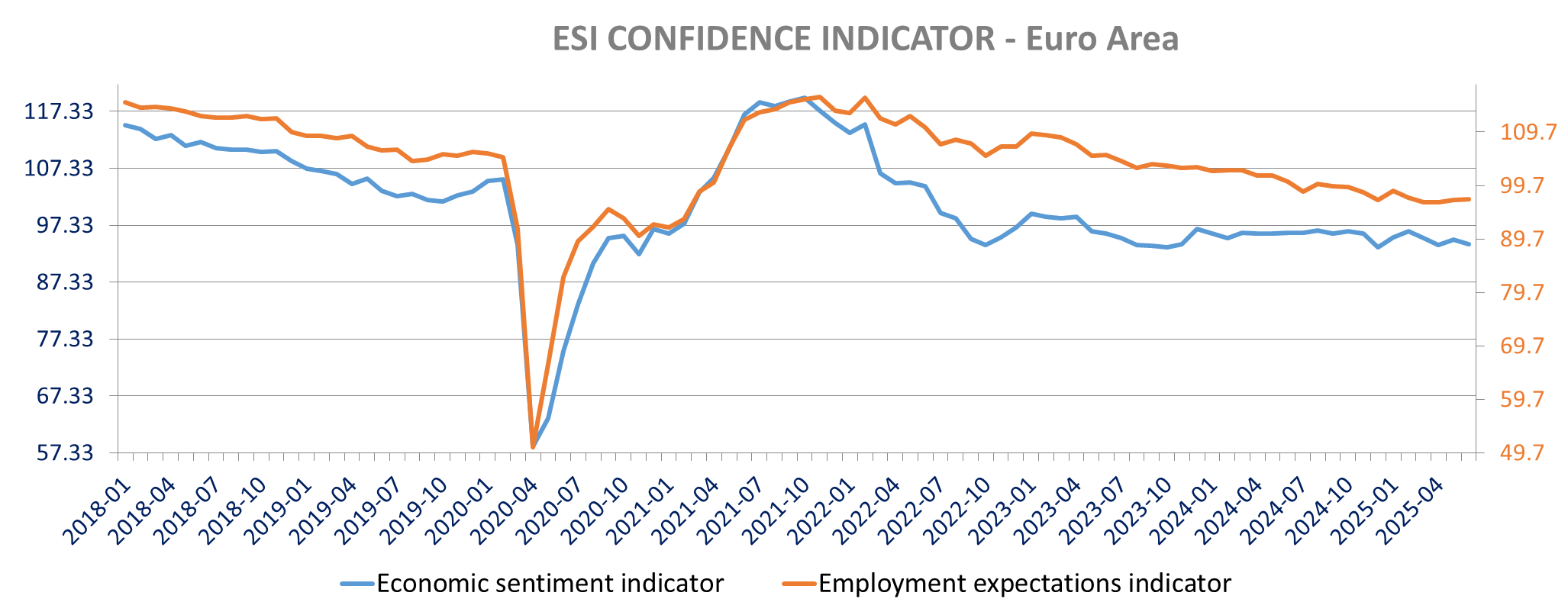

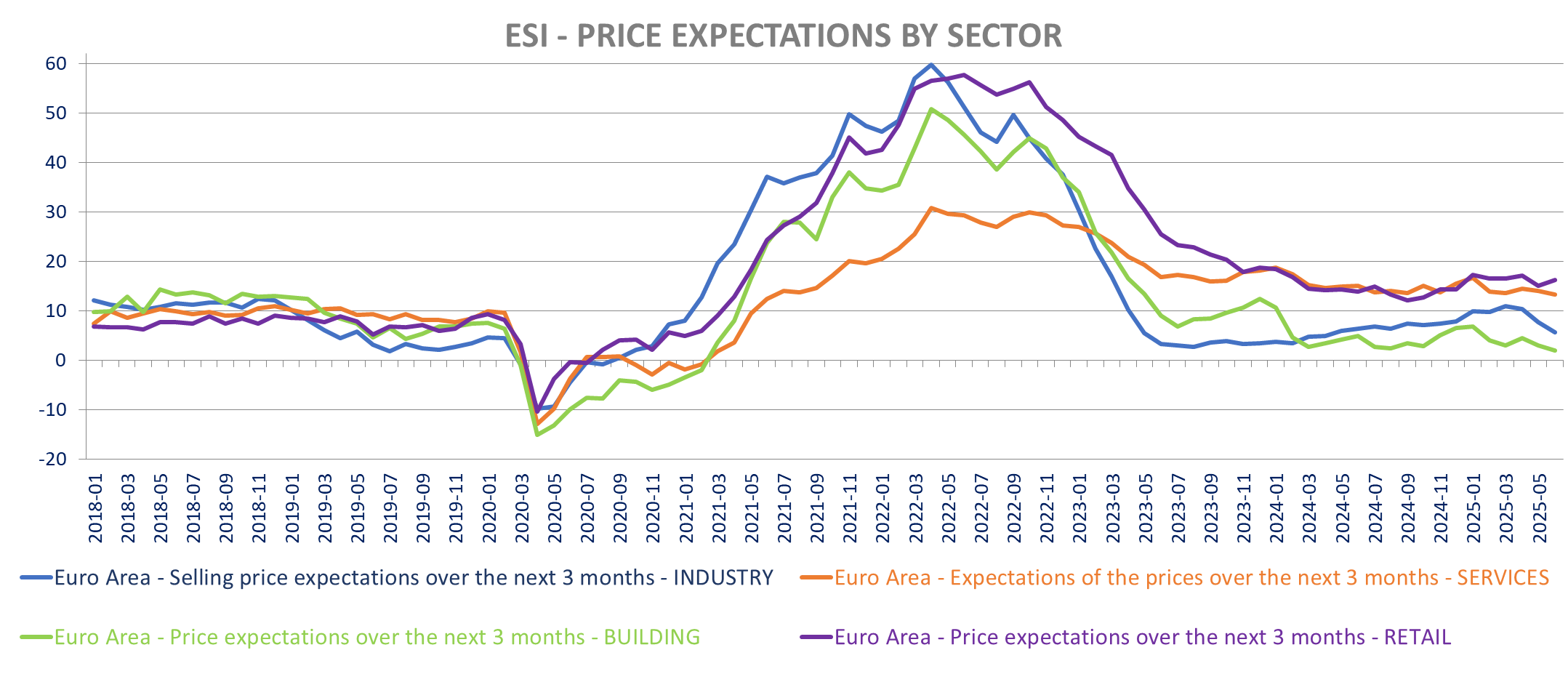

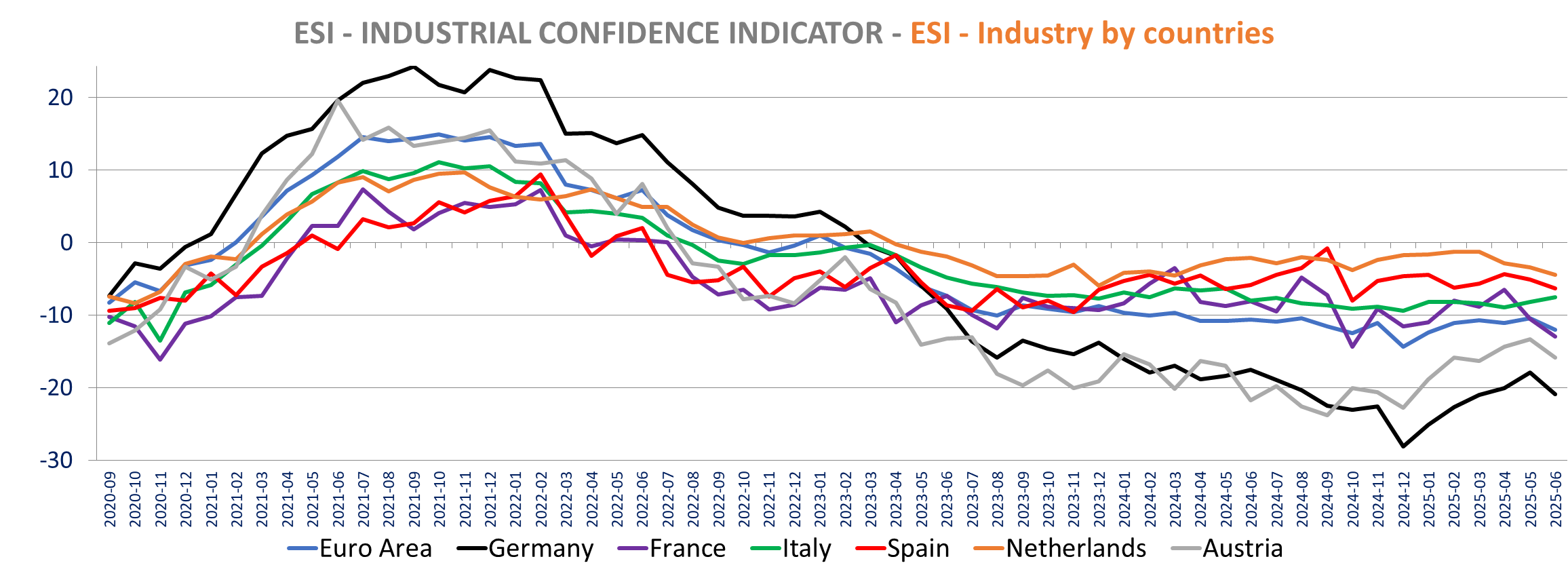

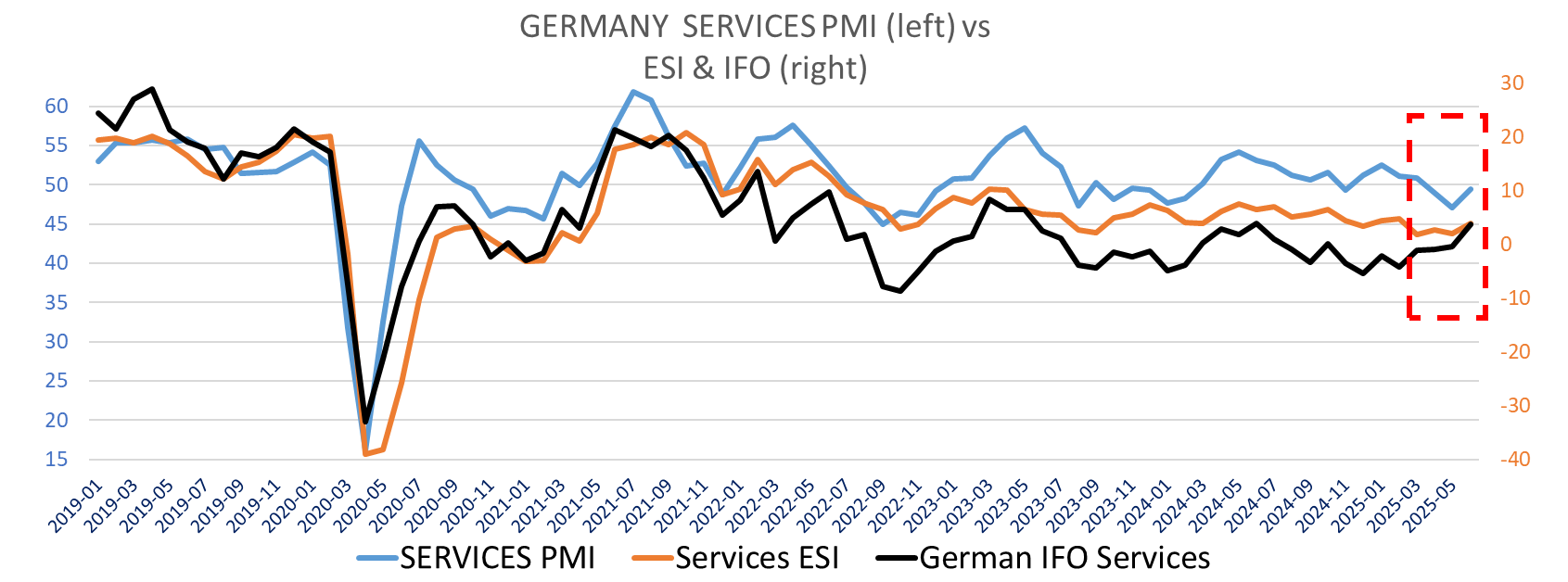

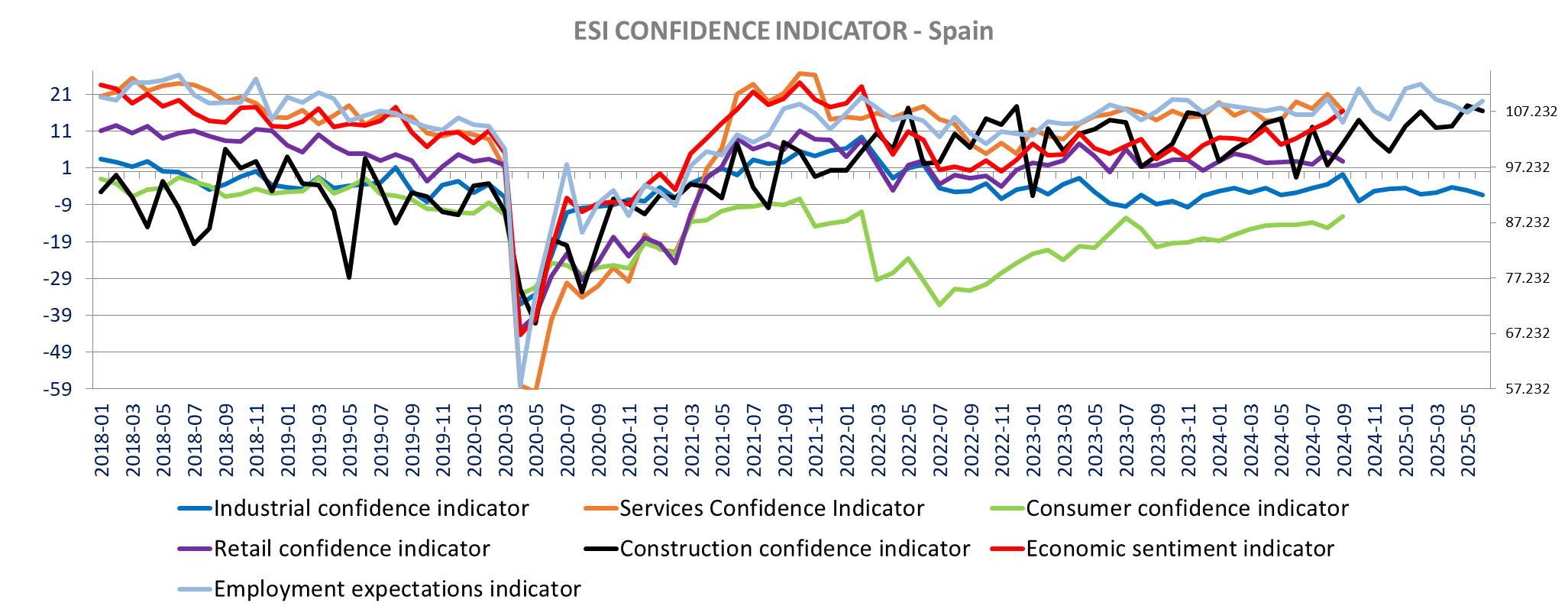

The Eurozone ESI is down in June (94 vs 94.8 in May) below expectations of an increase to 95.1. The decline is mainly due to weaker manufacturing (-12.0 vs -10.4, lowest since January), weaker than the Flash PMI released earlier this week (weaker than the flash PMI especially for Germany). The weakness in manufacturing is broad based, down in Germany, France, Spain, The Netherland and Austria (all more negative) and less positive in Greece. The Employment expectations Indicator improved marginally to 97.1 from 97 (best since February), improving in construction (+6.1 vs +4.2) and services (+0.9 vs +0.2) but declining slightly in retail (-2.5 vs -2.4) and manufacturing (+1.4 vs +1.5). The positive news is the tame price expectations. Price expectations are down in all sectors but retail (16.2 vs 15.1) falling to a 4-year low in services (13.3 vs 14.1), down in Manufacturing (5.6 vs 7.7m lowest since April 2024) and construction (2 vs 3, lowest since last October). The Question data also highlights the weak inflation expectations: 73.7% of service providers expects stable prices (up from 72.2% in May). 81.5% of manufacturers expects stable prices up from 79.7%.

