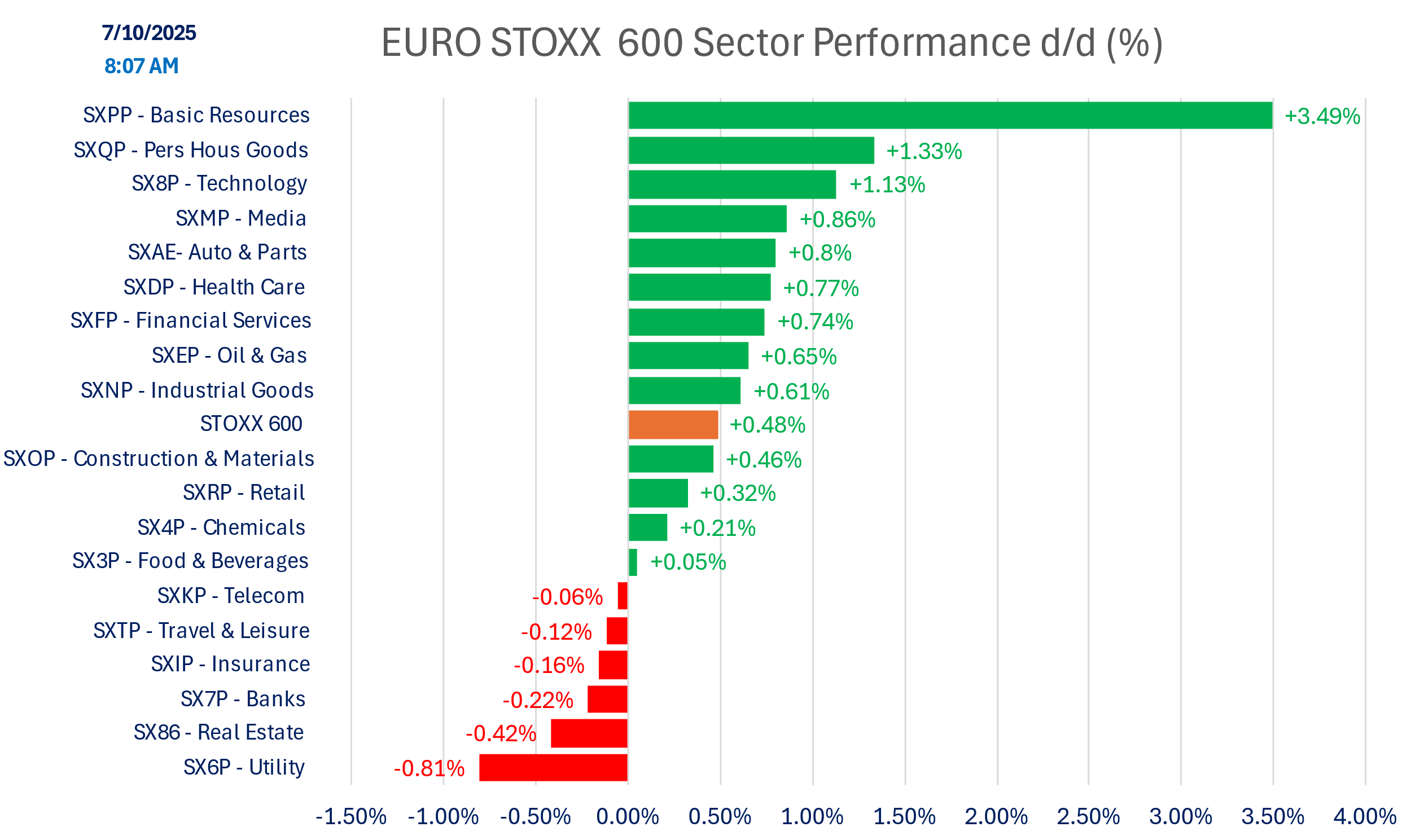

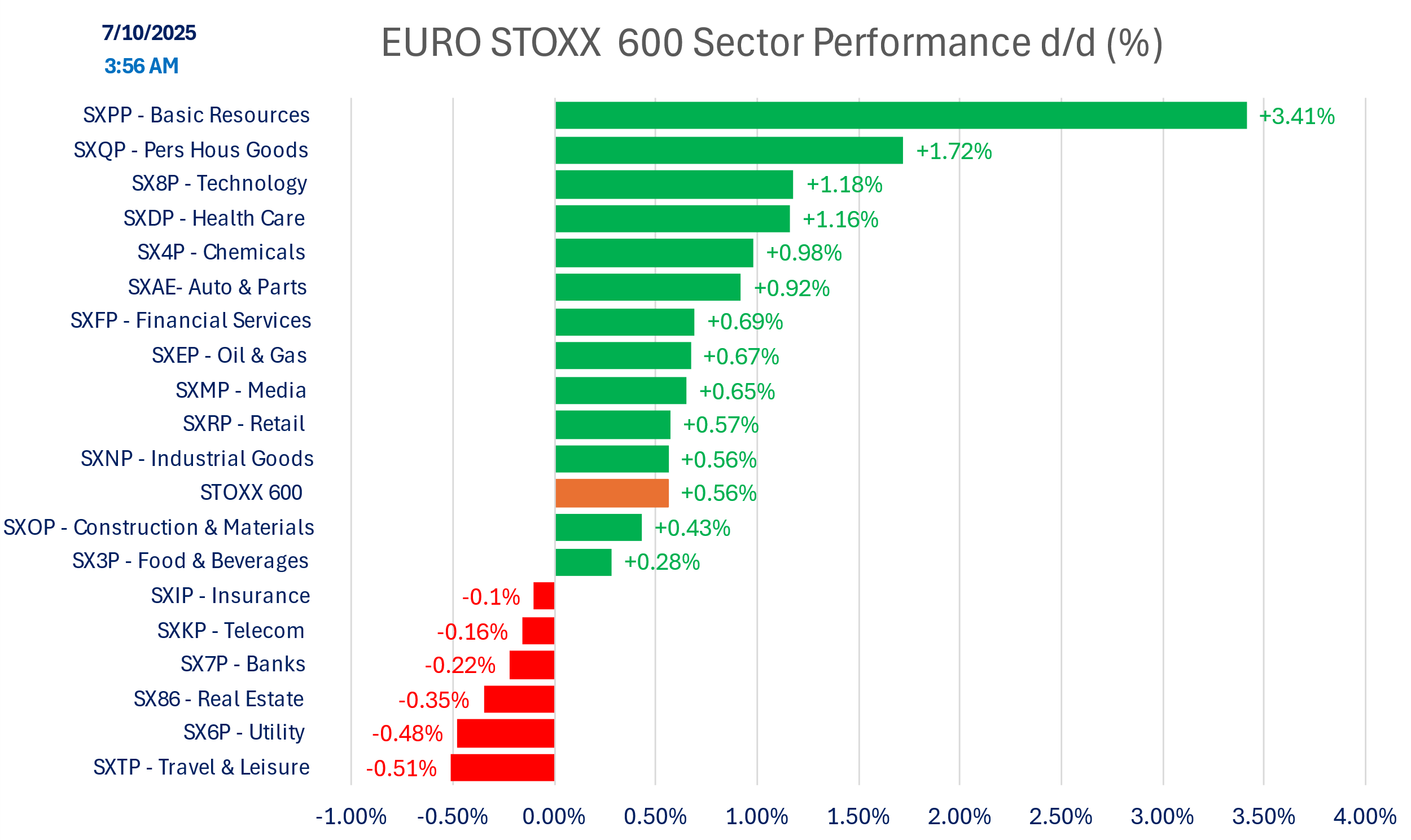

The 50% tariff on copper is confirmed with a start on August 1st, resulting in scramble to deliver copper ahead of the deadline. The COMEX-LME spread widen further. Copper is up 15% m/m and 23% yoy. Basic resources stocks are outperforming.

But the threat of 50% tariff on Brazilian goods is even more unsettling as it is a reminder that tariffs are not based on economic criteria, but remain highly political, making “deals” not so bidding. Market remains complacent, expecting some additional delay in tariff implementation or lower tariffs than expressed in recent letters (not that different from the flawed Liberation Day tariffs). More letters are expected, and the EU still hope to avoid one. True framework deals are slow to materialize and the blunt Lutnick approach seems to prevail.

