Two days ahead of the July 9 tariff deadline, Lutnick and Bessent point to some more time (August 1st) before the implementation of the tariffs level sent by letter to about 15 countries, leaving more time for negotiation. President Trump threat of 10% additional tariffs for BRICS countries, shows that whatever the accord will be, tariffs will still be subject to the president’s utterance. Sector tariffs should also be revealed, Unpredictability by design. It will only encourage the Fed to wait longer.

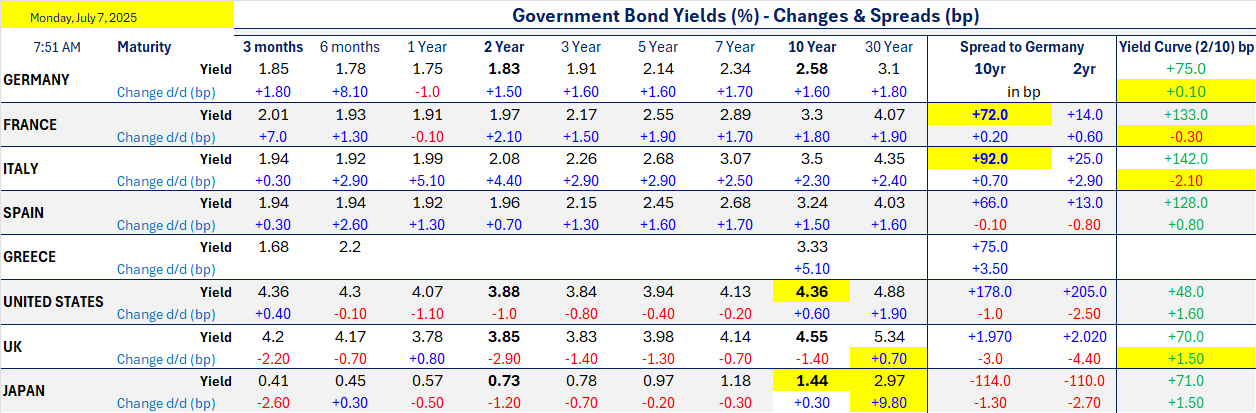

As mentioned Friday the approval of the 5bn debt increase will lead to liquidity draw as the Treasury rebuild the TGA (target of $850bn). US Treasury Secretary Scott Bessent said last Thursday that the rebuilding of the TGA will be done through T-Bill, not expecting to increase issuance of notes and bonds. Bessent expressed the belief that yields will come down with lower inflation as the Fed will end up easing. The SLR change (September) will help absorb some of the issuance and Bessent expects the growth in stable coins to support T-Bills demand, but we still see lower liquidity and reserves. Moreover, the approach of overloading the front-end exposed the US Treasury to higher inflation surprises. It also will undoubtedly incite the administration to increase pressure on the Fed to cut rates. The hope for the debt is that we will move back to a goldilocks environment of low inflation and a OBBB induced growth. The scenario is not impossible but seems unlikely when so many relationships are severely damaged. The latest non-farm-payrolls did show weakening in the private sector labor market.

The DXY is up as we see some pushback in Europe on the € as we near 120 as always, targeting a slower the pace of the parity move. After opening flat European stocks moved higher (after a weak Friday) and bond yields are slightly higher ~ 1.5 to 2bp on the European side along the curve. Rates slightly down in the UK and the front of the US curve. Note some volatility in 30yr JGB with 3 days of significant moves: +9bn today after -8bp Friday.

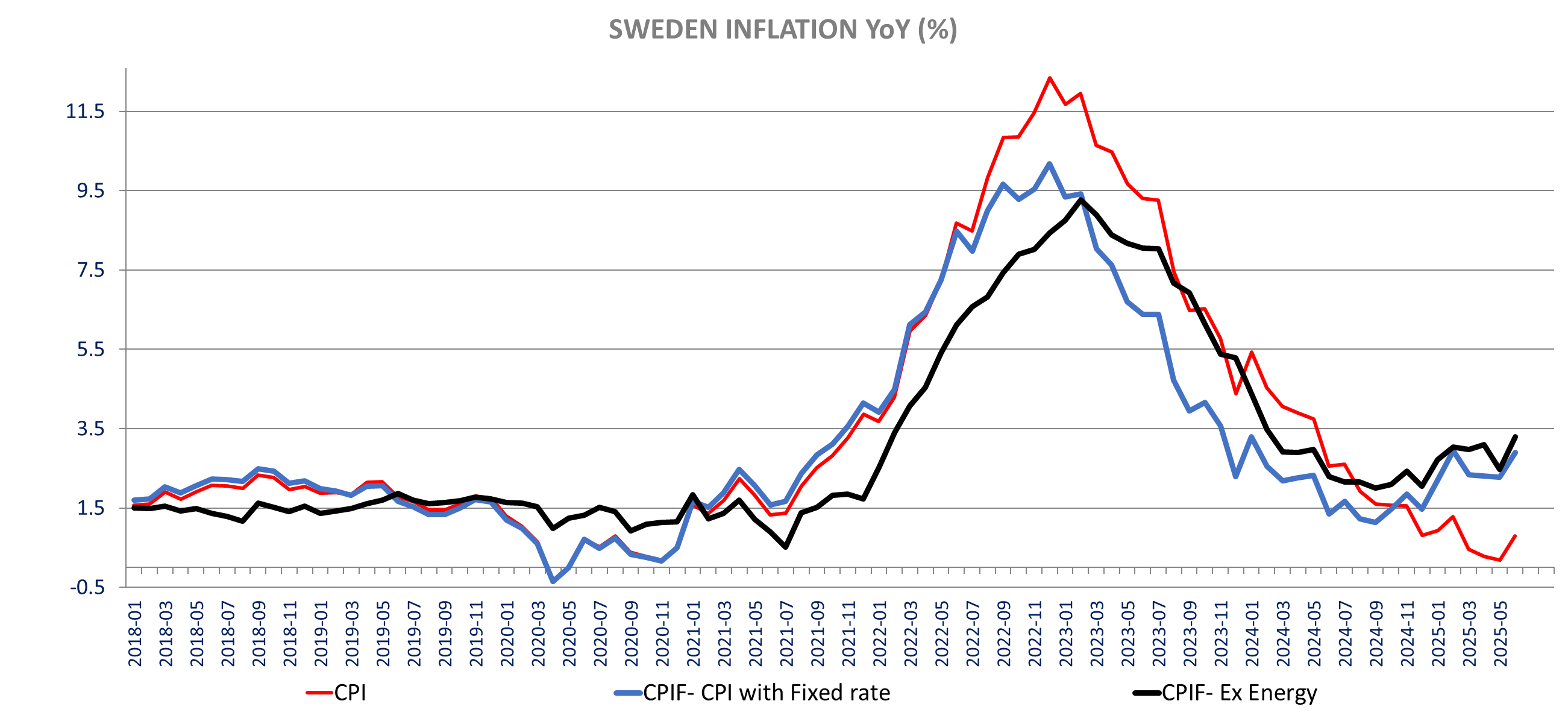

We have a negative surprise on inflation in Sweden, according to SCB preliminary estimates release, The CPI rose to 0.8% yoy from 0.2% yoy in May (+0.5%), the CPIF increased to 2.9% yoy (0.5% m/m) from 2.3% yoy in May, exceeding market expectations of 2.5% yoy / 0.2% m/m. The CPIF excluding energy rose to 3.3% yoy (0.7% m/m) the highest level since February 2024 (2.5% yoy then).

