A larger number of macro data in Europe ahead of next week’s PMI, but markets are moving with geopolitical headlines. Yields initially down on concerns of possible US intervention reversed course on hope for a possible diplomatic solution. Excluding more enrichment for good would favor the military solution rather than the diplomatic, controlled option.

The $ did finally benefit slightly from the geopolitical situation in the last days with DCY index above 99 yesterday but the DXY is down on the back of these hopes. In Japan, core inflation was higher than expected (3.7% vs 3.6% expected) bringing back rate increase on the table. With the BOJ cautious on the rate front, a stronger yen would be a logical solution to manage lower imported inflation while limiting the impact on the bond side.

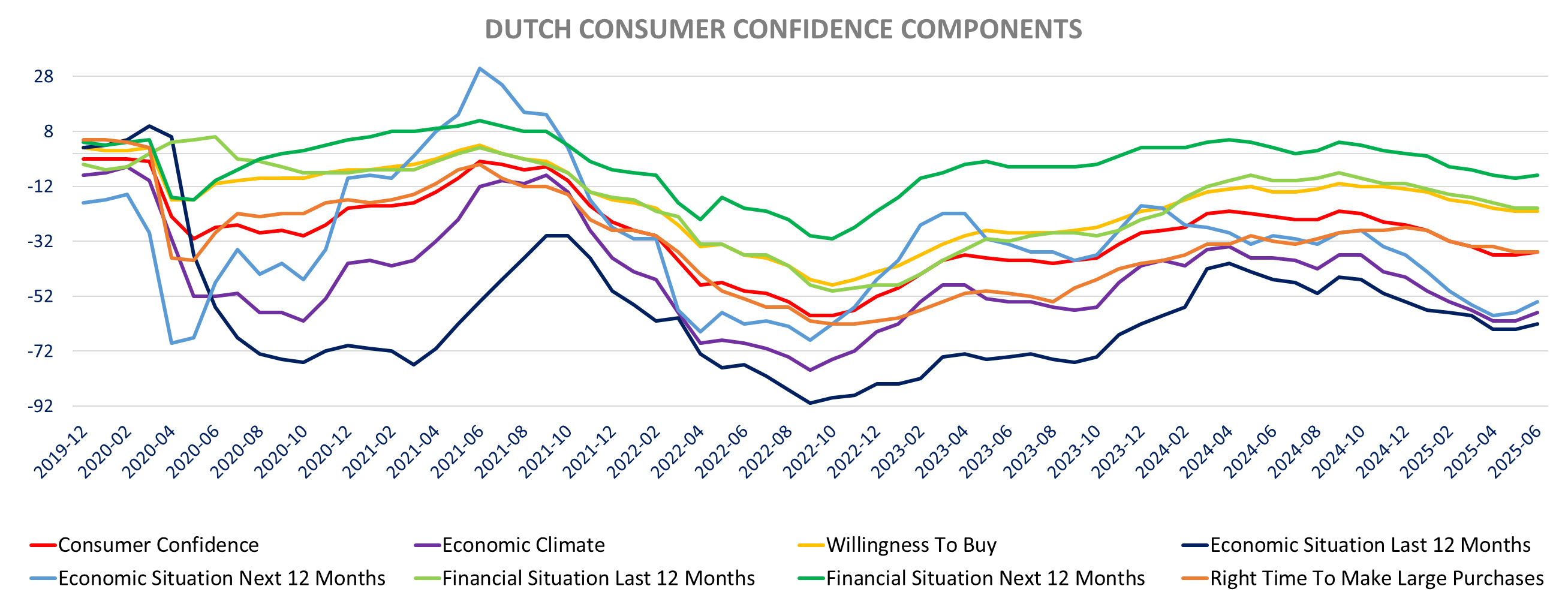

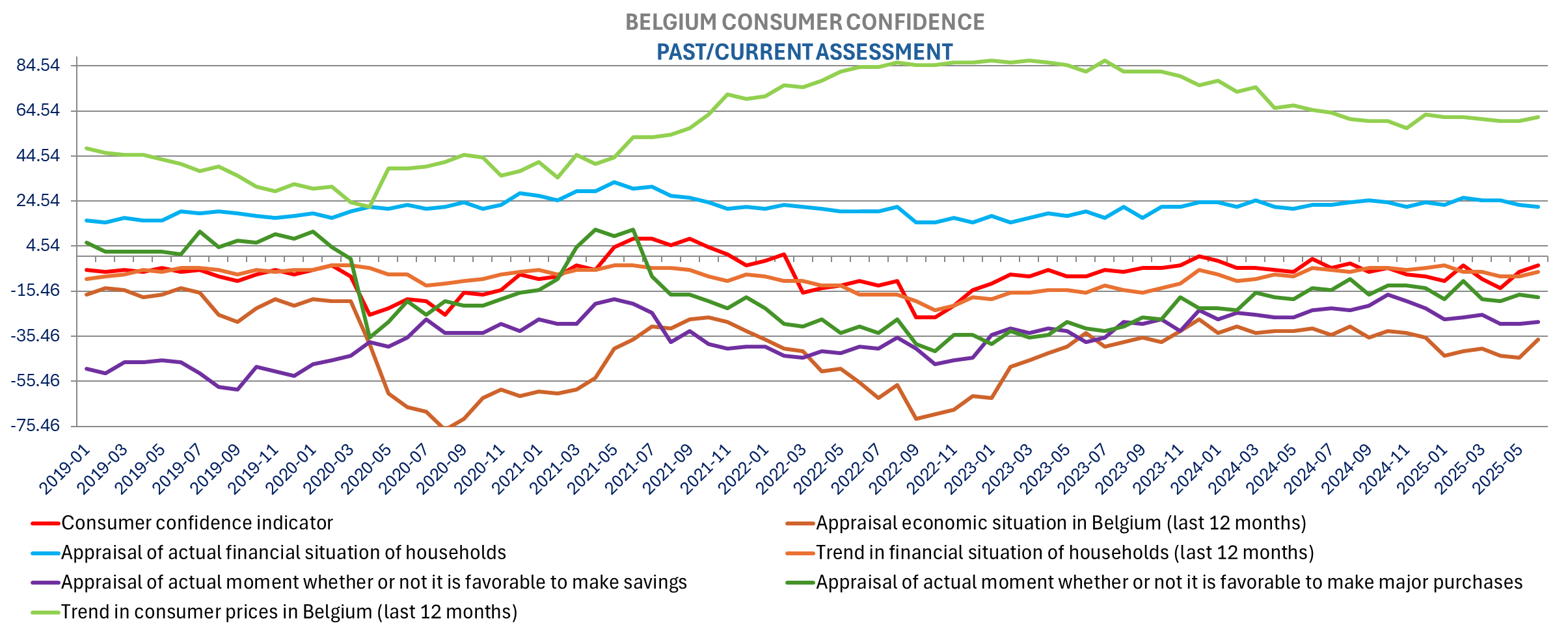

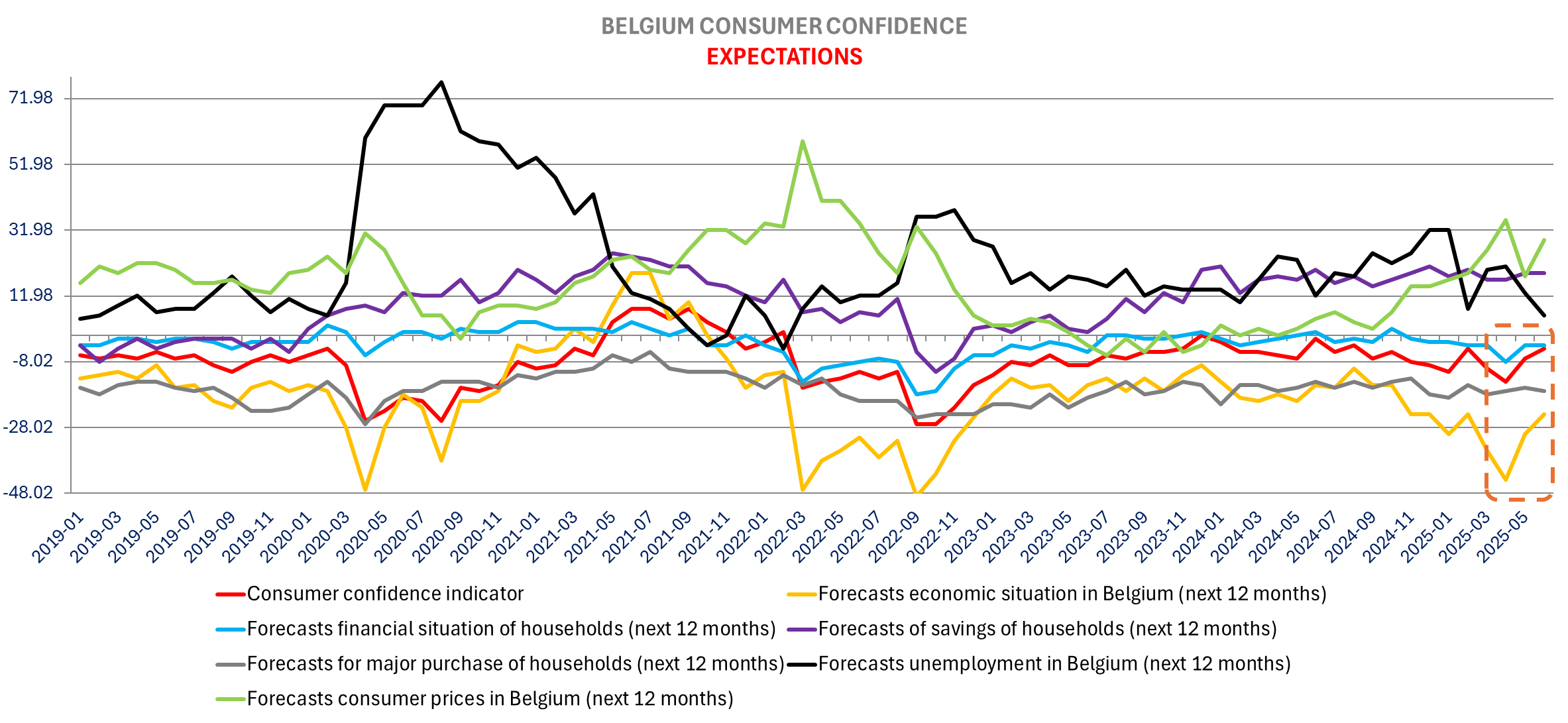

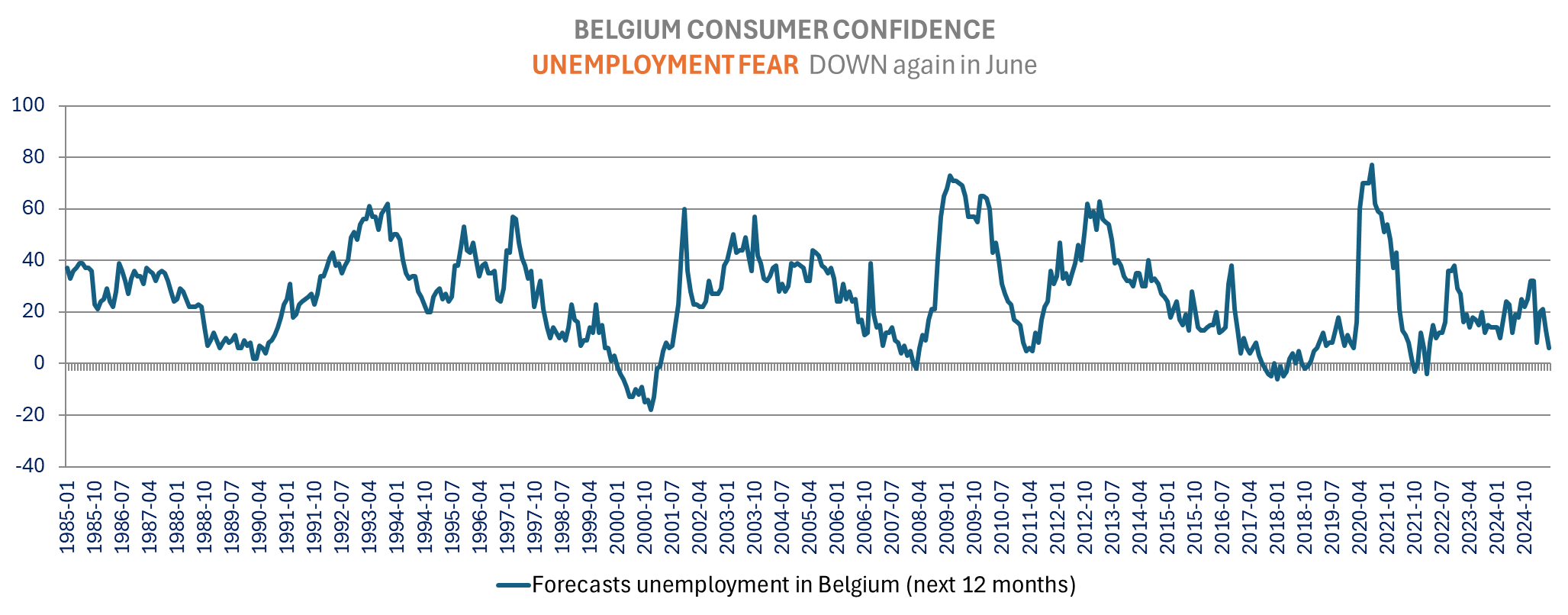

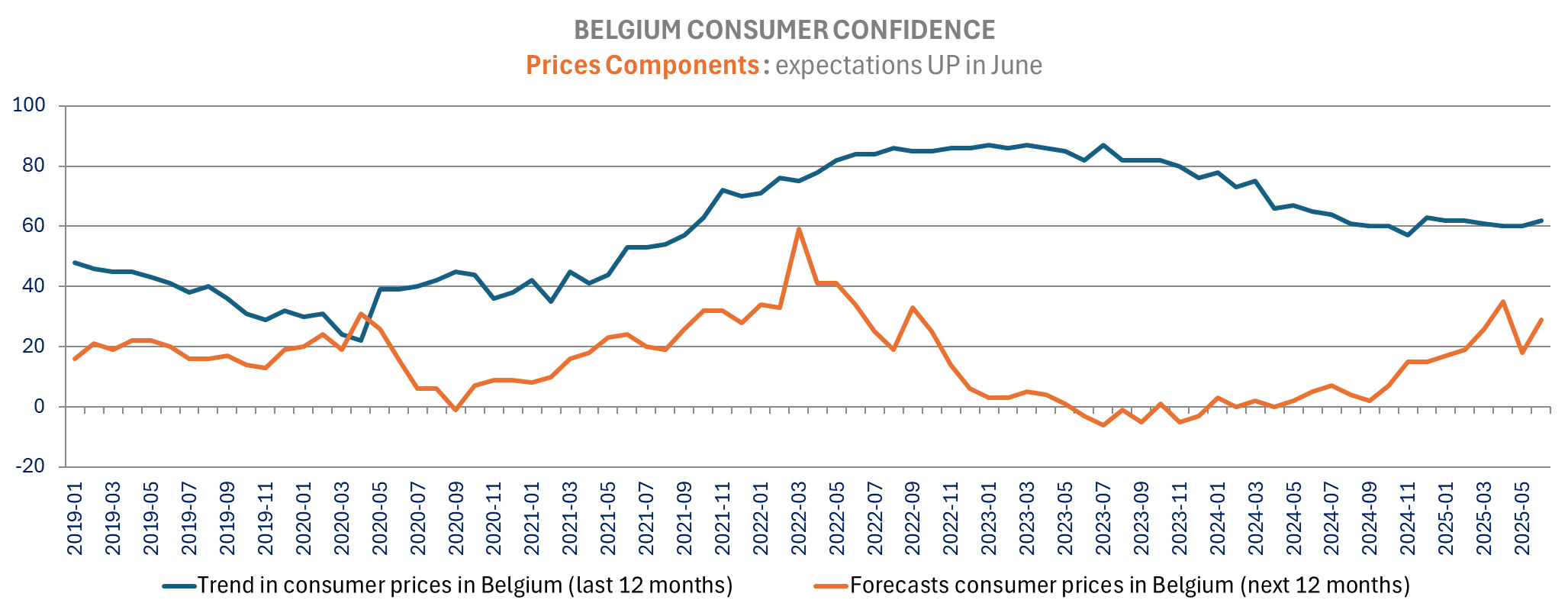

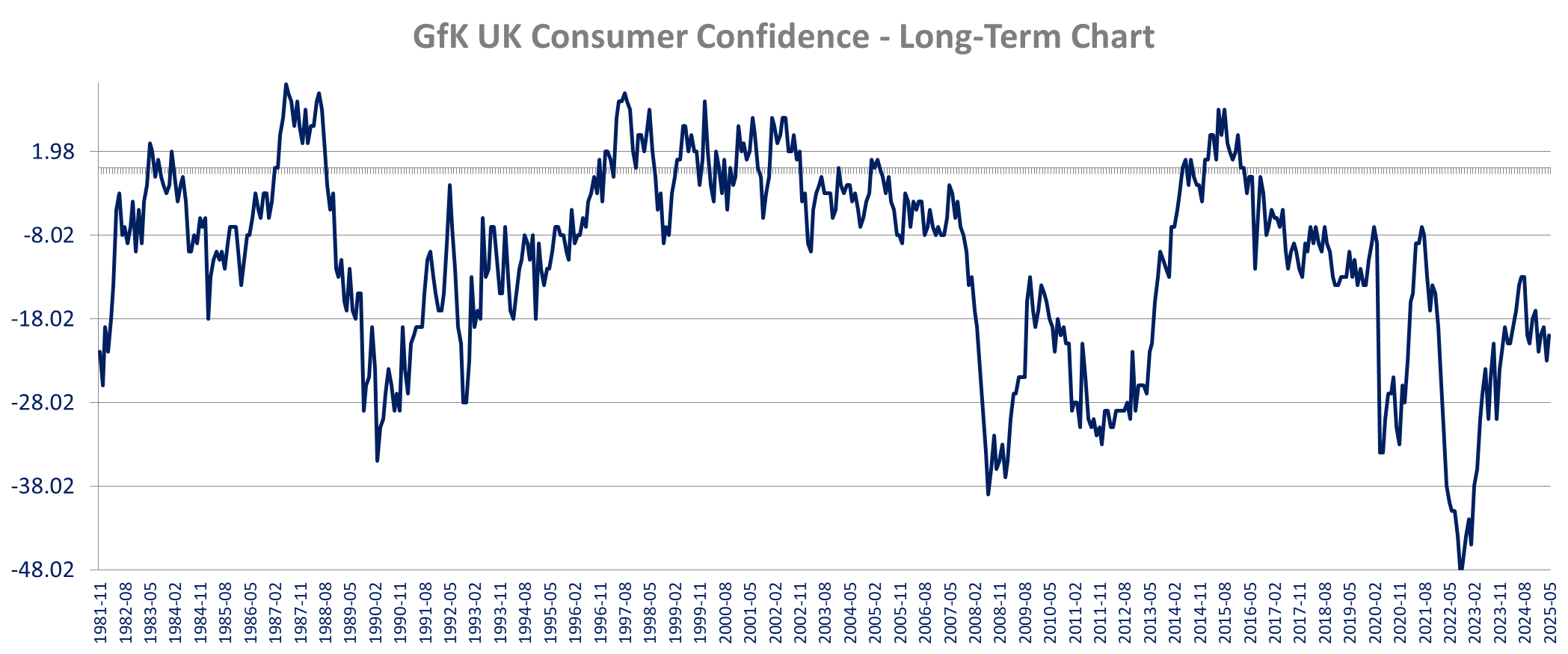

Consumer confidence improved in Belgium (-4 vs -7 , matching February’s level which was the highest since last August), The Netherlands (-36 from -37, best since March) and the UK (-18 vs -20 best since December)in June. In all three countries, sentiment improved on less negative view on the economy past & future after the higher concerns in April. Unemployment fear also eased significantly in Belgium and the Netherlands.

