Last day of the quarter, half year, official week of summer vacation start in most Europe, ECB Sintra summit (June 30-July 2) difficult delivery of a coherent “big, beautiful bill” by the 4th of July… and of course, tariffs, 10 days before the July 9 deadline. Some optimism on tariffs as Canada promptly dropped the 3% digital tax in order to continue negotiations after Trump utterance on Friday. European seems optimistic that a framework could be agree upon to continue negotiations post July 9.

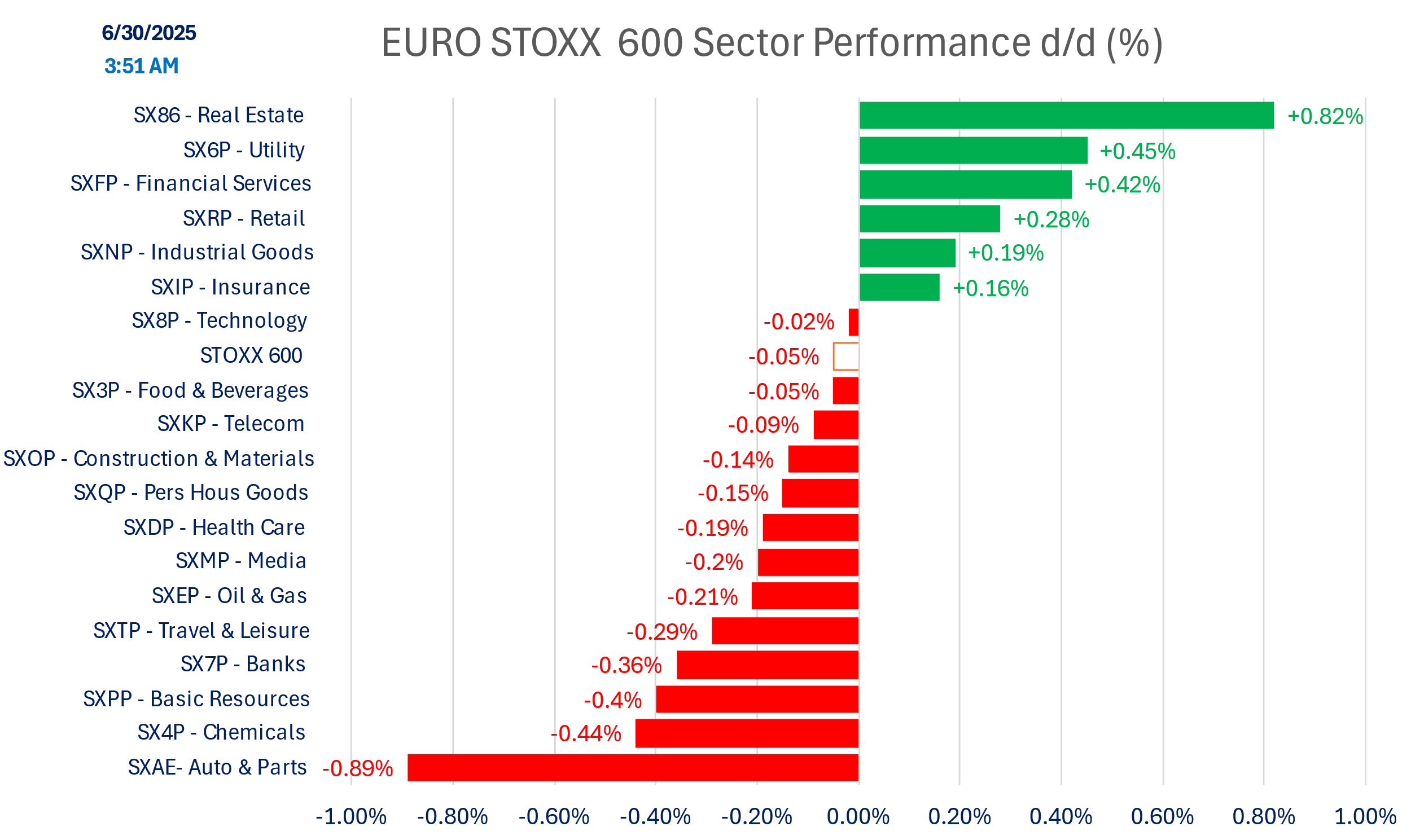

Stocks slightly down in Europe, yields slightly down and the $ weakens further. (DXY at 97.2)/

