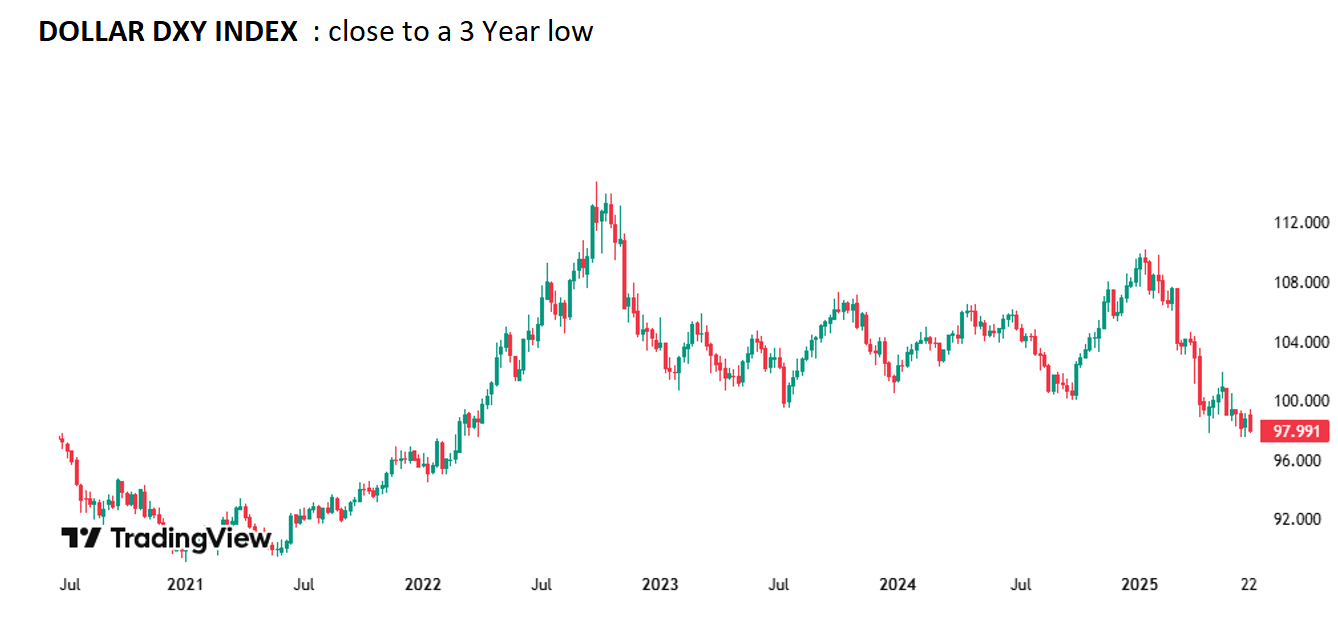

Sharp reversal after de-escalation in the Iran-Israël conflict and a ceasefire brokered by the US. The Iranian nuclear is setback, but not annihilated, with no information on the whereabouts of the enriched uranium stock. Nevertheless, the truce led to a relief rally in stock, already started with the tame, flagged Iran response yesterday. Oil price is down about -3.5% to ~$69 (Brent) and the $ gave up all the minimal gains observed in the past days. In fact, one would argue that the $ did not exhibit a haven status during the crisis. The performance seemed more related to positioning (negative $), reducing exposure rather than a flight to quality. The € is back above 1.16, the ¥ below 145 for a $. The DXY fell below 98, close to lowest in 3 years. Golds loses some ground, and the episode of the last week did – once again- highlighted the divergence in behavior between gold and Bitcoin, the later more in synch with the Nasdaq and risk off sentiment.

As NATO countries (but Spain) pledged higher defense spending, targeting 5% of GDP, Germany announced the intention to increase its military budget to 162bn by 2029, up 70% from last years 95bn, bringing defense spending to 3.5% of GDP from 2.4% this year. Germany aims at taking the lead in European defense spending and further support economic growth with the additional infrastructure spending.