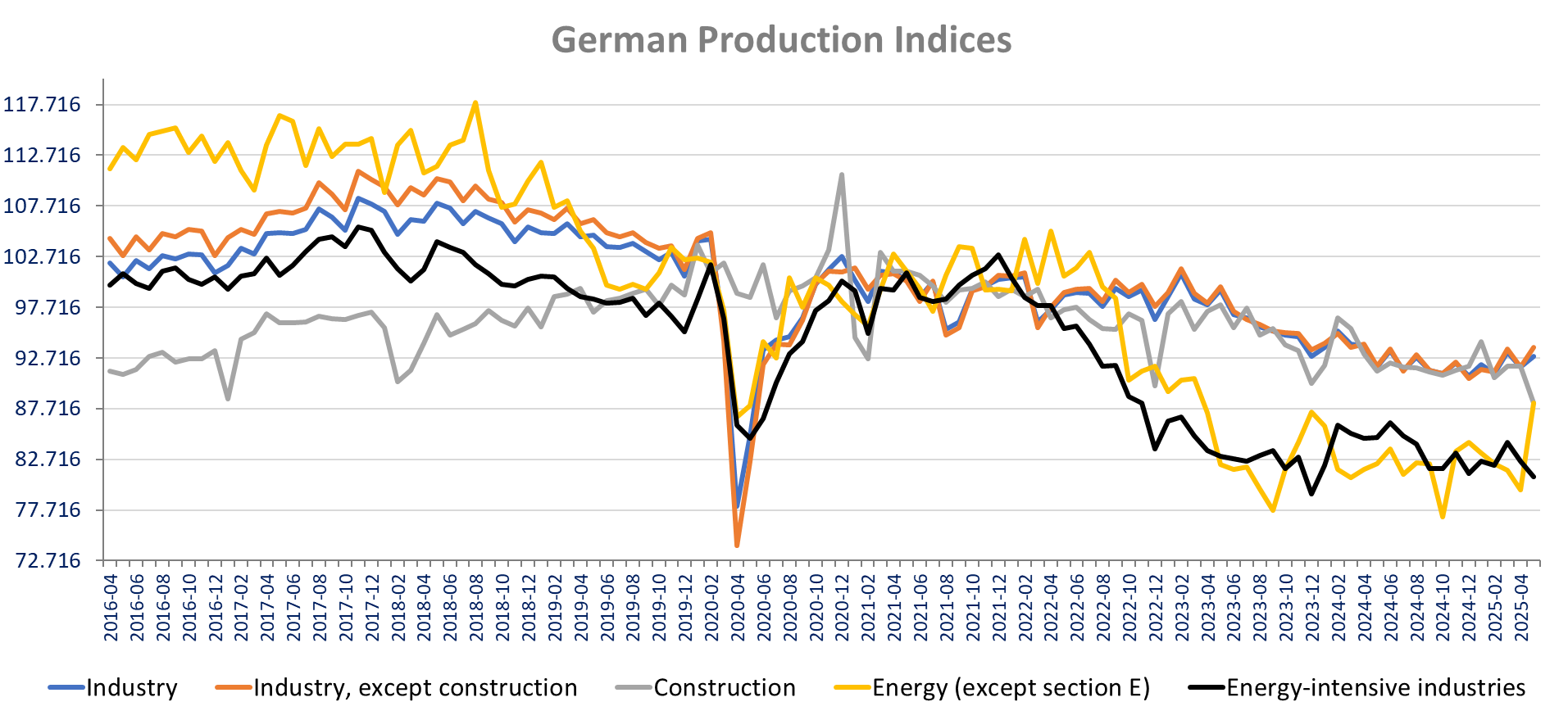

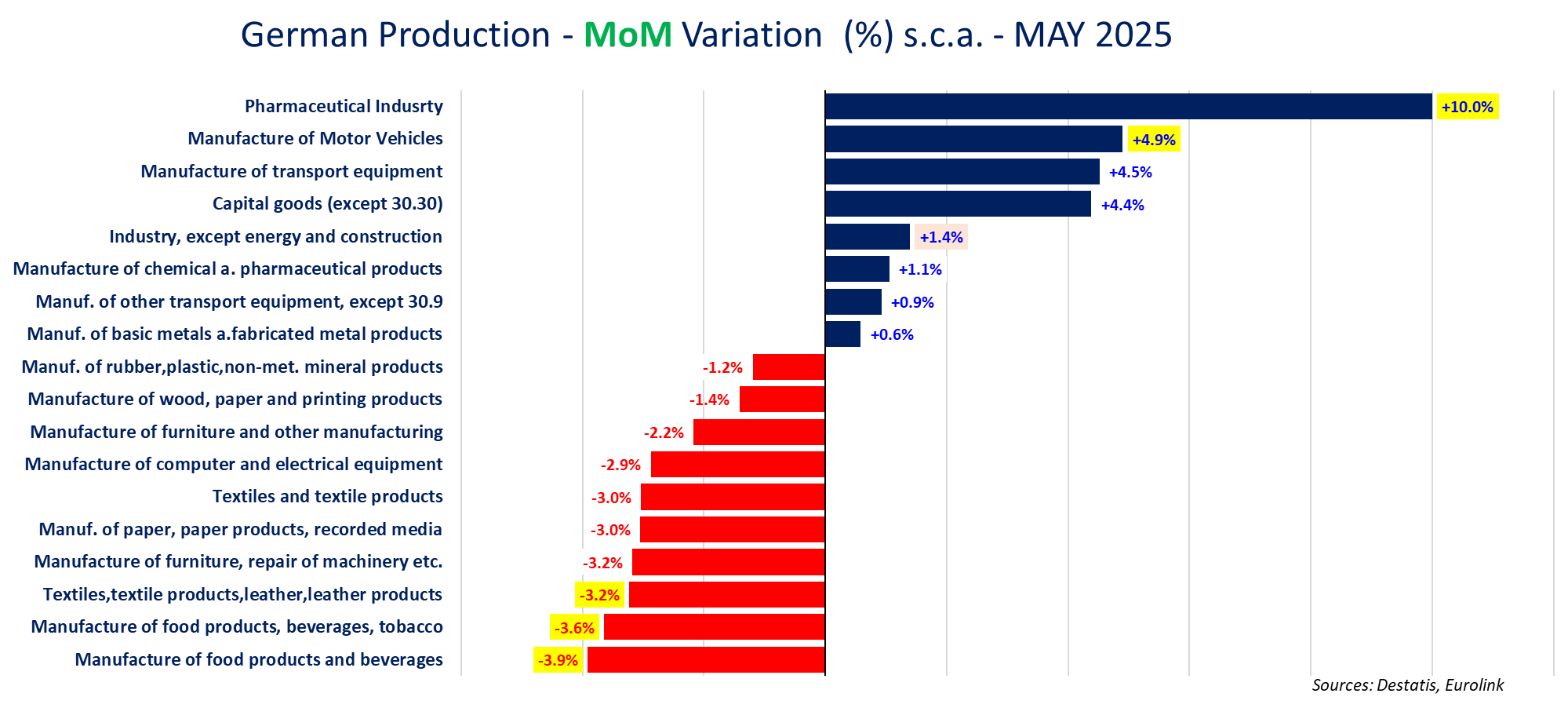

On the economic data front, May German production grew much stronger than expected by economists (even including the slight revision for April to -1.6% m/m from -1.4% m/m). Production increased +1.2% m/m in May versus 0% Expected. Energy production was up +10.8% m/m and construction down -3.9% (weakest in civil engineering, -4.1% m/m) after being flat in April (revised sharply down from +1.4%). When excluding both energy & construction, production increased +1.4% after a negative -1.9% m/m in April (unrevised). The details suggest tariff -delayed-related production increases, with pharmaceuticals up 10% m/m and motor vehicles higher by +4.9% m/m. In contrast we see a sharp decline in Food& beverages production, down -3.9% m/m and textiles -3.0 Furniture and paper/wood product also saw decline in production.