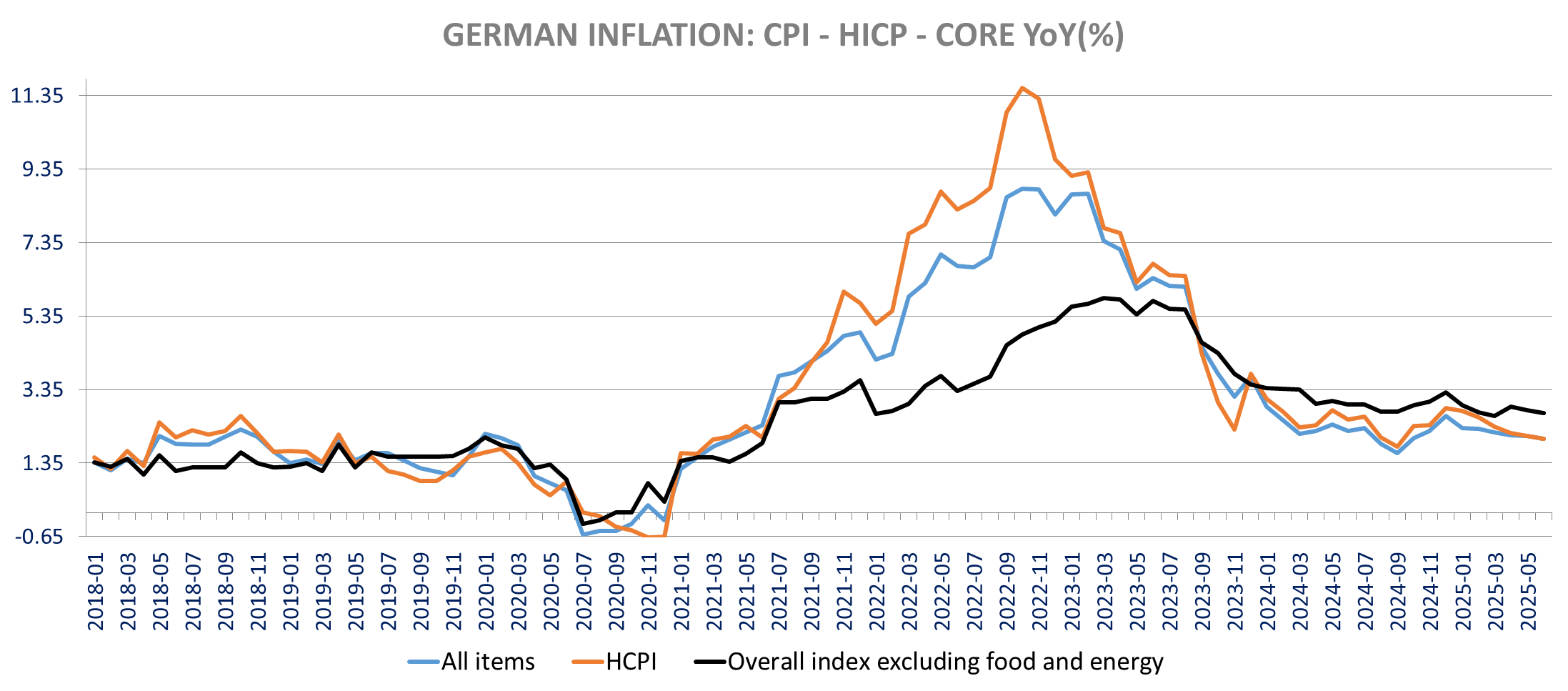

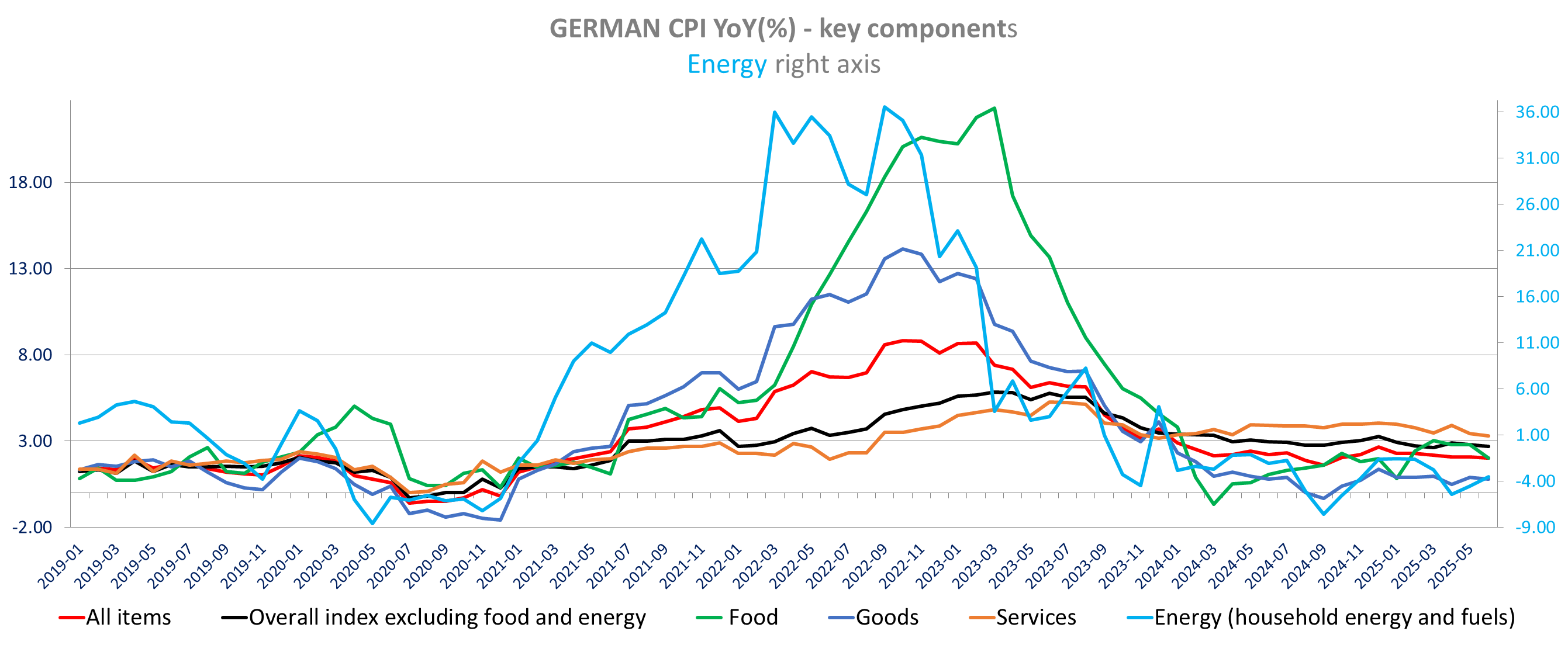

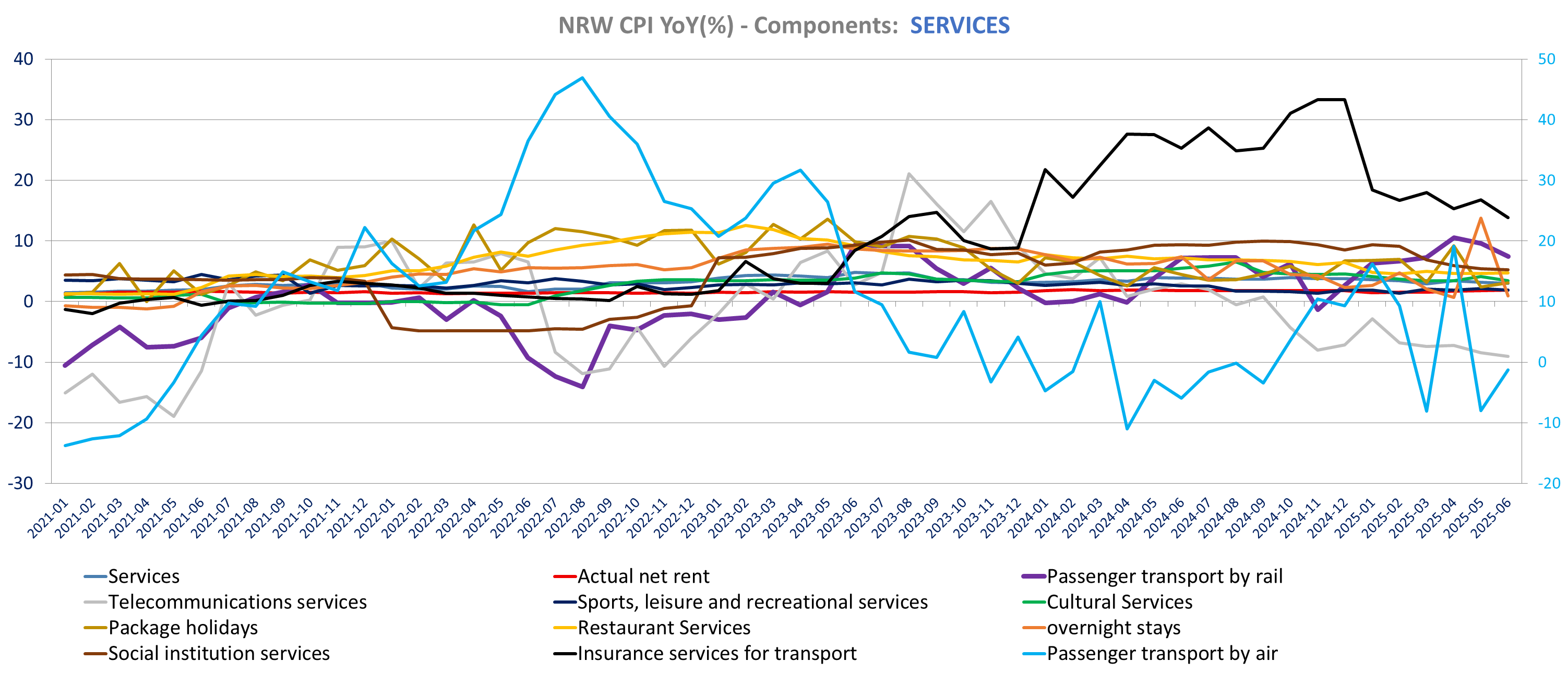

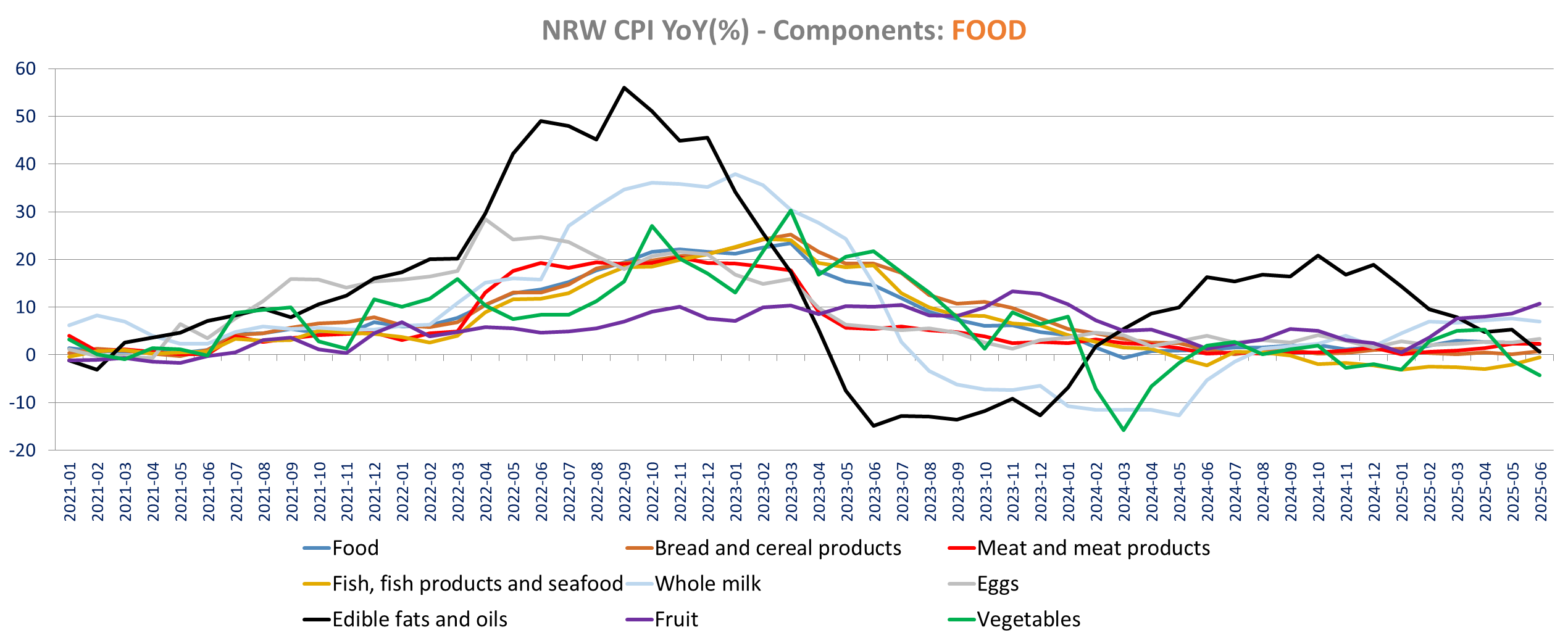

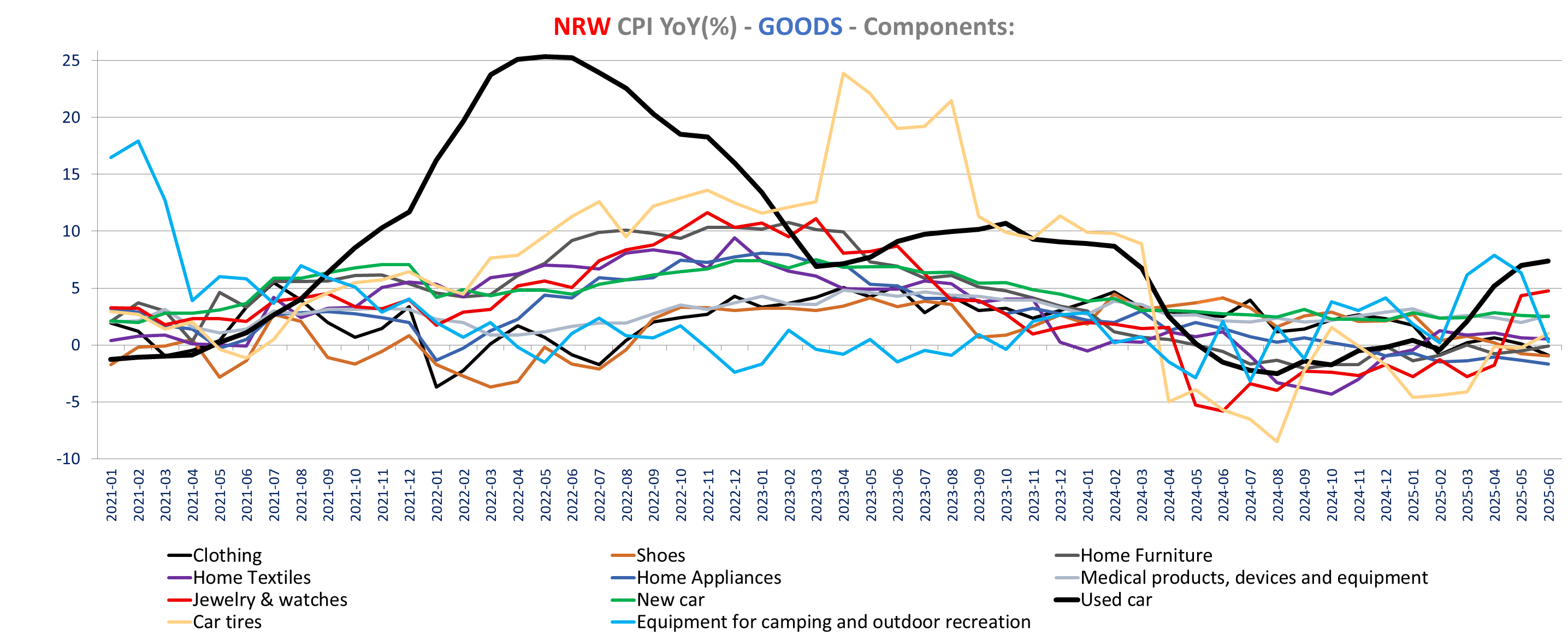

The German June preliminary inflation data is better than anticipated at 2% down from 2.1% when consensus expected an increase to 2.2%. Core inflation is down slightly to 2.7% from 2.8%. The biggest reason for the lower inflation came from food. Food inflation declined to 2% from 2.8%, services inflation eased to 3.3% from 3.4% and goods inflation fell to 0.8% from 0.9% (due to food) while energy inflation increased to -3.5% from -4.6%. The details for North-Rhine-Westphalia (NRW) shows a relatively broad-based decline in services inflation. NRW also shows the decline in food was mainly driven by vegetables, Oil & fats and dairy. The increase in energy inflation is driven by gas and liquid fuel. We also note further increase in used cars inflation in NRW to 7.4% yoy from 7%.