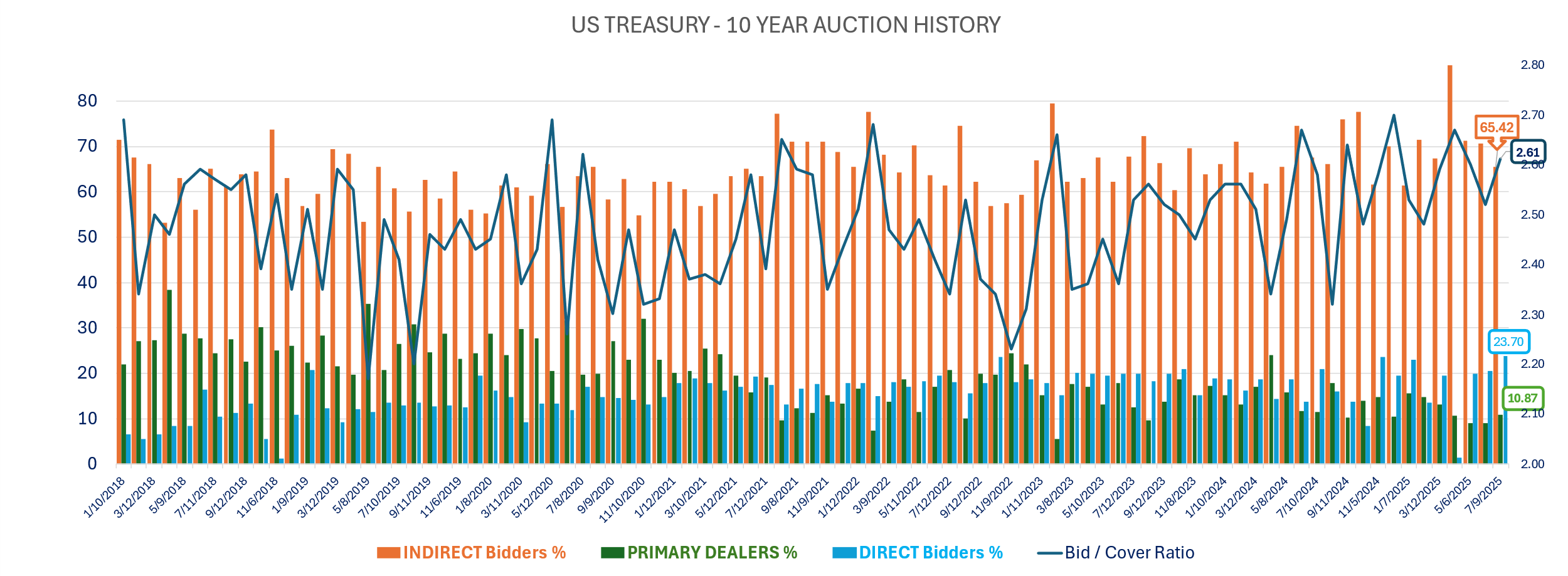

Bond yield eased yesterday after an OK 10yr US Treasury auction that was overall better than feared with relatively good demand but we see a slight increase this morning with the 30yr bonds yield increasing in Japan, US and Germany ahead of the $22bn 30yr auction today.

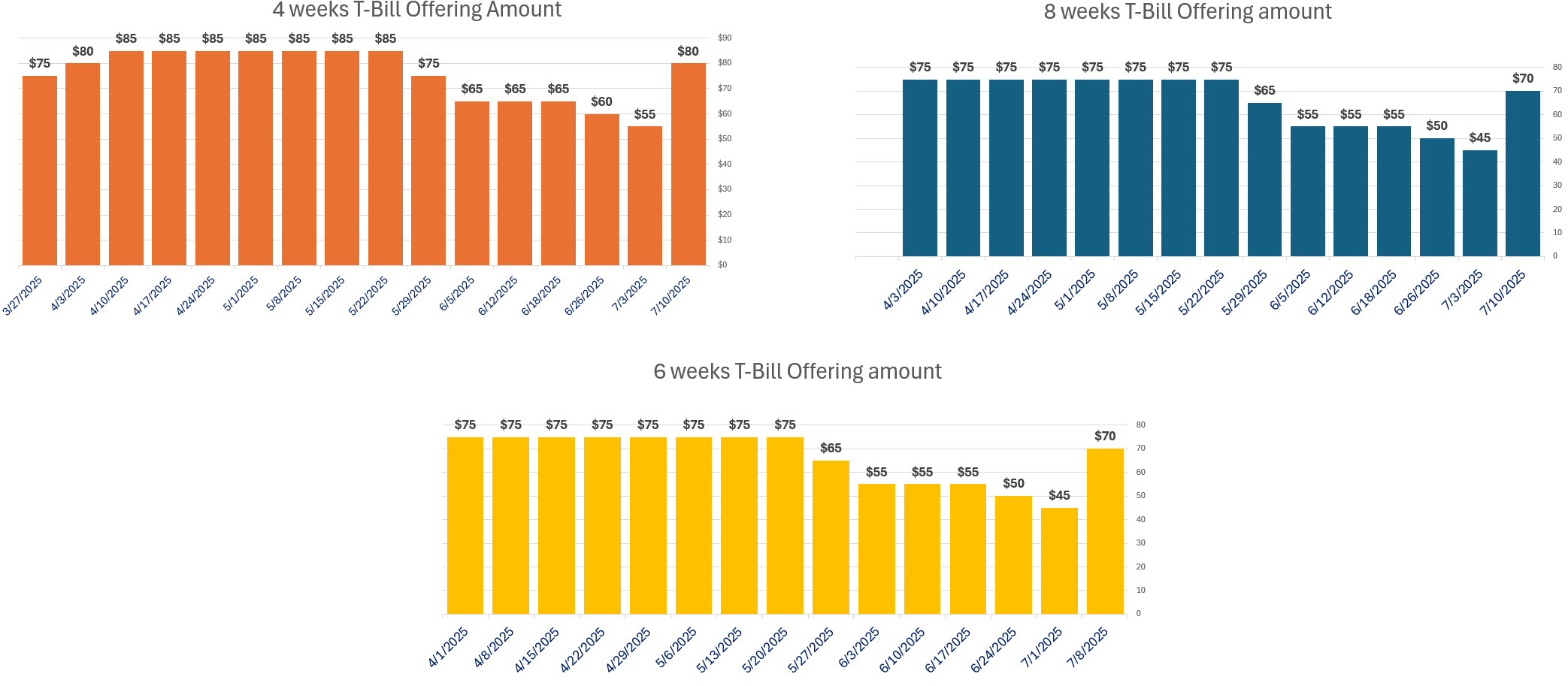

The US Treasury is already increasing the size of the T-bill auction by $25bn for the 4, 6 & 8week bills (4 and 8 week today) as the TGA rebuilding starts, taking liquidity out. The Treasury secretary has mentioned numerous times that the increase in stablecoins out standing will support T-bills, but as mentioned by Philip Lane (ECB) yesterday, Stablecoin creation are not adding liquidity, just resulting from money transfer from other assets. We should see widening of the T-Bill-OIS spread.

Lane also re-introduced old discussions about the creation of larger pool of Euro safe assets (necessary for the € to play a greater role), including the SBBS concept of Securitized Sovereign Bonds (Sovereign Bond-Backed Securities).