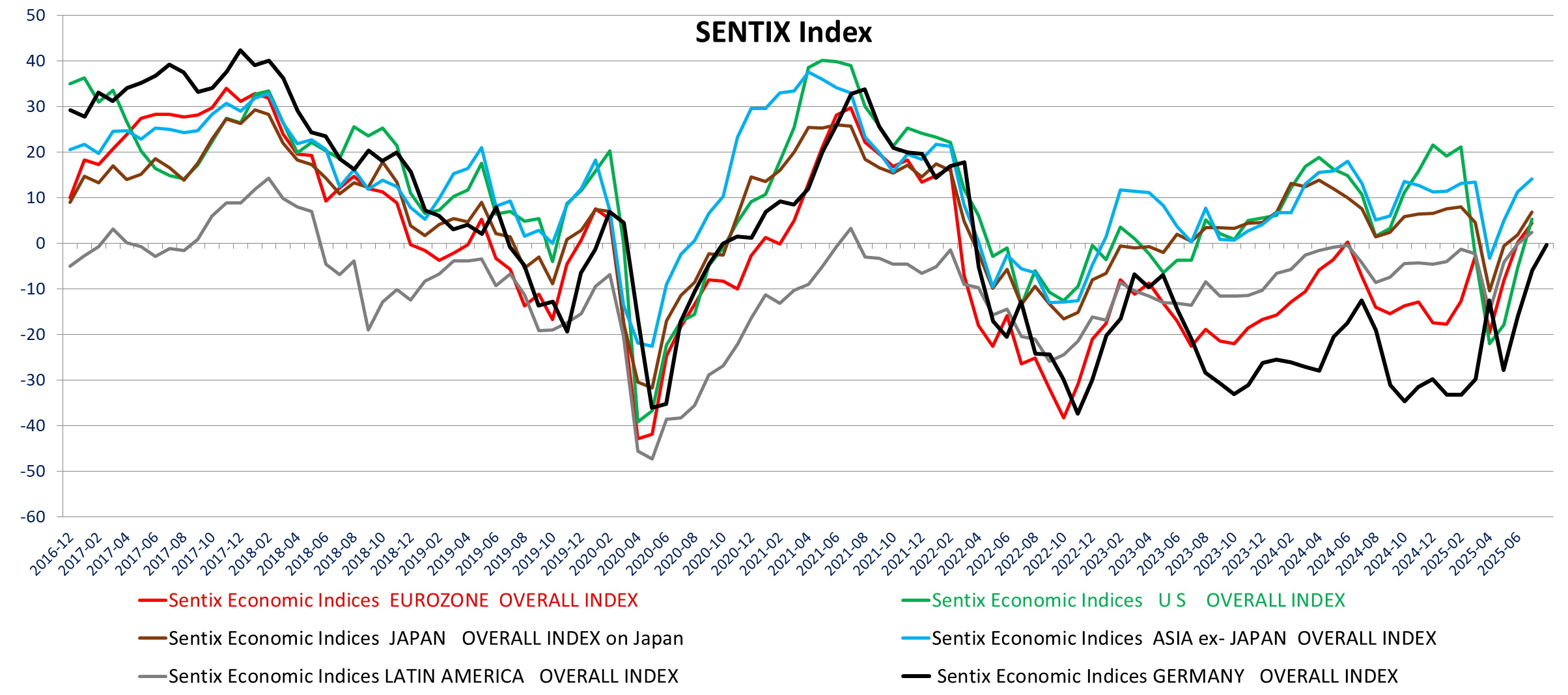

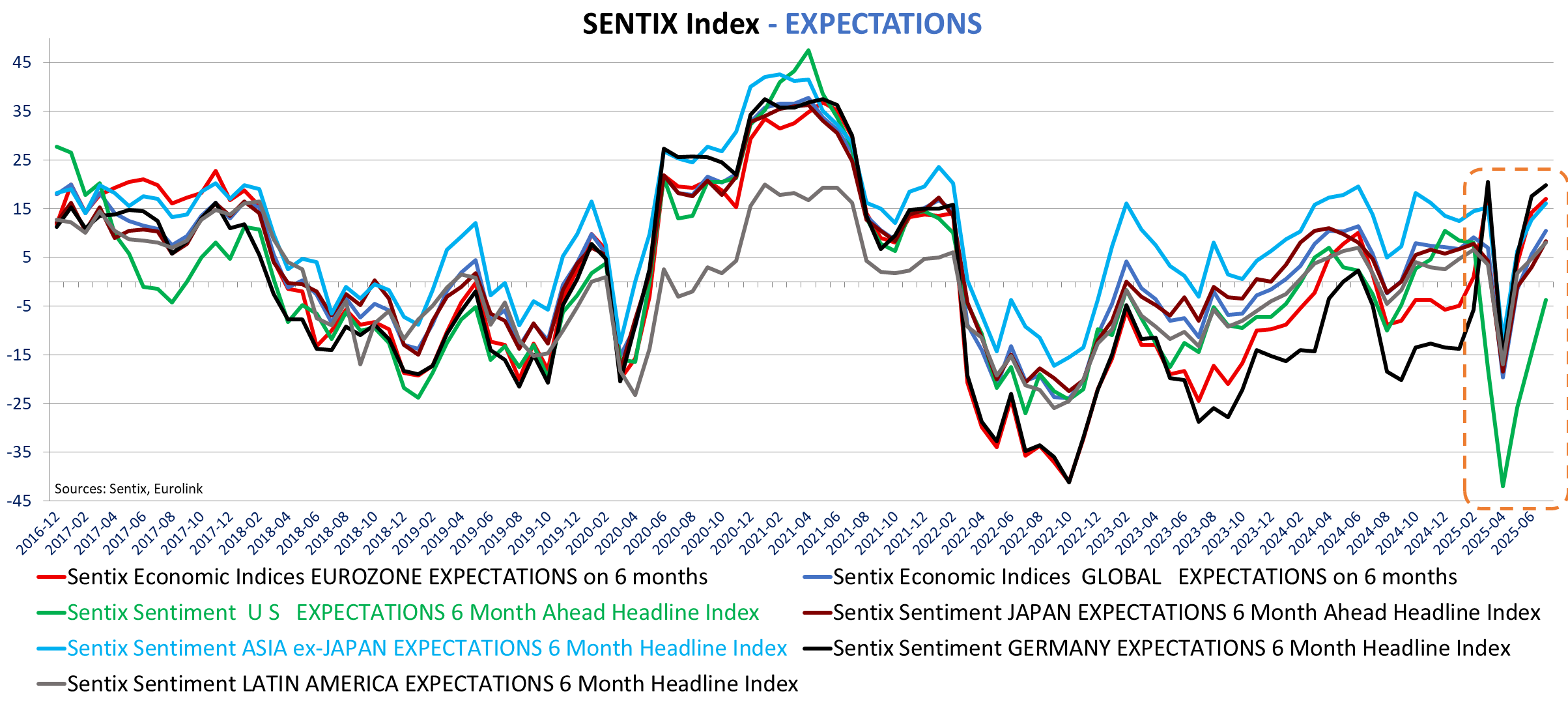

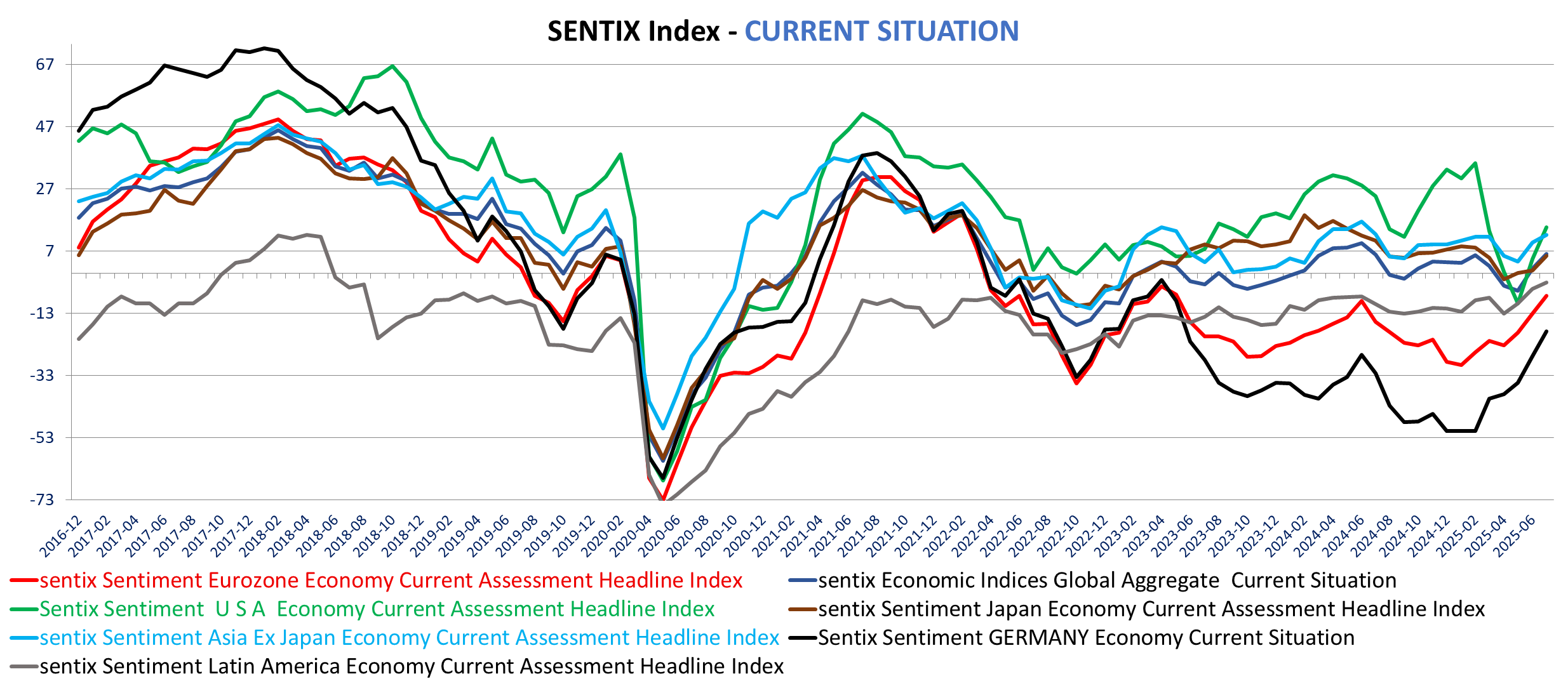

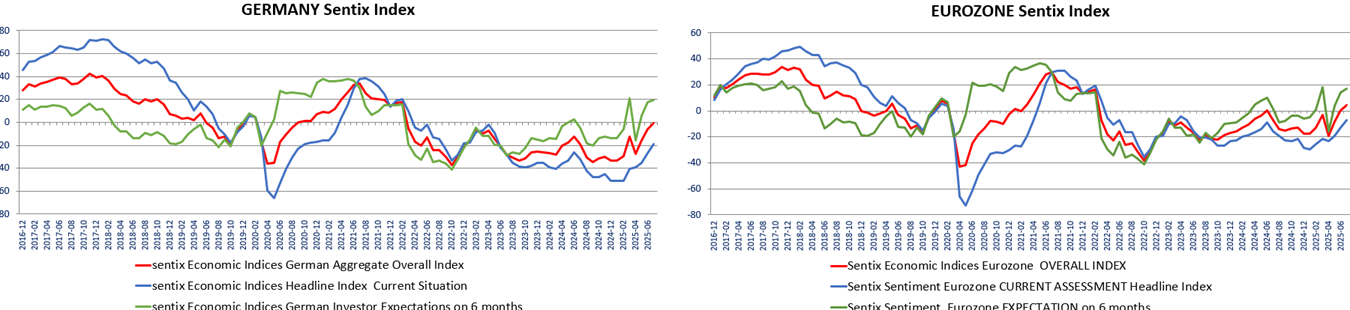

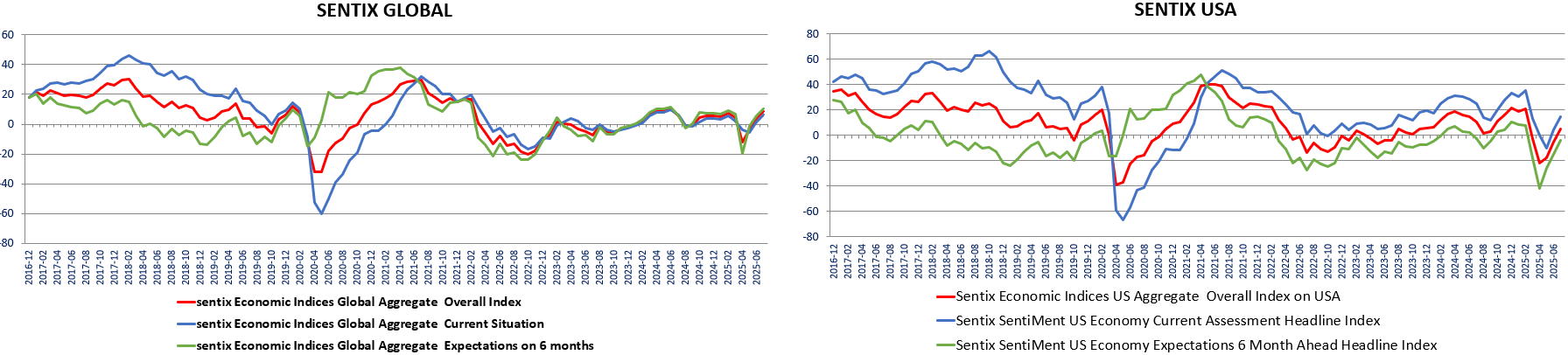

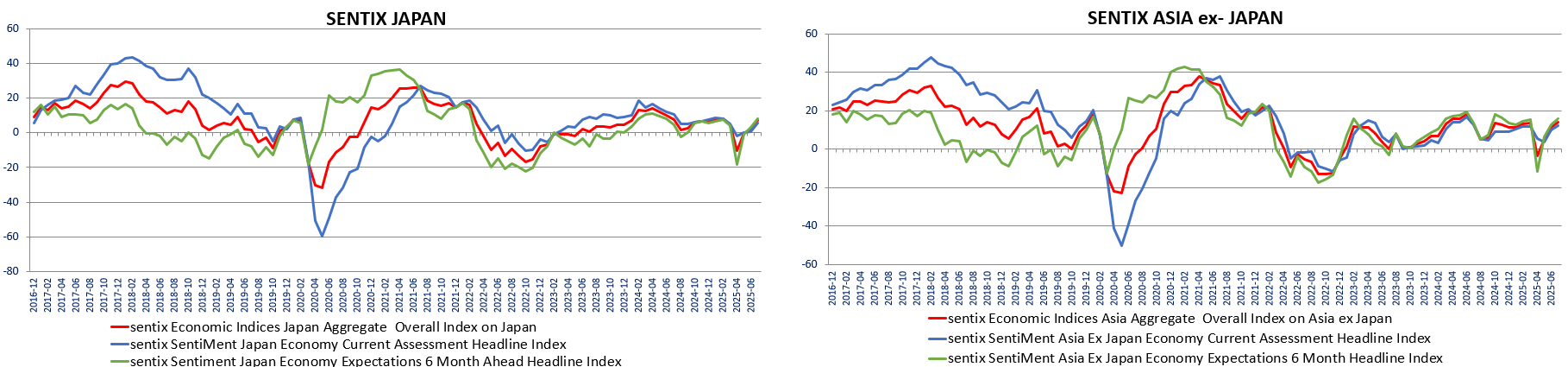

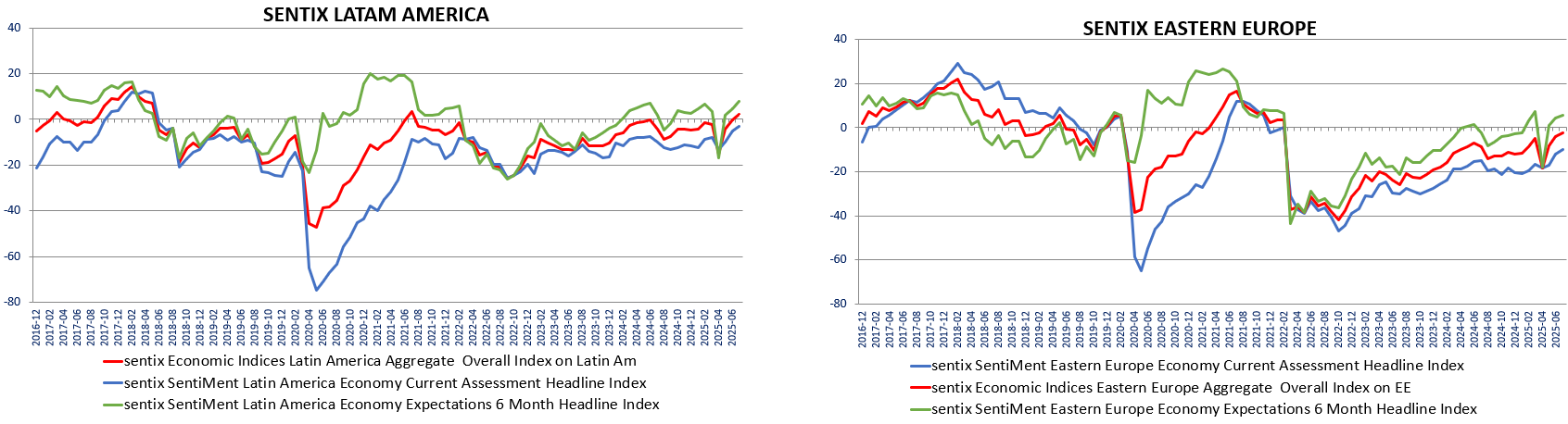

Investors sentiment increased significantly at the end of June /early July according to the latest Sentix Survey published this morning. Sentiment is the highest since February 2022 for the Eurozone (+4.5 vs 0.2 in June) for Germany (-0.4 vs -5.9) and for Eastern Europe (-2.3 bs -3.9). It is at the highest in 4 years (July 2021) for Latin America (+2.4 vs -0.2). Sentiment is at the highest since February in the US (+5.3 vs -5.4) and Japan (+6.9 vs +1.9) and the highest since June 2024 for Asia ex Japan (14.1 vs 11.2). Both current situation and current assessment are up in all regions, increasing the most in the US.

If you missed it, see Friday’s comment on Tesla European registrations, German , UK, Top-4 eurozone markets registrations, as well as German orders or Fed latest balance sheet update.