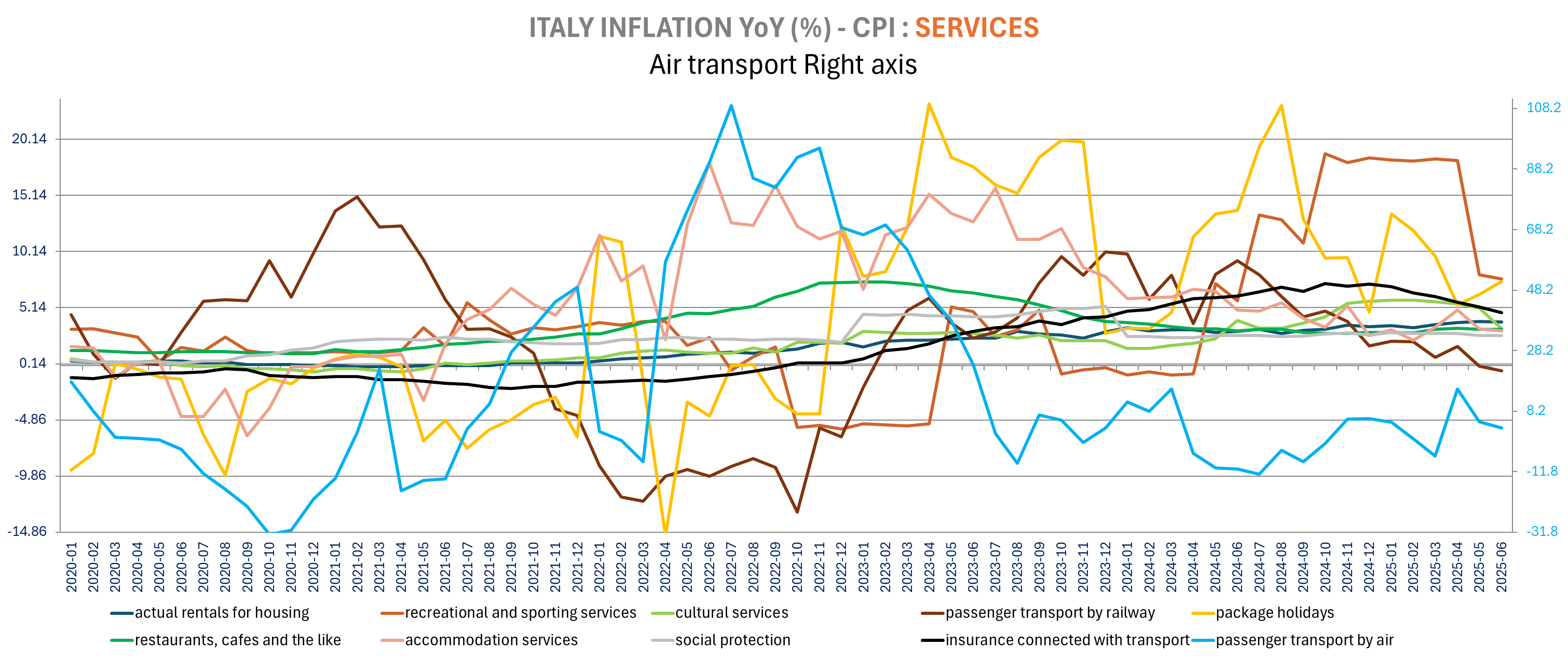

The Italian inflation is also lower than anticipated. The Italian CPI increased to 1.7% yoy in June from 1.6% in May (0.2% m/m), in line with market expectations. The HICP is unchanged at 1.7% (0.2% m/m), slightly lower than expectations for an increase to 1.8% yoy. Core inflation increased to 2.1% from 1.9% (0.4% m/m) with services inflation up to 2.7% from 2.6% (0.6% m/m). Contrary to Germany, Italian food inflation increased to 3.05% from 2.7%. with unprocessed food inflation accelerating to 4.15% from 3.5%. Meat, fish, milk cheese, fruit (6.8% vs 4.3%) inflation is higher in June than in May, but vegetables inflation decreases to 1% from 1.7% and for oil & fats (-8.4% vs -7.6%). In services inflation increased for package holidays (7.5% vs 6.3%) and transport services (2.85% vs 2.6% mainly road transport). Restaurants, social protection, education and rent saw stable inflation. Inflation decreased for accommodation (3.1% vs 3.3%), cultural services (3.3% vs 5.1%) and sporting & recreational services (7.7% vs 8.1%). Auto insurance inflation decreased to 4.7% from 5.2%.

A positive after the slightly higher than expected inflation in France and Spain last week. We will have the full set of PMIs this week. The earlier release did show some pick up in price charged for services, but last week’s ESI did not corroborate that. Consumer inflation expectations are also well anchored, but overall unemployment fear is down, and the ESI employment improved.

The ECB monetary strategy review, kicking off the start of the Sintra summit, points to higher uncertainty on inflation due to the geopolitical situation. Several articles also points to higher waiting times at European ports, partly due to low Rhine River level, but also increase in cargos from China (FT article).

The ECB will keep rates unchanged in July.

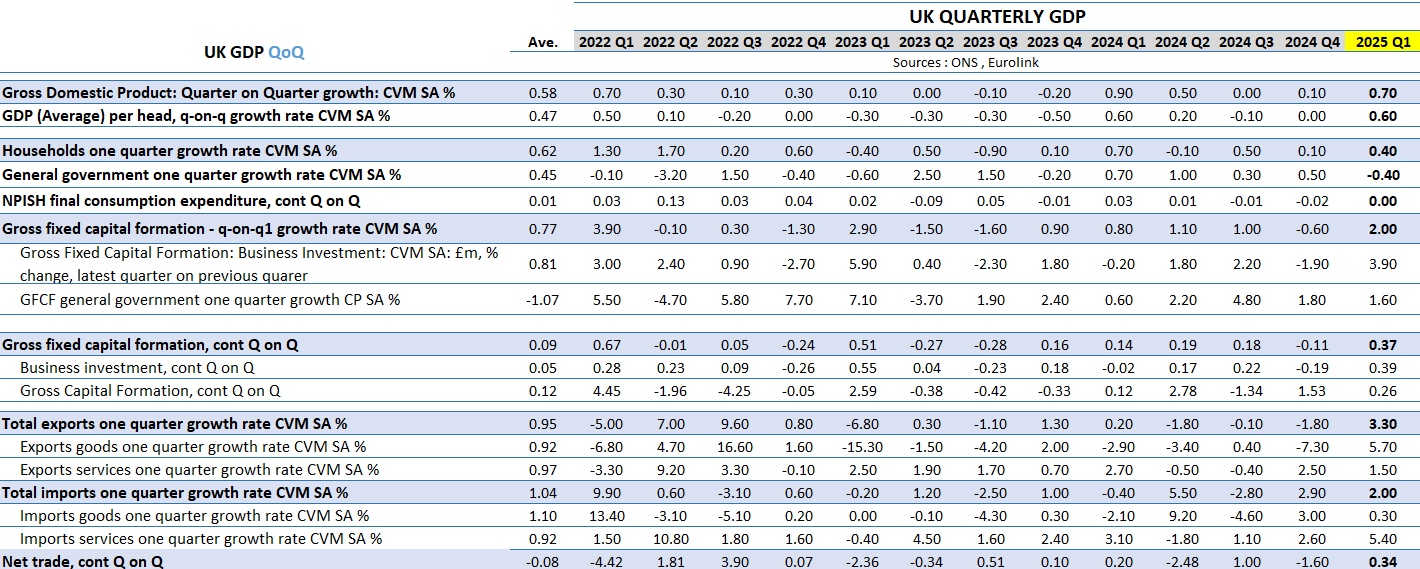

The UK Q1 GDP is confirmed at 0.7% q/q on strong GFCF and exports. The Q2 GDP will be lower and we expect the BoE to ease in August.