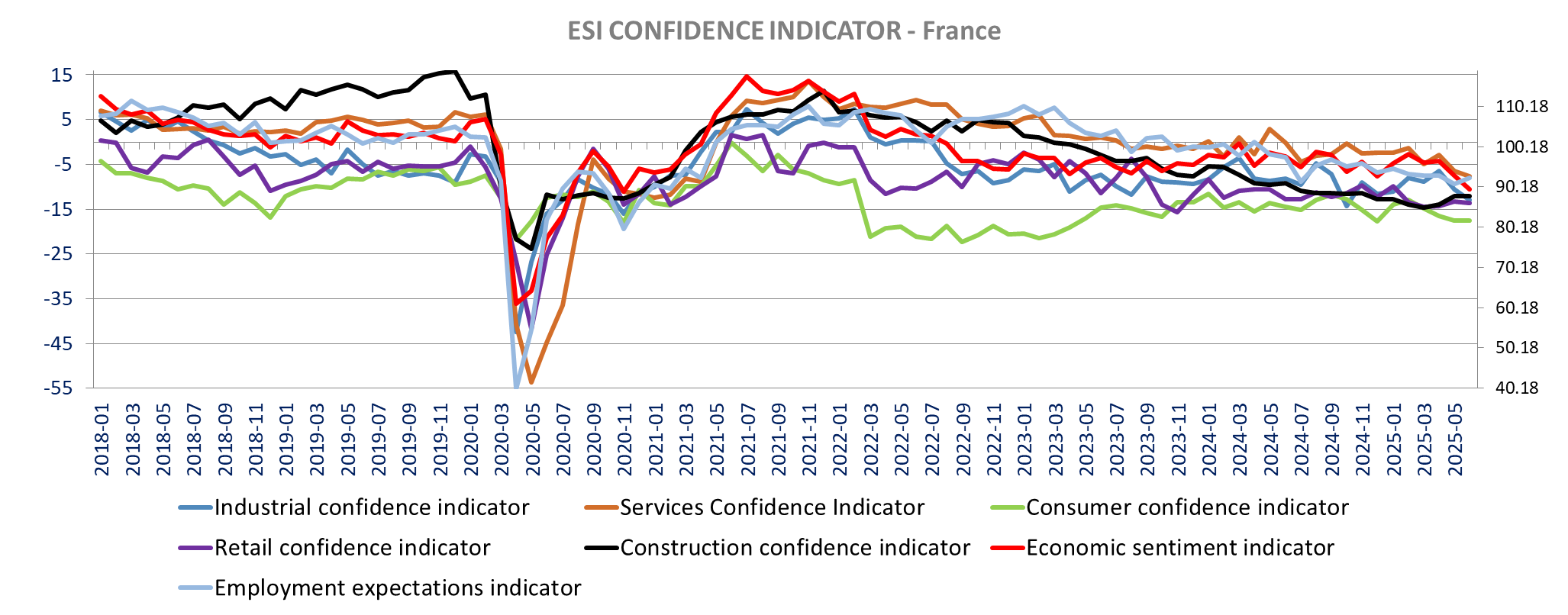

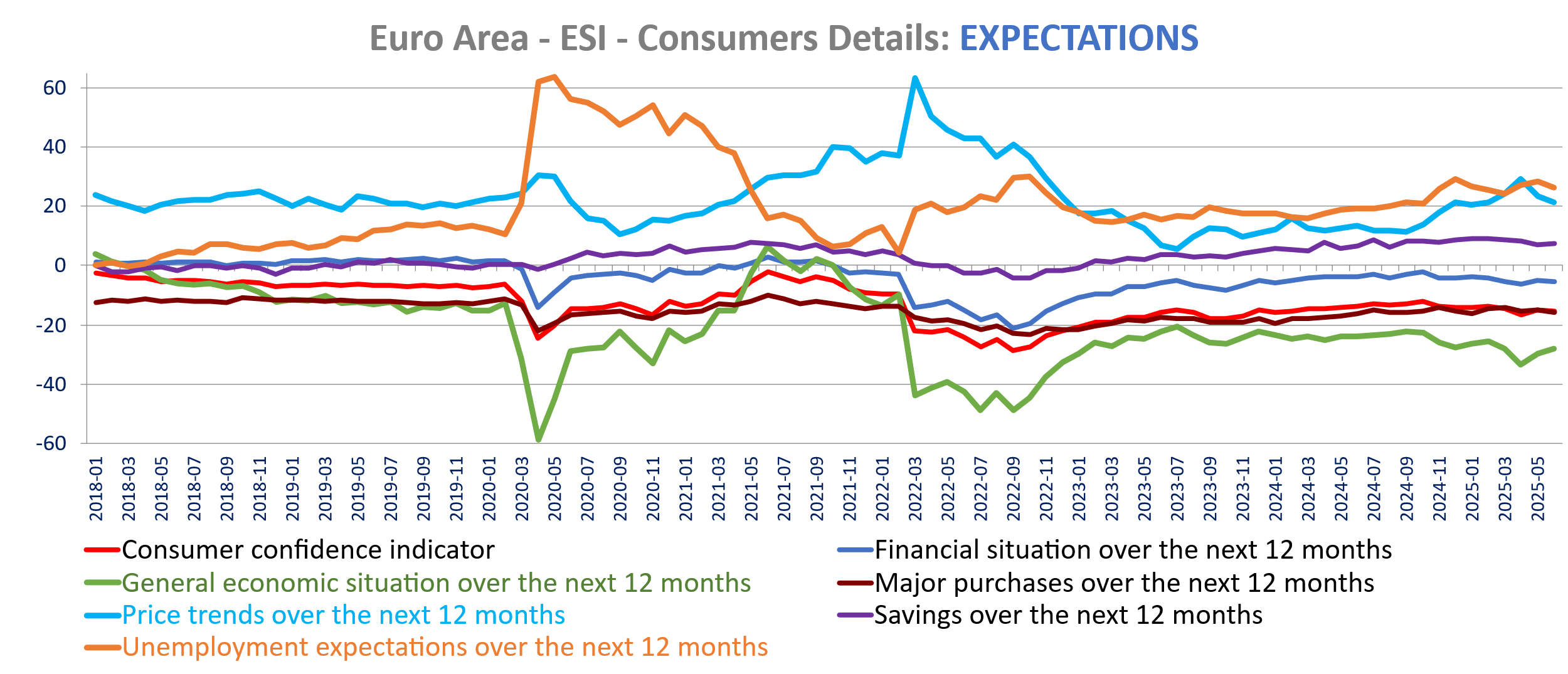

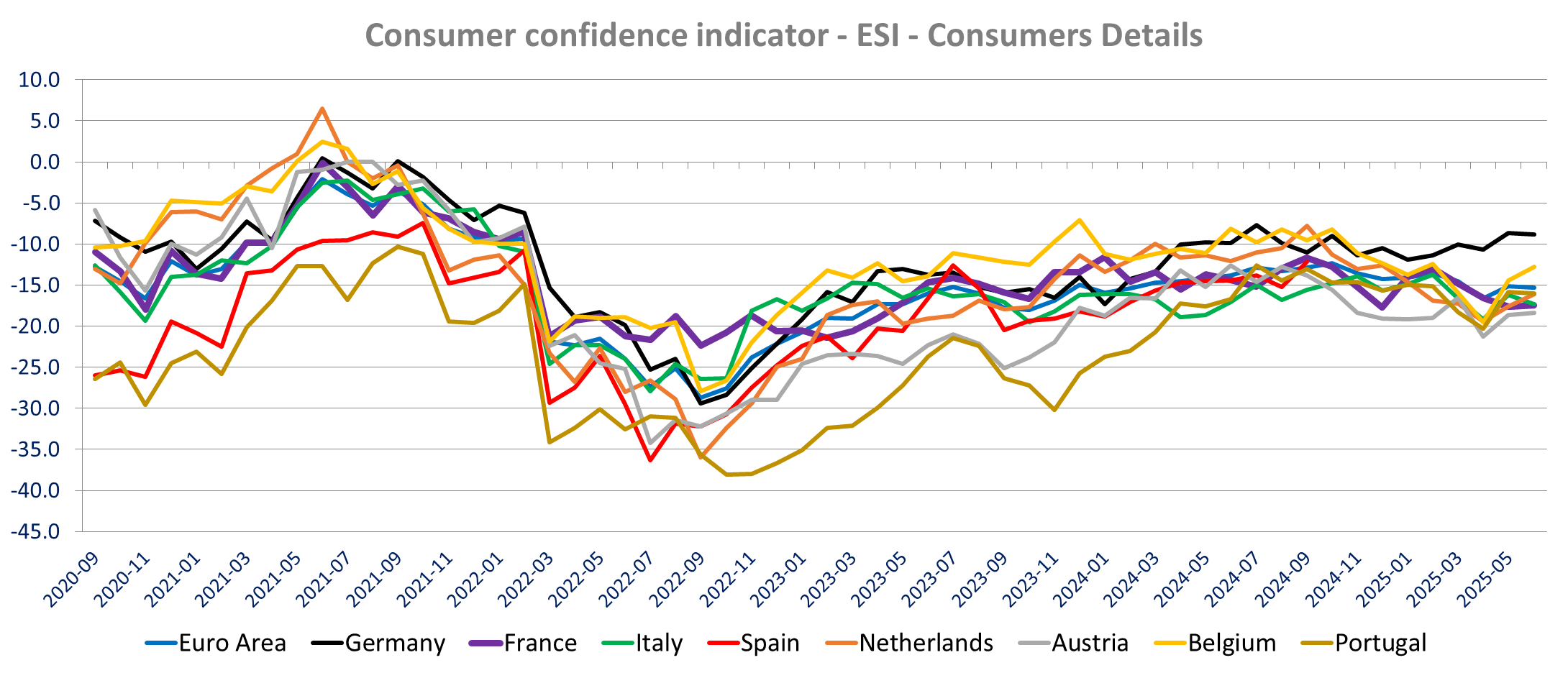

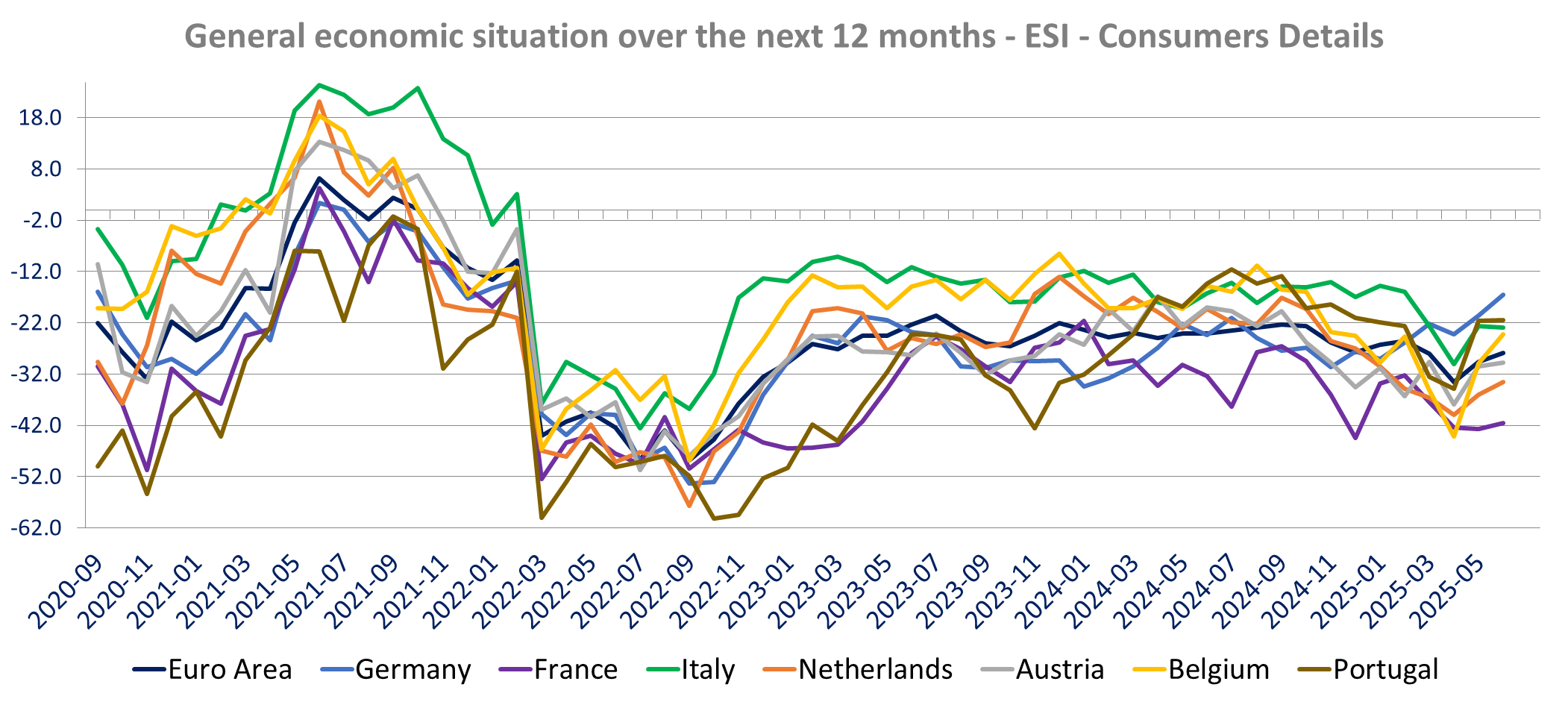

Little surprise from the Eurozone ESI consumer confidence. It is confirmed down to -15.3 from -15.1 in May exhibiting at the Eurozone level the characteristics we noted with the domestic data released earlier. Unemployment fear is down (26.2 vs 28.4), the sentiment over the economy has improved (outlook at -27.9 vs -29.5, best since February), and price expectations are tame (21.2 vs 23.6 lowest since January). Consumer confidence is up in most countries, marginally in France Finland and Austria but more marked in the Netherlands, Belgium Ireland. Confidence is marginally down in Germany and Portugal and down more significantly in Italy, and Greece. the ESI consumer survey shows a slight improvement for the economic outlook in France (INSEE was down) and. Italy, Greece are the only two countries showing a decline. All others show consumers less pessimistic in June on the economy ahead.