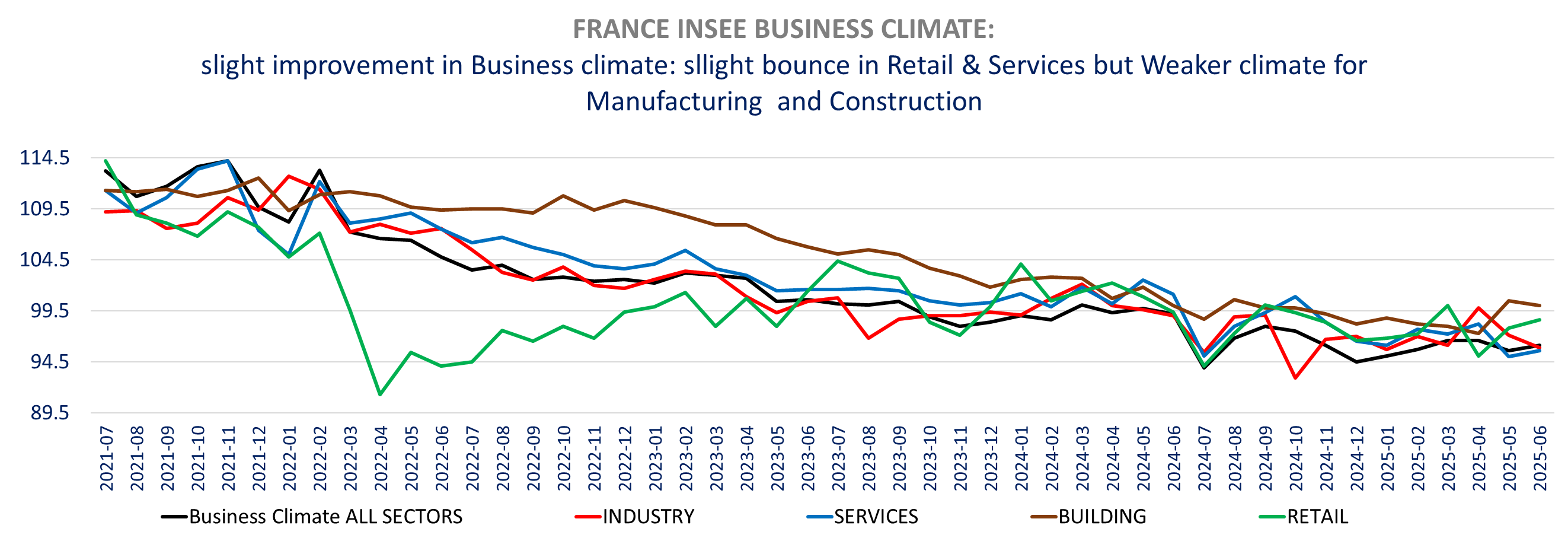

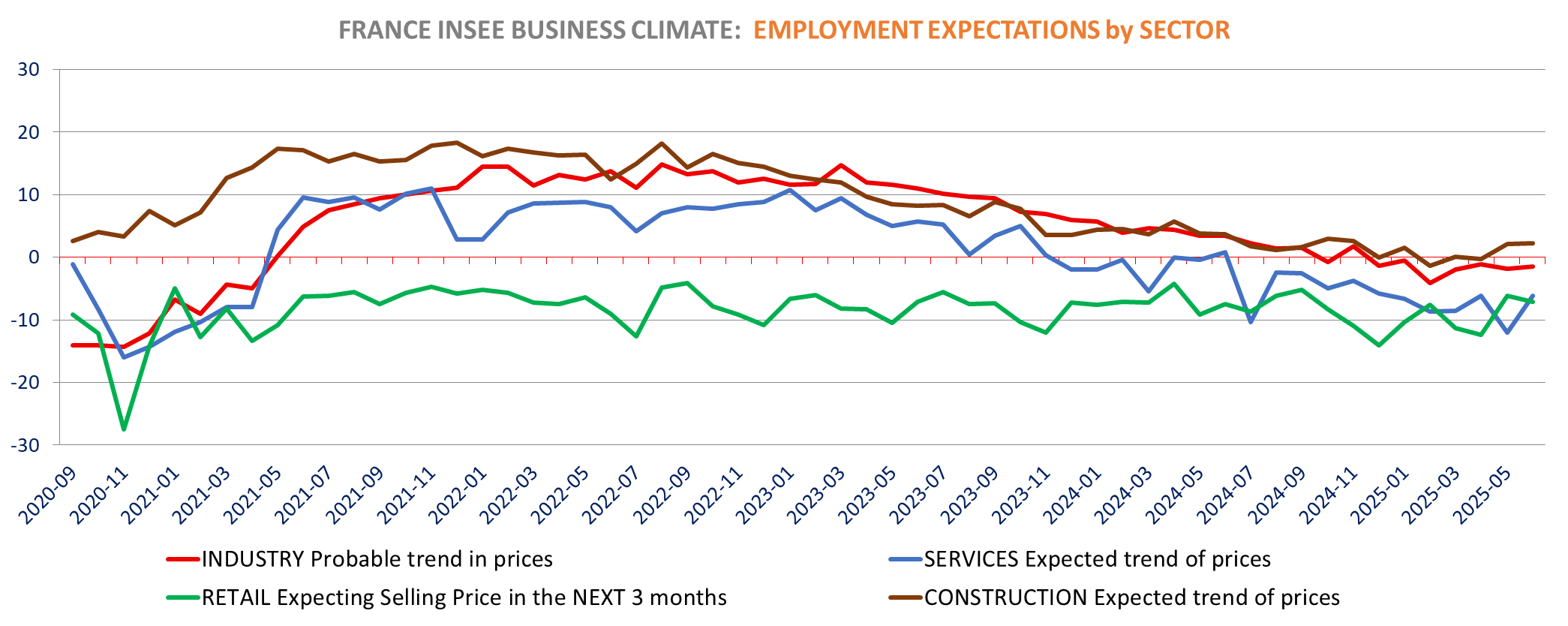

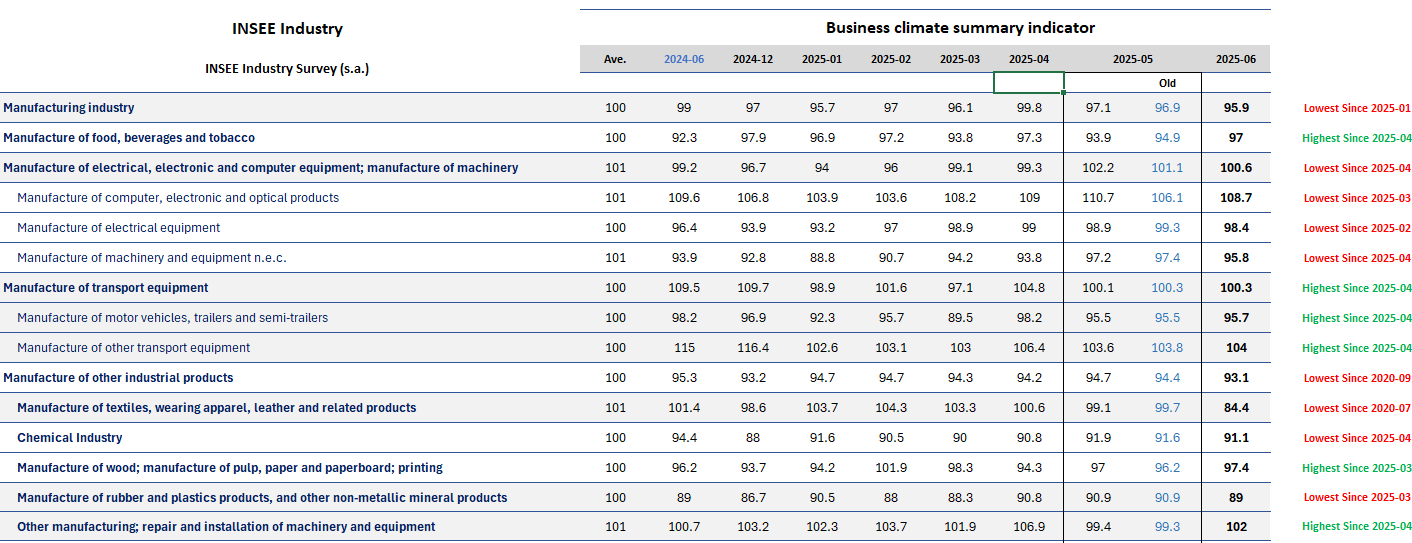

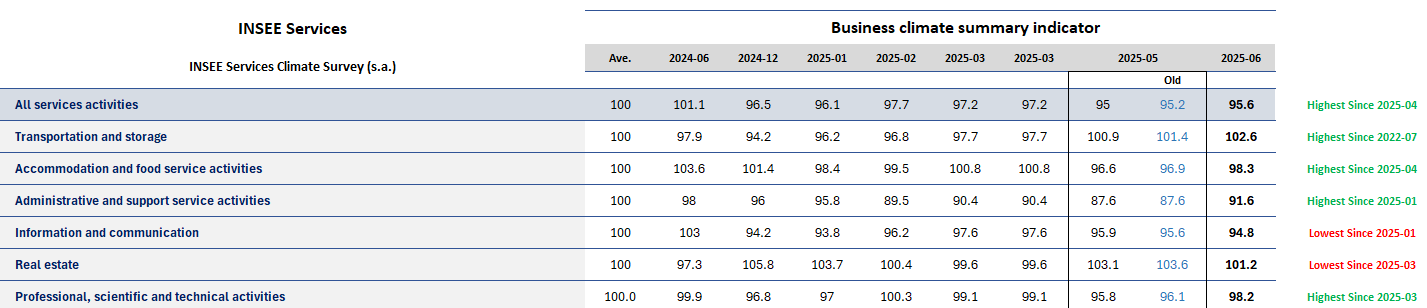

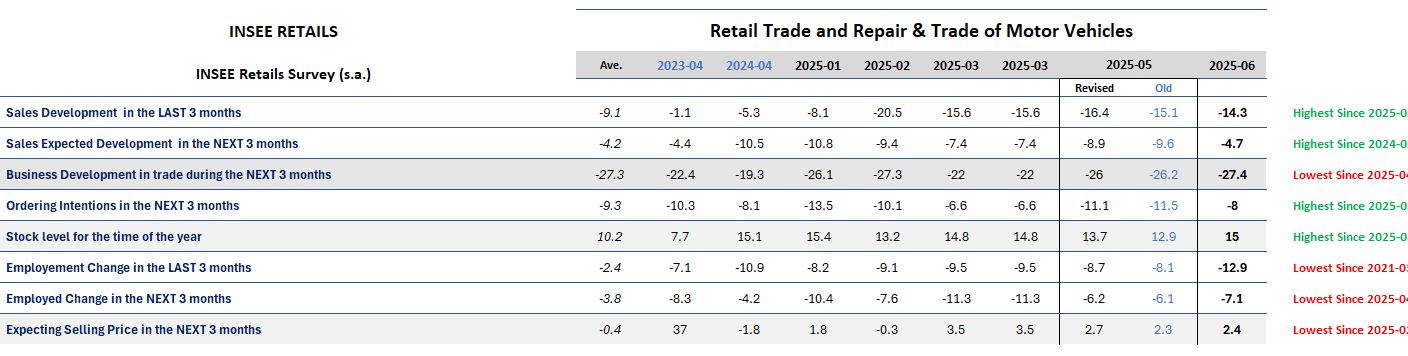

The French Business confidence improved slightly June to 96.1 from 95.6 in May (revised from 95.8) but reported as unchanged at 97. Manufacturing and construction climate is down but services and retail climates improved month-over-month. Services’ climate improved amid higher expectations for activity and demand. Within the INSEE business climate data we also see higher employment expectations (up in all sectors but Retail), consistent with the lower