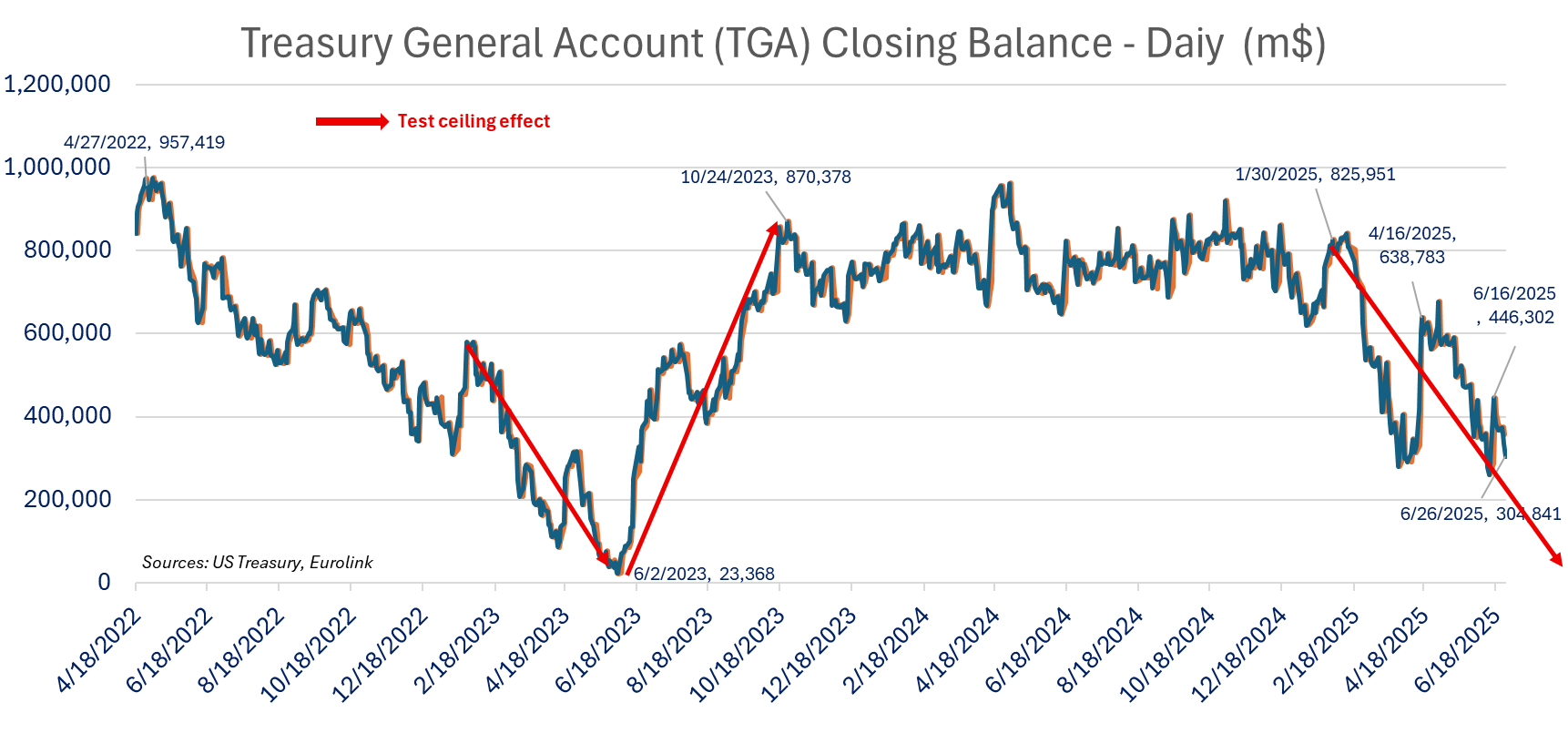

The latest data show further decline in the TGA (down to $304.8bn on Thursday, -$141.5bn from June Tax Day): the starting point of the TGA rebuilding towards $850bn will depend on when the debt ceiling is lifted. The Senate proposal is for an increase of $5tn, and points to sharper deficits…

On the companies’ front: Vallourec secured a significant order from Abu Dhabi National Oil Company (ADNOC) for the supply of more than 30,000 tons of carbon steel tubulars and associated accessories featuring VAM premium connections. This order is part of the ongoing Long-Term Agreement (LTA) for the supply of Oil Country Tubular Goods (OCTG) between Vallourec and ADNOC. This order fully aligns with ADNOC’s ambitious target of reaching 5 million barrels per day of production by 2027. Parvus Asset Management, a hedge fund registered in Britain, has acquired 5% of the share capital and 3.5% of the voting rights of Kering, a filing by France's financial regulator showed on Friday. Porsche shares were up 7% last Friday after the German newspaper Handelsblatt wrote that the car company is considering selling its IT and management consultancy MHP for approximately €1bn. According to Handelsblatt information, the market has already been probed – so far without result. 1&1 warned that its 2025 EBITDA is now expected to at approximately €810 million (previous forecast for 2025: approximately €836 million). This is primarily due to higher than planned wholesale costs for national roaming with Vodafone. More details on equities here

“Big Beautiful Bill” Marathon…

The ECB released its monetary policy strategy update. No major changes but more uncertainty in the inflation outlook.

The ECB confirms its symmetric approach to keeping price growth at that level over the medium term and said it will use an “appropriately forceful or persistent policy response” to large and lasting deviations in either direction. A slight change from “especially forceful or persistent” action to avoid too-low inflation becoming entrenched when the economy is “close to the lower bound.” 4 years ago.

The ECB also says the global economy was facing a number of "structural shifts" from geopolitical and economic fragmentation to demographics and climate change, that will make inflation more prone to large deviations from its target level.

"The inflation environment will remain uncertain and potentially more volatile, with larger deviations from the symmetric 2% inflation target,"

The latest TGA data (Daily Treasury update) continues to show further decline as expected: down to $304.8bn as of Thursday, a decline from $446.3bn on June Tax Day. The Senate proposal is for a $5tn increase in the debt limit. The timing of the approval will determine the TGA starting point for rebuilding. By the end of this week, we will be closer to $225bn. Target is to rebuild the TGA towards $850bn after the debt limit agreement, draining liquidity

…

The German States CPI is mixed in June, decreasing in North-Rhine-Westphalia (NRW, largest state and weight) to 1.8% from 2% yoy in May (-0.1% m/m), in Bavaria to 1.8% yoy down from 2.1% (-0.1% m/m) and Lower-Saxony (2.2% vs 2.3%,0.2% m/m). In May Inflation was up m/m in NRW and Lower-Saxony and unchanged in Bavaria when compared to April when inflation was unchanged at the German level.

June inflation rate is unchanged in Hesse (2.3%) and Brandenburg (2.2%) and up in Baden-Württemberg (2.3% vs 2.2%, 0.2% m/m), Rhineland-Palatinate (1.8% vs 1.7% yoy, up 0.2% m/m) and Saxony (2.4% yoy vs 2.3%, 0.2% m/m).

It would suggest the German inflation rate at 2-2.1% versus 2.1% in May, i.e. better than consensus of 2.2%.

Indeed, Destatis just released the CPI data, down to 2% from 2.1%, lower than expectations of 2.2%. Food inflation declined to 2% from 2.8%, services inflation eased to 3.3% from 3.4% and goods inflation fell to 0.8% from 0.9% (due to food) while energy inflation increased to -3.5% from -4.6%. The details for NRW shows a relatively broad-based decline in services inflation. NRW also shows the decline in food was mainly driven by vegetables, Oil & fats and dairy. The increase in energy inflation is driven by gas and liquid fuel. We also note further increase in used cars inflation in NRW to 7.4% yoy from 7%, (see NRW details below)

Details for North-Rhine Westphalia

The data for NRW shows a decline in core inflation to 2.35% from, 2.5% (0% m/m) with services inflation down to 3% from 3.2% with lower accommodations inflation (1% vs 13.4% in May, down -9.6% m/m), social services (5.25% vs 5.45%), outpatient services (2.5% vs 2.35% and car insurance (13.9% vs 16.8%). Rail transport inflation also eased to 7.4% from 9.6% along communication services (-9% vs -8.4), cultural services (3.45% vs 4.1%) and sport, leisure & recreational services (1.9% vs 2.1%). It was partially compensated for by higher air transport services inflation (-1.3% vs -8%), package holidays (3.1% vs 2.4%), restaurants (4.7% vs 4.6%), Education (4.8% vs 4.7%) and rent (1.9% bs 1.8%). NRW Release

Food inflation fell to 2.15% from, 2.6% (-0.4% m/m) with lower vegetable inflation (-4.2% vs -1.1%), Milk (6.9% vs 7.6%), oil & fats (0.6% vs 5.3%) sugar, stable meat inflation but higher inflation for fruit, fish, eggs and bred & Cereals.