On the companies’ front: Edenred’s A week after dropping its collaboration with Hims and Hers Health, Novo Nordisk announces a collaboration with WeightWatchers to offer patients living with obesity access to FDA-approved Wegovy through NovoCare Pharmacy. Novo Nordisk also said that the company is in talks with additional potential partners. Unilever today announced it has signed an agreement to acquire personal care brand Dr. Squatch from growth equity firm Summit Partners. Dr. Squatch is distributed through digital commerce, retail and direct-to-consumer channels, primarily in North America and Europe. The terms of the deal were not disclosed. Banca Monte dei Paschi di Siena Spa announced that its board of directors has approved a capital increase of up to €13.19 billion in order to support the total and voluntary Public Exchange Offer on the shares of Mediobanca Spa. More details on equities here

Merz First EU summit.

Merz: “We need to move faster!”

EU: “Are you new or what..?

ESI data detailed by answer categories (nsa) – low price increase expectations. 73.7% of service providers expects stable prices (up from 72.2% in May). 81.5% of manufacturers expects stable prices up from 79.7%.

The latest Fed Balance sheet (as of Wednesday June 25, H.4.1 Release) shows a +$24.3bn increase in reserves week-over-week (base money +$25.44bn w/w) with a renewed decline in the Treasury General Account following the boost from the higher-than-expected tax receipts last week. The TGA is down to $334.6bn (-$49.7bn week to week and down -$111.7bn from the high on Tax Day of $446.3bn), in line with expectations.

The Reverse Repo was about stable week-over-week as of Wednesday June 25 up only+6.86bn w/w (o/w 5.8bn for the domestic repo) having only a mild negative impact on reserves. The Daily domestic RR data shows the start of the traditional spike at the end of the month /quarter end, going into the weekend. The domestic RR increased to $252.4bn on Thursday June 26 from $210.9bn on June 25.

The X-Date is now expected early August with the TGA expected below $40bn by mid-August.

X-Date

Treasury Secretary Scott Bessent extended the debt-ceiling-special measures through July 24, extending the power to use special accounting measure to stay below the current $36.1tn debt ceiling (it was expiring on June 27). As mentioned in past days, the June tax receipts were stronger than expected, giving the US treasury couple of additional weeks before the effectiveness of the extraordinary measures runs off.

The X-date is now expected in the first two weeks of August.

Delay in the OBBB and the lifting of the debt ceiling will put the government shut down back on the table by then. Hence Bessent urges congress to act by the August congressional recess to protect the “full faith and credit of the United States.”

After increasing to $446bn on June 16, the TGA is down to $334bn as of June 25 Without the lifting of the debt ceiling in July, simulation shows the TGA will be below $40bn by mid-August.

FRANCE CPI (June Preliminary).

INSEE June preliminary estimates for France CPI is above expectations of 0.7% yoy at 0.9% yoy up from 0.7% yoy in May. Prices increased 0.3% m/m rather than 0.2% anticipated. The HICP is also higher than consensus forecasts at 0.8% yoy (0.4% m/m) up from 0.7% yoy in May when 0.7% yoy / 0.2% m/m was expected.

The core CPI (not published) should be up in June.

SPAIN INFLATION (June Preliminary)

Spain inflation is also higher than anticipated in June as the INE post preliminary estimate of an increase in the CPI to 2.2% yoy from 2% in May (0.6% m/m) when expectations were for an unchanged CPI at 2%. It is the first increase in 3 months and the highest since March, The Core CPI is unchanged at 2.2% yoy (0.4% m/m) in line with expectations. The HICP is also up to 2.2% yoy from 2% yoy (also +0.6% m/m) in May also beating expectations for an unchanged rate of inflation.

The INE Release does not provide more details but mentioned that the increase in inflation was mainly due to higher fuel prices in June (vs a decline in June 2024) and an increase in Food & non-alcoholic beverages inflation (higher monthly increase in June 2025 than in June 2024).

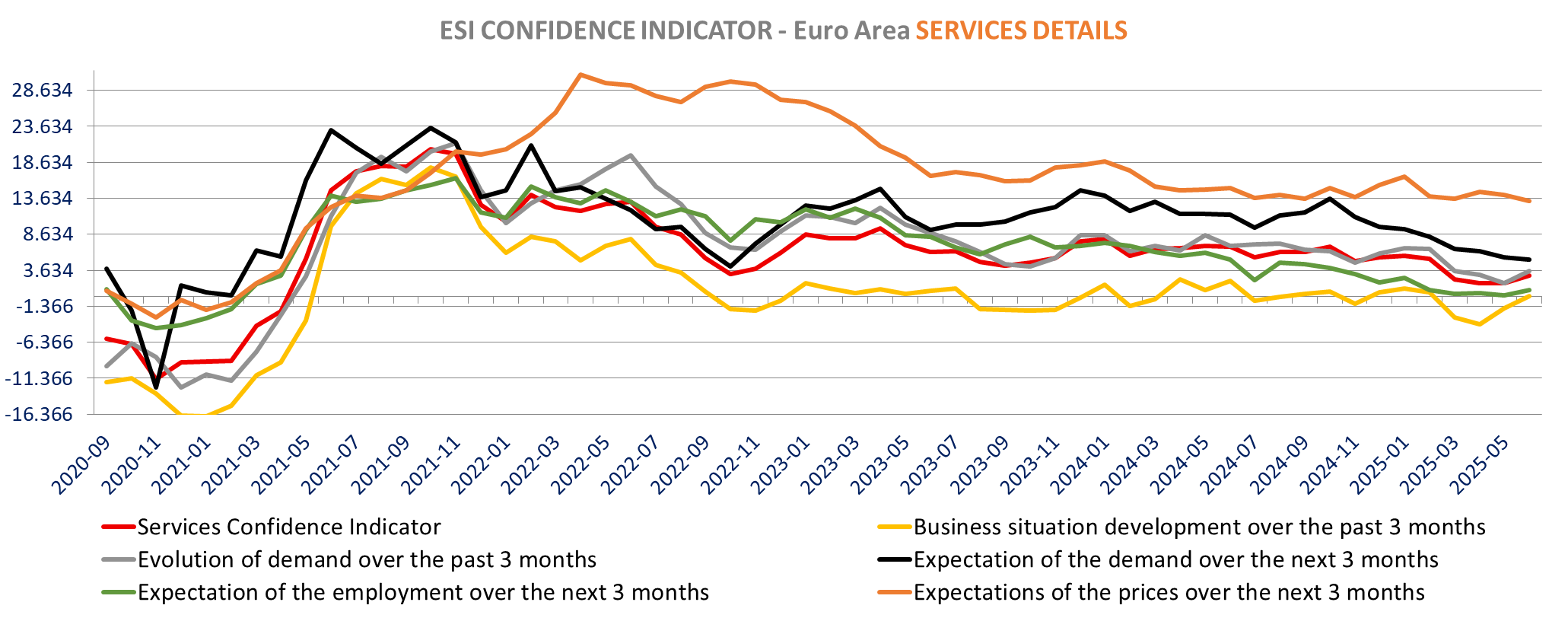

The Eurozone June ESI is down slightly to a two-month low of 94 from 94.8 in May, weaker than expectations for an improvement to 95.1. The decline is mainly due to weaker manufacturing (-12.0 vs -10.4, lowest since January), weaker than the Flash PMI released earlier this week (weaker for Germany). Services improved to the highest since February at +2.9 vs +1.8. Construction also improved in June at -2.8 from -3.5 a 1 ½ year high. Retail confidence is marginally lower at -7.5 vs -7.1.

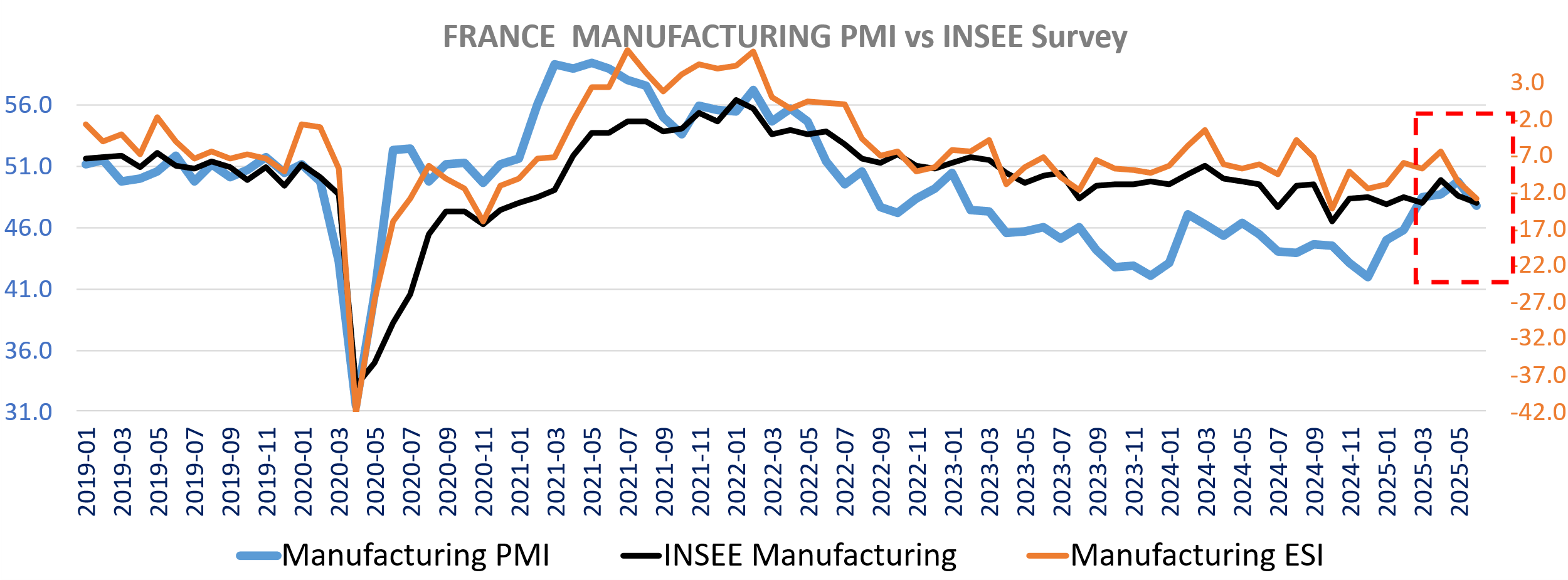

The weakness in manufacturing stems from lower order books assessment and lower output (-4.8 vs -2.2) as well as lower employment expectations. The weakness in manufacturing is broad based, down in Germany, France, Spain, The Netherland and Austria (all more negative). Italy, Belgium, Portugal and Finland are among the few countries seeing an improvement in manufacturing (less negative). Greece manufacturing ESI is down to +3.1 from+5.1, remaining in positive territory.