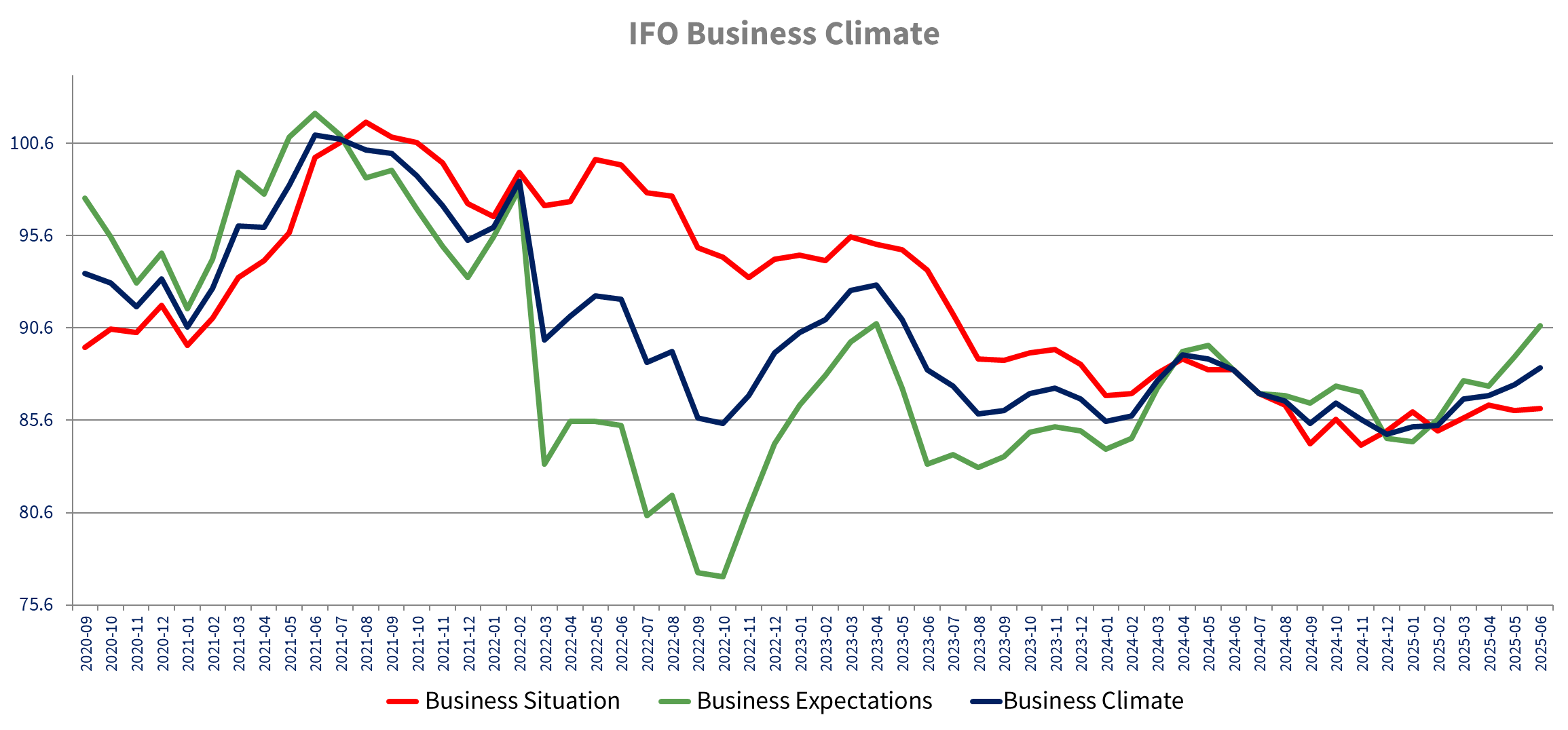

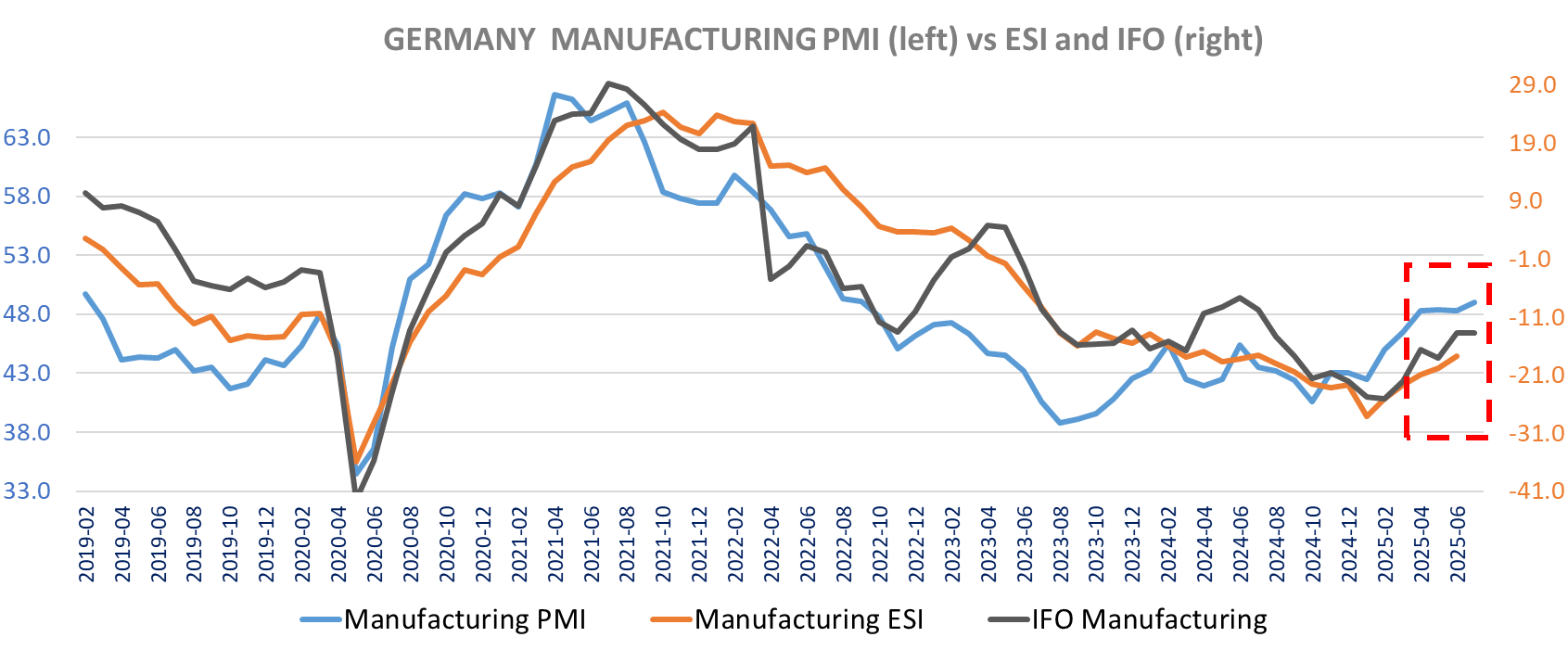

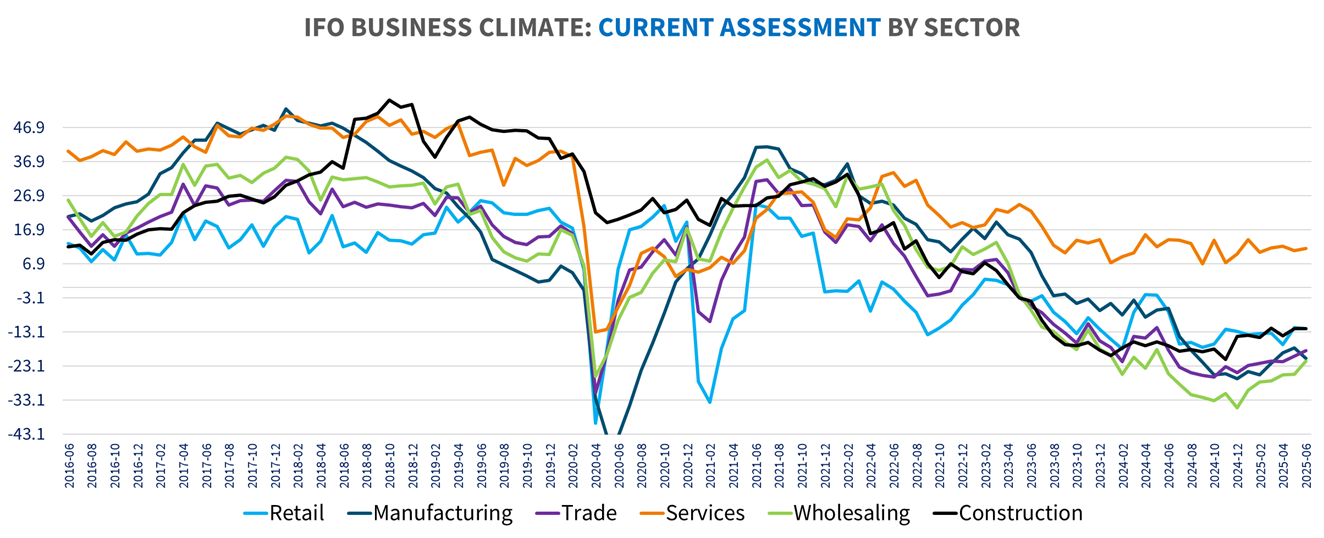

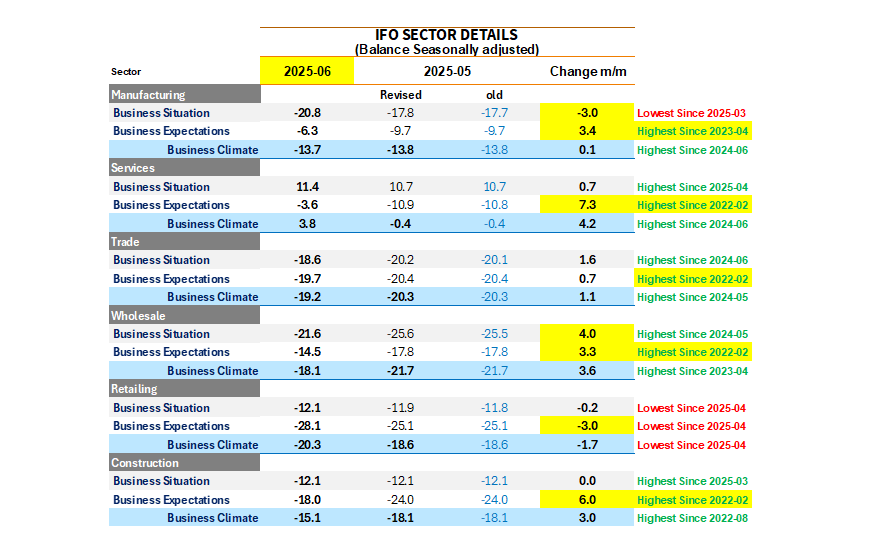

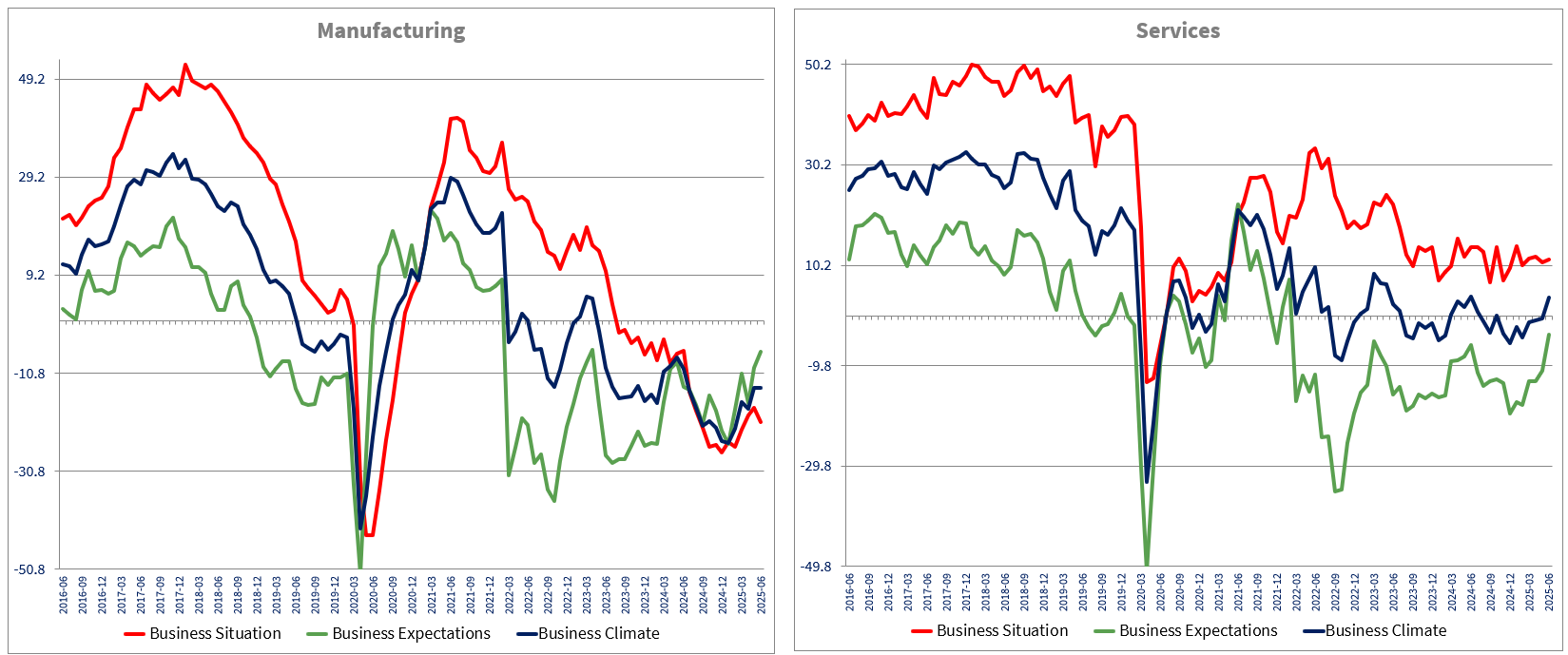

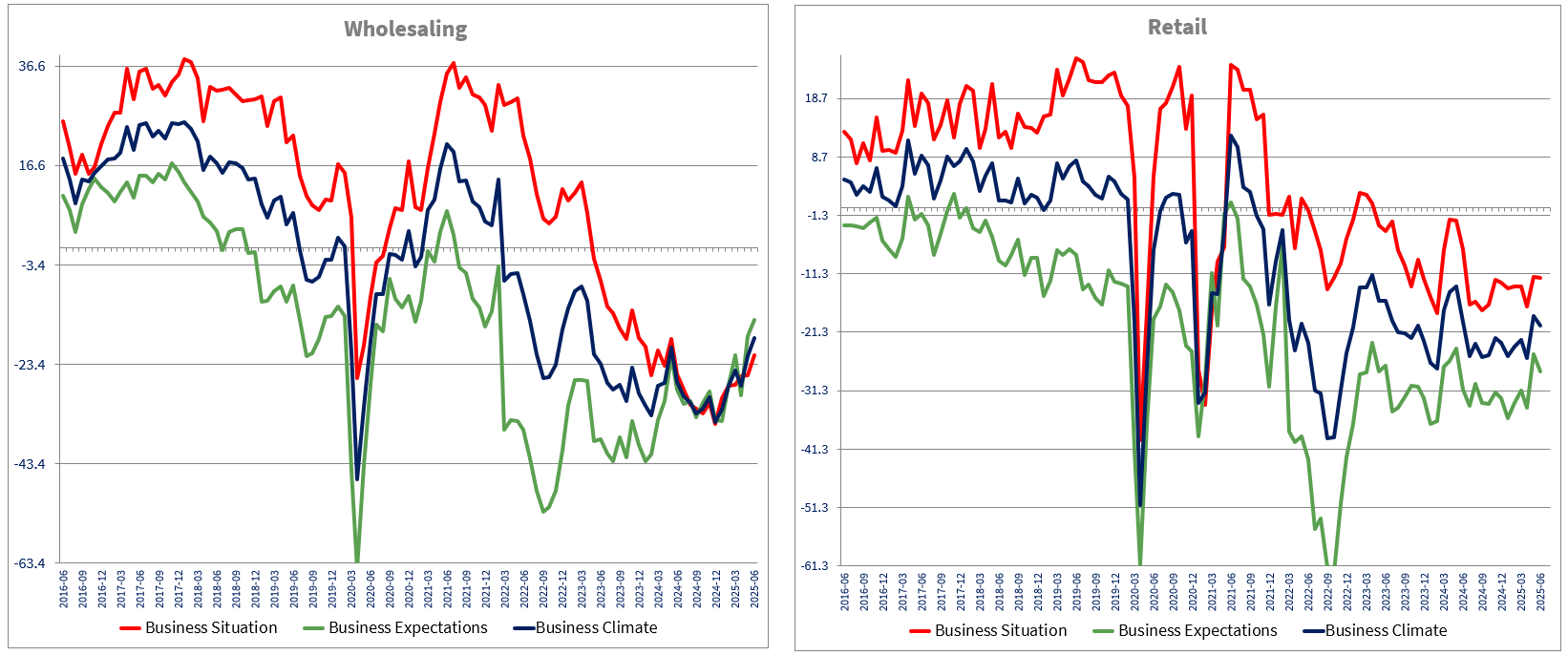

The June German IFO is better than expected amid a surge in expectations across sectors. The current assessment is about unchanged at 86.2 vs 86.1 in May below forecasts of 86.5. Business expectations increased to 90.7 from 89, the highest level in more than 2 years (April 2023) and above consensus of 90. Expectations are up in all sectors except retail while current assessments are about unchanged or down in all sectors but wholesale.