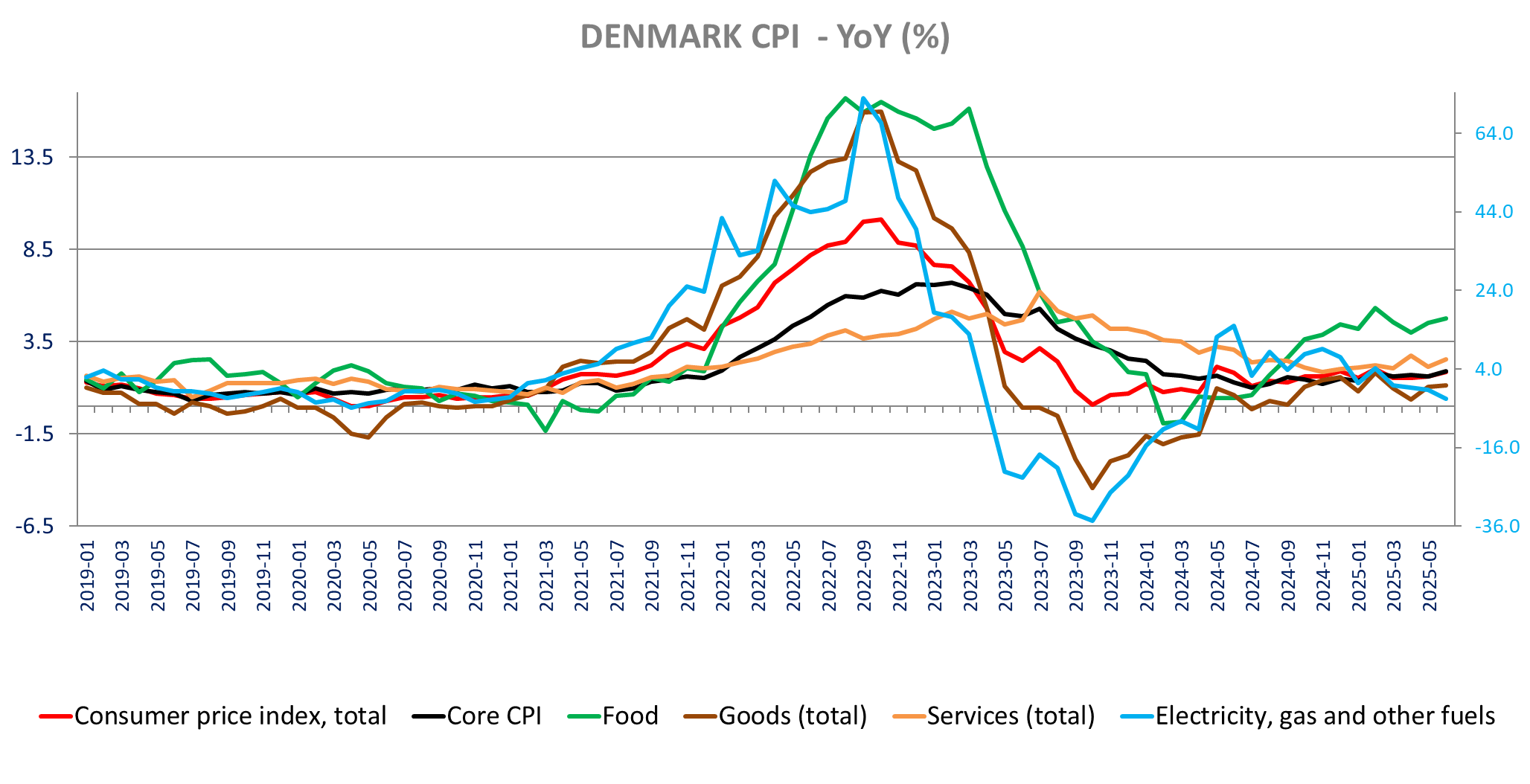

After the higher than expected inflation in Sweden released earlier this week, we have higher inflation in Denmark, and the first increase in core inflation in 4month in Norway.