On the companies’ front: Cap Gemini is acquiring WNS, a player in Digital BPS (Business Process Services) to combine capabilities and scale to address the strategic opportunity driven by Agentic AI. The deal is valued at $3.3bn and is expected to be accretive to Capgemini’s normalized EPS. In its Q2 trading update Shell raised its oil output and narrowed the LNG production outlook. Shell expects losses in its chemical division after suffering unplanned maintenance at its Monaca polymer plant in the United States while trading in its chemicals and products business was significantly lower than in the first quarter. Legrand announced two small acquisitions reinforcing its exposure to data centers and energy transition. Over the weekend Airbus announced that Malaysia Aviation placed a firm order for 20 more A330-900 aircraft. This new order will double Malaysia Airlines’ future A330neo fleet to 40 aircraft. AirAsia has signed a deal to buy 50 Airbus long-range A321XLR planes with conversion rights for another 20, as the budget airline nears the end of a restructuring process. Four years after establishing Yuh as a joint venture, Swissquote is acquiring PostFinance's 50% stake in the digital finance app Yuh. As of June 30, 2025, Yuh totaled 342'369 accounts for CHF 3.2 billion of assets. The transaction does value Yuh at CHF 180 million (100 %). More details on equities here

Back to tariffs…

German Industrial Production increased more than expected by economists in May. Up +1.2% m/m versus 0% Expected. April is revised down to -1.6% m/m from -1.4% but still beating expectations when including the revision. Energy production was up +10.8% m/m and construction down -3.9% (weakest in civil engineering, -4.1% m/m) after being flat in April (revised sharply down from +1.4%).

When excluding construction production is up 2.2% and when excluding both energy & construction, production increased +1.4% after a negative -1.9% m/m in April (unrevised). The energy intensive industry production declined -1.8% m/m.

– all monthly figures are seasonally, and calendar adjusted.

On a year-over-year basis (non-seasonally adjusted, calendar adjusted) production is up 1%, the best since March 2023, with energy up 6.9% yoy (was -2.3% yoy in April, and construction down -3.4% yoy. When excluding energy & construction, production is up 1.4% yoy the best in 2 years (May 2023) improving sharply form -2.5% yoy in April.

The details suggest tariff delayed related production, with pharmaceuticals up 10% m/m and Motor vehicles +4.9% m/m. In contrast we see a sharp decline in Food& beverages production, down -3.9% m/m and textiles -3.0 Furniture and paper/wood product also saw decline in production.