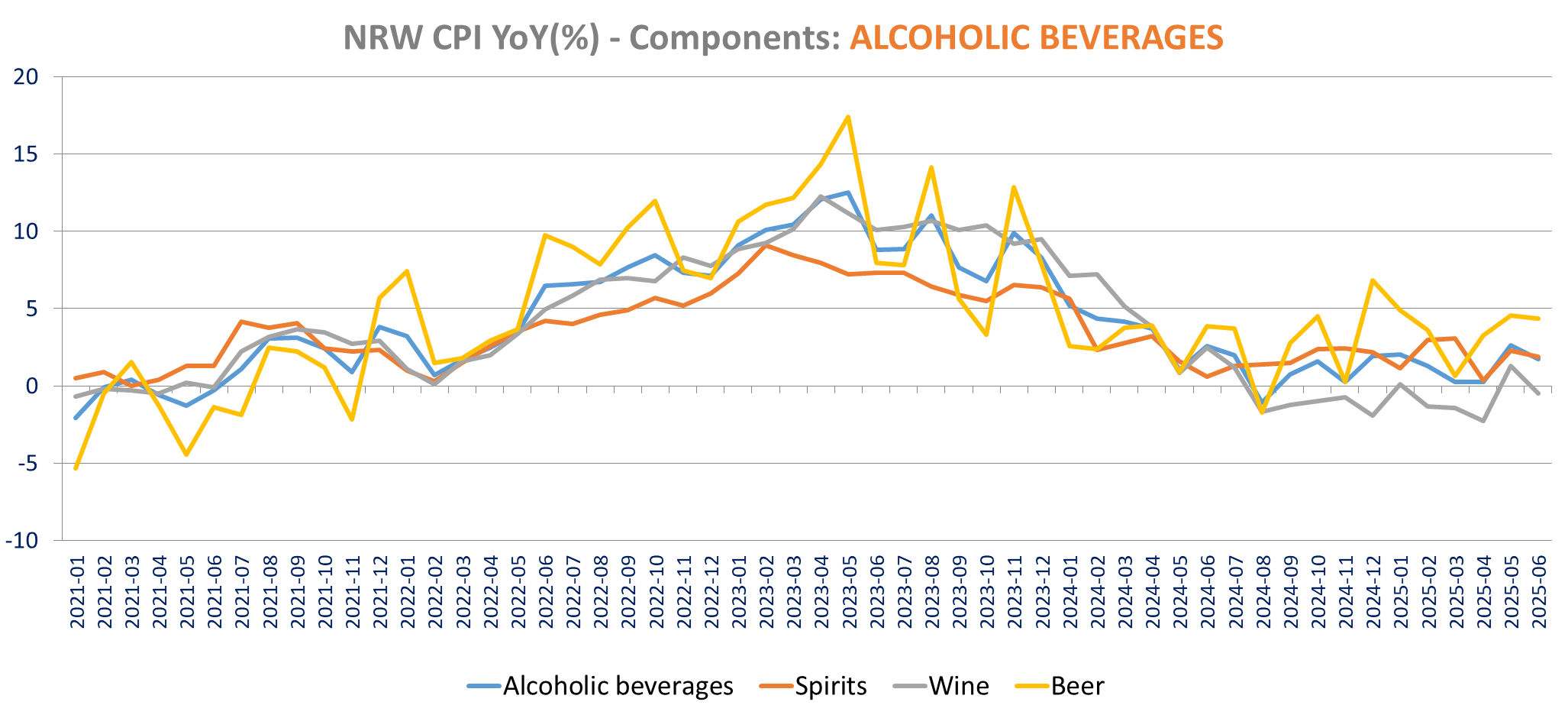

Alcoholic beverages inflation is down to 1.8% from 2.6% (especially down for wine).

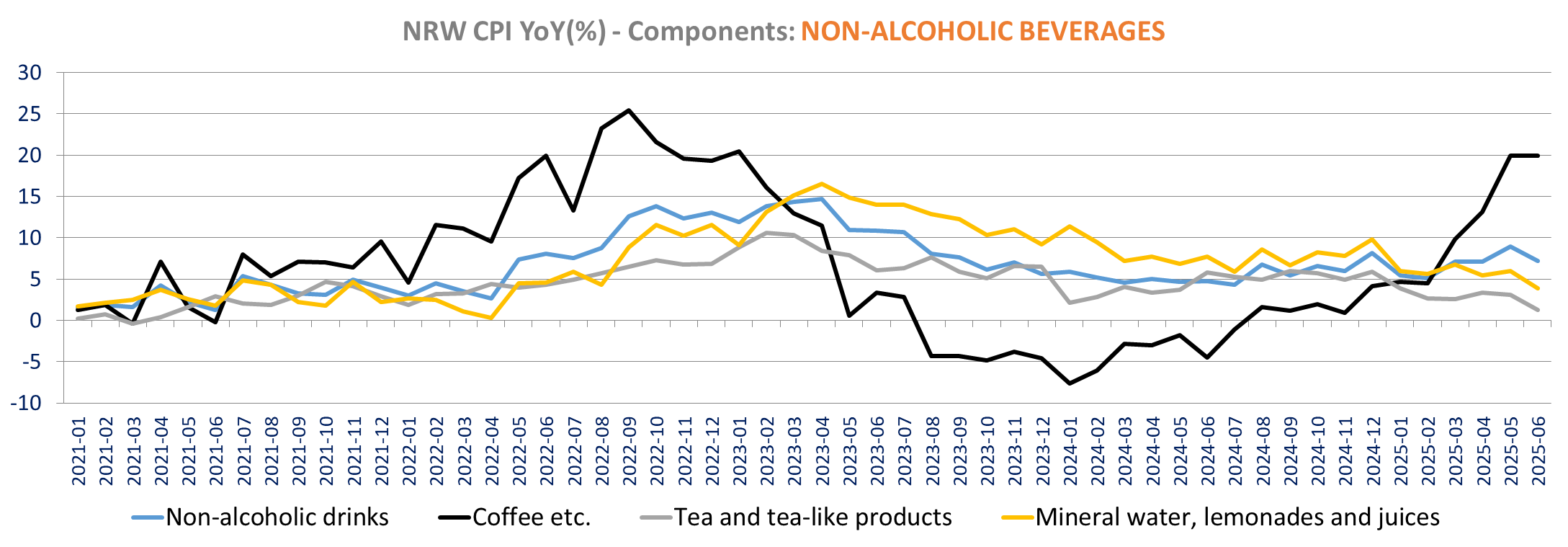

Non-alcoholic beverages inflation also decreased to 7.2% from 8.9^% yoy (-0.7% m/m), with stabilizing coffee inflation (20% vs 19.9%), lower tea, soft drinks and mineral water inflation. Tobacco inflation also increased to 9% from 8.8%.

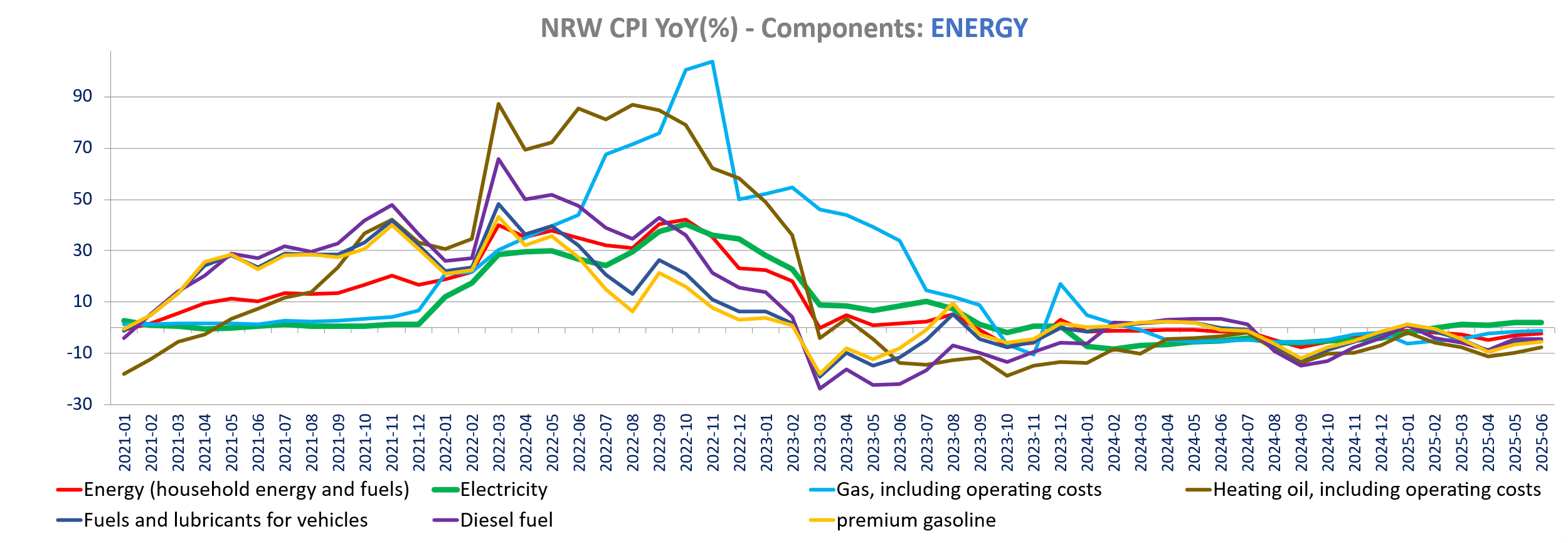

Energy inflation increased to -2.5% from -3.1% amid slightly higher gas price inflation but also heating oil and liquid fuel (notably gasoline). Electricity inflation is slightly lower at 1.9% yoy down from 2%.