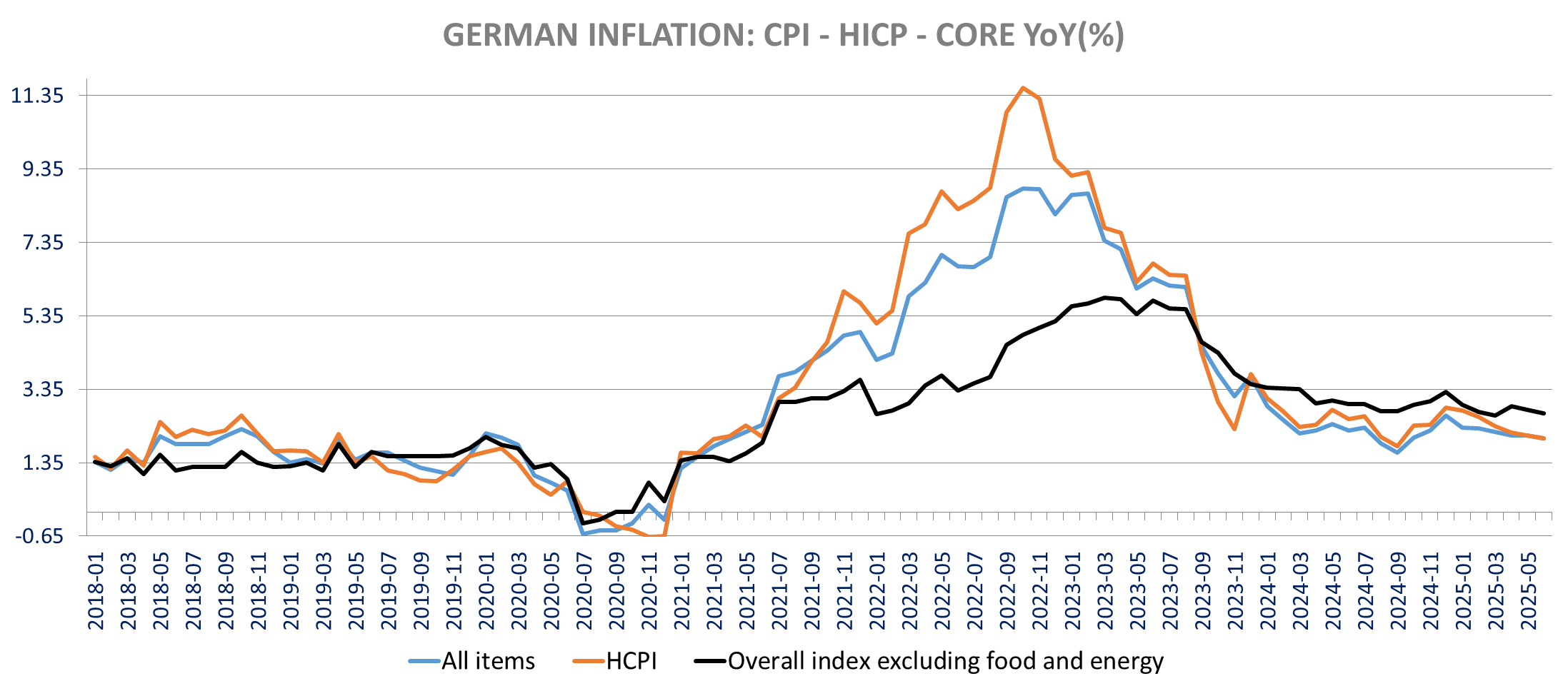

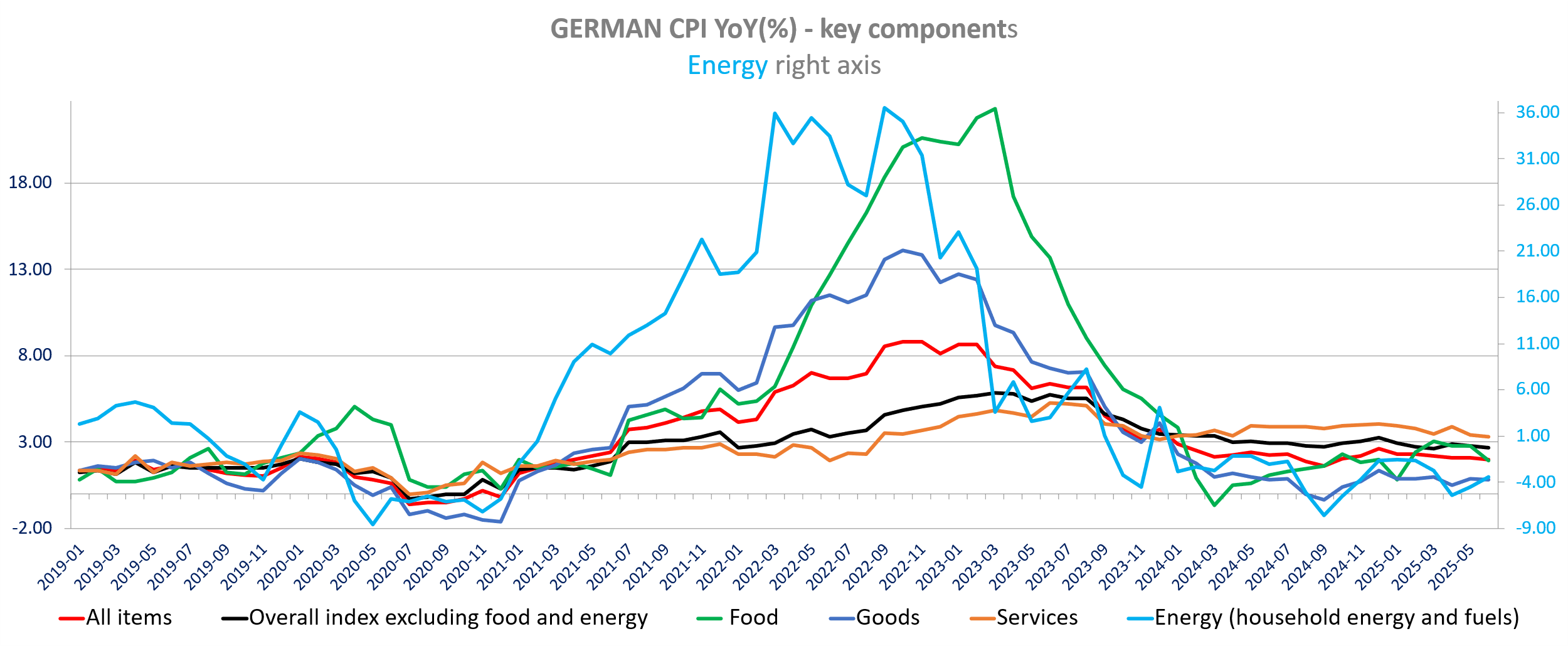

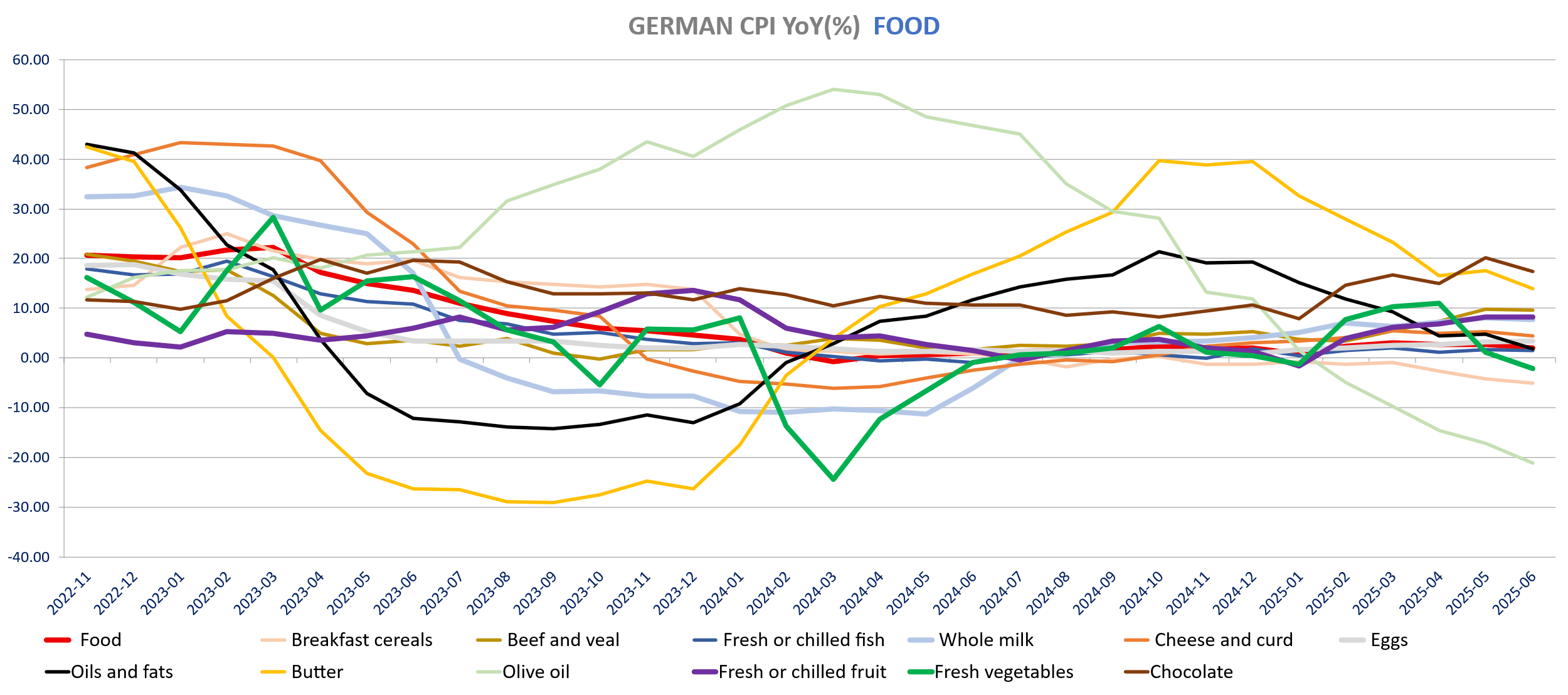

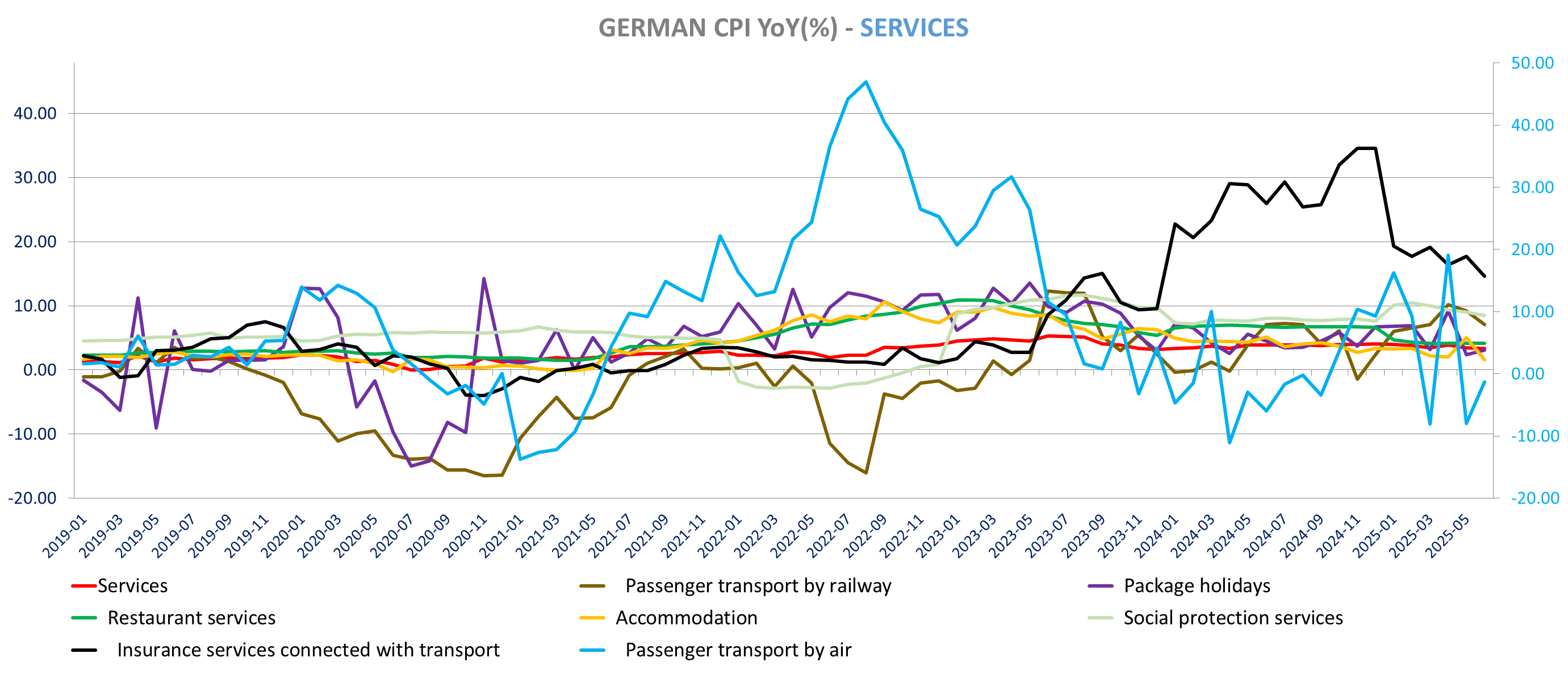

There was no surprise from the release of the German final June CPI, confirming the preliminary estimates and the details aligned with the state level data released at that time. Inflation declined to 2% from 2.1% in May with prices flat month-over-month. The HICP is also down to 2% from 2.1% with prices up 0.1% and the core CPI is slightly lower at 2.7% versus 2.8% yoy in May confirming a 0.2% m/m increase. As reported earlier Goods inflation eased to 0.8% yoy vs 0.9% yoy with energy inflation increased to -3.5% yoy from 4.6%yoy and food inflation down to 2% from 2.8%. Destatis also confirmed services inflation down to 3.3% from 3.4% yoy in May. As noted with the NRW details at the end of June, the decline in services inflation is broad based, up for Accommodation, rail transport, social protection, and insurance (up for air transport, package holiday). The Federal level data also confirmed that he main drag on food inflation came from fresh vegetables, oil & fats and dairy. Meat inflation is slightly up but unlike other European countries beef price inflation eased slightly. The increase in used car inflation noted for North Rhine Westphalia level is also confirmed at the federal level.