unemployment fear we see in Belgium and Holland and the latest employment, unemployment data we had across the Eurozone, all pointing towards good resilience.

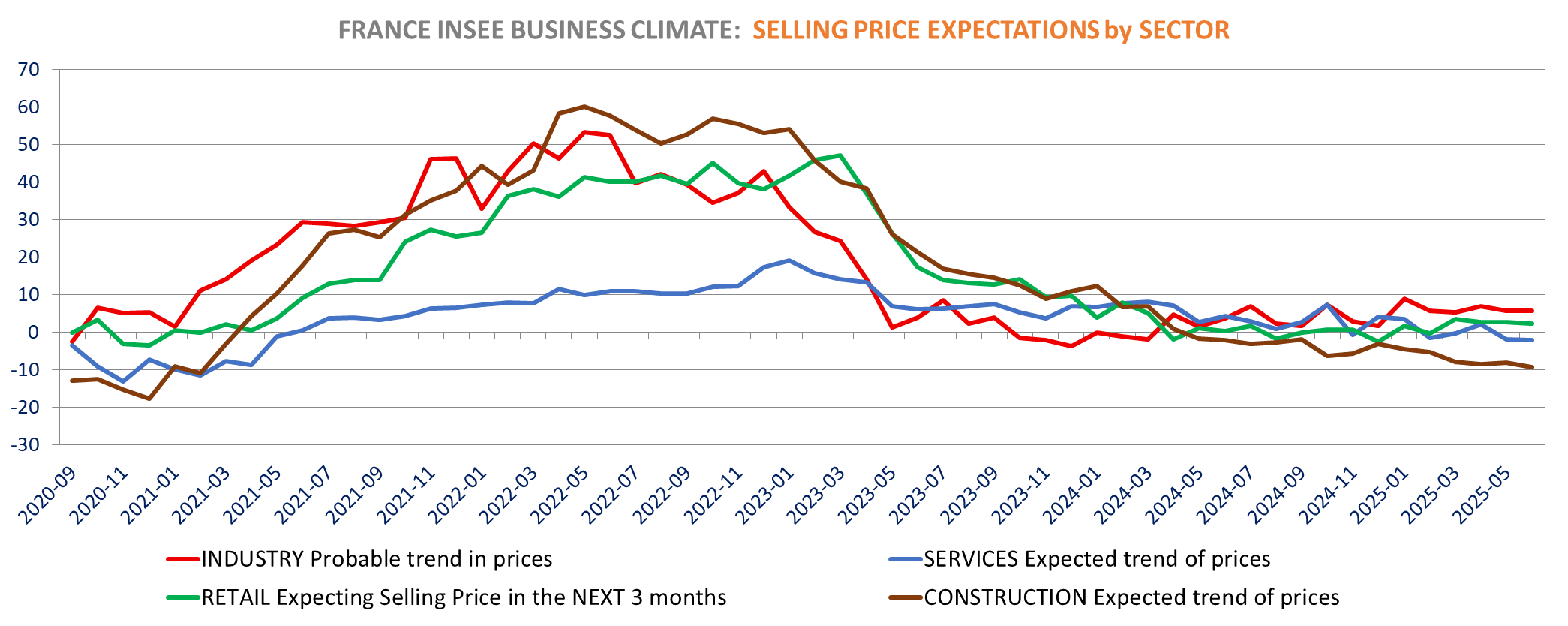

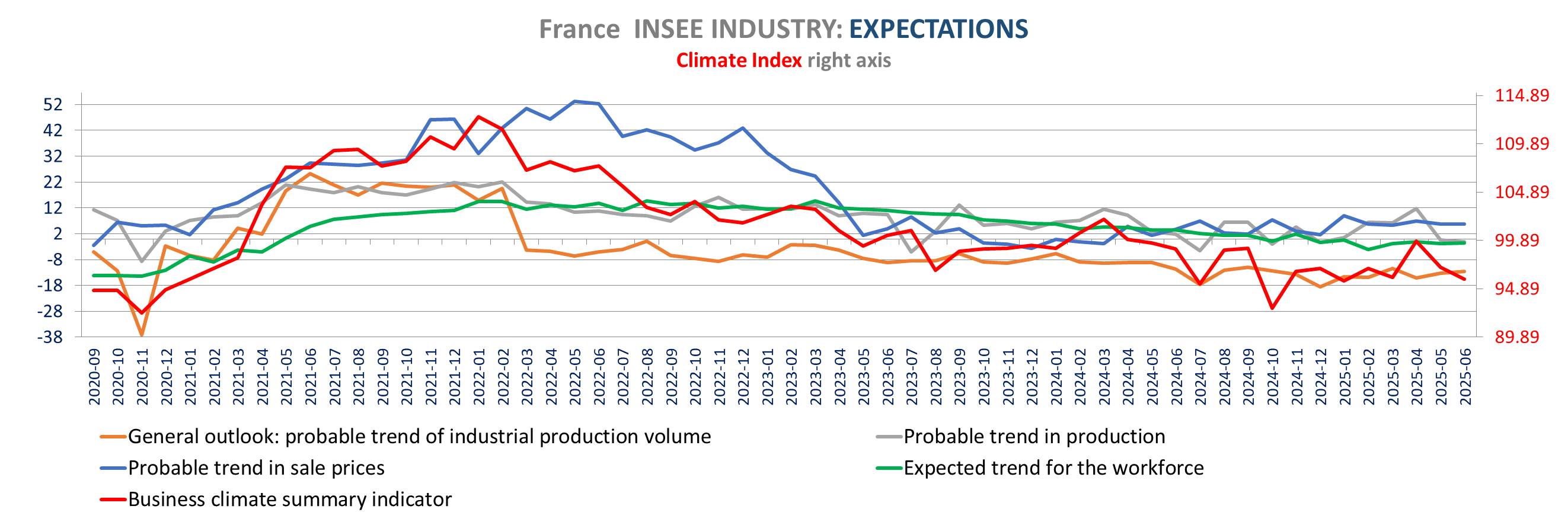

The INSEE Price expectations are lower and negative across sectors but manufacturing where the balance is at +5.8 unchanged from the revised May but higher than the preliminary data of 5.6.

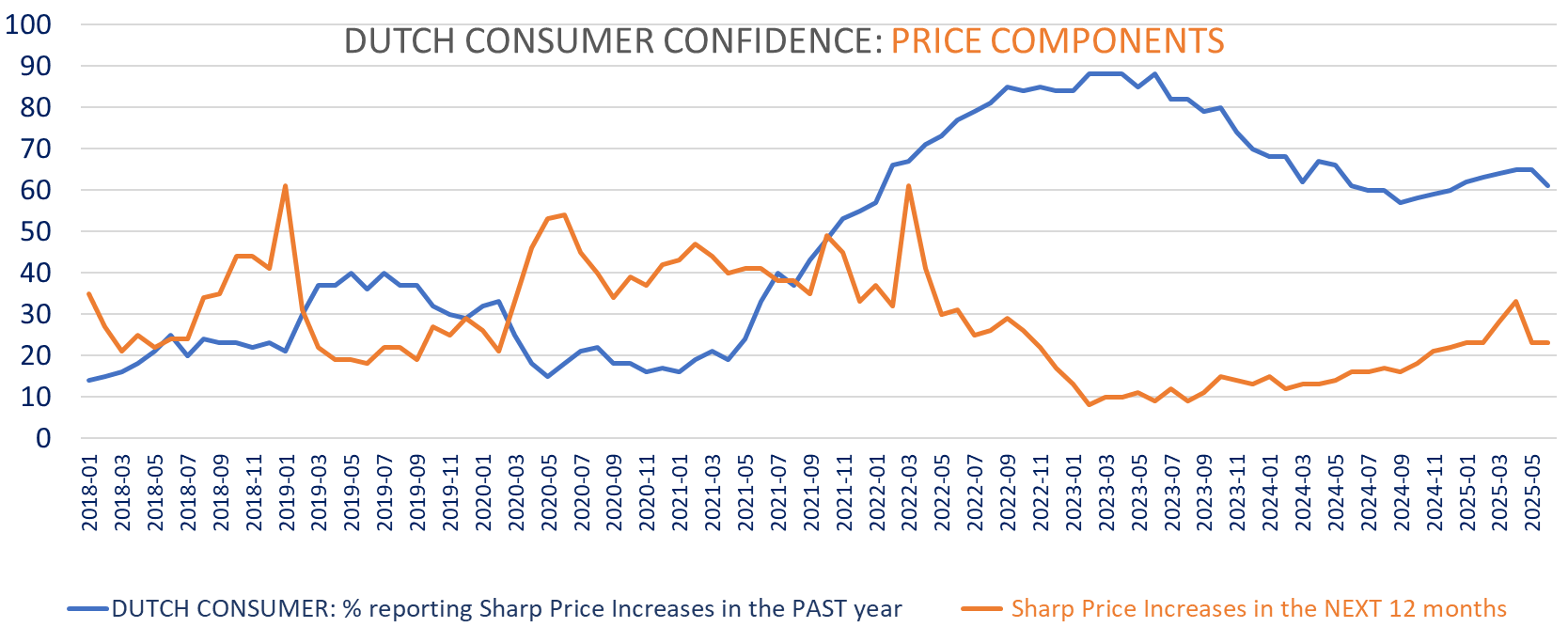

Price expectations also moderated in the Netherlands consumer sentiment data. On the other hand, price expectations are up in Belgium. PPI data in Germany, Portugal also were lower than expected.