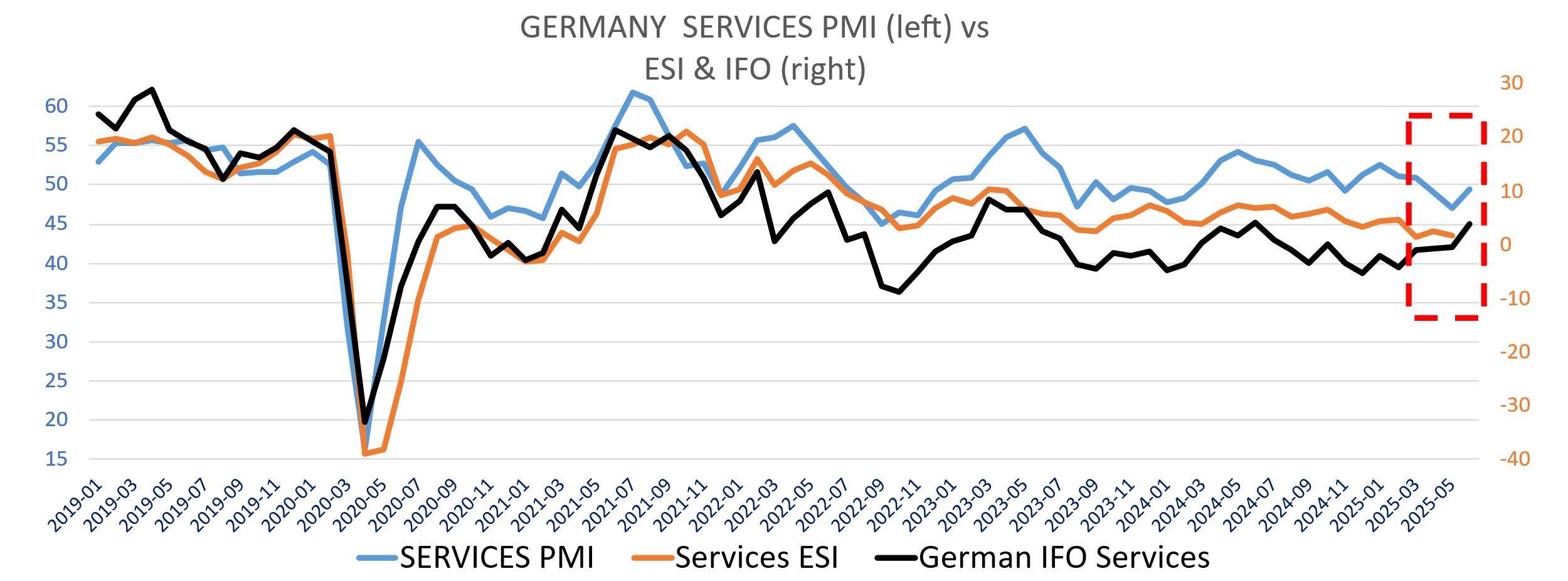

Services posting the strongest increase in business climate, turning positive to +3.8 for the first time since last October (-0.4 in May) and the highest in one year. Manufacturing barely improved to -13.7 from -13.8 in May but also the highest level since June 2024. The current assessment is down for manufacturing (- 3 points at -20.8) and about unchanged for services (+0.7 point to 11.4). Business expectations are up sharply, +3.4 points to -6.3 for Manufacturing (best since April 2023) and up 7.3 points or services to -3.6 for services, the highest since February 2022.! The changes are consistent with yesterday’s German Flash PMI which showed a sharper improvement in Services as well.

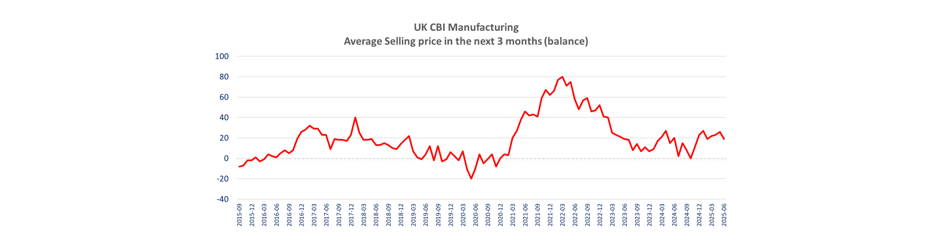

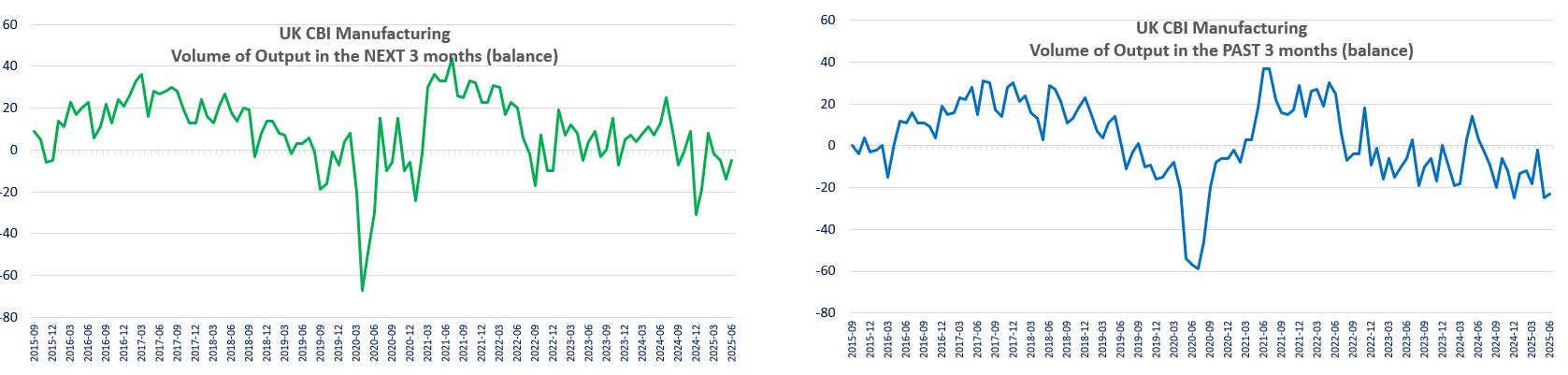

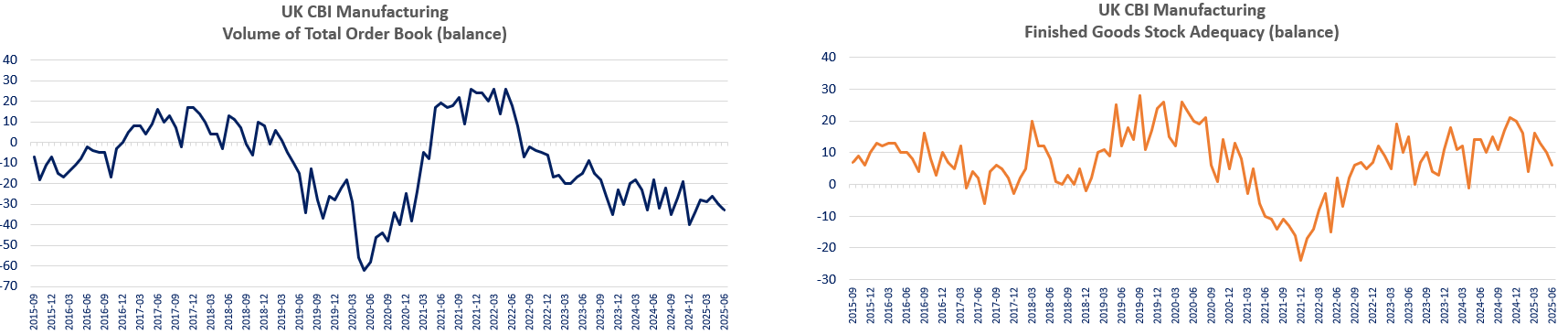

In the UK, The CBI manufacturing is disappointing for orders and past output but output expectations are improving as well. One other positive from the BoE standpoint is that selling price expectations are down (19% vs 26% balance). The net balance of new orders is down to -33 from -30, lowest since January when expectations were for an improvement to -27 even as export orders’ balance improved to -26 from -29. The CBI points to lower output in the past 3 months but by less than in May at –23 vs -25. Producers expected the decline in output to ease further in the next 3 months with a balance of -5 (was -14 in May).