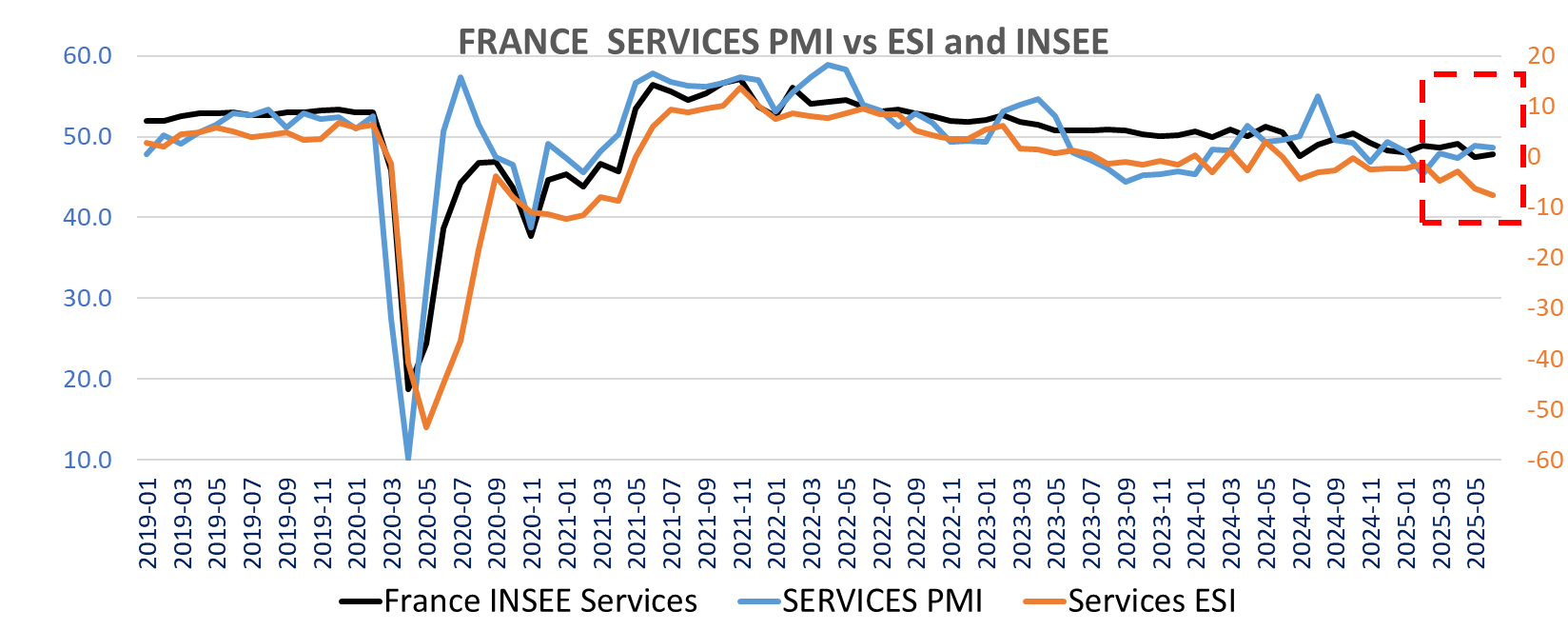

For services the improvement comes from the past business situation (0 vs -1.7) and demand (+3.5 vs 1.8) while expected demand is slightly down (5.1 vs 5.4). Employment expectations also improved (0.9 vs 0.2). In terms of countries, the improvement in services is relatively broad-based, down significantly in France (-7.6 vs -6.4), lower in Austria (4.8 vs 3.8), but higher in the other countries, Notably Belgium (+3.5 vs -0.3) and Portugal (4.2 vs 12.2). Germany (4 vs 2), Italy *2.5 vs 1.8) and the Netherlands (4.8 vs 3.8) also posted good improvement. The ESI services is in line with the flash PMI for the Eurozone, but much weaker for France.

The Employment expectations Indicator improved marginally to 97.1 from 97 (best since February), improving in construction (+6.1 vs +4.2) and services (+0.9 vs +0.2) but declining slightly in retail (-2.5 vs -2.4) and manufacturing (+1.4 vs +1.5)