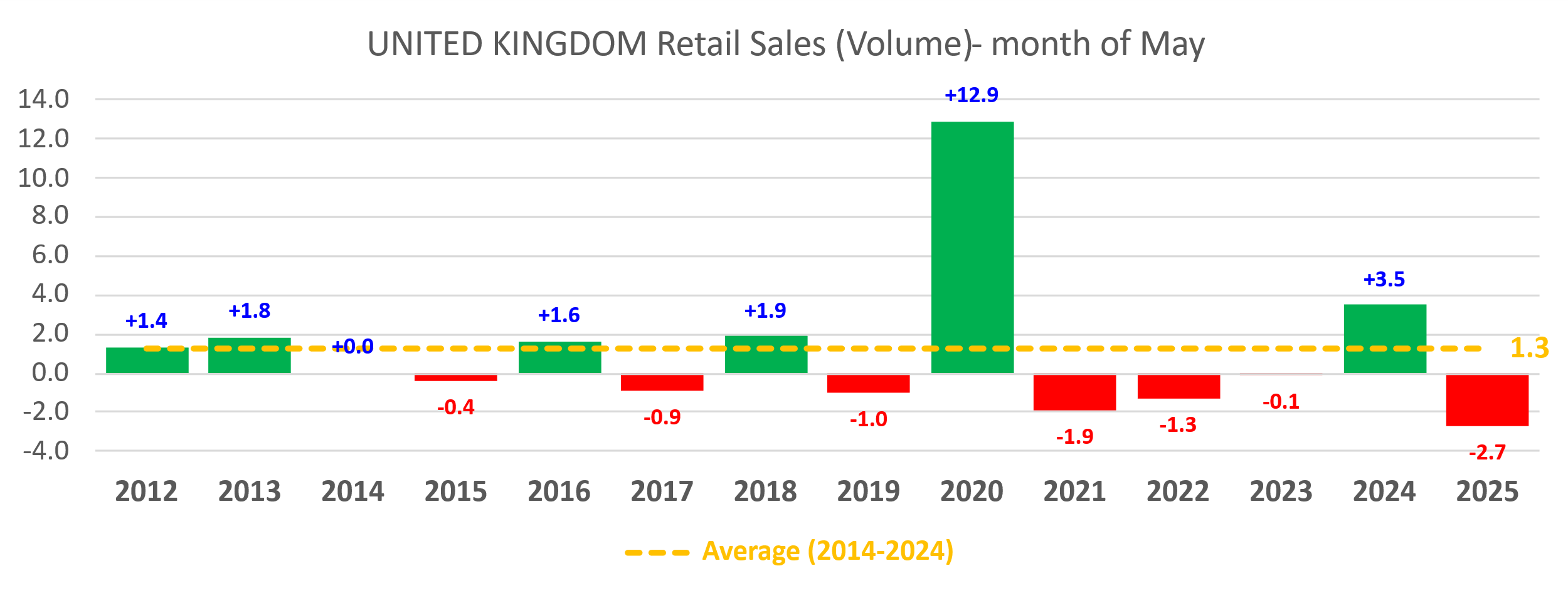

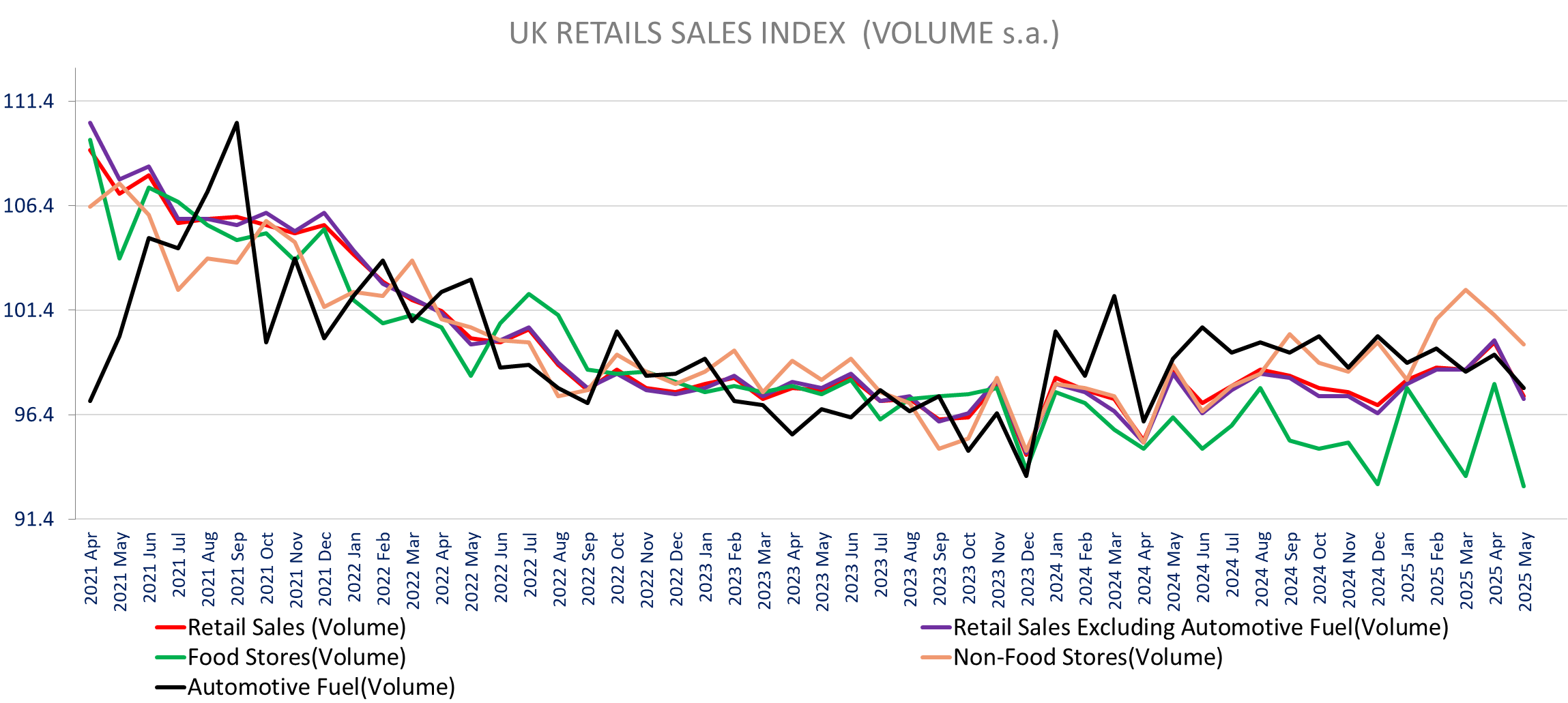

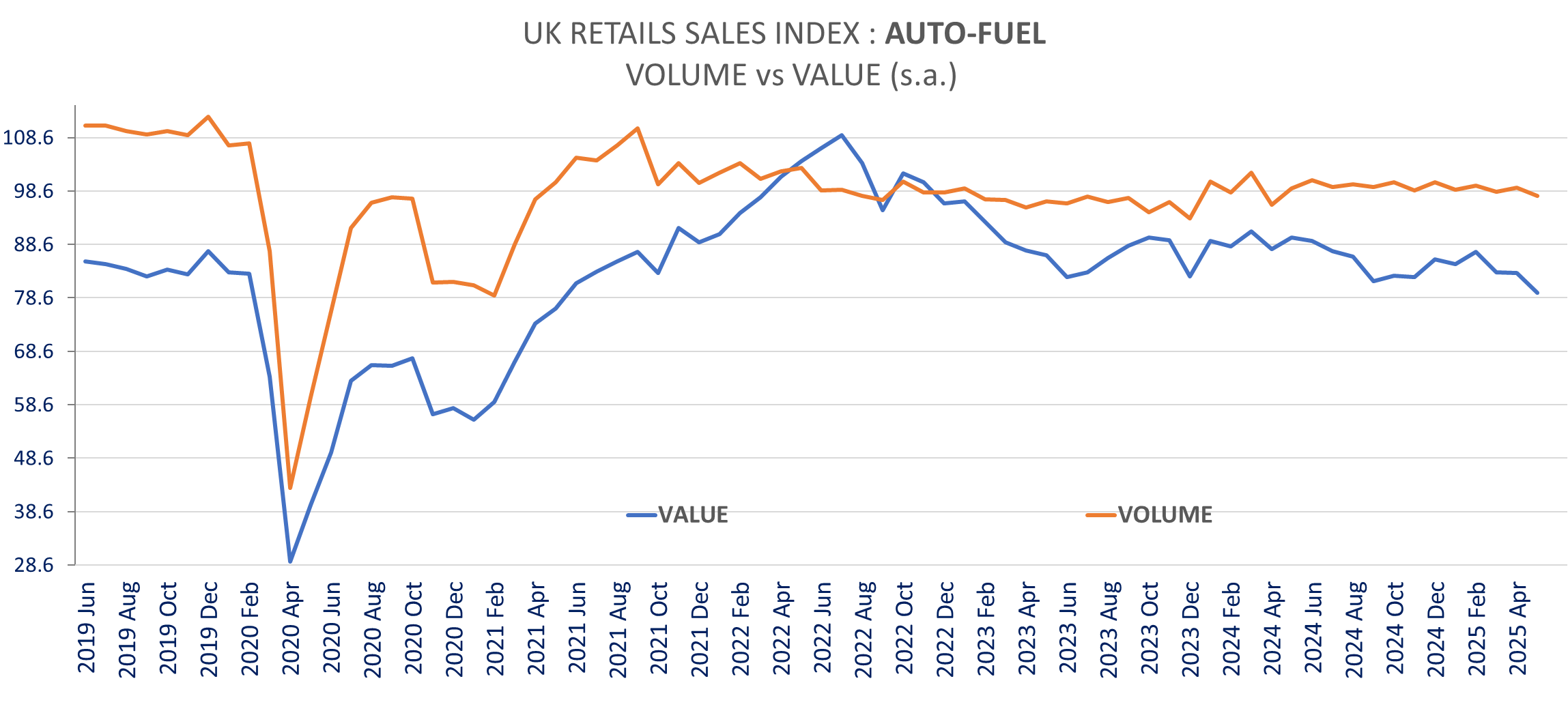

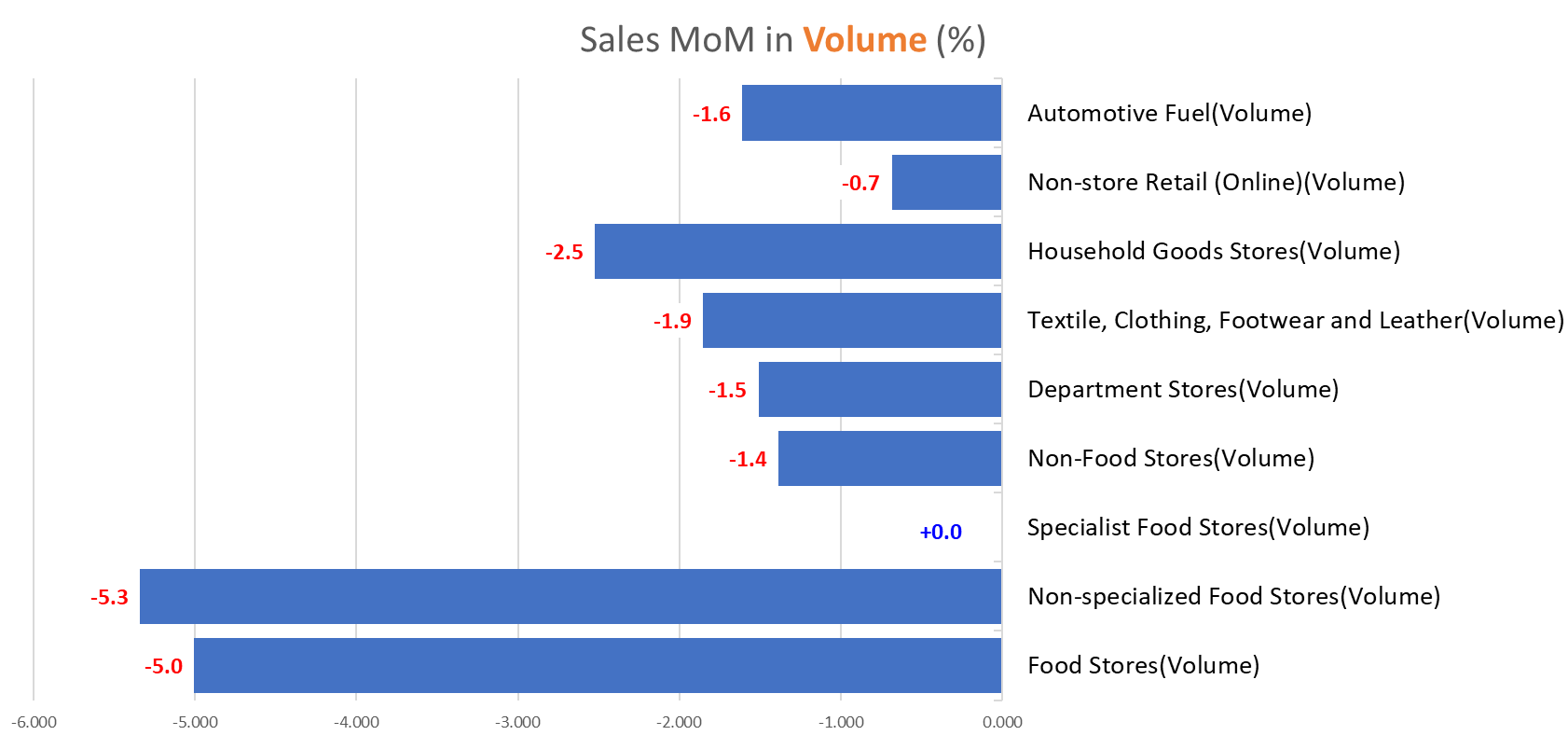

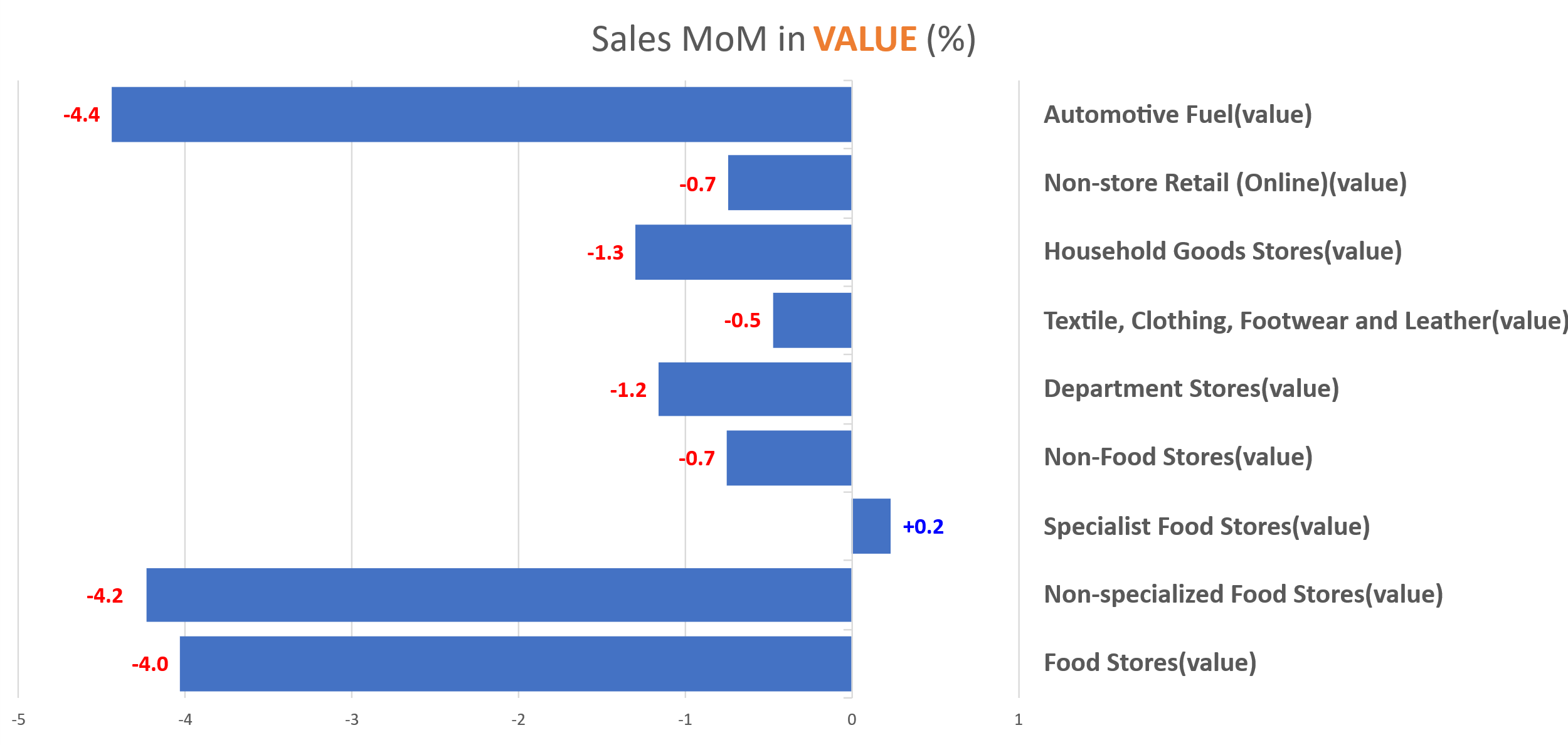

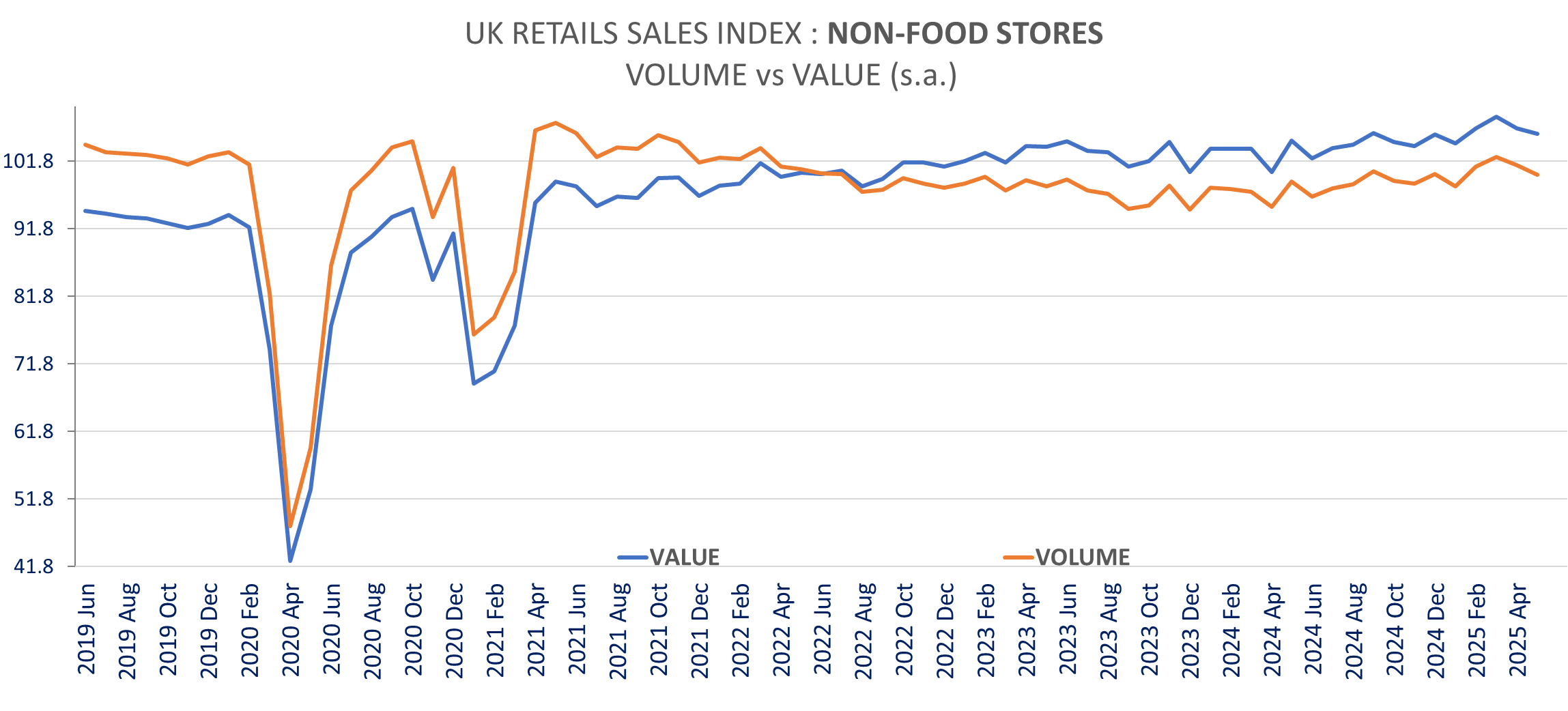

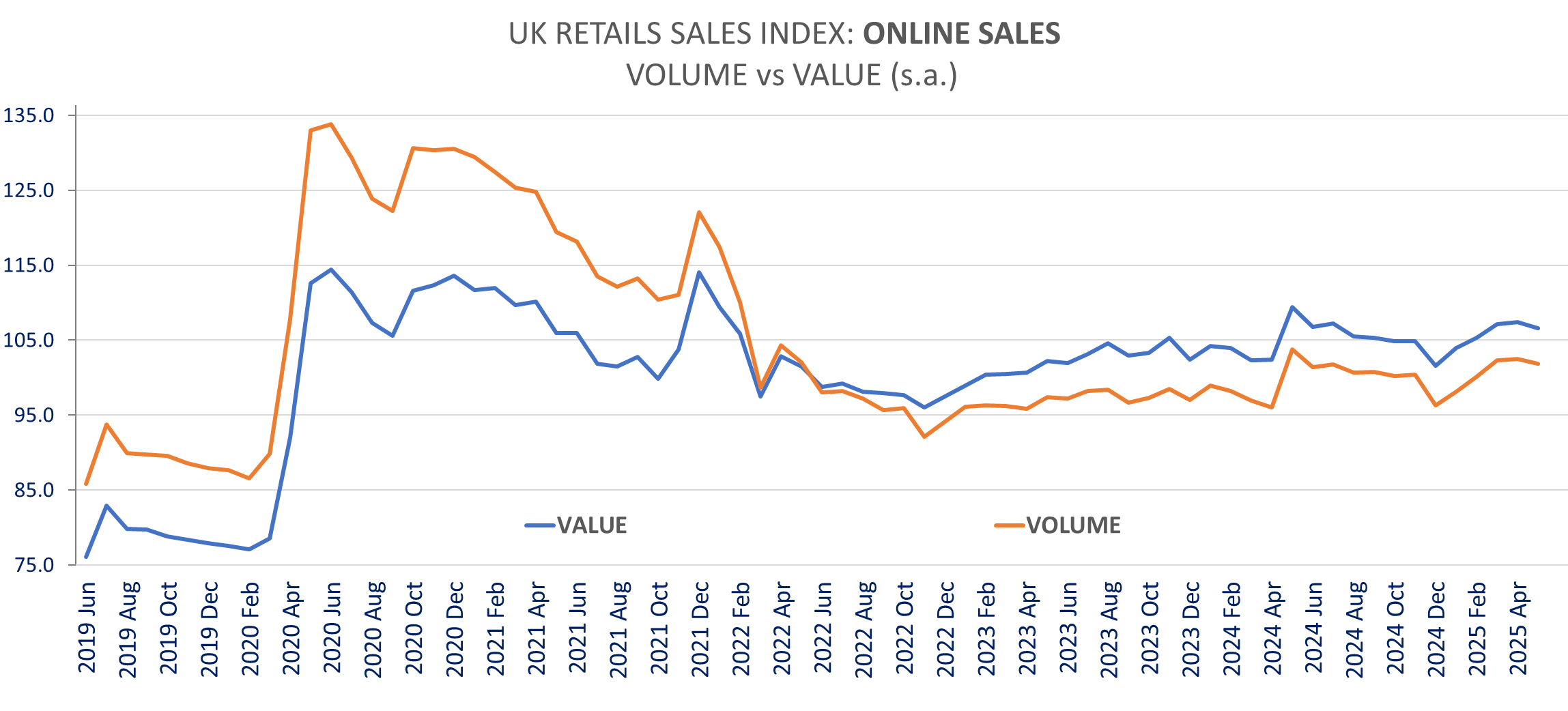

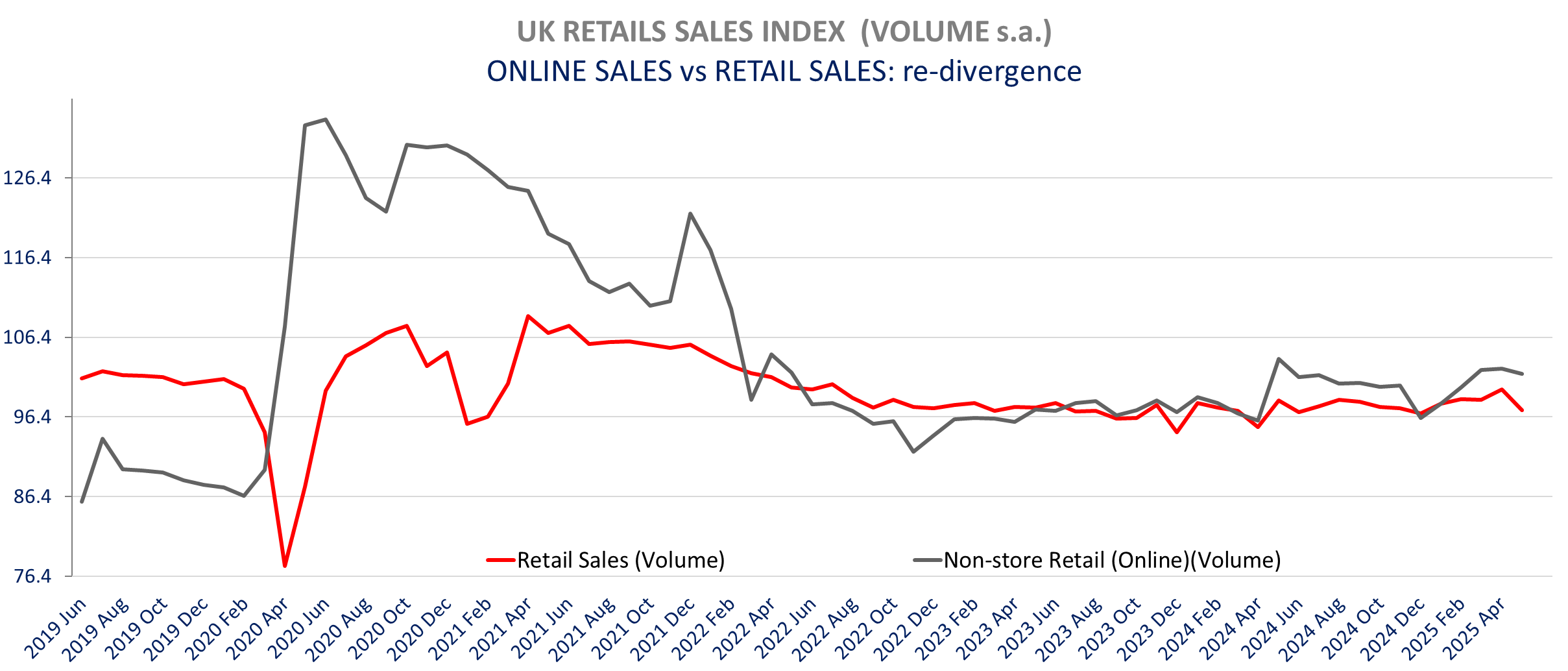

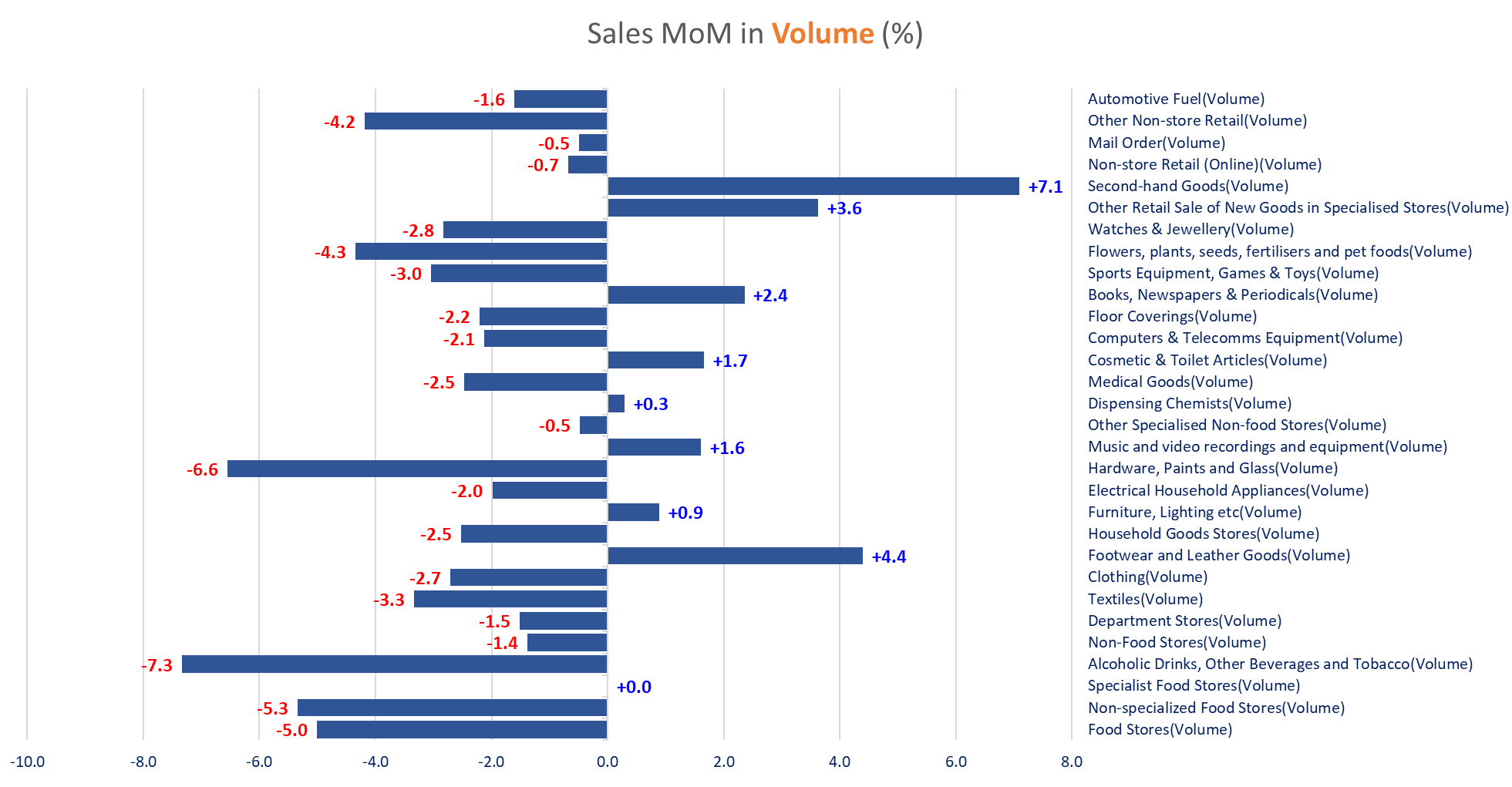

In the UK the May retail sales were far lower than expected at -2.7% m/m in volume versus -0.5% expected. April sales +1.3% overstated the trend benefiting from unusually warm weather and the timing of Easter. May sees some payback, but it is still the largest monthly decline for the month of May on record (since 1996) and the largest monthly decline since December 2023. Food and non-specialized food stores sales posted a sharp decline (-5% and -5.3% respectively). Non-food sales are down -1.4% m/m