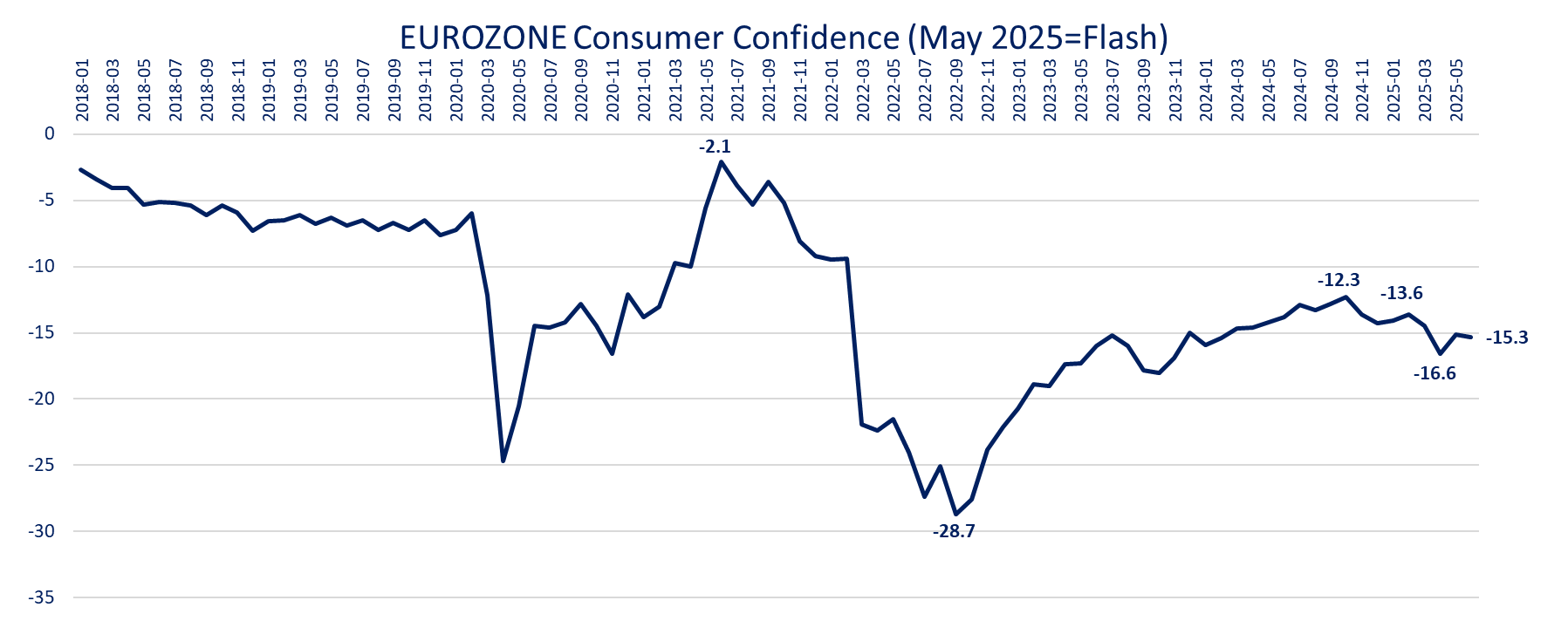

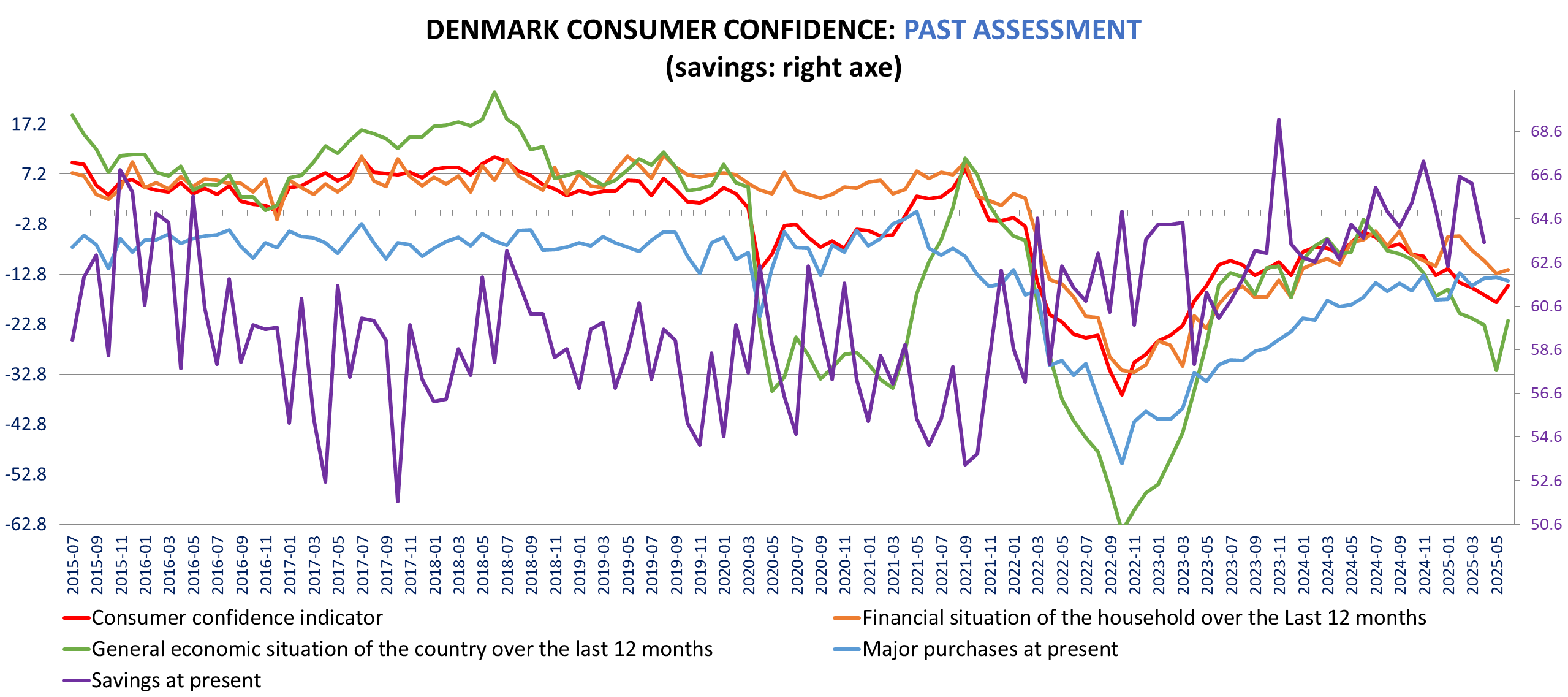

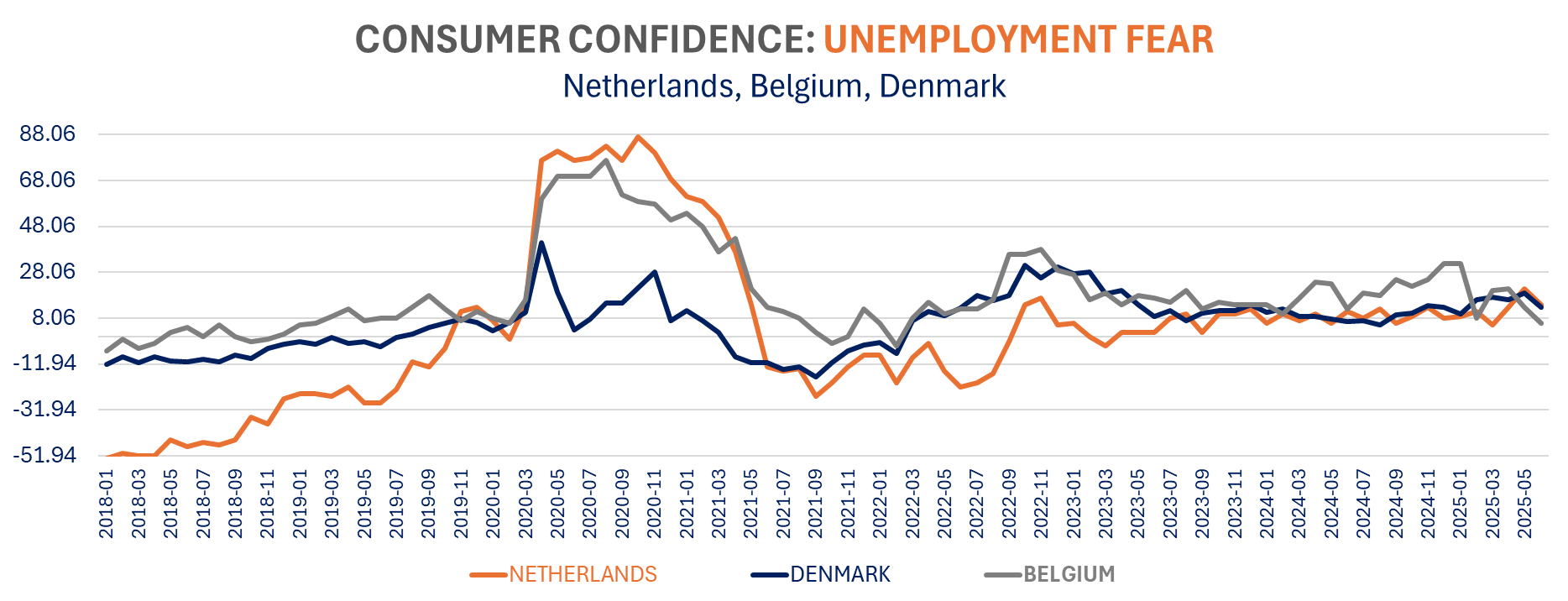

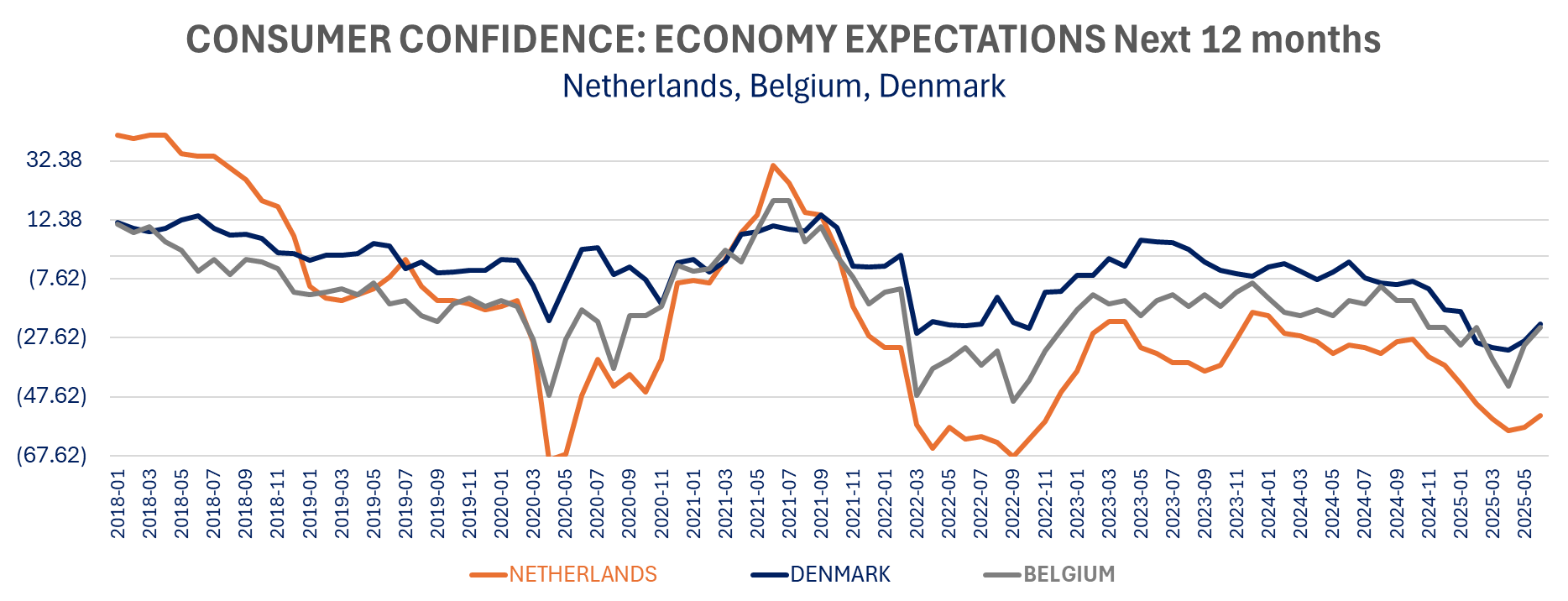

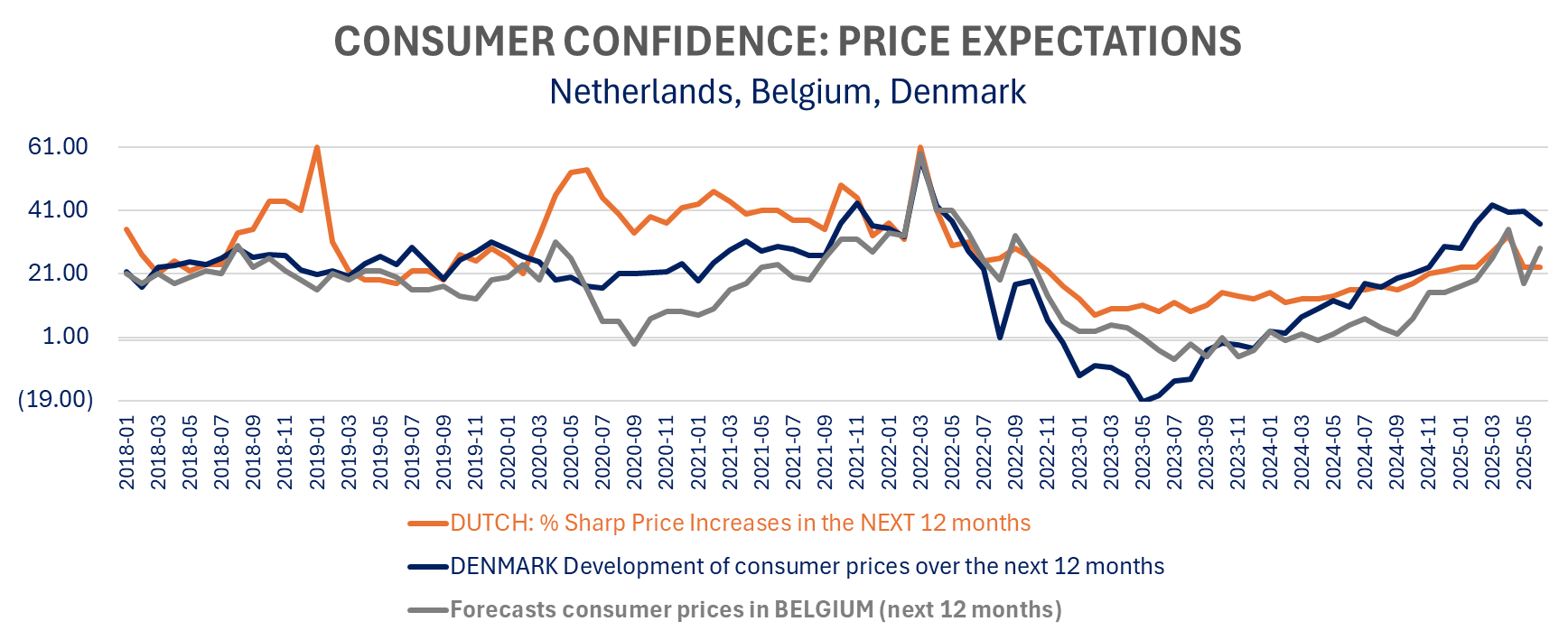

The June Eurozone consumer confidence flash release (Friday) disappointed at -15.3 down from -15.1 in May below expectations of -14.5. The decline comes even as we saw improvement in the Dutch consumer confidence and Belgian consumer confidence in the last few days. Denmark consumer confidence is also higher in June, up to -15.1 from -18.4, the highest since February. The data exhibits a similar trend than the Dutch or Belgian consumer confidence, with a less negative view on the general economy, and lower unemployment fear. Danish consumers price expectations are down when they were up in Belgium and flat in Holland though (see charts).

Bond Yields are moving higher on the back of the ceasefire but also the better German data. The front end of the UK is doing better post the CBI, pointing to lower price pressure. The Eurozone PMI yesterday, on the other hand did point to renewed selling price pressure in services.

On the companies’ front: Alstom will supply SNCF Voyageurs with 96 additional RER NG trainsets for the RER D line in order to complete and renew the fleet on this line. Financed at 100% by Île-de-France Mobilités, this order worth around €1.7 billion is part of the framework agreement signed in 2017 between SNCF Voyageurs and Alstom. The European Central Bank has cleared Monte dei Paschi di Siena's proposed acquisition of rival Mediobanca, a source with knowledge of the matter told Reuters. Over the period 2025/28 FDJ United expects to achieve an average annual organic revenue growth of around 5% and a recurring EBITDA margin of over 26% by 2028, driven by