For other goods we note lower inflation for clothing, footwear, home appliances, camping & outdoor equipment, home textiles and medical products, but slightly higher inflation for furniture, tires, jewelry & watches. Inflation increased again for used cars to 7.4% yoy from 7%, new car inflation is slightly lower at 2.5% vs 2.6%

ITALIAN INFLATION (June Preliminary)

The Italian CPI increased to 1.7% yoy in June from 1.6% in May (0.2% m/m), in line with market expectations. The HICP is unchanged at 1.7% (0.2% m/m), slightly lower than expectations for an increase to 1.8% yoy. Core inflation increased to 2.1% from 1.9% (0.4% m/m) with services inflation up to 2.7% from 2.6% (0.6% m/m). ISTAT Release

In services inflation increased for package holidays (7.5% vs 6.3%) and transport services (2.85% vs 2.6% mainly road transport). Restaurants, social protection, education and rent saw stable inflation. Inflation decreased for accommodation (3.1% vs 3.3%), cultural services (3.3% vs 5.1%) and sporting & recreational services (7.7% vs 8.1%). Auto insurance inflation decreased to 4.7% from 5.2%.

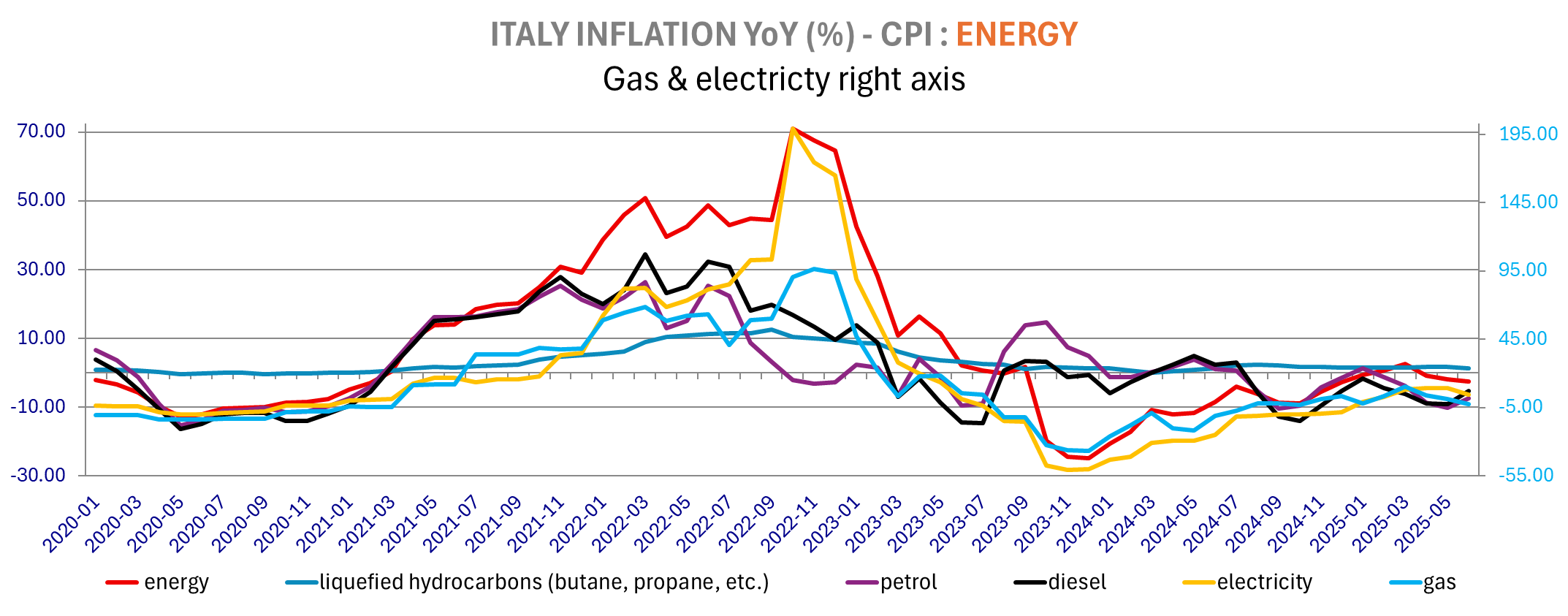

Energy inflation decreased to -2.5% from -2% yoy lower regulated energy inflation (22.7% down from 29.25%, down -2.9% yoy). Electricity and gas inflation but we see higher inflation for diesel and gasoline.

Food inflation increased to 3.05% from 2.7%. with unprocessed food inflation accelerating to 4.15% from 3.5%. Meat, fish, milk cheese, fruit (6.8% vs 4.3%) inflation is higher in June than in May, but vegetables inflation decreases to 1% from 1.7% and for oil & fats (-8.4% vs -7.6%).

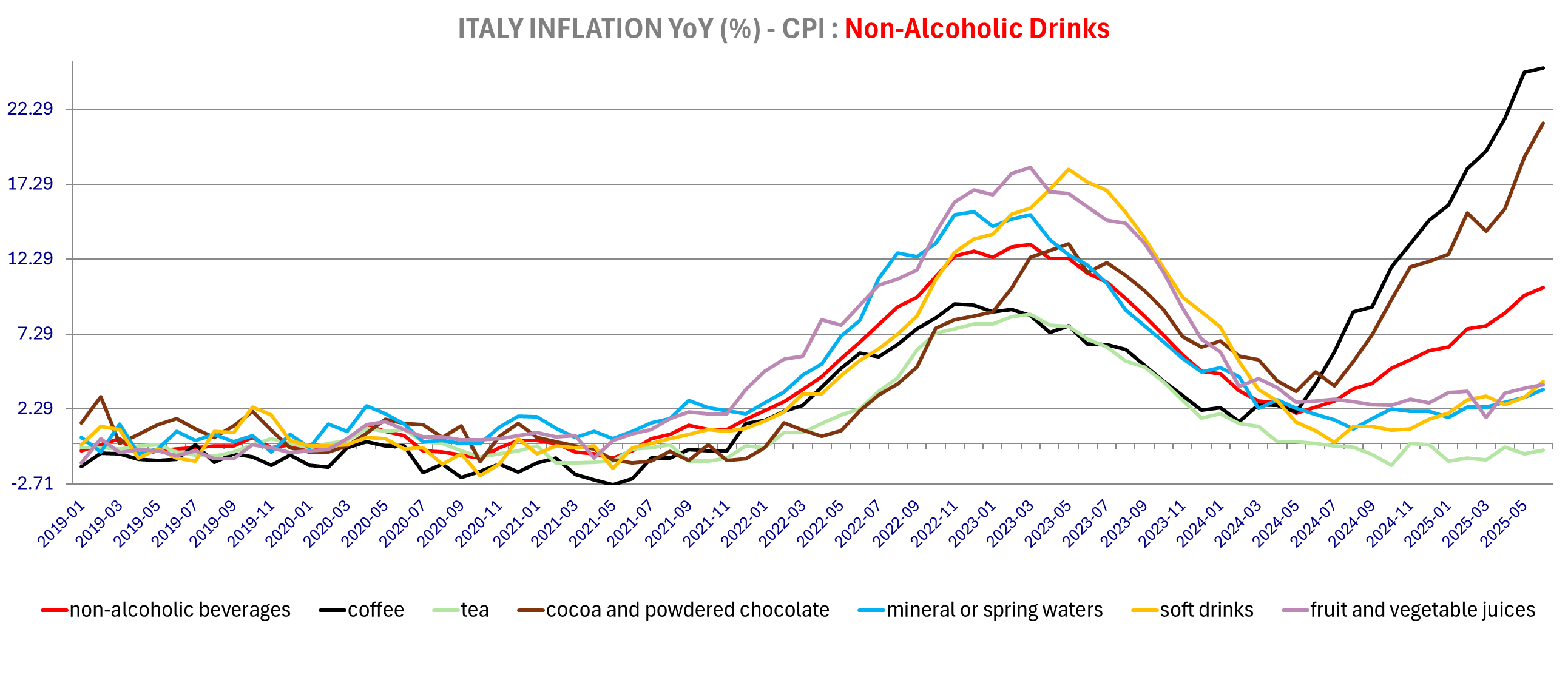

Non-alcoholic beverages inflation increased again to 10.4% from 9.8% with coffee up (25% vs 24.7%) along cocoa-based drink (21.4% vs 19.1%), soft drinks (4.1% vs 3.05%), Juices (3.9% vs 3.7%) and mineral water (3.6% vs 3%).