after -1.2% in April (revised from -0.7%), down -0.7% in value. In May, online sales showed resilience, decreasing just -0.7% month-over-month in both value and volume.

Data from inflation to trade, retail sales, consumer confidence and PMI have been significantly by the stop & go on tariffs (Higher production and trade ahead of announcements, inflation and economic concerns), the different timing of Easter yoy and weather…

On the companies’ front: Eutelsat is contemplating €1.5bn capital increase. Coupled with a dedicated debt refinancing plan, this capital increase will reinforce the Company’s financial flexibility by accelerating its deleveraging and support investment in its existing Low Earth Orbit (LEO) capabilities and the future IRIS constellation. The French Government is participating and will end up with a 30% stake in the share capital followed by India's Bharti Space Limited at 18.7%. In an interview with La Repubblica, UniCredit CEO said the bank was likely to withdraw its offer for smaller Banco BPM, a day after receiving European antitrust approval. UniCredit is facing the opposition of the Italian government. The homebuilder Berkeley announced that Chairman Michael Dobson will step down from the board in September 2025 to be replaced by current CEO Rob Perrins and Richard Stearn (Current CFO) to become CEO. While Berkeley FY26 guidance is only slightly below the consensus, the homebuilder added that its long-term target is to make a pre-tax return on equity above 15% over the cycle but will be below this in the medium-term while the current operating environment volatility persists, and it invests in the BTR platform to increase future delivery. More details on equities here

Last hope for a “diplomatic solution”