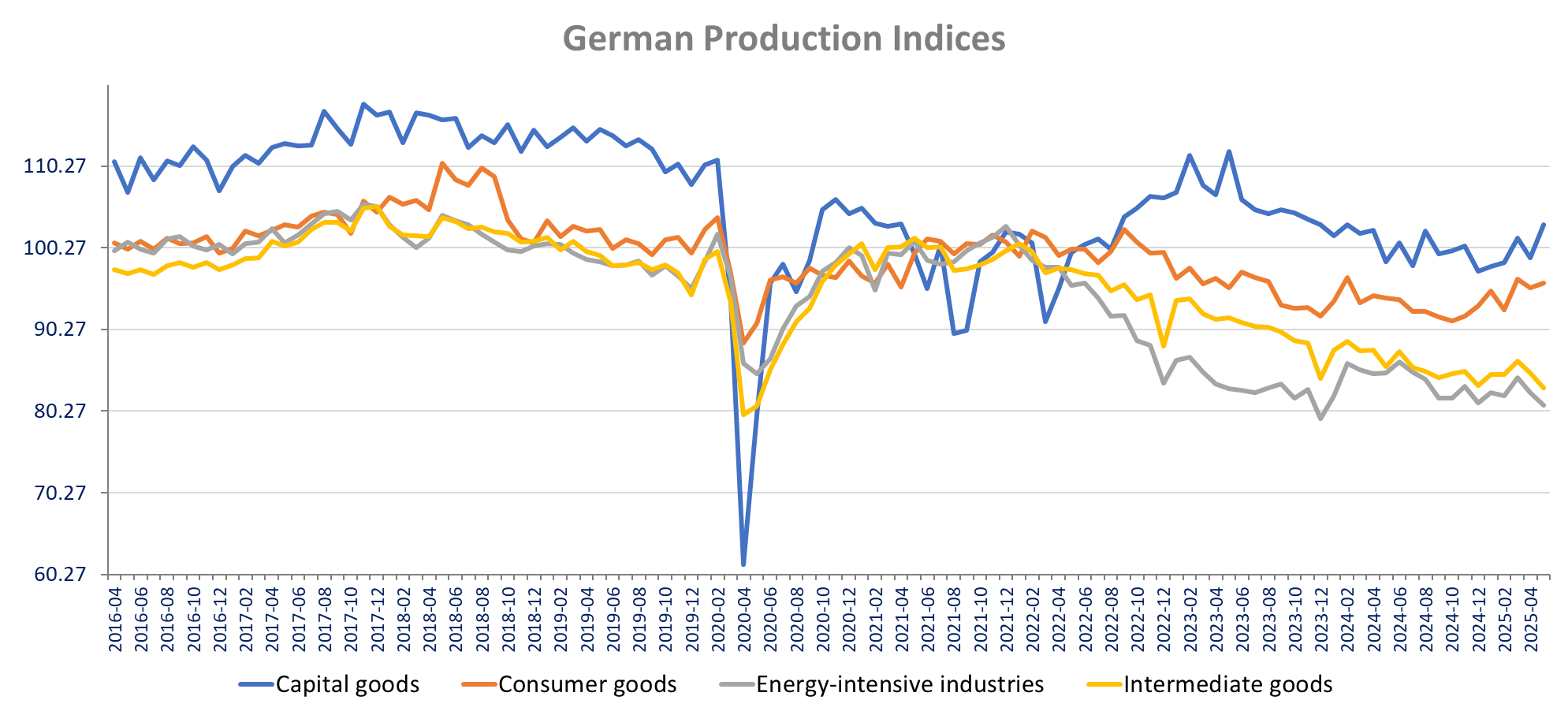

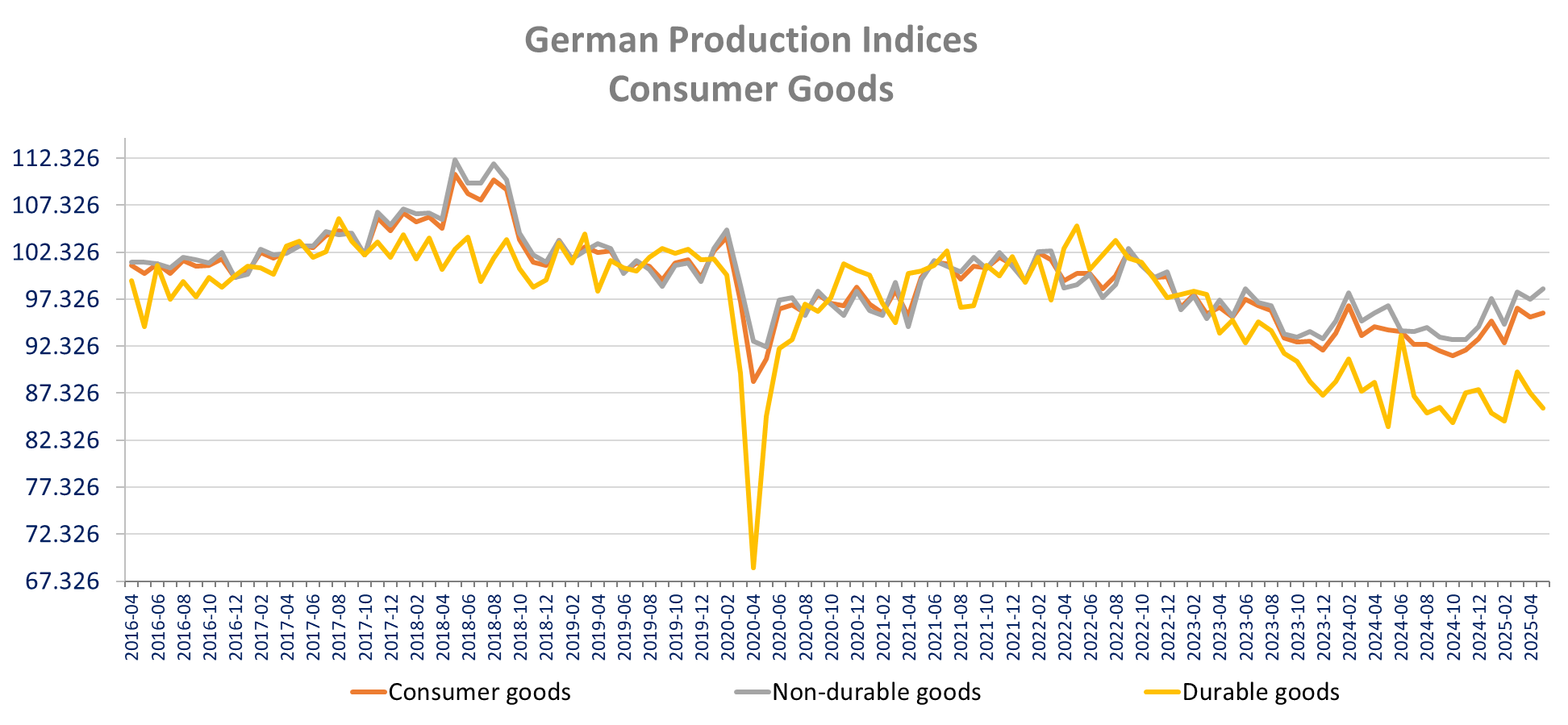

In term of broader categories, capital goods production increased +4.1% m/m in May (+4.7% yoy best since June 2023), Intermediate goods declined -2.1% (-3% yoy) and consumer goods increased 0.5% m/m (1.9% yoy). Consumer non-durable is up 1.1% (1.8% yoy) thanks to pharmaceuticals and durable goods declined -1.9% m/m After -2.5% m/m in April (revised from -1.2%) but are still up 2.1% yoy (-5.3% m/m in May 2024).

SWEDEN INFLATION (Prelim June)

Sweden inflation increased more than expected in June according to SCB preliminary estimates release, The CPI rose to 0.8% yoy from 0.2% yoy in May (+0.5%), the CPIF increased to 2.9% yoy (0.5% m/m) from 2.3% yoy in May, exceeding market expectations of 2.5% yoy / 0.2% m/m. The CPIF excluding energy rose to 3.3% yoy (0.7% m/m) the highest level since February 2024 (2.5% yoy then). The SCB release does not provide more details, final figures will be released July 14,

Sharp improvement in the Sentix investor sentiment index across all region in July. Sentiment is the highest since February 2022 for the Eurozone (+4.5 vs 0.2 in June) for Germany (-0.4 vs -5.9) and for Eastern Europe (-2.3 bs -3.9). It is at the highest in 4 years (July 2021) for Latin America (+2.4 vs -0.2). Sentiment is at the highest since February in the US (+5.3 vs -5.4) and Japan (+6.9 vs +1.9) and the highest since June 2024 for Asia ex Japan (14.1 vs 11.2).

Sentiment has improved for 3 months in a row in Germany, assessment for 5 consecutive month and expectation for 3 successive months, with according to Sentix fulfil the “triple rule” when the 3 components improved 3 consecutive months, which it consider as a turning point for the economy. Sentix Release

Both current situation and current assessment are up in all regions, increasing the most in the US.