Alcoholic beverages inflation is up to -0.3% from -0.8% yoy.

Non-energy industrial goods inflation increased to 0.4% from 0.3% yoy., up for furniture, house textiles, stable for Autos, appliances and clothing& footwear.

Detailed table

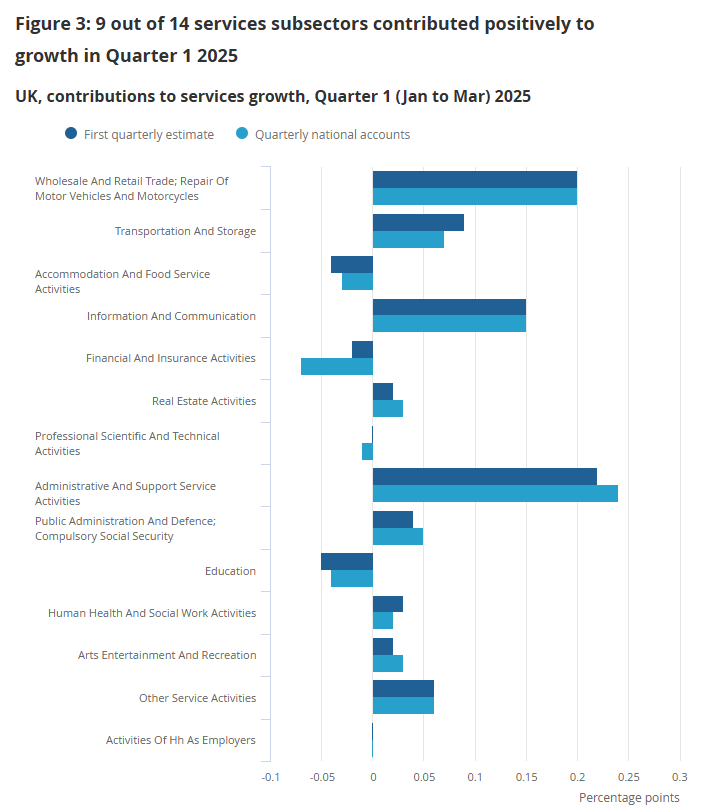

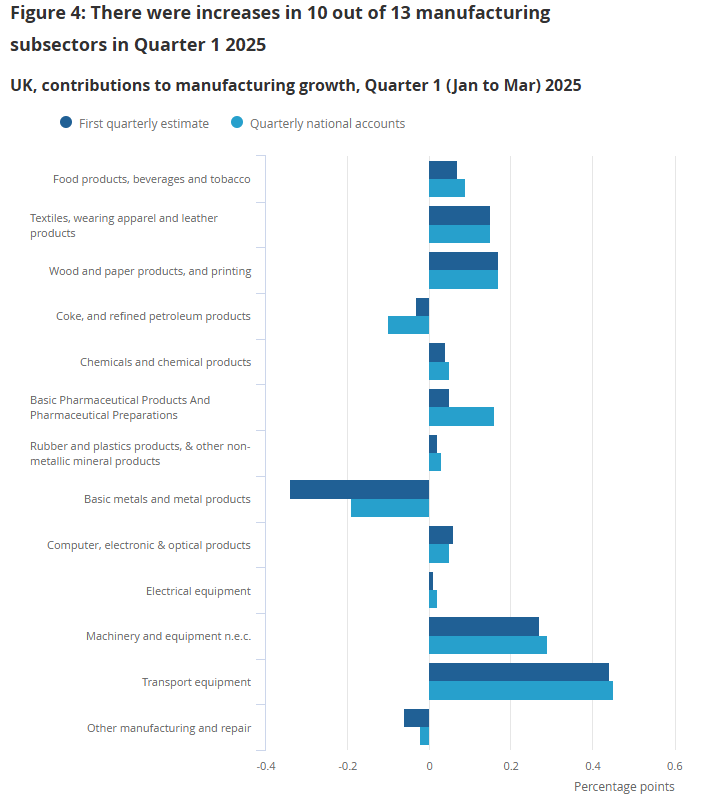

The UK Final estimate of Q1 GDP shows stronger growth, up 0.7% q/q in line with the preliminary estimates Services grew 0.7%q/q with the largest contribution from administrative and support service activities (3.7%) and wholesale and retail trade (1.6%). Construction is up 0.3% and production 1.3% (o/w manufacturing 1.1% q/q and water supply, sewerage, Waste management up 4% q/q, energy up 2.5% m). Within manufacturing transport equipment increased 2.8% and machinery and equipment 4%.

In term of output, GFCF increased 2% q/q with business investment up 3.9% and net trade had a positive contribution: exports up 3.3% q/q (5.7% for goods, 1.5% services) outpacing imports’ growth of 2% (0.3% for goods and 5.4% for services). Household consumptions lagged, up 0.4% q/q. The ONS data shows that the savings rate fell to 10.9% form 12% and Real household disposable income (RHDI) per head is estimated to have decreased in the latest quarter by 1.0% from a revised 1.8% increase in the previous quarter.

See ONS Release

|

|

Monday, June 30, 2025 | ||

|

VK | |||

|

DKK |

15.87 |

+4.00% | |

|

VK |

Vallourec has secured a significant order from Abu Dhabi National Oil Company (ADNOC) for the supply of more than 30,000 tons of carbon steel tubulars and associated accessories featuring VAM premium connections. This order is part of the ongoing Long-Term Agreement (LTA) for the supply of Oil Country Tubular Goods (OCTG) between Vallourec and ADNOC. This agreement also involves an integrated suite of services, such as VAM® Field Service and value-added digital solutions designed to optimize installation and maintenance practices. These services will ensure that ADNOC’s oil and gas fields operate with maximum efficiency | ||

|

|

|

|

|

|

KER | |||

|

EUR |

186.74 |

+1.38% | |

|

KER |

Parvus Asset Management, a hedge fund registered in Britain, has acquired 5% of the share capital and 3.5% of the voting rights of Kering, a filing by France's financial regulator showed on Friday. | ||

|

|

|

|

|

|

P911 | |||

|

0 |

42.42 |

+0.07% | |

|

P911 |

Porsche share were up 7% last Friday after the German newspaper Handelsblatt wrote that the car company is considering selling its IT and management consultancy MHP. According to Handelsblatt information, the market has already been probed – so far without result. | ||

|

|

|

|

|

|

1U1 | |||

|

EUR |

18.60 |

-0.96% | |

|

1U1 |

1&1 warned that its 2025 EBITDA is now expected to at approximately €810 million (previous forecast for 2025: approximately €836 million). This is primarily due to higher than planned wholesale costs for national roaming with Vodafone. The national roaming agreement between 1&1 and Vodafone is based on a capacity model, whereby 1&1 pays Vodafone a fixed price per percentage point for the percentage of the Vodafone network used by its customers in Germany. Based on the 1&1 usage share determined by Vodafone in its invoices, the Company now believes that its assumptions regarding data growth on the Vodafone network in 2025 were too optimistic and that 1&1 will therefore have to purchase a higher percentage of the Vodafone network than planned in order to serve its mobile customers. Reminder: United Internet made an offer to acquire 1&1 the entire share capital. | ||

Versus early hours:

SECTOR PERFORMANCE

Relative performance to STOXX 600

Today’s Performance

Versus early hours:

Indices

Versus early hours

Commodities

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.