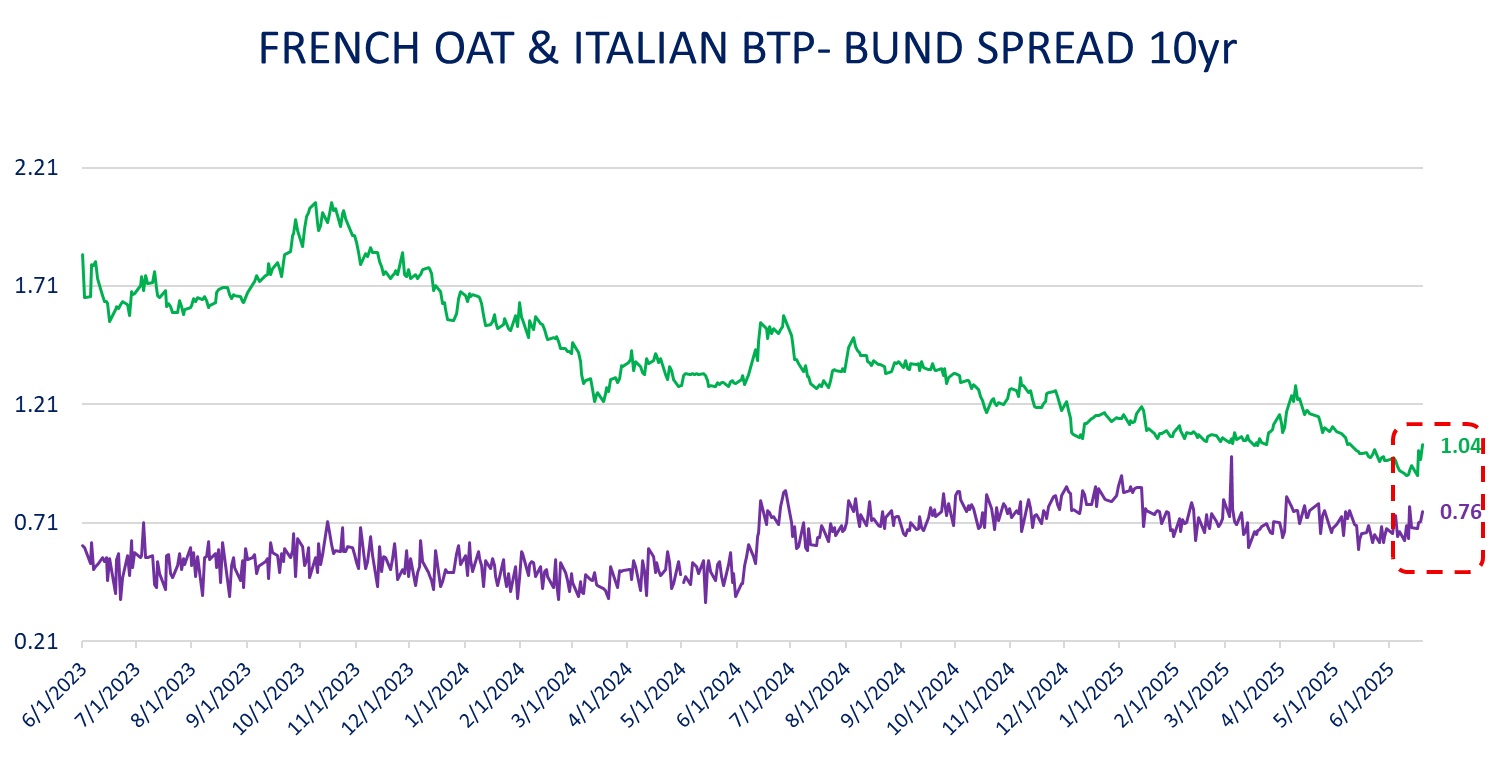

Higher sovereign spreads in Europe (as of yesterday) with flight to Bund

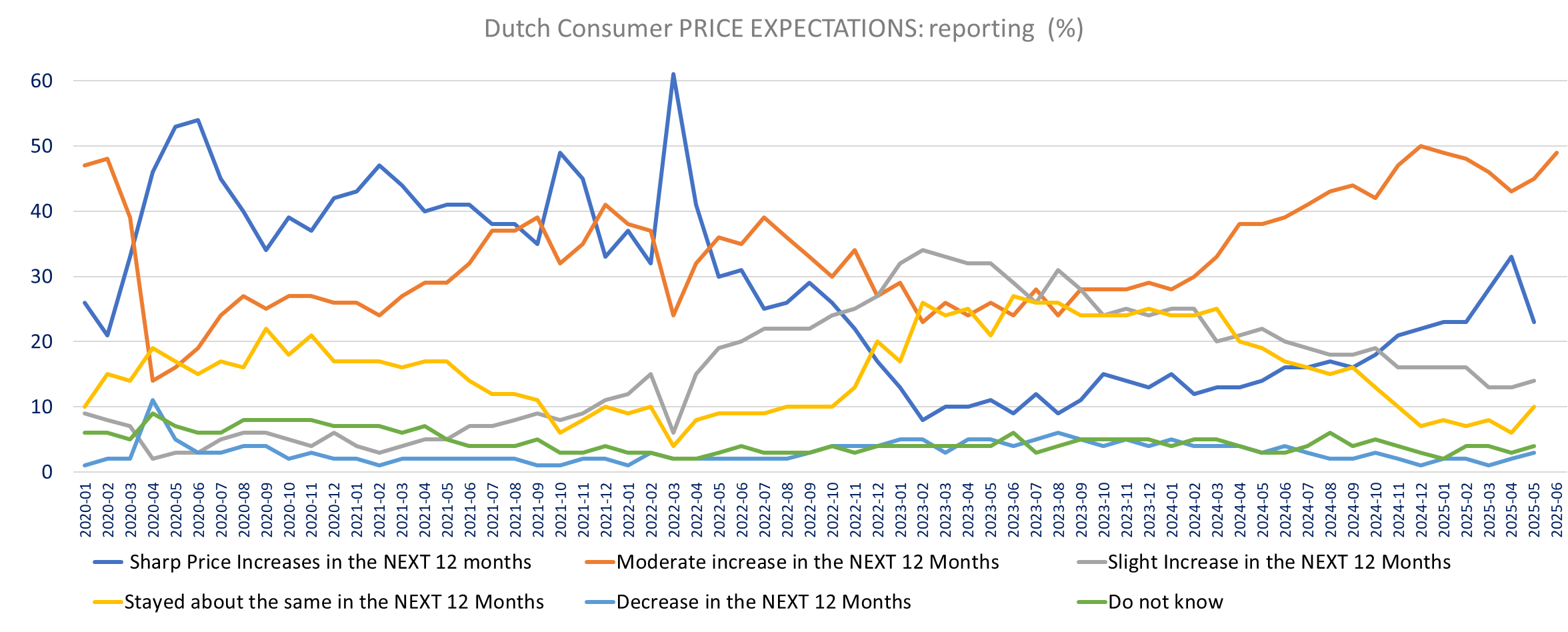

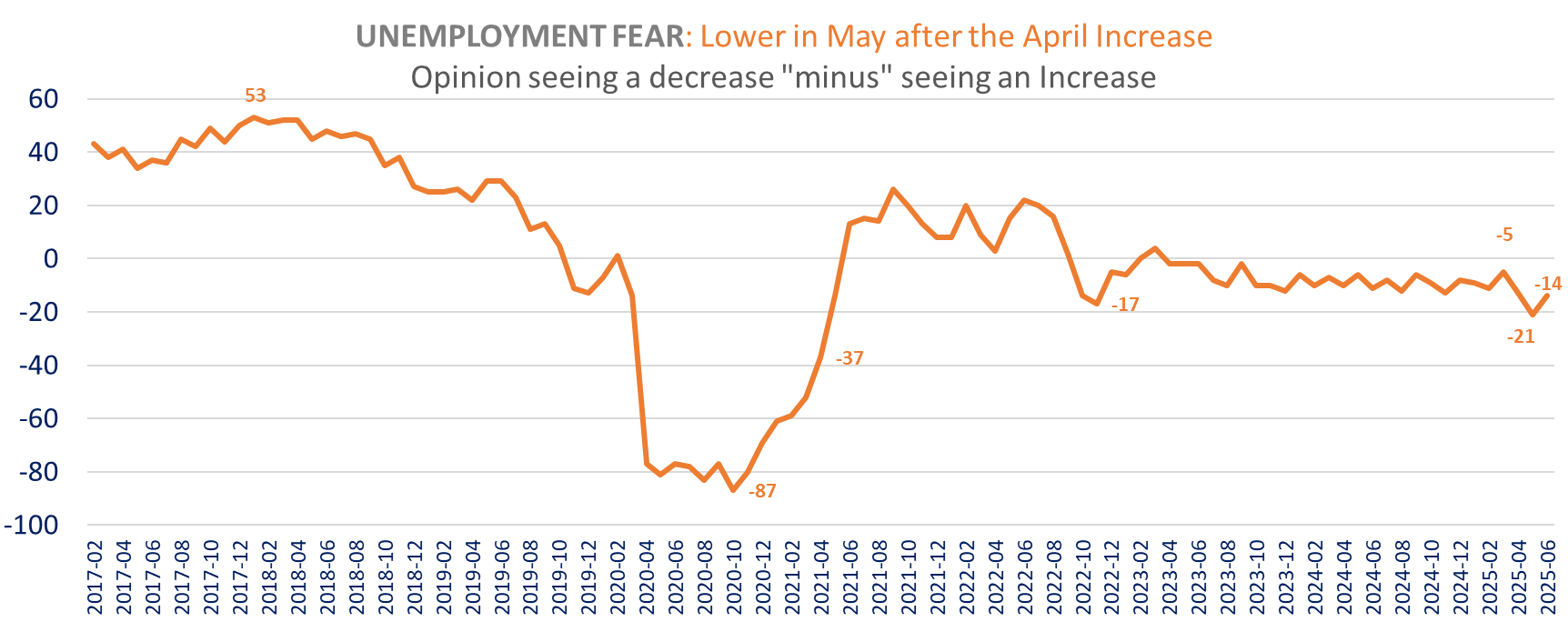

Dutch consumer confidence improved slightly in June to -36 from -37 (still below March Level of -34), remaining at low level by historical standard (-3.4 average). Unemployment fear lessen to -14 balance the dip in April (-21, was the highest fear since April 2021). The Unemployment balance is the difference between % seeing a decrease in unemployment and the % seeing a increase (the lower the higher the unemployment fear). The improvement in confidence comes from a less negative view on the economy, both the past economy (-62 vs. -62) and the 12 months outlook (-54 vs -58, Best since February, up for the 3rd month in a row. The current/past financial situation unchanged (-20) but the future financial situation improved slightly (-8 vs -9). On the price side the % of households expecting price sharply higher is unchanged at 23%, and the percentage expecting a moderate increase in the next 12 months is up to 49% from 45%. Only 1% see lower prices. 61% report a sharp increase in prices in the last 12 months down from 64%. Willingness to Buy, large purchase intention and savings’ intentions balance are unchanged month-over-month.

France Business confidence improved in June to 96.1 from 95.6 in May (revised from 95.8), reported as unchanged at 97. Services climate improved to 95.6 from 95 (revised from 95.2) reported at 96 up from 95 and Retail climate improved a tad more to 98.6 from 97.8 (revised from 97.7), reported at 99 up from 98.

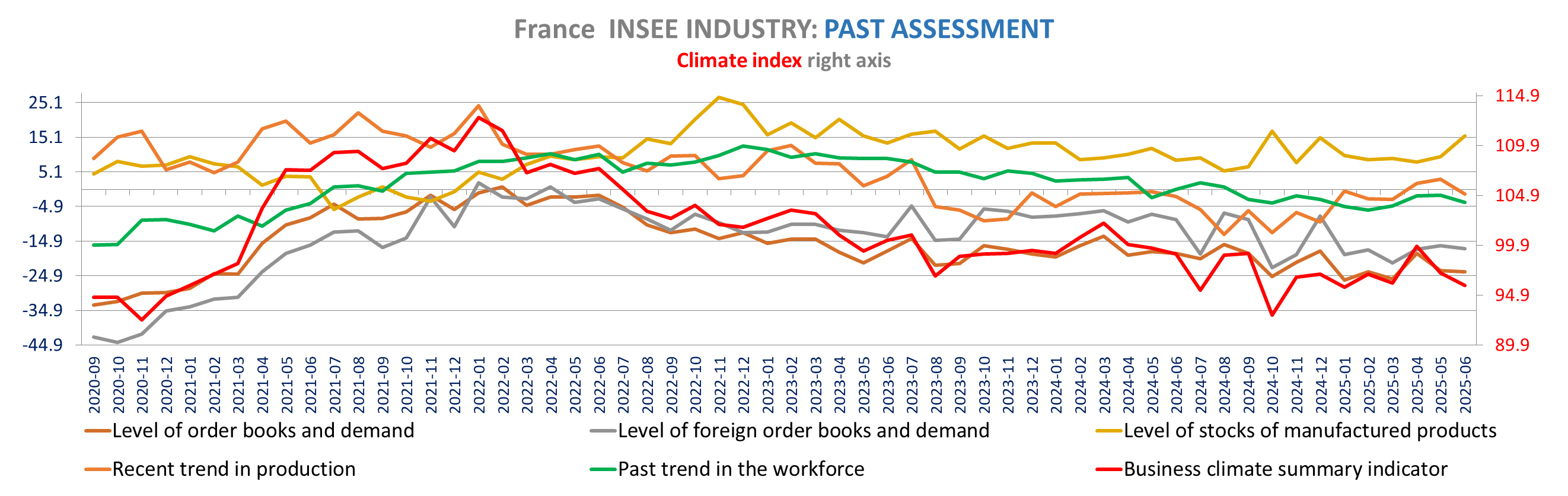

Manufacturing was the main drag at 95.9 down from 97.1 (revised up from 96.9), reported at 96 down from 97. Construction is back to the average of 100 down from 100.5 in May.

Inflation remains benign with selling prices lower (and negative balance) for services (lowest since April 2021 at -2), retail and construction (lowest since February 2021 at -9.3!). The balance for price expectations unchanged for manufacturing at +5.8 (although up from 5.6 initially reported in May).

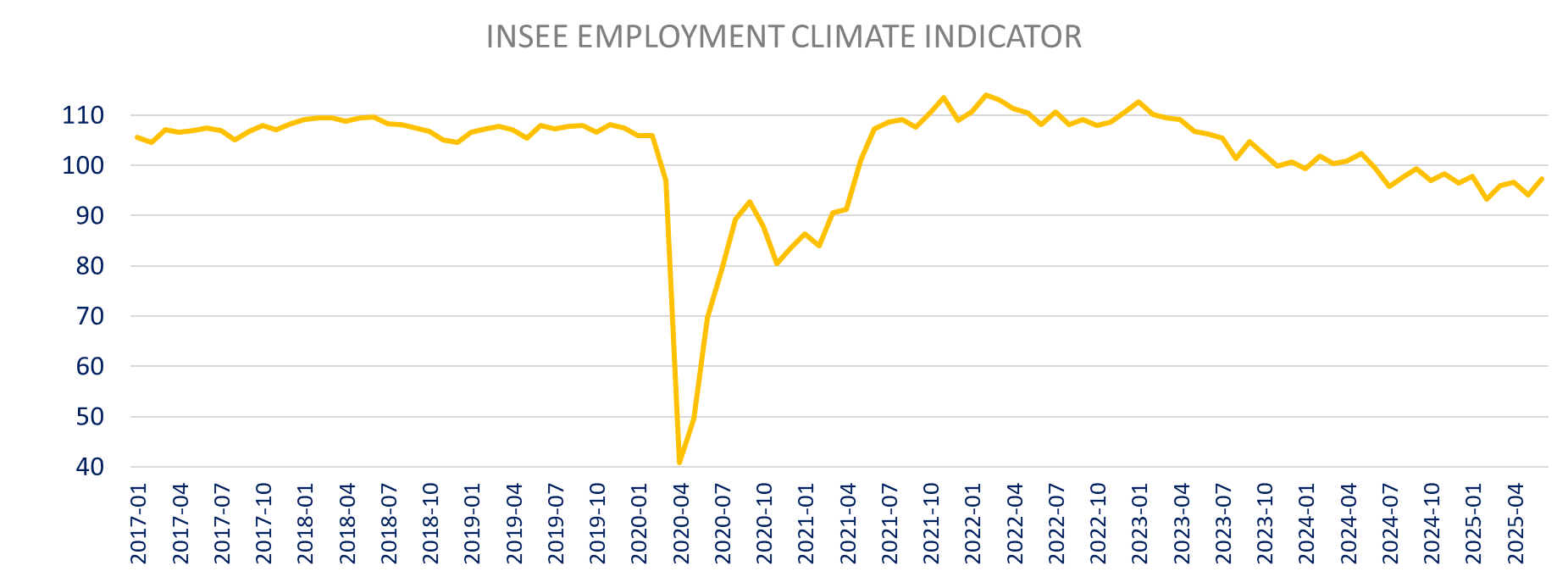

Employment expectations are higher. The INSEE climate indicator is up to 97.3 from 94.2, highest since February. The balance for future employment improved marginally for Manufacturing (-1.5 vs -1.8) and construction (+2.2 vs +2.1) but saw a bigger jump for services (-6.1 vs -12, best since December). On the other hand, employment expectations worsened for Retail (-7.1 vs -6.2).

In services, the climate improvement comes exclusively from higher expectations for activity and demand, while past assessments are weaker. Sentiment improved for transport & storage, accommodation and support services, but declined for real estate services and professional, Scientific & technical services.

In Manufacturing the weaker sentiment is relatively broad based, with slightly weaker order books, production turning negative, decline in past employment and higher stocks of finished goods. Sentiment improved for food (97 vs 93.9) and marginally for transport equipment, paper but declined for textiles (84.4 vs 99.1) machinery and chemicals.