operating leverage combined with the efficiency measures taken by FDJ UNITED. Novo Nordisk announced the launch of weight-loss drug Wegovy in India. Wegovy, a once-a-week injection, will be in pharmacies by the end of the month, Novo said. It will compete against Eli Lilly's Mounjaro who hit Indian markets in March. Novo Nordisk also announced that Ozempic receives EU recommendation in peripheral arterial disease, for people with type 2 diabetes and comorbidities. AstraZeneca and its Japanese partner Daiichi Sankyo scored an accelerated approval from the US Food and Drug Administration for Datroway as a treatment for a type of advanced lung cancer that has become resistant to past therapies More details on equities here

CRACKS in NATO

Dollar Index, not a safe haven status, only minor bid during the “12 days war”, more due to positioning than flight quality

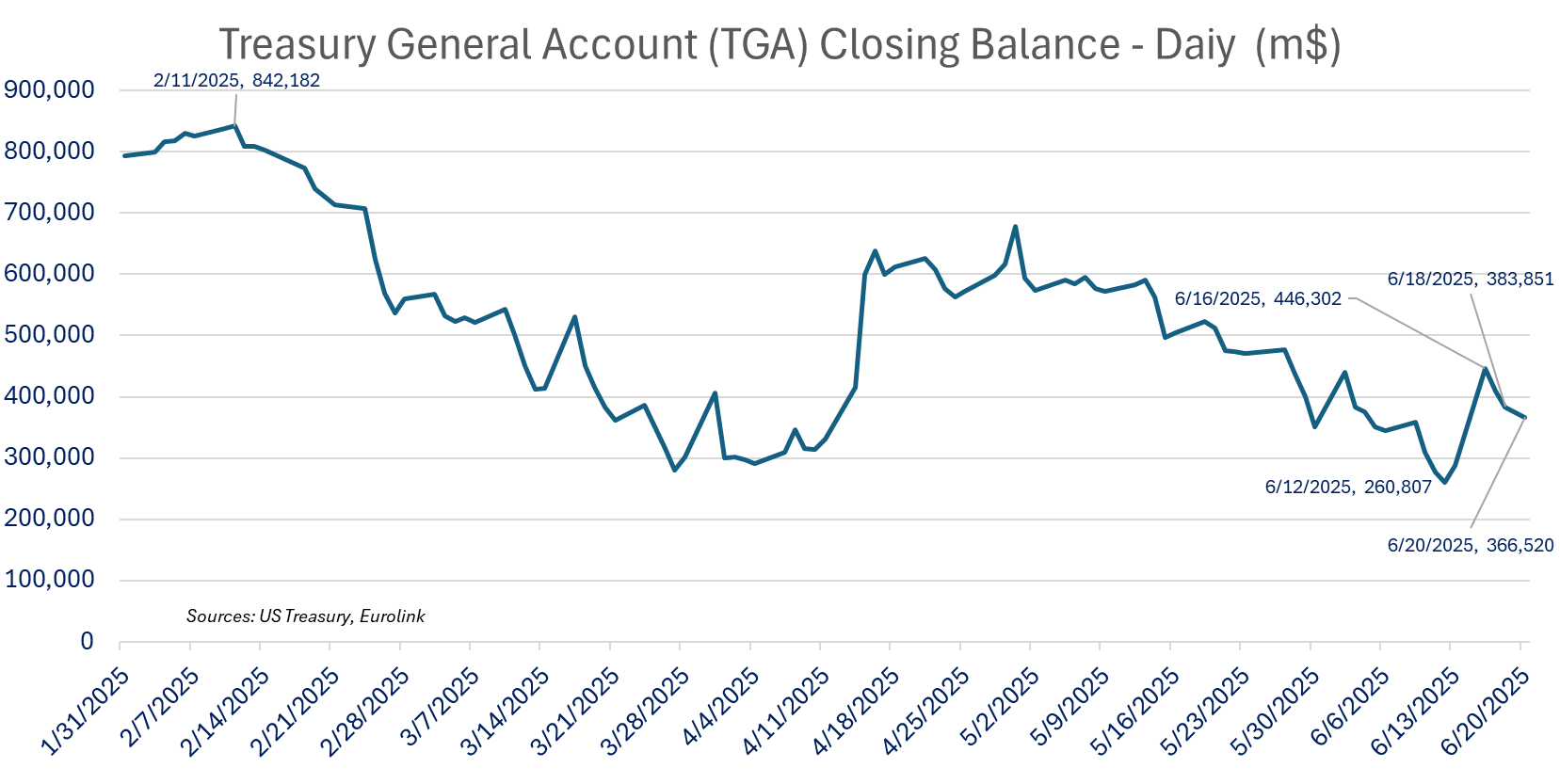

US TREASURY TGA MOVE AROUND TAX PAYMENTS

The Daily data (end of Day) highlights the greater tax receipts in June. The TGA jumped above $400bn to $446bn on June 16, but are declining fast since, down to $366bn on June 20. (The latest Balance sheet update was on June 18)

The German IFO Business Climate index increased to the highest in 13 months in June to 88.4 from 87.5 beating consensus expectations of 88.2. The improvement comes from an increase in Business expectations to 90.7 from 89 (revised from 88.9), the highest level in more than 2 years (April 2023) and above consensus of 90. Expectations are still below the long-term average of 95.6. Current assessment remained gloomy though, at 86.2 barely up from 86.1 in May and below consensus of 86.5. Expectations are up in all sectors except retail while current assessments are about unchanged or down in all sectors but wholesale.