For Denmark, the CPI increased in June to 1.9% yoy from 1.6% (CPI) with prices up 0.25% m/m, with both the annual and monthly rate at their highest since February. Core inflation also increased to 1.9% from 1.6% in May with higher services inflation (2.55% yoy bs 2.1% yoy in May). The HICP rose to 1.8% from 1.5%. Energy inflation is down on lower electricity/gas prices, food inflation increased with higher meat prices (especially beef & veal inflation surging to 20.5% yoy from 15.5% yoy , up +5.6% m/m), but non-alcoholic beverages inflation declined despite higher inflation for cocoa beverages and coffee. Goods inflation increased nevertheless with higher non-energy, non-food goods inflation.

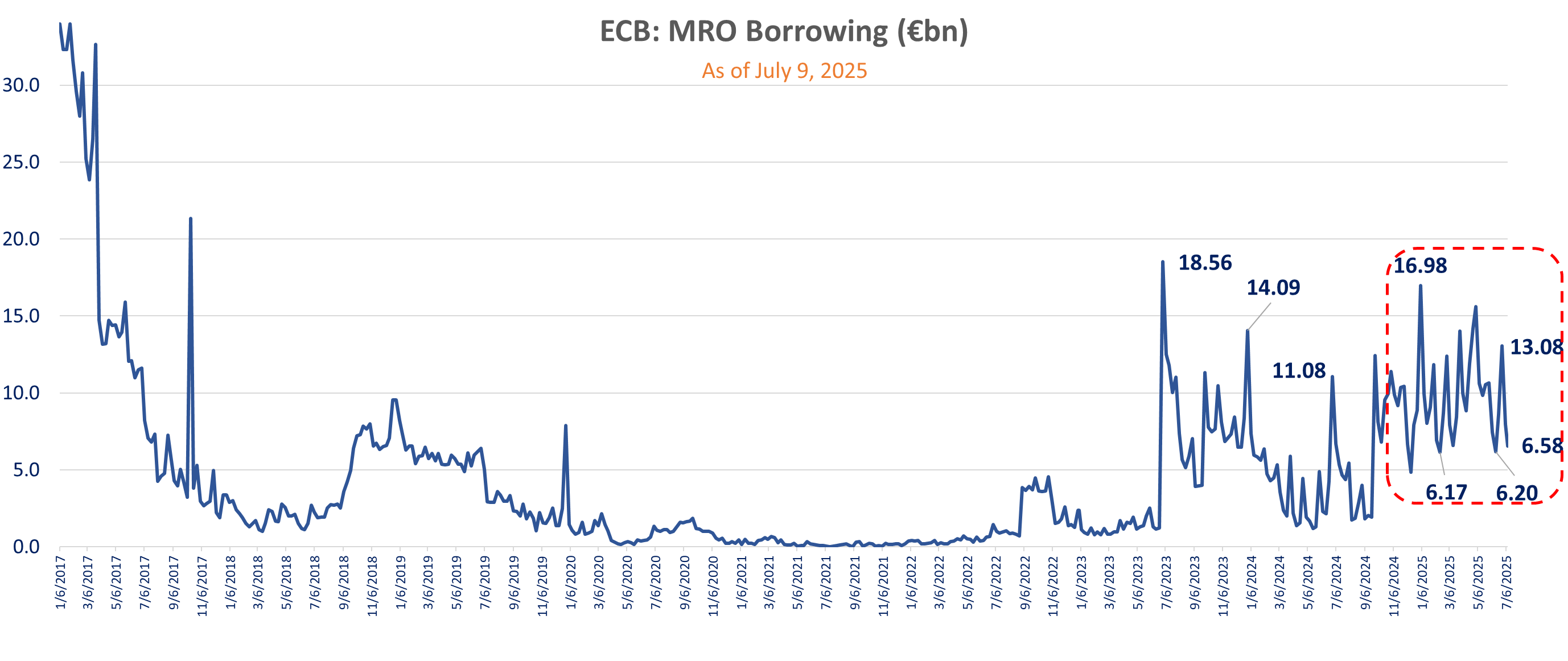

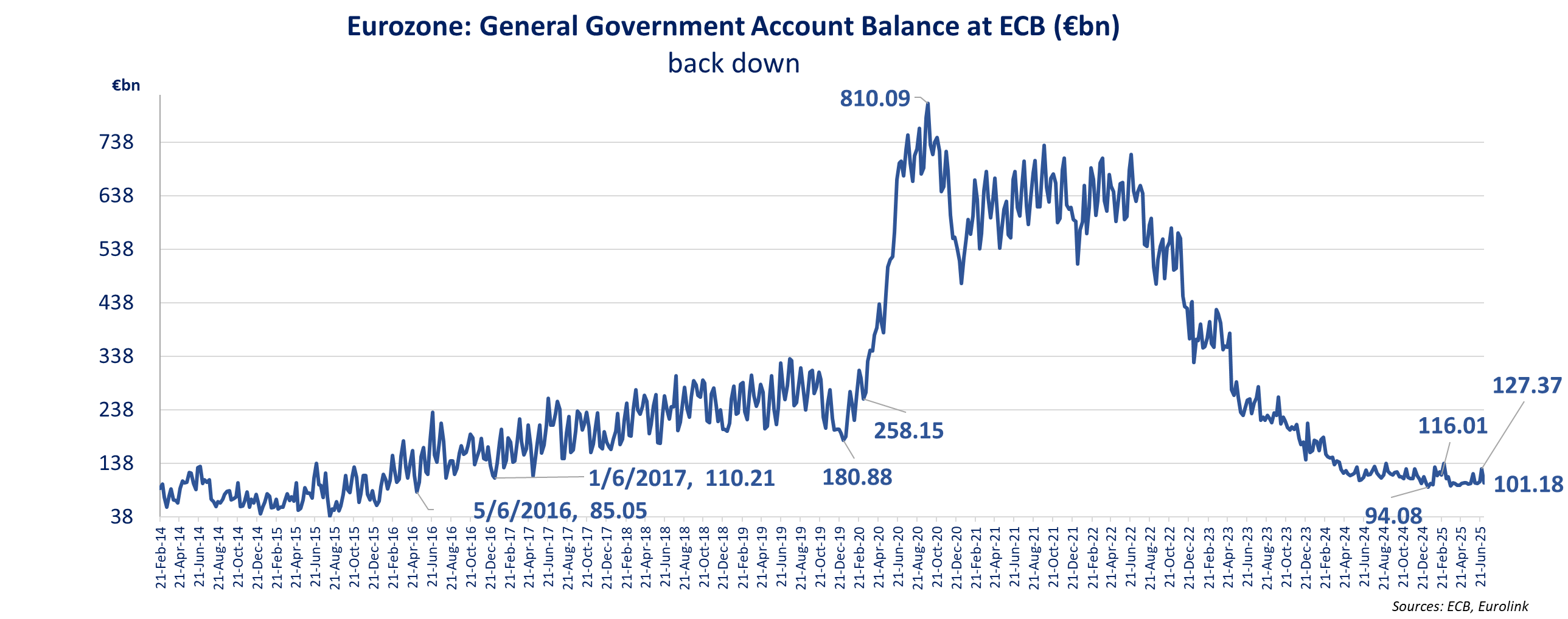

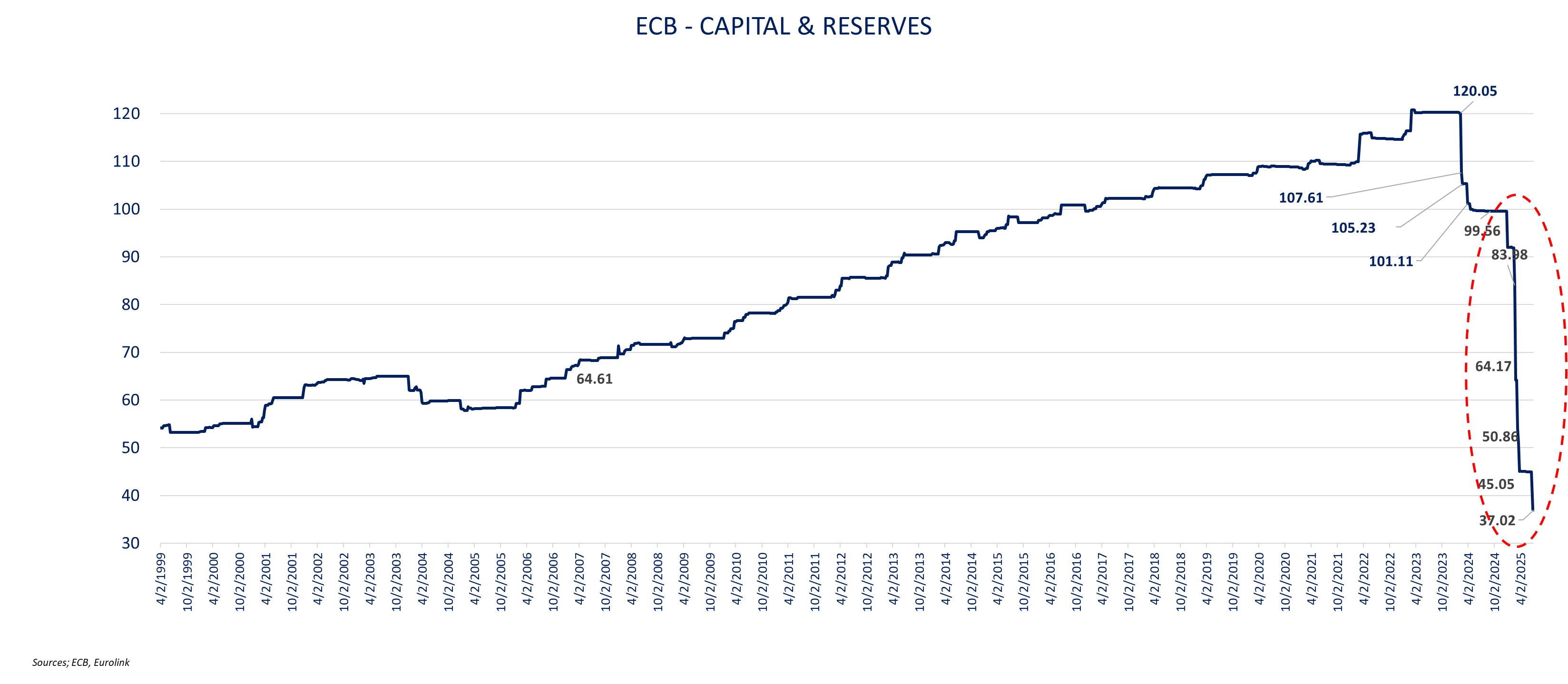

The latest ECB Balance sheet release continues to show little signs of stress with Lower MRO borrowing (down again yesterday), little take for the $ weekly offering and lower liabilities in € to non-euro resident. The release includes the quarterly adjustment due to the stronger € (valued at 1.1720). The Overall balance sheet declined by -€90.85bn w/w with -€59.2bn devaluation of assets (notable 29.7bn in gold reserves and -26.97bn in FX). Without adjustment the balance sheet would have declined by €31.6bn on lower MRO and securities holdings (-€25.2bn). Despite that the drop in the General Government Account (-€26.2bn) meant that excess liquidity declined by only €4.97bn w/w.

On the companies’ front: Barry Callebaut’s group volume dropped more than expected at - 9.5% in Q3, vs consensus of -5.5% as customers continues to adapt to high cocoa prices and U.S. tariff uncertainty. Legrand announce the signing of an agreement on the acquisition by Legrand of Cogelec, specializing in access control in buildings, with revenue of €74 million in 2024. Südzucker revenue and profit were weaker than expected. The decline is primarily due to a significant drop in sugar prices and a decrease in export volumes as well. The BMW Group reported higher sales year-on-year in the second quarter: Between April and June, deliveries of BMW, MINI and Rolls-Royce vehicles increased by +0.4% to 621,271 units driven by Europe (+10) and Germany (+7.8%) offset by Asia (-10%), China (-13.7%) while the Americas and USA were slightly up. The UK homebuilder Vistry continues to hope that further rate cuts will provide additional stimulus to Open Market sales in the second half. More details on equities here

Interesting comments from Philip Lane yesterday on the need for more Euro “safe bonds” – reviewing earlier concepts – and on Stablecoins.

SBBS (Sovereign Bond-Backed Securities.)

In his comments yesterday Lane discusses how to expand the pool of Safe assets in Europe.

Besides agreements on general common issuance or issuance of subset of countries (coalition of the willing) Lane mentions two concepts expressed before:

ON STABLE COIN

Also, within his comments, he said – as I mentioned earlier regarding the US /Bessent Comments on Stablecoin:

The supply of stablecoins is not elastic (unlike central bank money) since their issuance is driven by upfront purchases by customers. In contrast, central bank money can be issued elastically (especially during a crisis) by lending to counterparties or through open market operations.

Additionally, one-to-one parity between the value of a stablecoin and the value of a currency cannot be guaranteed under all circumstances, such that stablecoins do not protect the singleness of money.”

INCREASE IN T-BILL BORROWING this week

TGA Rebuilding in the front-end T-Bill issuance increased this week: T-Bills 4 weeks (tomorrow), 6 weeks (yesterday) and 8 weeks (tomorrow) auction’ size increased by + $25bn each compared to the previous auction…

The ECB balance sheet update as of July 4, 2025, includes the quarterly adjustments, impacting mostly Gold and FX reserves (euro appreciations vs other currencies and lower gold prices in Euro terms down), the securities holdings and the other assets.

Total assets are down -90.85bn w/w with -31.61bn decline pre-revaluation and a -59.24bn revaluation.

On the liabilities’ side, most of the revaluation is reflected in the adjustment line (item 11) down -€44.52bn, the counterpart of the IMF SDR (-€8.205bn) and other liabilities (item 10) down -€13.55bn w/w including -€5.755bn due to revaluation

It also impacted marginally the item 6 (liabilities to non-euro area residents denominated in euro down -€6.61bn w/w out of which -€6.57bn before adjustment.

The Government General Account, largely unaffected by the quarterly adjustment, declined sharply, down -€26.2bn to €101.2bn reversing most of the previous week’s increase.

Overall, despite the sharp decline in total assets, excess liquidity only declined -€4.97bn w/w and base money by -€7.02bn w/w.

The ECB capital & reserves remained at ~€37bn a in the previous week (when they declined from €45bn)

The final June German CPI confirms the preliminary data. Inflation declined to 2% from 2.1% in May with prices flat month-over-month. The HICP is also down to 2% from 2.1% with prices up 0.1% and the core CPI is slightly lower at 2.7% versus 2.8% yoy in May confirming a 0.2% m/m increase. As reported earlier Goods inflation eased to 0.8% yoy vs 0.9% yoy with energy inflation increased to -3.5% yoy from 4.6%yoy and food inflation down to 2% from 2.8%. Destatis also confirmed services inflation down to 3.3% from 3.4% yoy in May. As noted with the NRW details at the end of June, the decline in services inflation is broad based, up for Accommodation, rail transport, social protection, and insurance (up for air transport, package holiday). The Federal level data also confirmed that he main drag on food inflation came from fresh vegetables oil & fats and dairy. Meat inflation is slightly up but unlike other European countries beef price inflation eased slightly. The increase in used car inflation noted for North Rhine Westphalia level is also confirmed at the federal level. Destatis release