We see a particular strong increase in current assessment in Europe exceeding the progress in expectations: up 8 points for Germany to -18.8 (highest since May 2023), up 5.7 points -7.3 for the Euro Area (highest since May 2023 as well). Expectations are still up 2.3 points for Germany to 19.8 and 2.8points for the Eurozone to 17.

For the US expectations (+11points to -3.8) increased a tad more than the current situation (+10.3 points to +14.8).

Similarly for Japan expectations on a little more, up 5.3 points to 8.3 while current assessment rose 4.8 points to 5.5. For Asia ex-Japan expectation are up 3.3 points to 16 and current assessment 2.6 points to 12.3.

|

|

Monday, July 7, 2025 | ||

|

SQN | |||

|

CHF |

478.60 |

+7.65% | |

|

SQN |

Four years after establishing Yuh as a joint venture, Swissquote is acquiring PostFinance's 50% stake in the digital finance app Yuh. As of June 30, 2025, Yuh totaled 342'369 accounts for CHF 3.2 billion of assets. The transaction values Yuh at CHF 180 million (100 %). Swissquote paid part of the purchase price in the form of treasury shares. Marc Burki, CEO of Swissquote, said:

| ||

|

|

|

|

|

|

AIR | |||

|

EUR |

177.10 |

+1.46% | |

|

AIR |

Orders: Malaysia Aviation Group, the parent company of national carrier Malaysia Airlines, has placed a firm order with Airbus for 20 more A330-900 aircraft. This new order will double Malaysia Airlines’ future A330neo fleet to 40 aircraft. AirAsia has signed a deal to buy 50 long-range Airbus A321XLR planes with conversion rights for another 20, as the budget airline nears the end of a restructuring process, | ||

|

|

|

|

|

|

LR | |||

|

EUR |

112.80 |

+0.71% | |

|

LR |

Legrand announced two small acquisitions. Amperio Project is a Swiss specialist in busbars. Based in Murten, the company employs around 20 | ||

|

|

|

|

|

|

REP |

Repsol SA | ||

|

EUR |

12.34 |

-0.64% |

|

|

REP |

Q2 trading statement after market close | ||

|

|

|

|

|

|

GALP |

Galp Energia SGPS SA | ||

|

EUR |

15.85 |

-1.31% |

|

|

GALP |

Q2 trading statement after market close | ||

|

|

|

|

|

|

SHEL | |||

|

GBp |

2551.50 |

-2.91% | |

|

SHEL |

Q2 trading update. Shell raised the lower end of its guided oil output, projecting 1.66 million to 1.76 million boed, up from the previously forecast 1.56 million to 1.76 million boed and narrowed the production guidance of the integrated division to 900,000 to 940,000 barrels of oil equivalent per day (boed), compared with the company's previous projection of 890,000 to 950,000 boed. LNG production is expected to come in at 6.4 million to 6.8 million metric tons in the second quarter, Shell said, compared with a previous range of 6.3 million to 6.9 million tons. Shell expects losses in its chemical division after suffering unplanned maintenance at its Monaca polymer plant in the United States while trading in its chemicals and products business was significantly lower than in the first quarter. | ||

|

|

|

|

|

|

CAP | |||

|

EUR |

137.40 |

-5.40% | |

|

CAP |

Cap Gemini is acquiring WNS a player in Digital BPS (Business Process Services) to combine capabilities and scale to address the strategic opportunity driven by Agentic AI. The deal is valued at $3.3bn and is expected to be accretive to Capgemini’s normalized EPS by 4% before synergies in 2026 and 7% post synergies in 2027. | ||