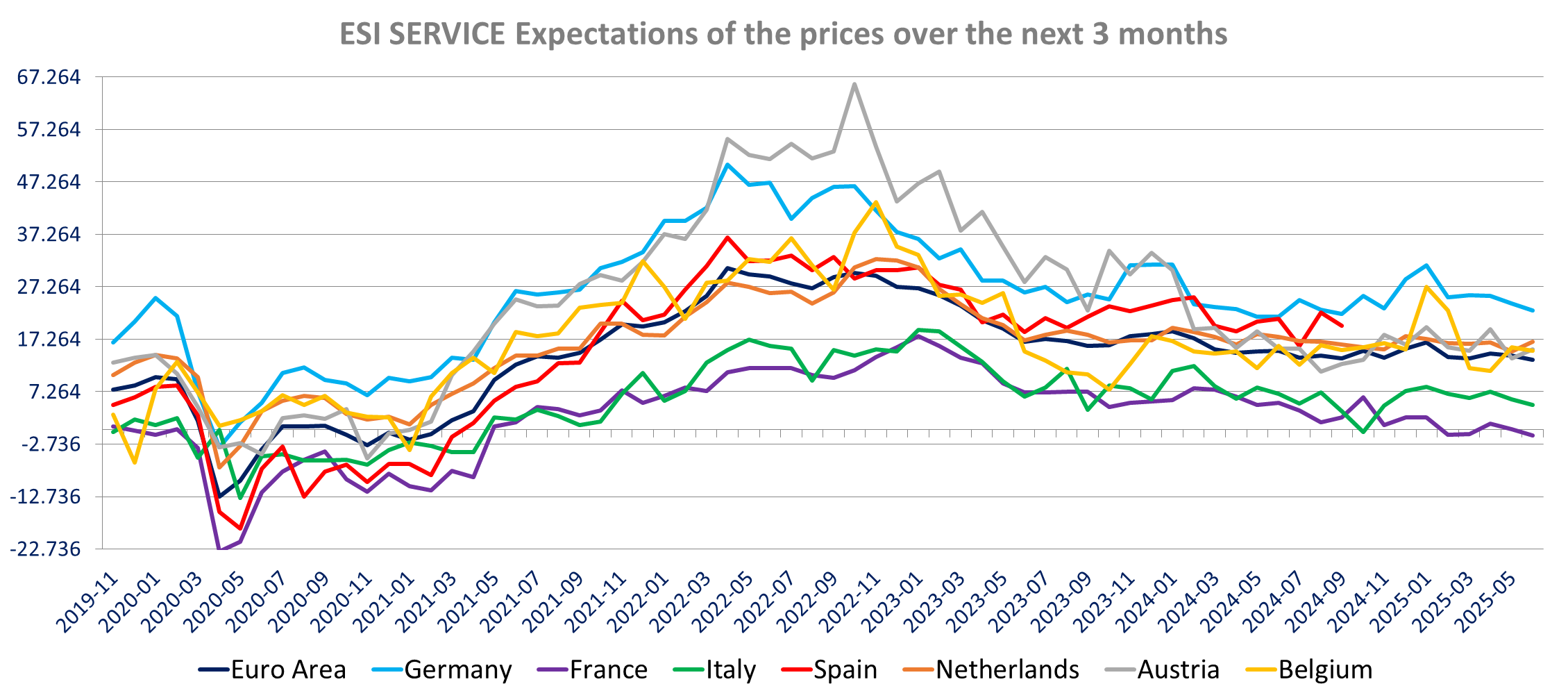

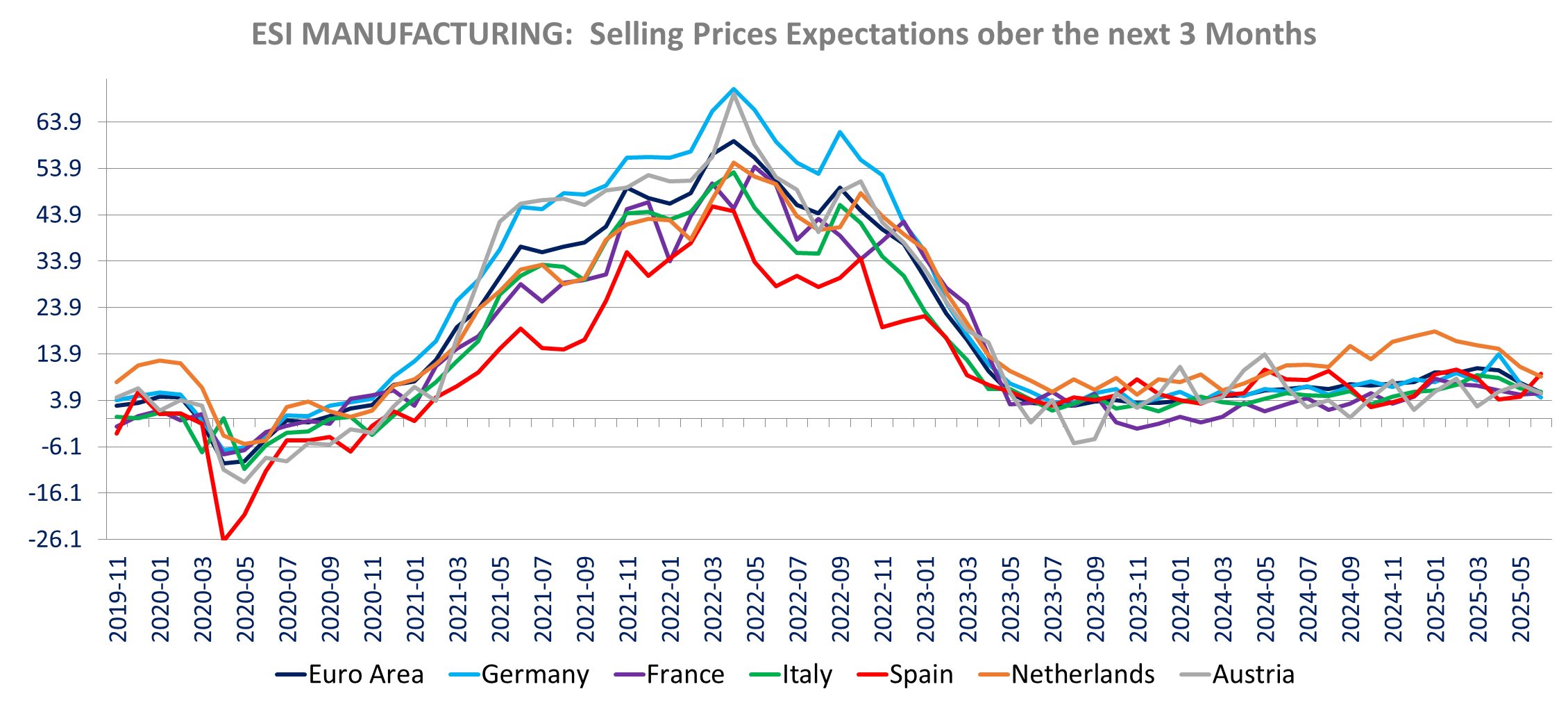

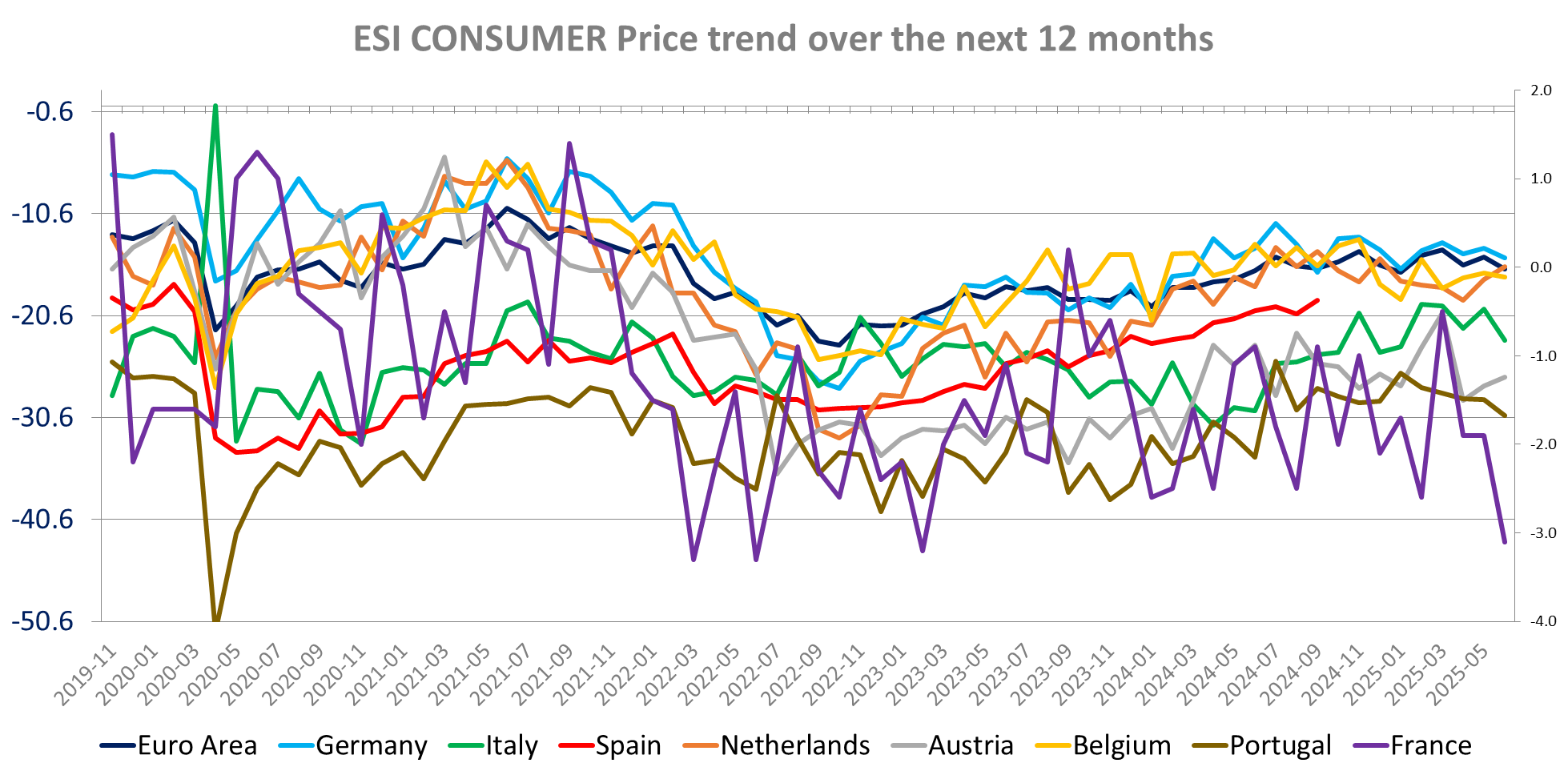

Price expectations are down in all sectors but retail (16.2 vs 15.1) falling to a 4-year low in services (13.3 vs 14.1), down in Manufacturing (5.6 vs 7.7m lowest since April 2024) and construction (2 vs 3, lowest since last October). Consumers’ price expectations are also lower to 21.2 from 23.6, lowest since January. Services Price expectations are down in Germany, France and Italy, and up in Belgium, the Netherlands and slightly in Austria. In manufacturing selling price expectations are down in all major countries but Spain (9.7 vs 4.7) and more marginally France (5.4 vs 5.2).

Sector Details

Country Details

The Eurozone June consumer confidence is confirmed down to -15.3 from -15.1 in May exhibiting at the Eurozone level the characteristics we noted with the domestic data released earlier. Unemployment fear is down (26.2 vs 28.4), the sentiment over the economy has improved (outlook at -27.9 vs -29.5, best since February), and price expectations are tame (21.2 vs 23.6 lowest since January). On the other hand, the consumer confidence is dragged down by weaker personal financial situation past (-12 vs -11.2) and Future (-5.3 vs -5) and lower propensity to make large purchases (-16 vs -14.8, lowest since January). As seen in Germany, savings intentions are higher (7.5 vs 7.1).