All Sectors but retailing saw an improvement in the climate index with services posting the strongest increase, turning positive to +3.8 for the first time since last October (-0.4 in May) and the highest in one year. Manufacturing barely improved to -13.7 from -13.8 in May but also the highest level since June 2024. The changes are consistent with yesterday’s German Flash PMI with a sharer improvement in Services as well.

The current assessment is down for manufacturing (- 3 points at -20.8) and about unchanged for services (+0.7 point to 11.4), but expectations are up sharply, +3.4 points to -6.3 for Manufacturing (best since April 2023) and up 7.3 points or services to -3.6 for services, the highest since February 2022.

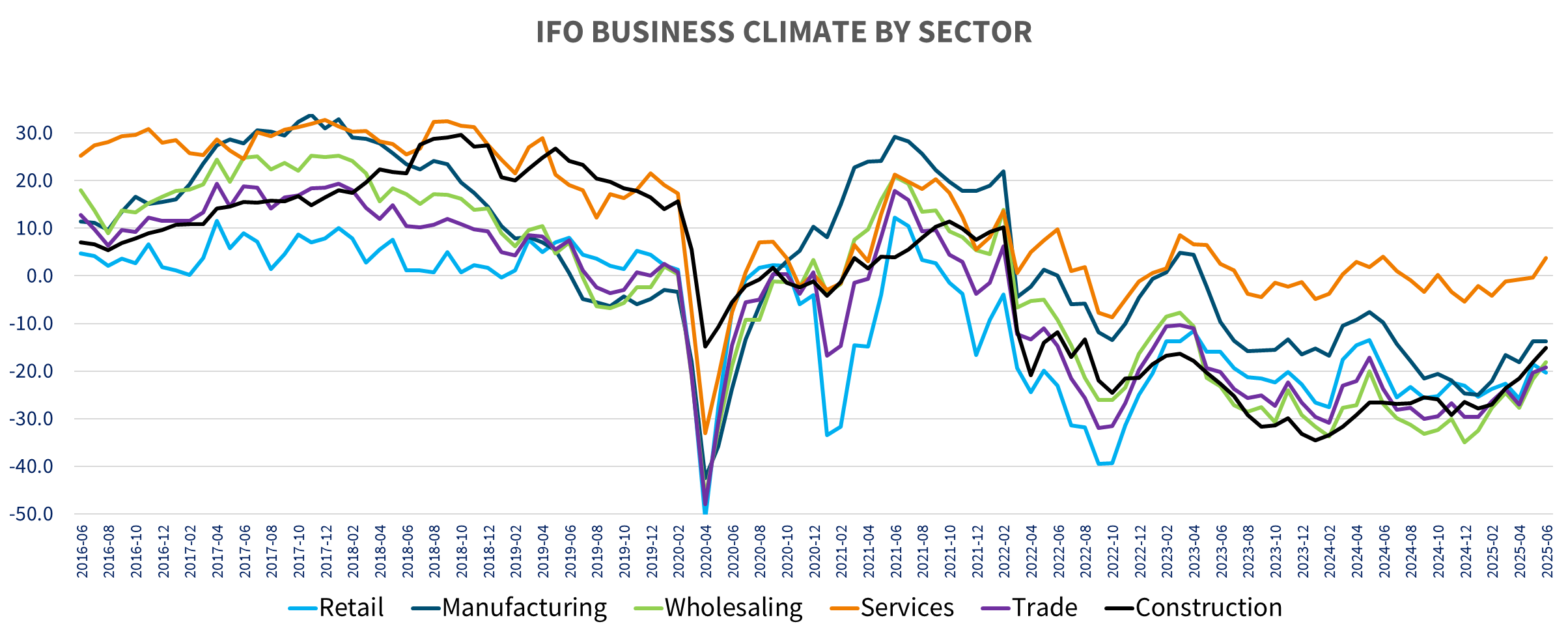

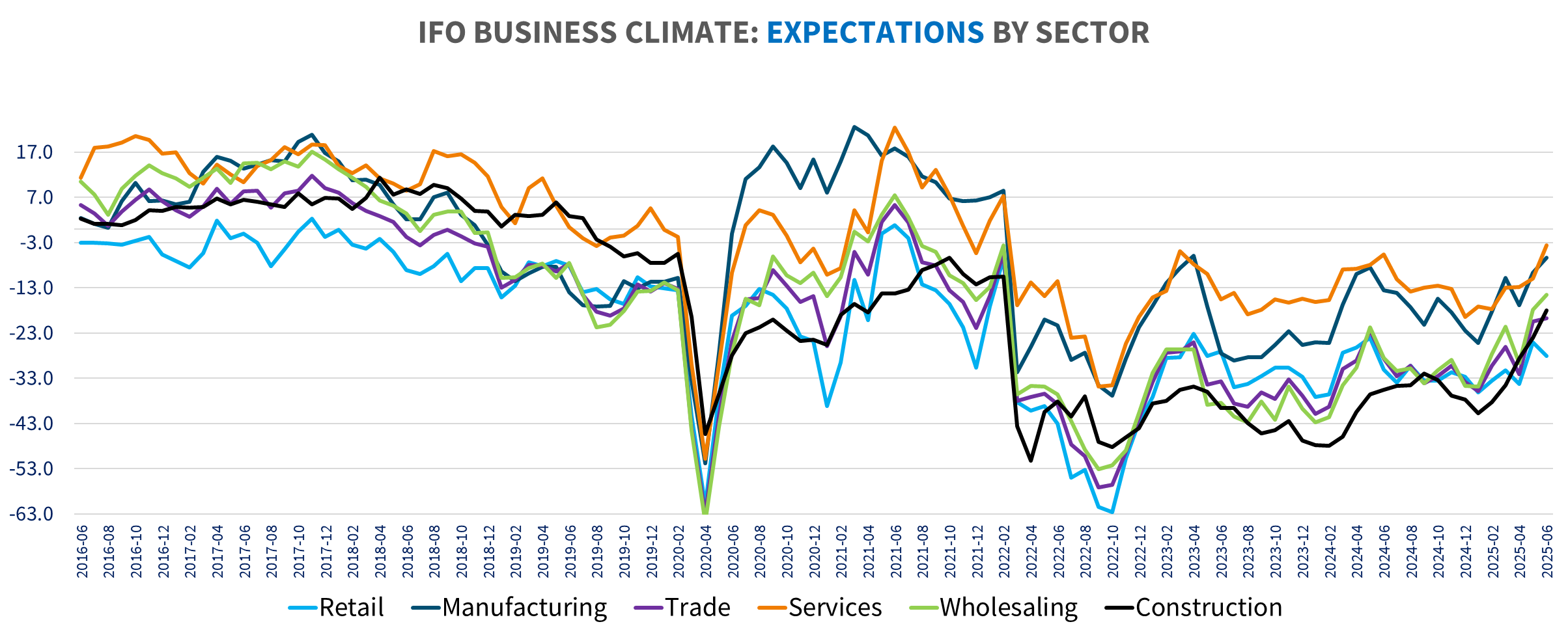

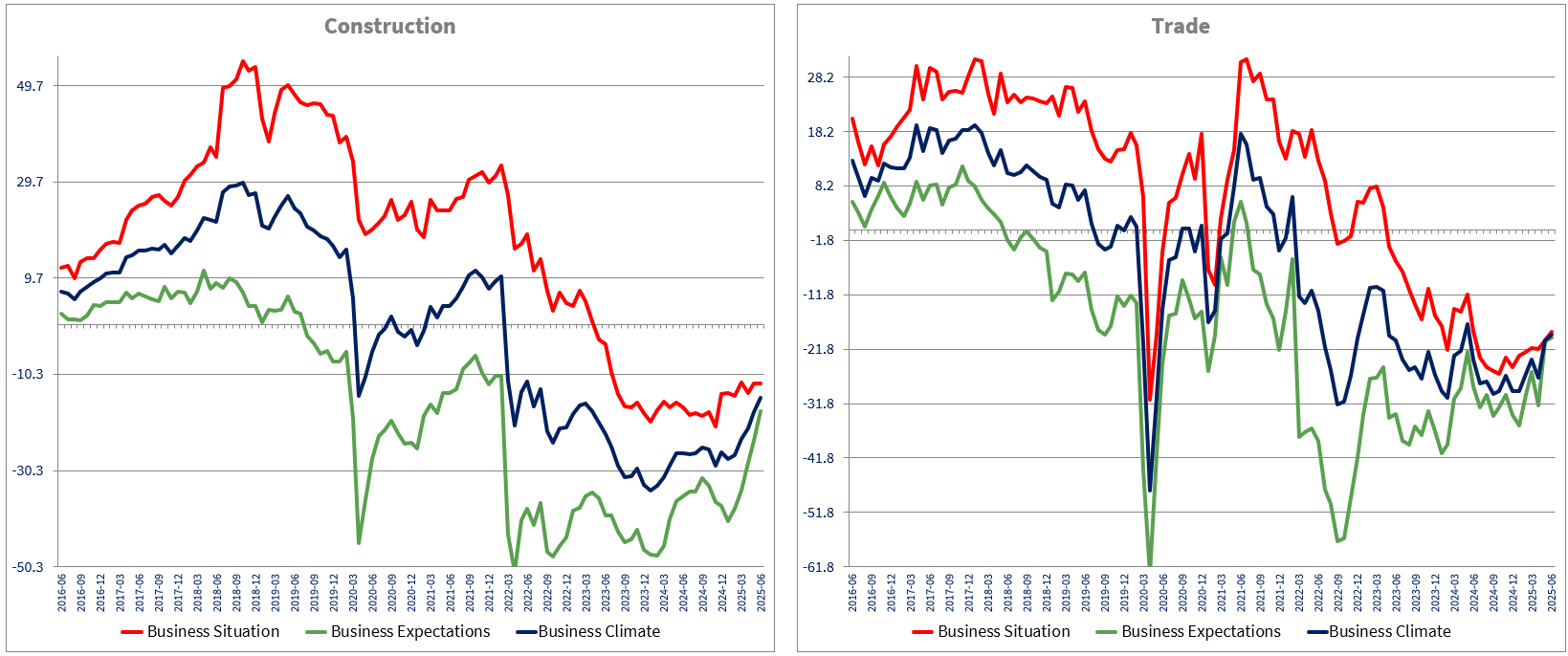

Sentiment also improved for construction, also driven t by expectations. the Construction climate increased 3 points to -15.1 (best since August 2022), current assessment being unchanged at -12.1 but expectations increasing 6 points to -18, best since February 2022.