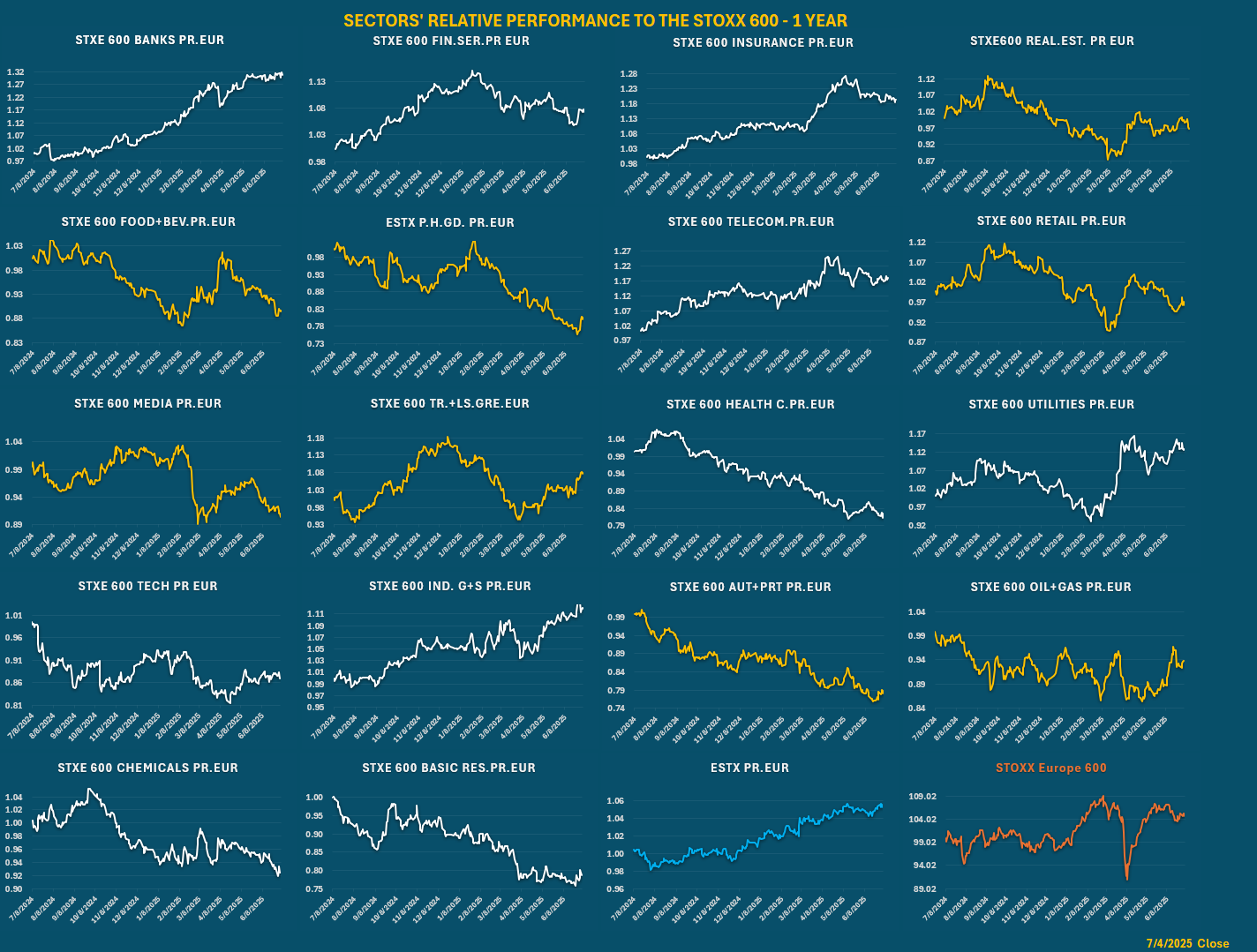

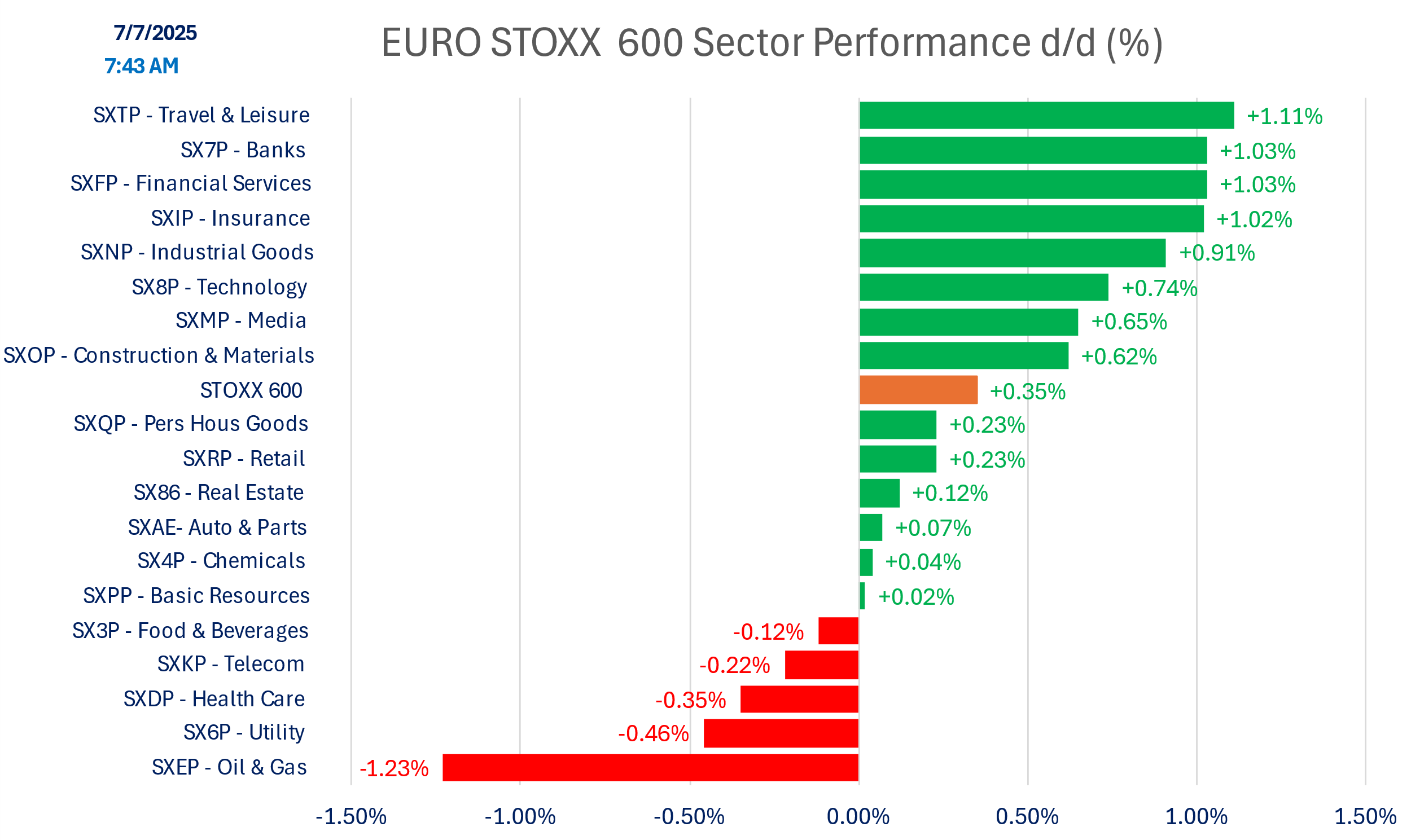

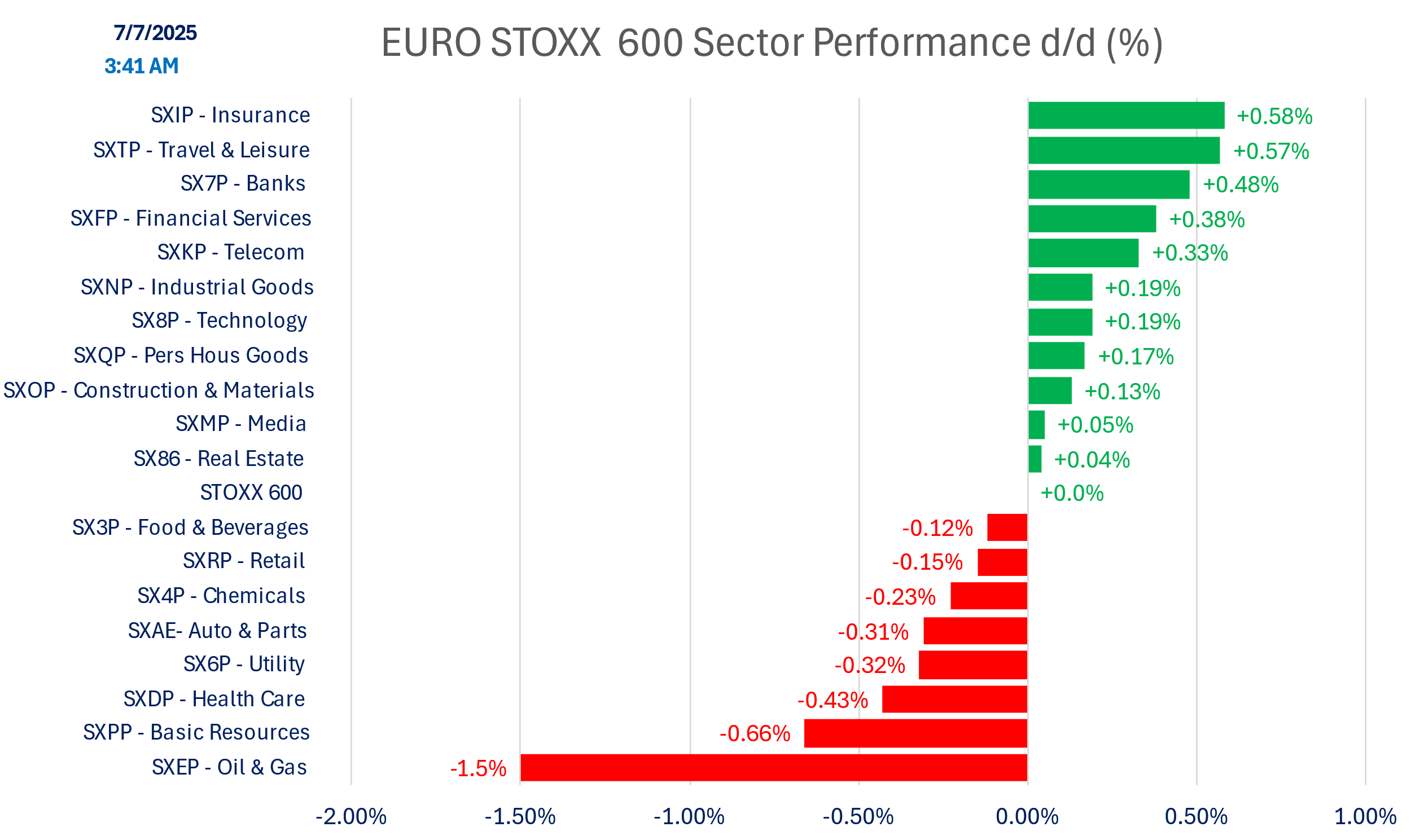

SECTOR PERFORMANCE

Relative performance to STOXX 600

Today’s Performance

Versus early hours:

Indices

Versus early hours

Commodities

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.