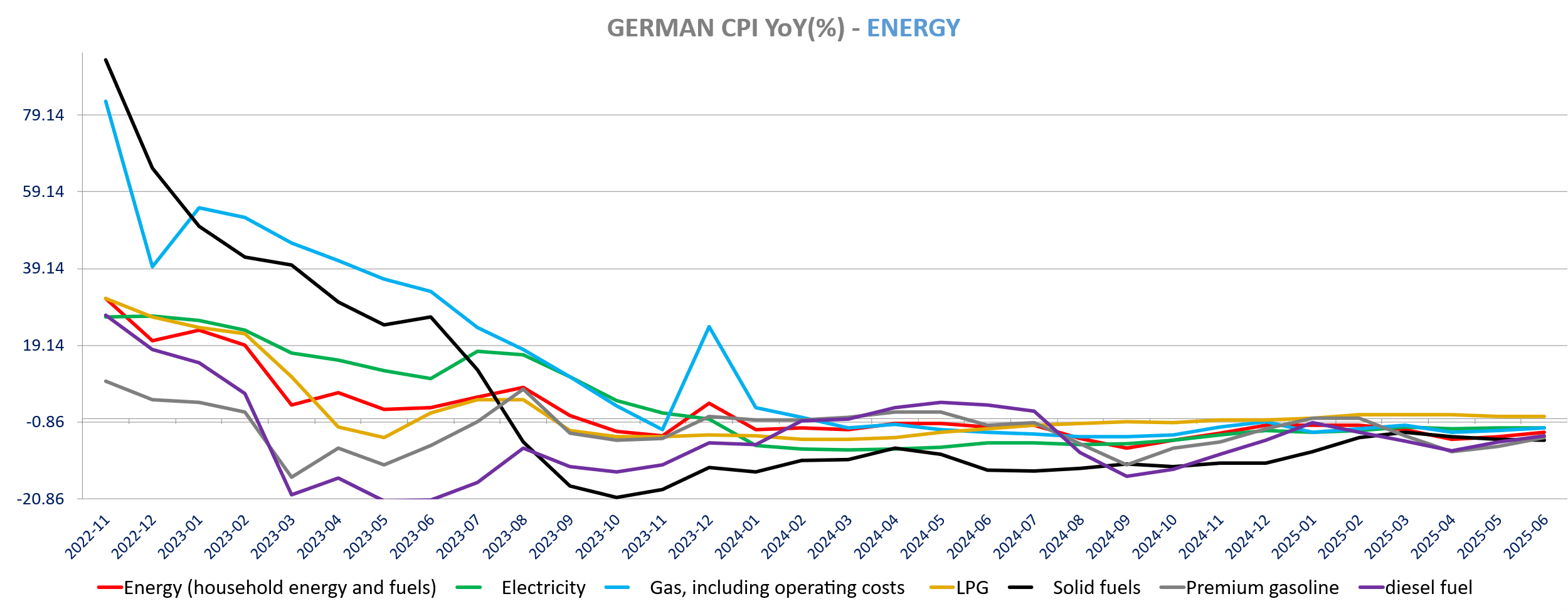

Energy inflation increased to -3.5% yoy from -4.6% due mainly to higher liquid fuel prices inflation (gasoline at -4.8% vs -7.2%) buy inflation is also up for has (-2.4% vs -2.9%) and marginally for electricity (2.43% vs 2.35%).

Food inflation declined to 2% from 2.8% yoy in May dragged down by lower fresh vegetables inflation (-2.2% yoy vs +1.15%, down -4.2% m/m) and oil & fats (1.85% vs 4.7% yoy) with decline in inflation for olive oil (-21.1% yoy vs -17.2%) and butter (13.9% vs 17.6%). Meat inflation is up only marginally to 2.2% from 2.1%, but at least for Germany, Beef &veal inflation is down slightly (9.7% vs 9.8%). Fresh fruit inflation is stable at 8.2% and we see lower inflation for whole milk, fresh fish. Eggs inflation slightly higher (3.4% vs 3.25%)

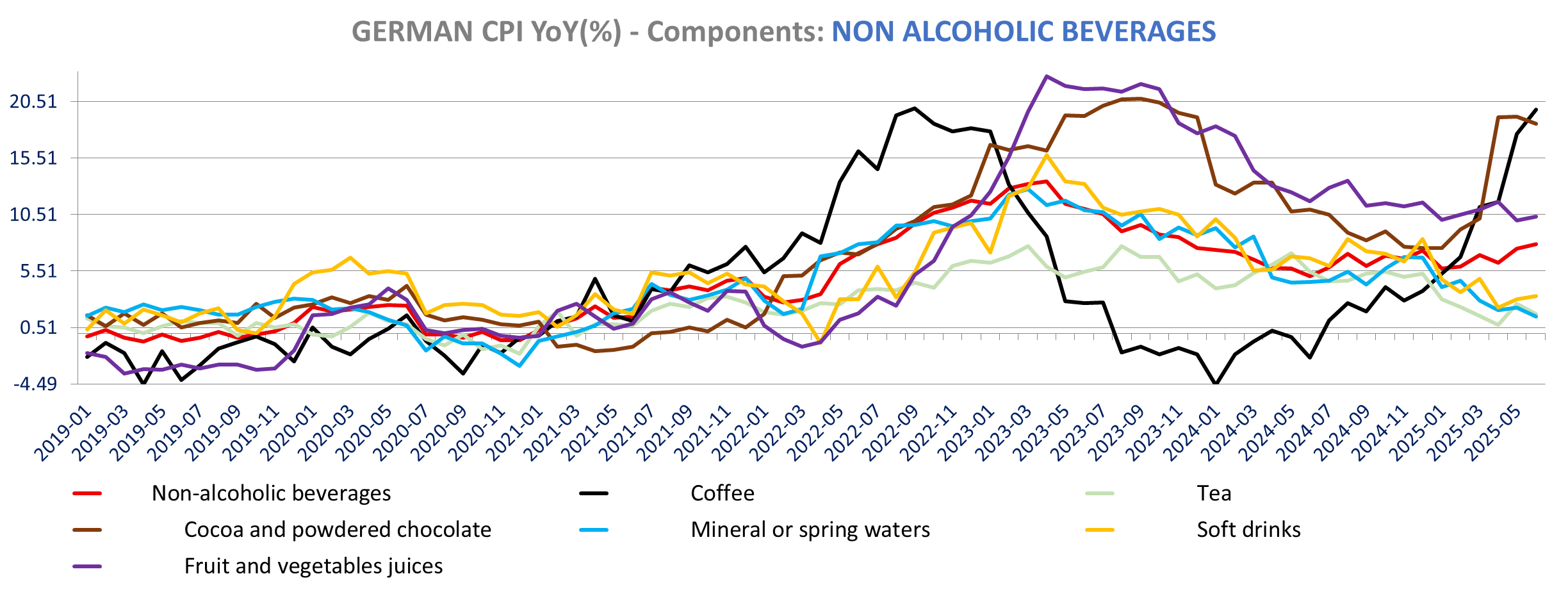

German non-alcoholic beverages inflation rose in June to 7.9% yoy from 7.5% yoy in May as coffee inflation increased further (19.8% vs 17.6%) along Juices (10.3% vs 10%). Cocoa based drinks inflation declined (8.55% vs 19.15%) along with soft drinks and mineral water inflation.

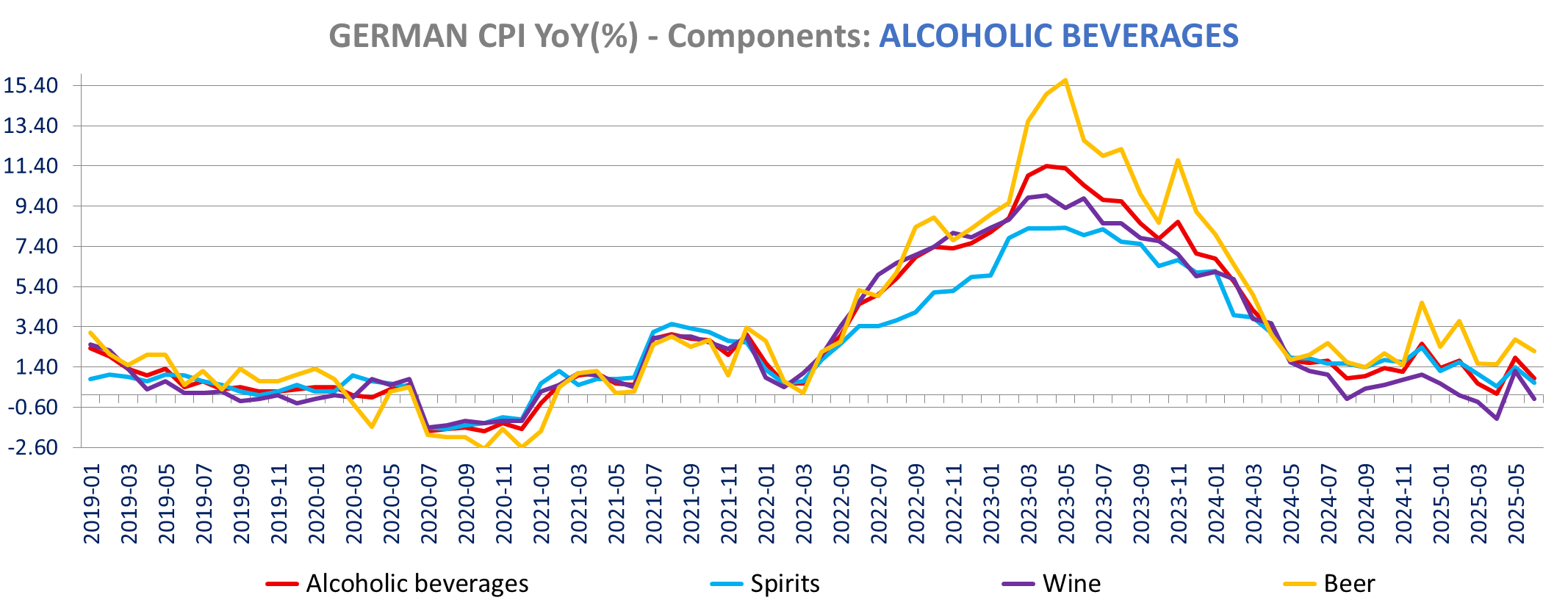

For alcoholic beverages, inflation is down to 0.8% yoy in Jue from 1.8% in May, declining most for wine, but also down for beer and spirit.

Tobacco inflation increased to 6.45% from 5.9%.