Trade improved slightly to -19.2 form -20.3 but driven by improvement in the current situation (+1.6 to -18.6, one year high), and driven by wholesale, improving to18.1 from -21.7 with both higher current assessment and expectations. Retail sentiment declined to -20.3 form -18.6 with lower expectations (-3 points to -28.1) and minor decrease in current assessment (-0.2 point to -12.1 from -11.9), all only at 2 months low.

EUROZONE CONSUMER CONFIDENCE - FLASH

The Eurozone Flash consumer confidence published by the EU commission last Friday was below expectations. It fell slightly to -15.3 from -15.1, below economists’ consensus for an increase to -14.5 and remains below average.

The Danish June consumer confidence published yesterday is up to -15.1 from -18.4, the highest since February. The data exhibits a similar trend than the Dutch or Belgian consumer confidence, improving with less negative view on the general economy, and lower unemployment fear. Danish consumers price expectations are down when they were up in Belgium and flat in Holland (see charts).

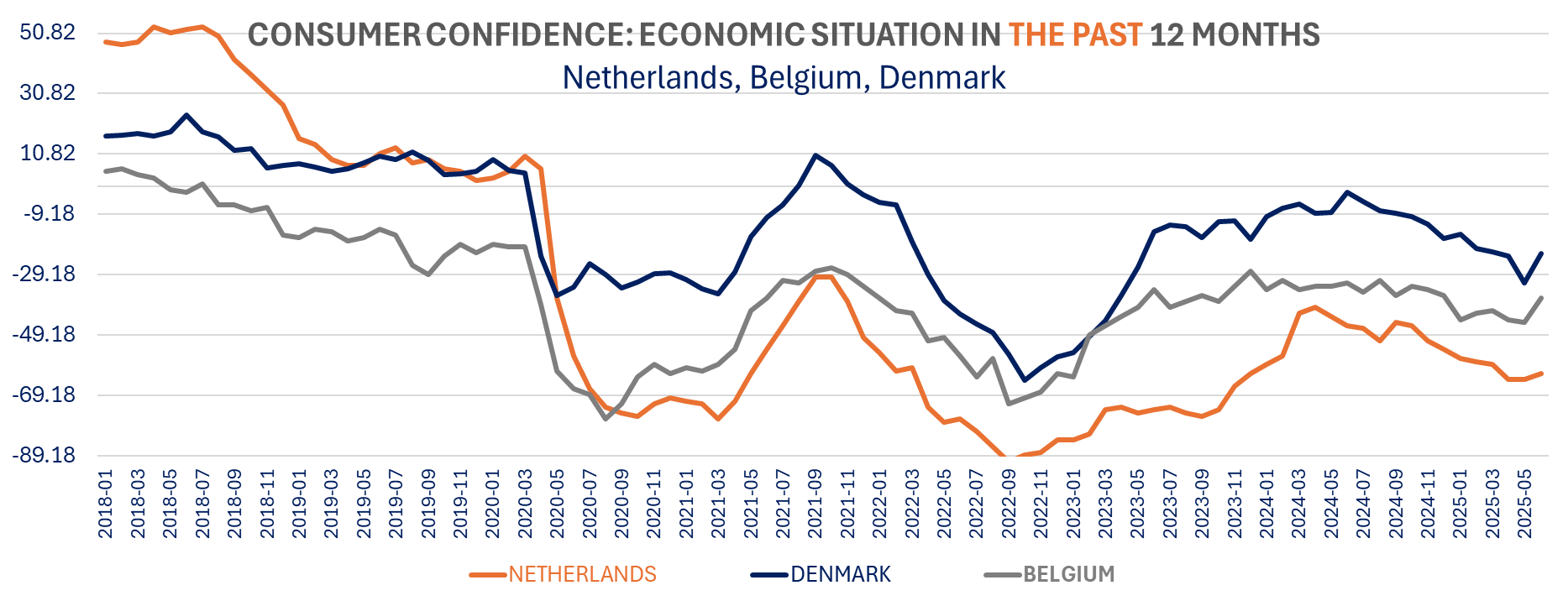

Danish Consumers balance regarding the economic outlook in the past 12 months in up significantly to -22.1 from -32. The balance for the economic outlook increased to -22.8 from -28.6. We see a smaller improvement for the personal financial situation: past -11.9 vs -12.7 and future -4.7 vs -5.5. Households are more negative about making large purchases and are less inclined to save. As mentioned, we have a significant decline in unemployment fear, down to 12.9 from 19.1, the lowest in 6 months. Denmark consumers past prices assessments are higher (47.3 vs 44, the highest since May 2023), bit prices expectations are down to the lowest since January at 36.7 vs 40.8 in May.

Comparison Belgium, Netherlands & Denmark

Lower unemployment fear and less negative on the economy

The June UK CBI Manufacturing survey is weaker than expected with the net balance of new orders down to -33 from -30, lowest since January when expectations were for an improvement to -27. Export orders’ balance improved to -26 from -29.

UK manufacturers are also pointing to lower output in the past 3 months but by less than in May at –23 vs -25 after he sharp improvement in April (-2). Producers expected the decline in output to ease further in the next 3 months with a balance of -5 (was -14 in May).

Manufacturers judge finished goods inventories more adequate in June than in May at +6 vs +10 (below average). UK manufacturers selling price expectations eased to +19 from +26% remaining above average.

The CBI says output declined in 14 out of the 17 sub-sectors covered “with the declined riven by the chemicals, metal products and mechanical engineering sub sectors.”

|

|

Tuesday, June 24, 2025 | ||

|

ALO |

Alstom SA | ||

|

EUR |

19.73 |

+7.23% | |

|

ALO |

Alstom will supply SNCF Voyageurs with 96 additional RER NG trainsets for the RER D line in order to complete and renew the fleet on this line. This order, formalized by SNCF Voyageurs, follows the vote on the financing agreement by Île-de-France Mobilités Board of Directors on 10 April 2025. | ||

|

|

|

|

|

|

BMPS |

Banca Monte dei Paschi di Siena SpA | ||

|

EUR |

7.35 |

+6.32% | |

|

BMPS |

The European Central Bank has cleared Monte dei Paschi di Siena's proposed acquisition of rival Mediobanca, a source with knowledge of the matter told Reuters. A spokesperson for the ECB declined to comment. The decision was taken by the ECB's supervisory board via a written procedure. It is now set to be rubber stamped by the policymaking governing council of the ECB. | ||

|

|

|

|

|

|

FDJU |

FDJ United | ||

|

EUR |

33.36 |

+2.58% | |

|

FDJU |

Capital Market Day. FDJ announces its financial and non-financial strategy and goals for 2028. Over the period 2025/28 FDJ expects to achieve an average annual organic revenue growth of around 5% and a recurring EBITDA margin of over 26% by 2028, driven by operating leverage combined with the efficiency measures taken by FDJ UNITED. Year-on-year dividend growth, reflecting the Group’s performance and medium-term outlook, based on a payout ratio of at least 75% of adjusted net profit. By business activity: The French lottery and retail sports betting BU, The main driver of growth over the period 2025-2028 is expected to be the influx of more than one million additional players, compared with 27 million players in 2024.3 This influx will be driven both by the expansion of the point-of-sale network to cover large food retailers – which could account for 20% of the physical network by 2028, to offset closures in the traditional network of bar-tobacco-press outlets – and by the development of the online channel, which is expected to account for 20% of lottery revenue by 2028. The Online betting and gaming BU’s ambition is to expand its positions in all | ||

|

|

|

|

|

|

NVO |

Novo Nordisk A/S | ||

|

USD |

457.50 |

+1.60% | |

|

NVO |

Novo Nordisk announced the launch of weight-loss drug Wegovy in India. Wegovy, a once-a-week injection, will be in pharmacies by the end of the month, Novo said. It will compete against Eli Lilly's Mounjaro who hit Indian markets in March. | ||

|

|

|

|

|

|

AZN |

ASTRAZENECA PLC | ||

|

GBp |

10390.00 |

-0.29% | |

|

AZN |

Datroway (datopotamab deruxtecan or Dato-DXd) has been approved in the US for the treatment of adult patients with locally advanced or metastatic EGFR-mutated non-small cell lung cancer (NSCLC) who have received prior EGFR-directed therapy and platinum-based chemotherapy. Following approval in the US, an amount of $45 million is due from AstraZeneca to Daiichi Sankyo as a milestone payment for the locally advanced or metastatic EGFR-mutated NSCLC indication. Sales of Datroway in the US are recognized by Daiichi Sankyo. | ||

Versus early hours:

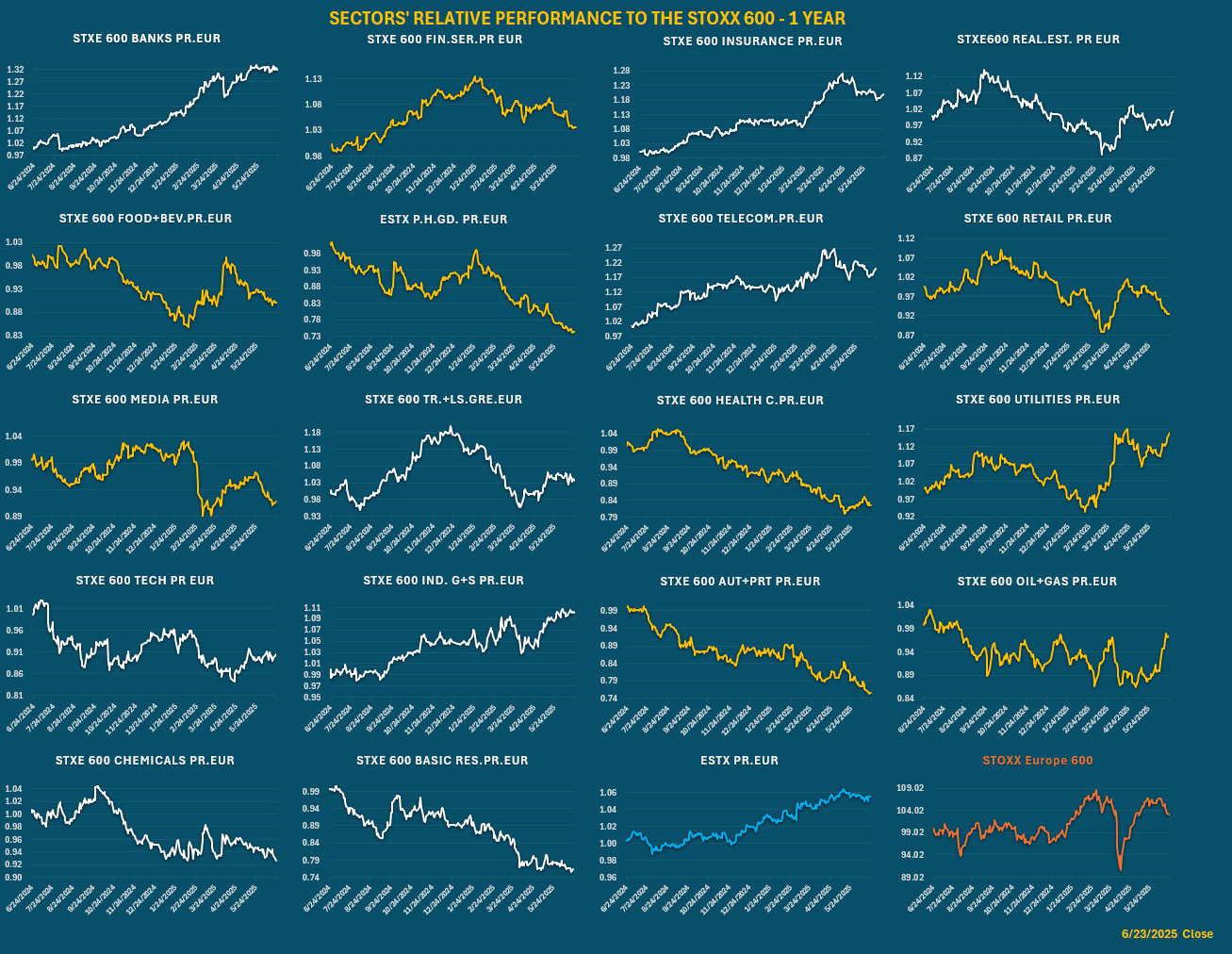

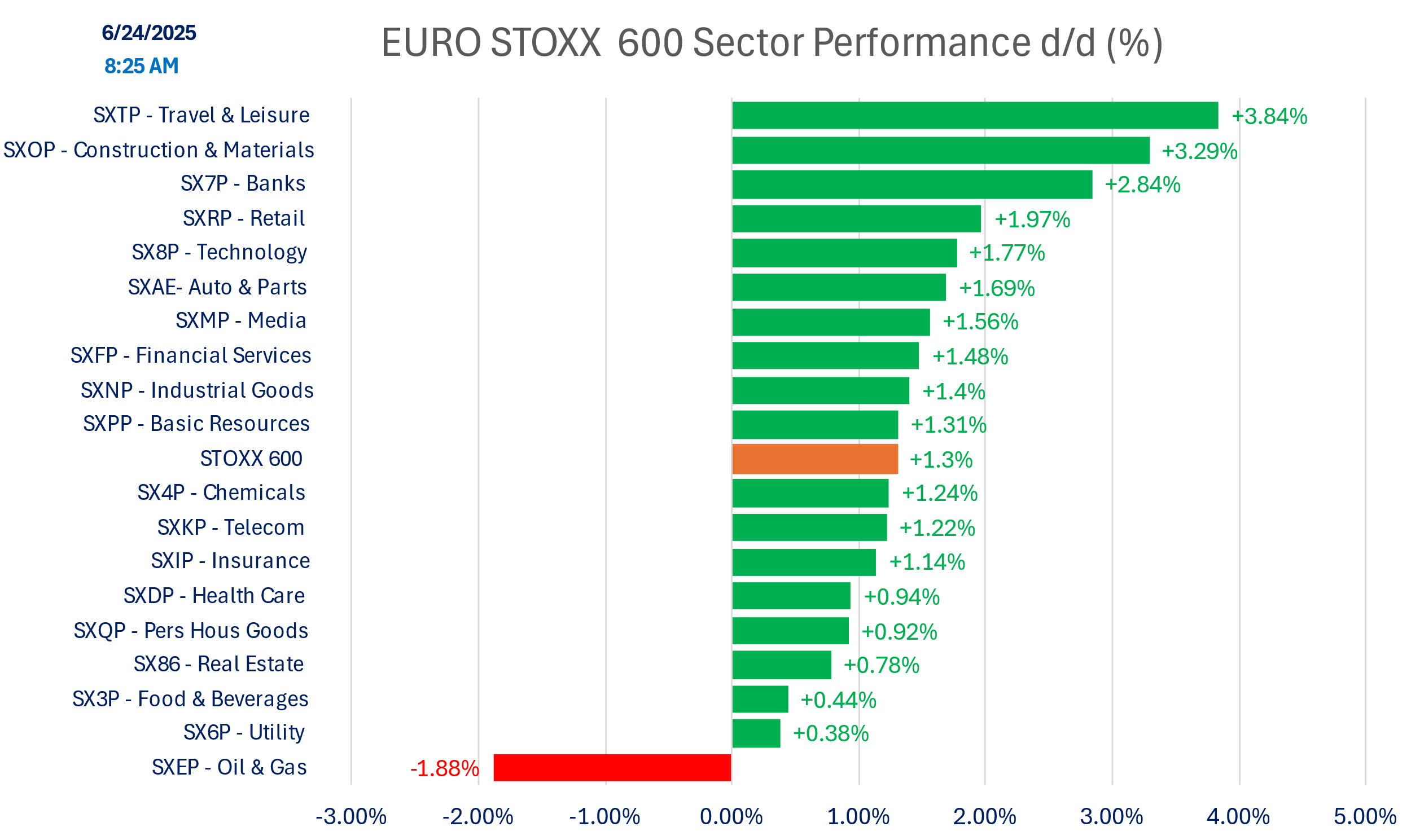

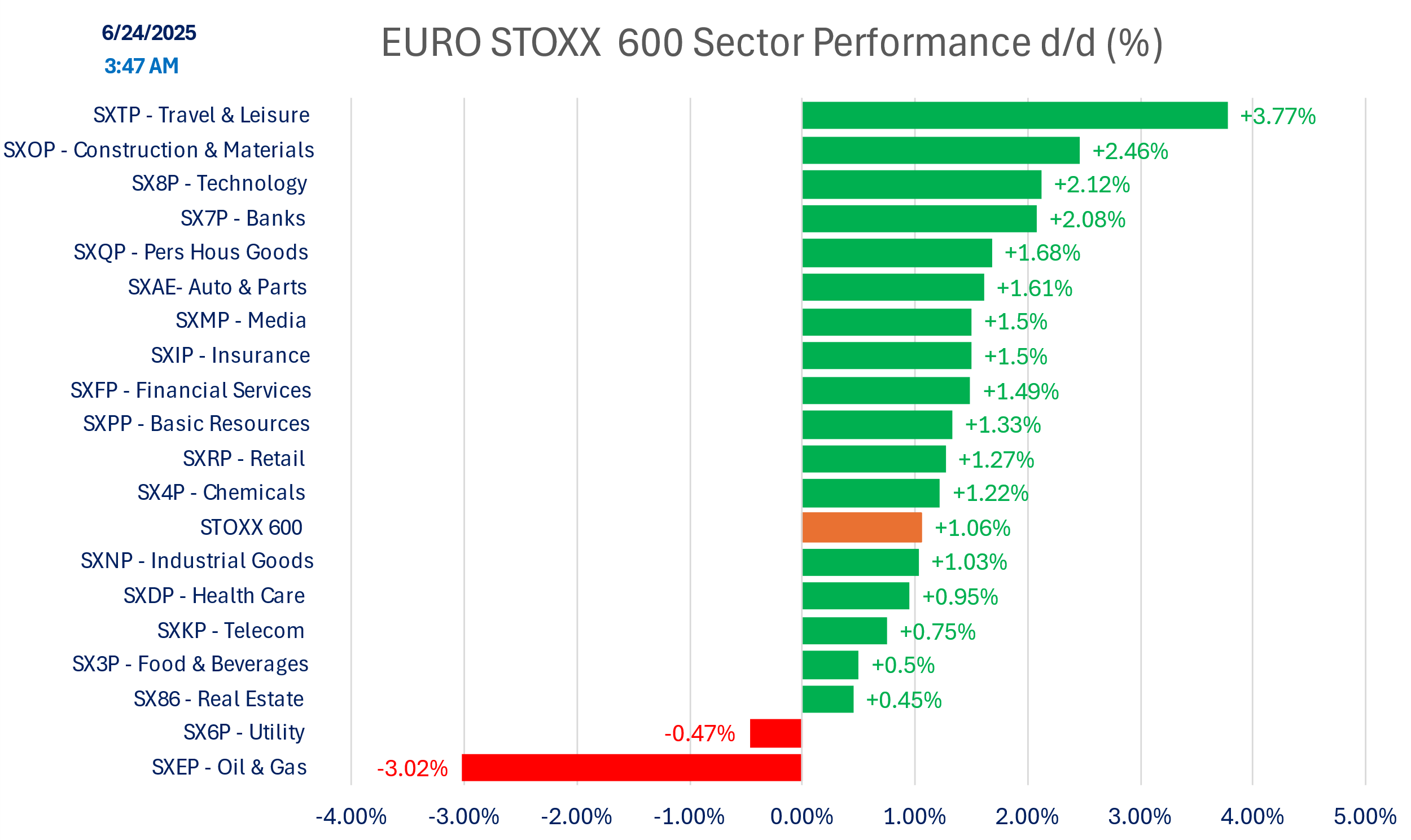

SECTOR PERFORMANCE

Relative performance to STOXX 600

Today’s Performance

Versus early hours:

Indices

Versus early hours

Commodities

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.