FINLAND CONSUMER CONFIDENCE

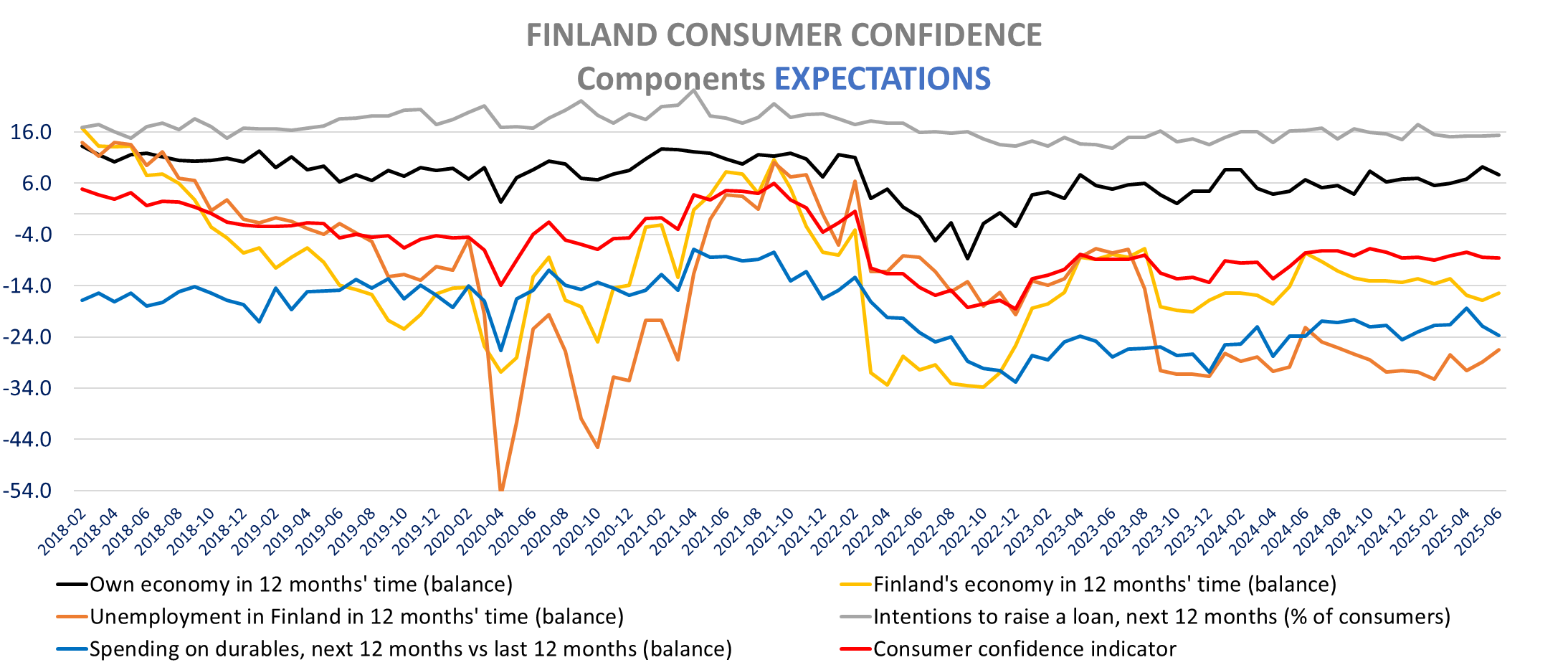

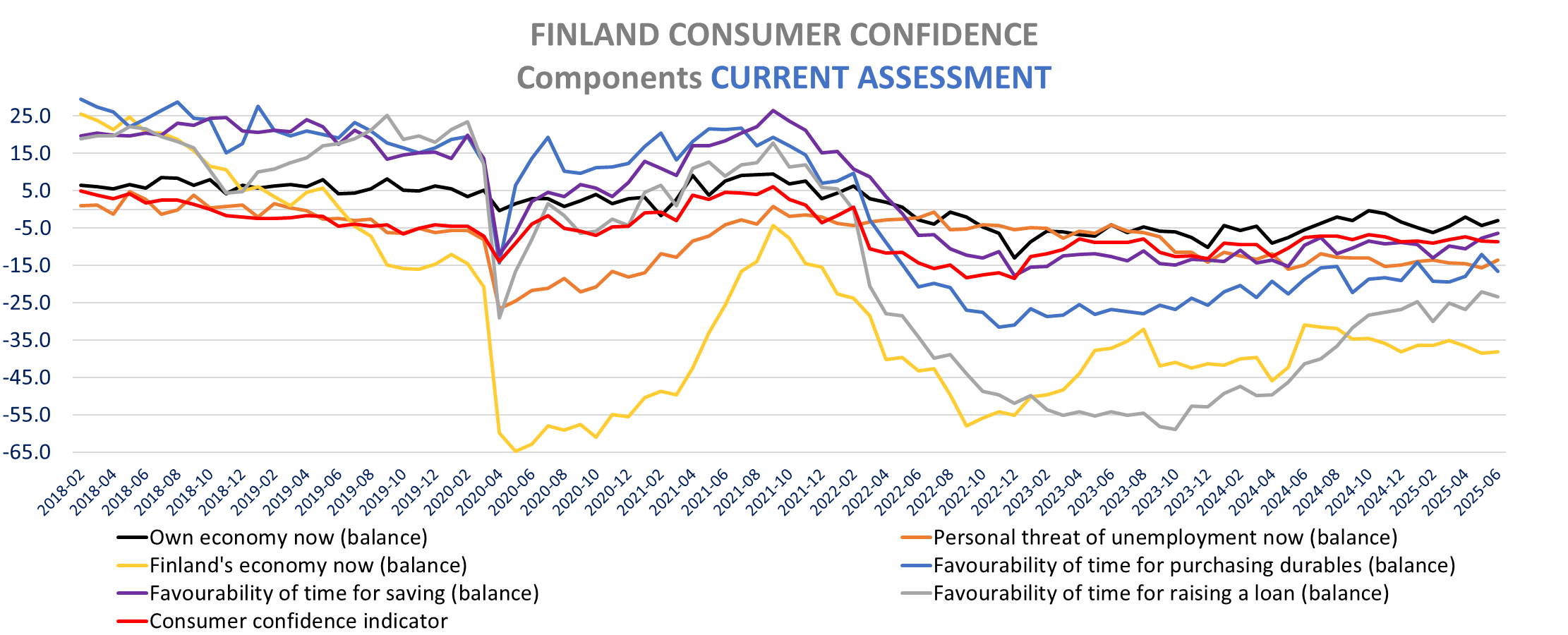

Finland consumer confidence decline slightly in June to -8.6 from -8.4, the lowest level since February (-9) on weaker personal situation ahead. Albeit remaining low Finnish consumers view on the economy is less negative in June, both nowt (-38.2 vs -38.6) and in 12 months’ time (-15.4 bs -16.8). Consumer surveys for all European countries so far but France have posted an improvement in economy outlook.

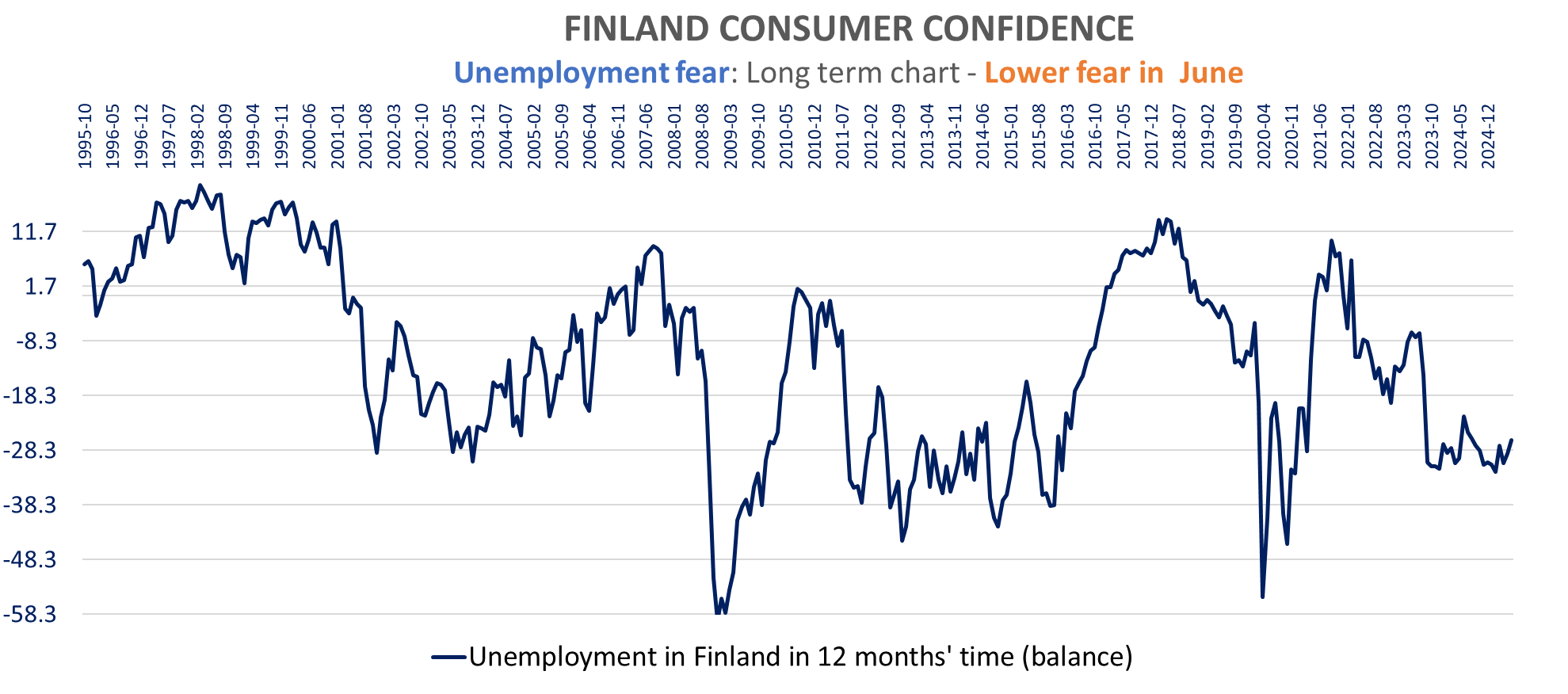

Finland households also join the other European countries with lower unemployment fear: General at -26.5 vs -28.9, lowest since August 2024 and personal at -13.5 vs -15.7, the lowest since last October.

Inflation expectations are slightly down (4% vs 4.1%). Consumers remain cautious and intentions to make large purchases is down both now (-16.7 vs -12.1) and in the next 12 months (-23.7 vs -21.9). It is the case for cars, dwelling and Households see the present time as less favorable for raising a loan (-23.4 vs -22)

|

|

|

|

|

|

|

Friday, June 27, 2025 | ||

|

NVO | |||

|

DKK |

441.10 |

+2.36% | |

|

NVO |

A week after dropping its collaboration with Hims and Hers Health, Novo Nordisk announces a collaboration with WeightWatchers to offer patients living with obesity access to FDA-approved Wegovy through NovoCare Pharmacy. Novo Nordisk also said that the company is in talks with additional potential partners. | ||

|

|

|

|

|

|

UNVB | |||

|

EUR |

51.98 |

+0.85% | |

|

UNVB |

Unilever today announced it has signed an agreement to acquire personal care brand Dr. Squatch from growth equity firm Summit Partners. "This complementary acquisition marks another step in expanding Unilever’s portfolio towards premium and high growth spaces." Dr. Squatch has reached millions of people through its retail and direct-to-consumer model with natural, high-performance personal care products including natural soaps and body washes, deodorants, hair care, skin care, and other men’s grooming products with unique scents and quality ingredients. Dr. Squatch is distributed through digital commerce, retail and direct-to-consumer channels, primarily in North America and Europe. The terms of the deal were not disclosed. | ||

|

|

|

|

|

|

BMPS | |||

|

EUR |

7.05 |

-2.69% | |

|

BMPS |

Banca Monte dei Paschi di Siena Spa announced that its board of directors has approved a capital increase of up to €13.19 billion, in accordance with the delegation granted by the general meeting of April 17, in order to support the total and voluntary Public Exchange Offer on the shares of Mediobanca Spa. | ||

Versus early hours:

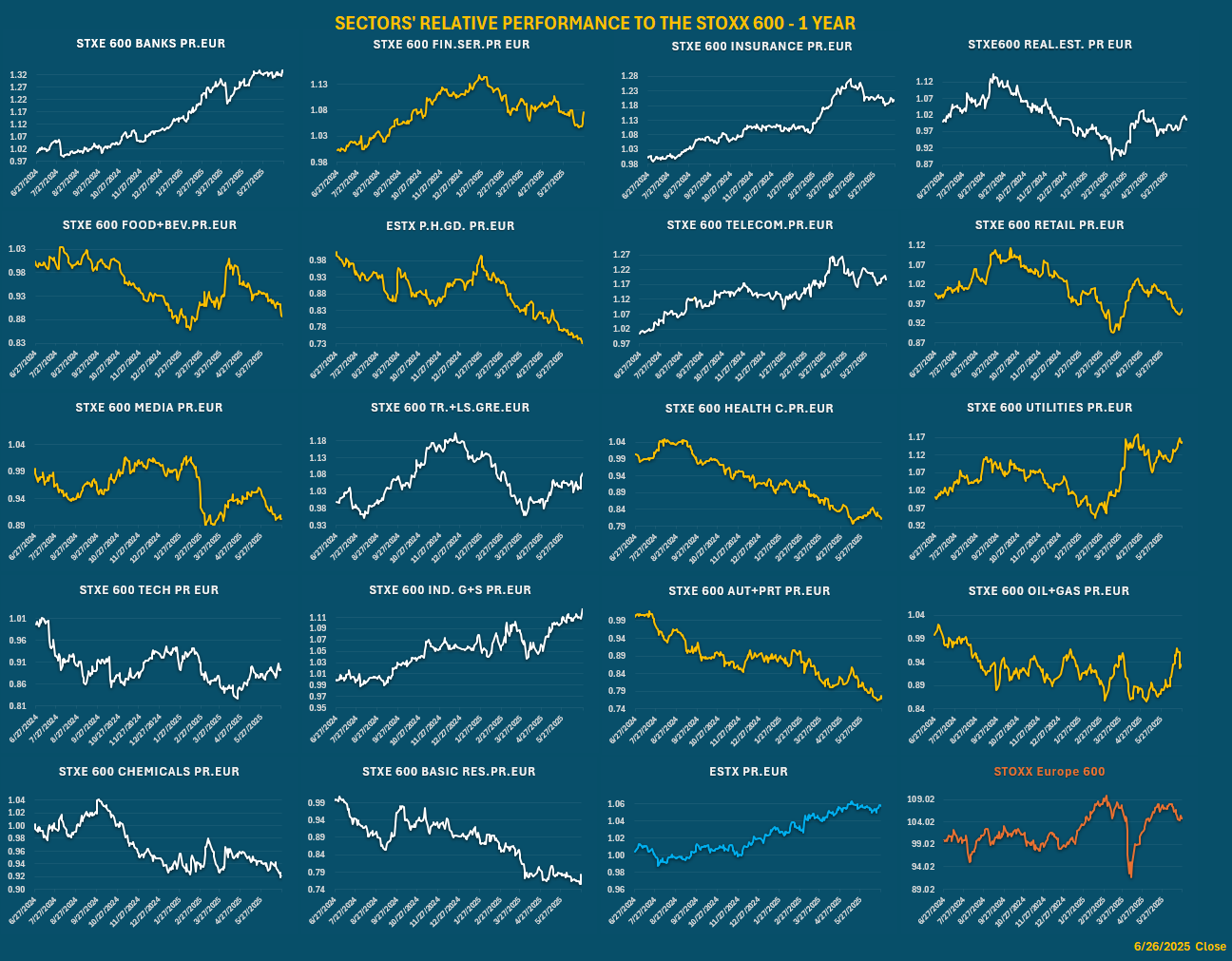

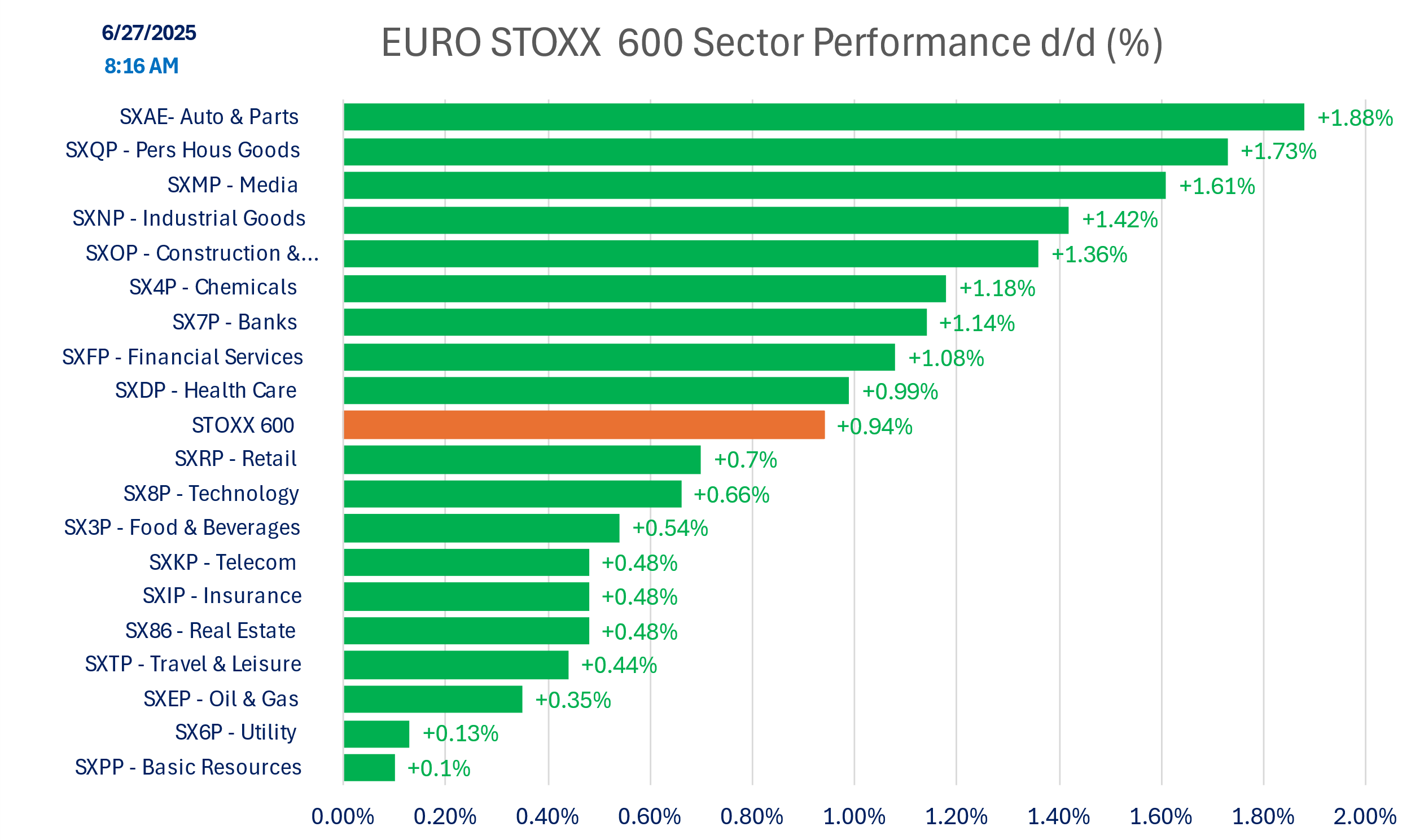

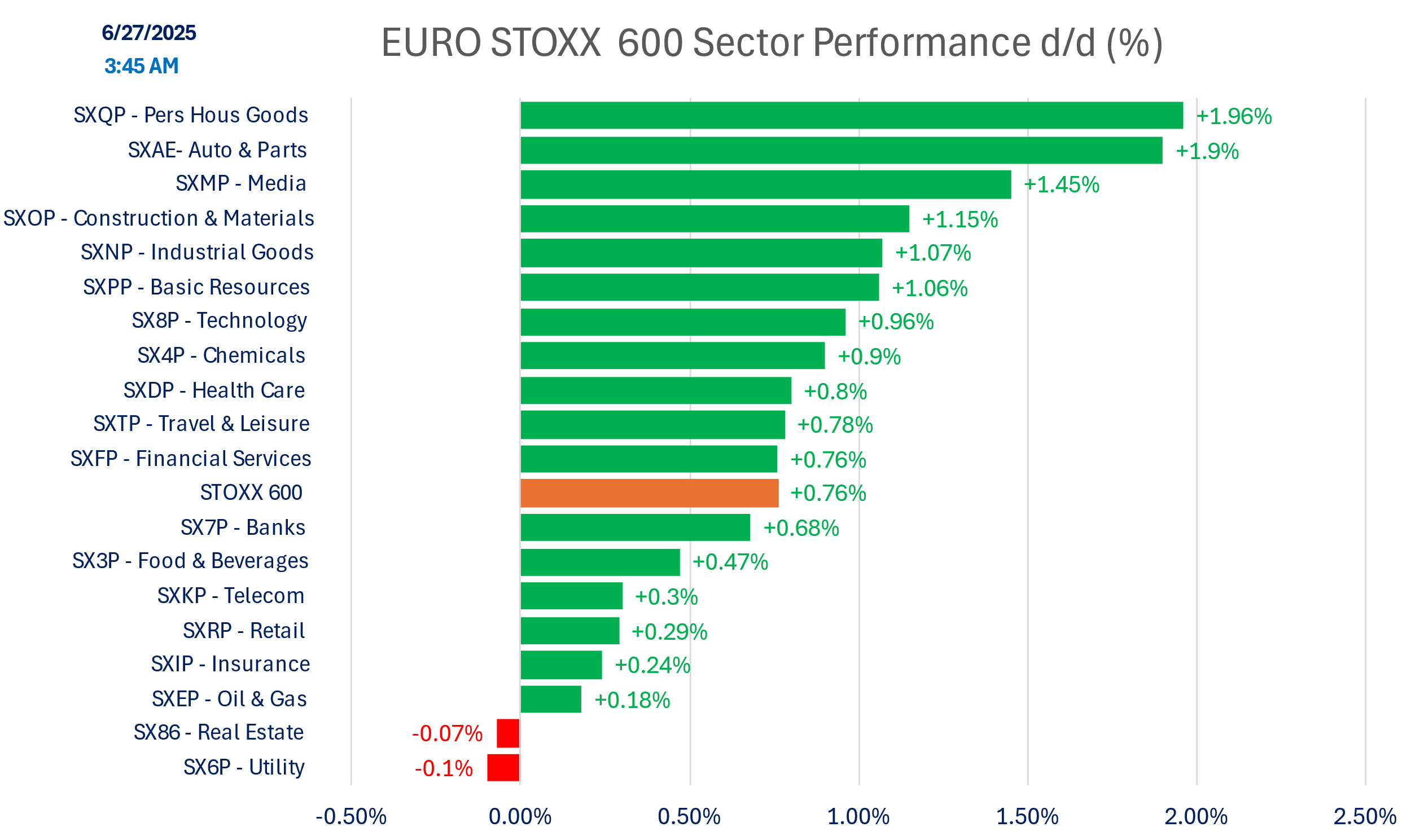

SECTOR PERFORMANCE

Relative performance to STOXX 600

Today’s Performance

Versus early hours:

Indices

Versus early hours

Commodities

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.