Goods inflation decreased to 0.8% yoy from 0.9% (-0.2% m/m with consumer goods inflation down to 0.5% from 0.7% yoy in May. For non-food, non-energy goods we saw a decline in clothing inflation (-0.4% vs +0.7%), lower inflation for medical products (2.3% vs 2.4%), tools, appliances. Other aggregates are posting higher inflation, up for furniture, household textiles, autos and tires. New car inflation is marginally down (2.5% vs 2.6%) but used cars inflation Increased again, now at 7.4% yoy up from 7%.

Services’ inflation fell in June to 3.3% from 3.4% with prices up 0.3% m/m. Comparison level were neutral in June and will remain neutral in July (0.9% m/m in July 2024 in line with 10yr average). The decrease in services’ inflation is relatively broad-based as picked up from the state level preliminary data released June 30. We saw increase in inflation for air transport and package holiday, but inflation declined for Accommodation (1.6% vs 5.1%), social protection (8.1% vs 9.35%), Motor vehicle Insurances (15.7% vs 19.1%), railways transport (7.1% vs 9.2%), cold rent (2% vs 2.1%) … Restaurant inflation was stable at 4.15%.

Detailed table

DENMARK INFLATION (June Final)

Denmark inflation increased in June to 1.9% yoy from 1.6% (CPI) with prices up 0.25% m/m, with both the annual and monthly rate at their highest since February. Core inflation also increased to 1.9% from 1.6% in May with higher services inflation (2.55% yoy bs 2.1% yoy in May). The HICP rose to 1.8% from 1.5%. Energy inflation is down on lower electricity/gas prices, food inflation increased with higher meat prices, but non-alcoholic beverages inflation declined despite higher inflation for cocoa beverages and coffee. Goods inflation increased nevertheless with higher non-energy, non-food goods inflation.

Energy inflation fell to -3.5% yoy in June from -1.3% the previous month (-1.9% m/m) with lower electricity (-3.8% m/m to -8.5% yoy from -4% yoy) and gas (-0.7% m/m to -14.1% from -11.5% yoy) inflation. Liquid fuel inflation increased to -1.1% yoy from -2.1% yoy (+1.2% m/m).

Food inflation increased to 4.8% from 4.5% with, as seen in most countries, higher meat price inflation (2.8% m/m to 6% from 4.3% yoy) as beef & veal inflation surged to 20.5% yoy from 15.5% yoy (+5.6% m/m). Cheese inflation also rose to 8.1% from 7.9% but eggs and whole milk inflation fell. Fresh fruit inflation increased to 4.8% from 3.4% (1.3% m/m) while fresh vegetables inflation decreased to 3.6% from 4.55%. Oil & fats inflation increased to 5.9% yoy from 5.3% (3.6% m/m) with butter prices up 5.8% m/m to 14.4% yoy (13.25% yoy in May).

Non-alcoholic beverages inflation decreased in June to 8.2% yoy from 9.7% yoy in May (0.2% m/m) despite higher inflation for coffee (29.2% vs 26.2%) and cocoa based beverages (21.2% vs 16.8%) as we saw a sharp decline in soft drinks inflation to -4.4% yoy from +0.9% yoy (-3.6% m/m), mineral water inflation (0.5% yoy vs 6.8% yoy , -3.3% m/m vs +2.8% m/m in June 2024). Tea and juice inflation increased.

Alcoholic beverages inflation is less negative at -0.4% yoy in June versus -1.7% yoy in May, increasing most for beer and wine.

Goods inflation still increased to 1.1% from 1% (1.14% from 1.049%) with higher inflation for furniture, house textiles, appliances, garden furniture, new cars (-3.6% vs -4.4%), pharmaceuticals products (3.45% yoy up from 0.5% yoy) and medical products (3.5% vs 2.2%). Utensils and footwear (-2.3% vs -1.4%) inflation fell along clothing (-0.7% vs -0.6%), used cars.

For services the increase in inflation to 2.55% from 2.1% was due to higher accommodations (6.45% vs 3.3%) with higher holiday park/camping (12.15% vs 4.45%), air transport (7.4% vs -0.9%), package holiday (4.55% vs -4.3%). Restaurants inflation increased more marginally to 0.2% yoy from 9%. Recreational & sporting services inflation is up 3.5% from 3.3% and cultural services inflation rose to 3.4% from 2.8%. Insurance, rent inflation was stable,

Detailed table

|

|

Thursday, July 10, 2025 | ||

|

BMW | |||

|

EUR |

82.62 |

+0.78% | |

|

BMW |

The BMW Group reported higher sales year-on-year in the second quarter: Between April and June, deliveries of BMW, MINI and Rolls-Royce vehicles increased by +0.4% to 621,271 units driven by Europe (+10) and Germany (+7.8%) offset by Asia (-10%), China (-13.7%) while the Americas and USA were slightly up. In the first half of the year, the company delivered a total of 1,207,388 vehicles (0.5%). Electrified vehicles saw significant sales growth compared to the previous year. With 318,949 fully electric and plug-in hybrid vehicles delivered to customers, the BMW Group grew its sales by +18.5% in the first half of 2025. New orders across all drive technologies developed positively in the first six months, showing significant year-on-year growth. | ||

|

|

|

|

|

|

BC |

Brunello Cucinelli SpA | ||

|

EUR |

107.90 |

+0.70% |

|

|

BC |

Preliminary Revenue figures as of 30th June 2025 later today | ||

|

|

|

|

|

|

LR | |||

|

EUR |

114.40 |

+0.57% | |

|

LR |

Legrand and Cogelec announce the signing of an agreement on the acquisition by Legrand of Cogelec, specializing in access control in buildings, with revenue of €74 million in 2024. The contemplated transaction values Cogelec at | ||

|

|

|

|

|

|

DCC |

DCC PUBLIC LIMITED COMPANY | ||

|

GBp |

4786.00 |

+0.42% | |

|

DCC |

AGM Trading statement: In the seasonally less significant first quarter of the year, Group operating profit on a continuing basis was in line with expectations and modestly behind the prior year. DCC Energy traded in line with expectations and modestly below the prior year while DCC Technology traded in line with the prior year. Outlook DCC continues to expect that the year ending 31 March 2026 will be a year of good operating profit growth on a continuing basis, strategic progress and continued development activity. | ||

|

|

|

|

|

|

FHZN |

Flughafen Zuerich AG | ||

|

CHF |

226.00 |

-0.44% |

|

|

FHZN |

June traffic later today | ||

|

|

|

|

|

|

SHA0 |

Schaeffler AG | ||

|

EUR |

4.82 |

-1.11% |

|

|

SHA0 |

Pre-close conference call Q2 2025 after market close | ||

|

|

|

|

|

|

SZU | |||

|

EUR |

10.91 |

-1.53% |

SuedZucker Release |

|

SZU |

Suedzucker revenues fell during Q1 by 15% to €2153m (consensus €2325m). They declined in the sugar, special products, CropEnergies and starch segments, but increased in the fruit segment. Group EBITDA decreased significantly to € 96m (previous year: 230) vs consensus €. The consolidated group operating result dropped in the first quarter 2025/26 significantly to €22 (previous year: 155) consensus €44m. The substantial decreases in the sugar, special products, | ||

|

|

|

|

|

|

VTY | |||

|

GBp |

611.40 |

-2.33% | |

|

VTY |

Group H1 profits in line with expectations, with adjusted operating profit expected to be c. £125m (H1 24: £161.8m1), and adjusted profit before tax c. £80m (H1 24: £120.7m1). Net debt as of 30 June 2025 is better than management expectations at c. £295m and lower than last year (30 June 2024: £322.0m) despite a £92m higher opening balance as at 31 December 2024. During the first half, the Group delivered c. 6,800 completions (H1 24: 7,792), with c. 73% (H1 24: 76%) Partner Funded and c. 27% (H1 24: 24%) Open Market. The Group's sales rate averaged 1.022 (H1 24: 1.21) with average selling prices remaining firm. Outlook | ||

|

|

|

|

|

|

BARN | |||

|

CHF |

809.00 |

-15.11% | |

|

BARN |

Barry Callebaut group volume dropped more than expected at - 9.5% in Q3, vs consensus of -5.5% as customers continue to adapt to high cocoa prices and U.S. tariff uncertainty. Due to unprecedented market conditions, the Group revises its FY 24/25 volume guidance and now expects a mid-single-digit decrease in Global Chocolate and a double-digit decrease in Global Cocoa. This results in an overall -7% volume decrease (from mid-single digit) and a mid-to high-single digit increase in EBIT (from double digit) recurring in local currencies in FY 24/25. | ||

Versus early hours

SECTOR PERFORMANCE

Versus early hours:

Indices

Versus early hours

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.