INSEE manufacturing Release, INSEE Services, INSEE Retail, INSEE Construction

Belgium consumer confidence also improved in June, for the second consecutive month, up to -4 from -7, matching February’s level which was the highest since last August. Unemployment fear is down in Hune to +6 from +13 the lowest since February 2022 (Ukraine invasion). Besides unemployment fear the biggest improvement is for the economic outlook to -24 from -30 and the past economic assessment (-37 vs -45). Households are slightly less positive on their current personal situation *22 vs 23) but less negative on expectations (-7 vs -9, best since January). Purchasing intentions are slightly lower and households are slightly less unfavorable for saving now. Price expectations are back up (+29 in June vs +18 in May) after the fall in May from +35 in April on tariffs concerns (up from 26 in March). NBB Release

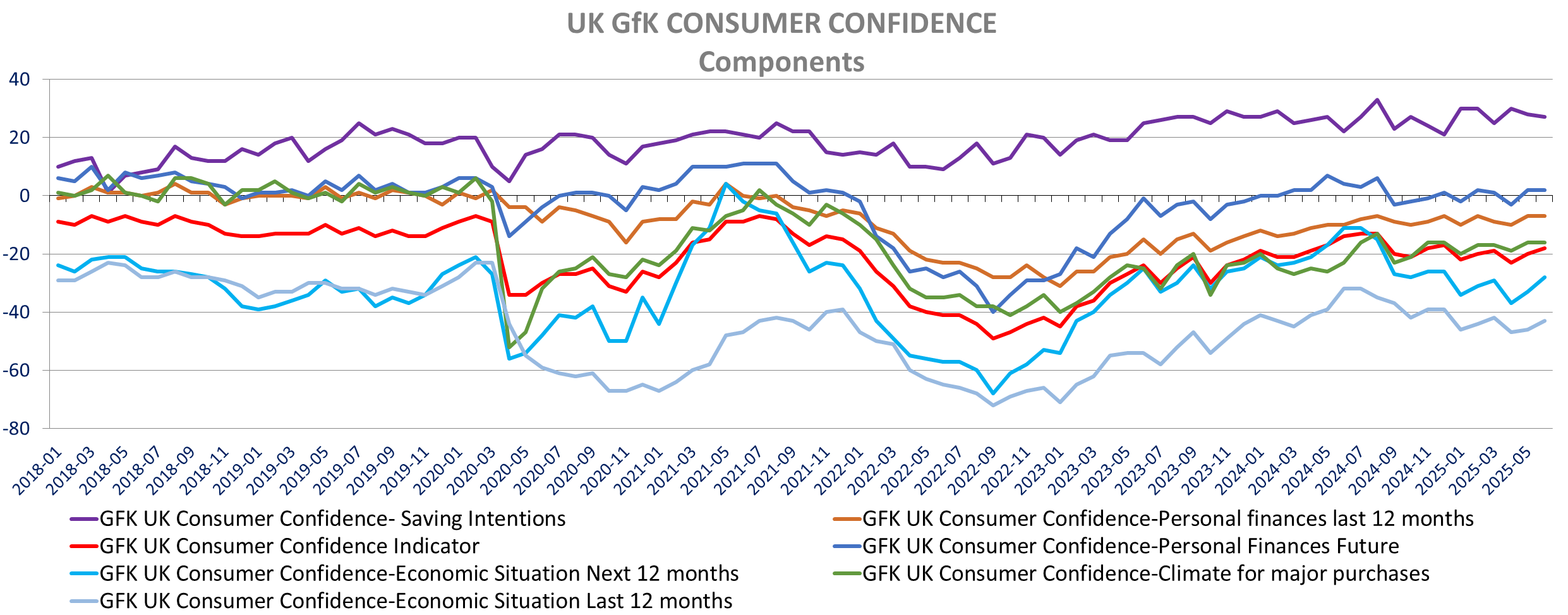

The UK June GfK consumer confidence improved by 2 points in June to -18, the best level since December 2024, but still at a low level. Personal financial situation for the past 12 months (-7) and for the next 12 months (+2) remained unchanged from May. The improvement in the overall confidence index comes from a less negative appraisal of the general economic situation, regarding the last 12 months (-43 vs -46) but also regarding the outlook 12 months out (-28 vs -33, best since December). Consumers remain cautious though: purchasing intention unchanged at -16 and savings’ intention only marginally lower at 27 vs 28 (was 25 in March, pre-tariff). GfK Release

.

UK June retail sales fell more than anticipated, down -2.7% m/m in volume (-0.5% expected) following the strong April (+1.3% m/m revised form +1.2%). This is the weakest May on record. (+1.3% 10yr average) and the sharpest monthly decline since December 2023. April sales were supported by a warmer than usual weather and the timing of Easter. ONS Release In value, sales are down -2.4% m/m after 1.1% in April. Fuel store sales are down -1.6%m/m in volume and -4.4% in Value.

When excluding Auto fuel, sales are down -2.8% m/m in volume (after +1.6% m/m in April revised form 1.3%) but only -2.2% in value (after +1.2% m/m in April). YoY Sales are now down -1.2% after being up 4.9% yoy in April (volume). Ex fuel sales are down -1.2% yoy after +5.2% yoy in April.

Online sales resisted much better in May, down only -0.7% m/m, both in value and volume.

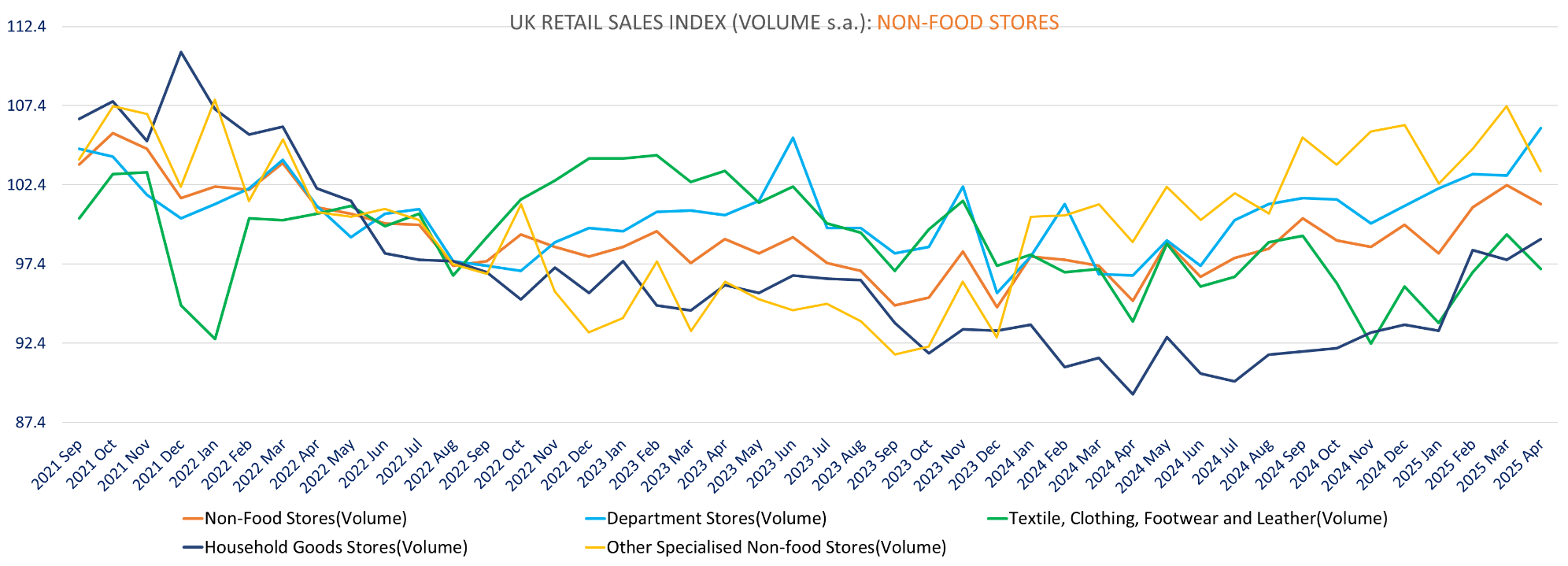

Looking at more details, footwear & leather sales were up 4.4% m/m while textiles fell -3.3% and clothing -2.7% m/m. We also saw sharp decline in flower/plans (-4.3% m/m) and electrical household appliances (-6.6%), Sports equipment/Games/toys (-3%). Othe the other side, second-hand stores’ sales increased by +7.1%, books/newspaper +2.4% and cosmetic +1.6% m/m (all in volume)

|

|

Friday, June 20, 2025 | ||

|

ETL | |||

|

EUR |

3.66 |

+28.87% | |

|

ETL |

Eutelsat is contemplating €1.5bn capital increase. Coupled with a dedicated debt refinancing plan, this capital increase will reinforce the Company’s financial flexibility by accelerating its deleveraging and support investment in its existing Low Earth Orbit (LEO) capabilities and the future IRIS constellation. A reserved capital increase of €716 million at a price per share of €4 corresponding to a +32% premium to the 30-day-VWAP of the shares, which would be subscribed by the French State via the “Agence des Participations de l’Etat” (“APE”), Bharti Space Limited, CMA CGM, and Le Fonds Stratégique de Participations (“FSP”), and a rights issue of €634 million, which would be subscribed for their rights by the above investors. . On the back of the forthcoming capital increase,

| ||

|

|

|

|

|

|

UCG | |||

|

EUR |

56.42 |

+1.93% | |

|

UCG |

In an interview with La Repubblica, Unicredit CEO said the bank was likely to withdraw its offer for smaller Banco BPM, a day after receiving European antitrust approval. Unicredit is facing the opposition of the Italian government.

The BPM bid resumes on Monday after a suspension triggered by a lawsuit UniCredit brought to challenge government-imposed conditions which it says prevent it from pursuing the bid. The Italian government has imposed its "golden powers" over the bid, on the grounds of national security concerns. | ||

|

|

|

|

|

|

BKG | |||

|

GBp |

3854.00 |

-7.13% | |

|

BKG |

Berkeley Group announced that Chairman Michael Dobson will step down from the board in September 2025 to be replaced by current CEO Rob Perrins and Richard Stearn (Current CFO) to become CEO. FY25 PBT came in line with consensus expectation at £529m or -5% Y/Y. For FY26 Berkeley PTB guidance is £450 million (Consensus £462), with FY27 likely to be similar, based on current sales rates.

" Our long-term target is to make a pre-tax return on equity above 15% over the cycle but will be below this in the medium-term while the current operating environment volatility persists, and we invest in our BTR platform to increase future delivery and maximize long-term value for shareholders." | ||

Versus early hours:

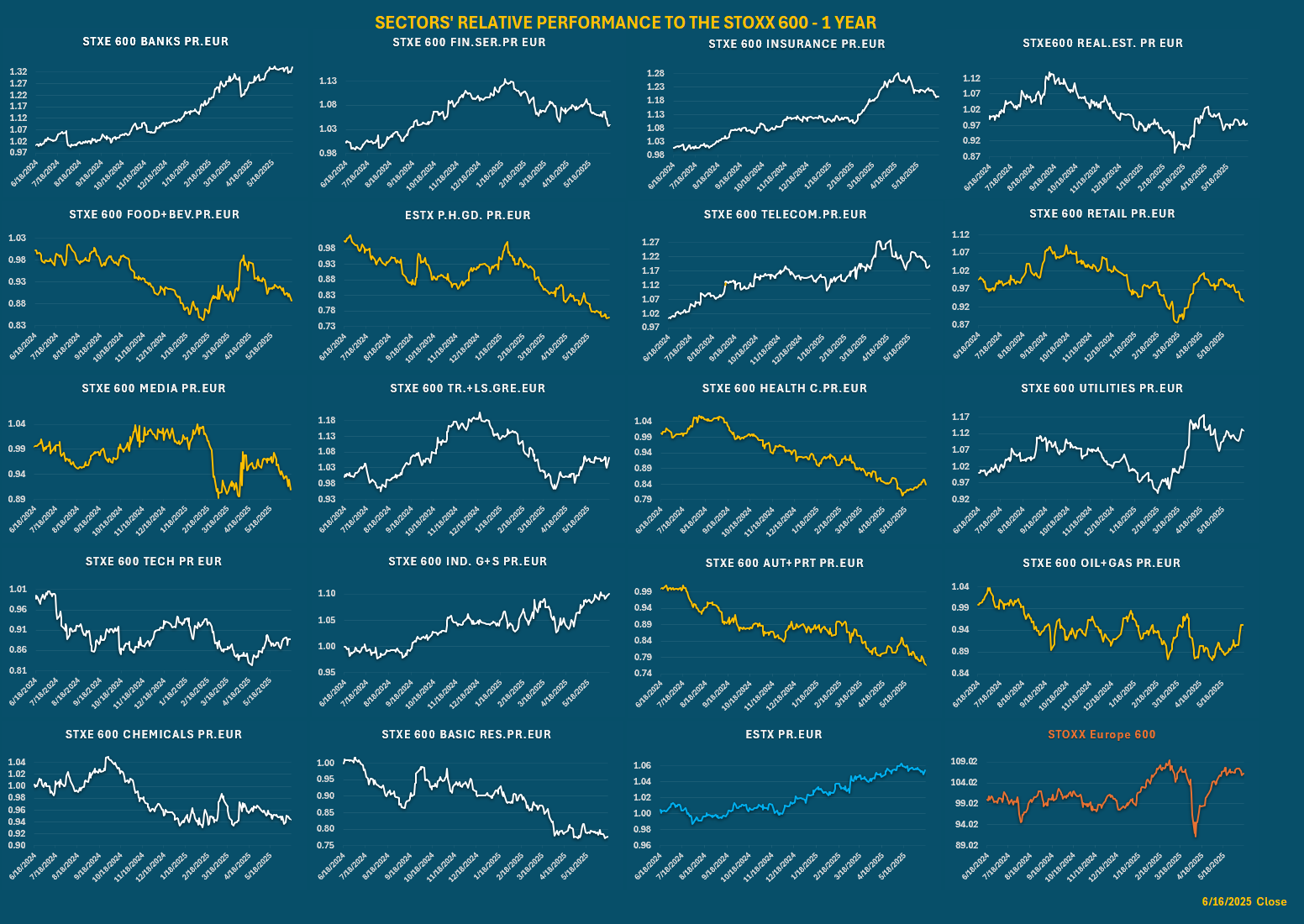

SECTOR PERFORMANCE

Relative performance to STOXX 600

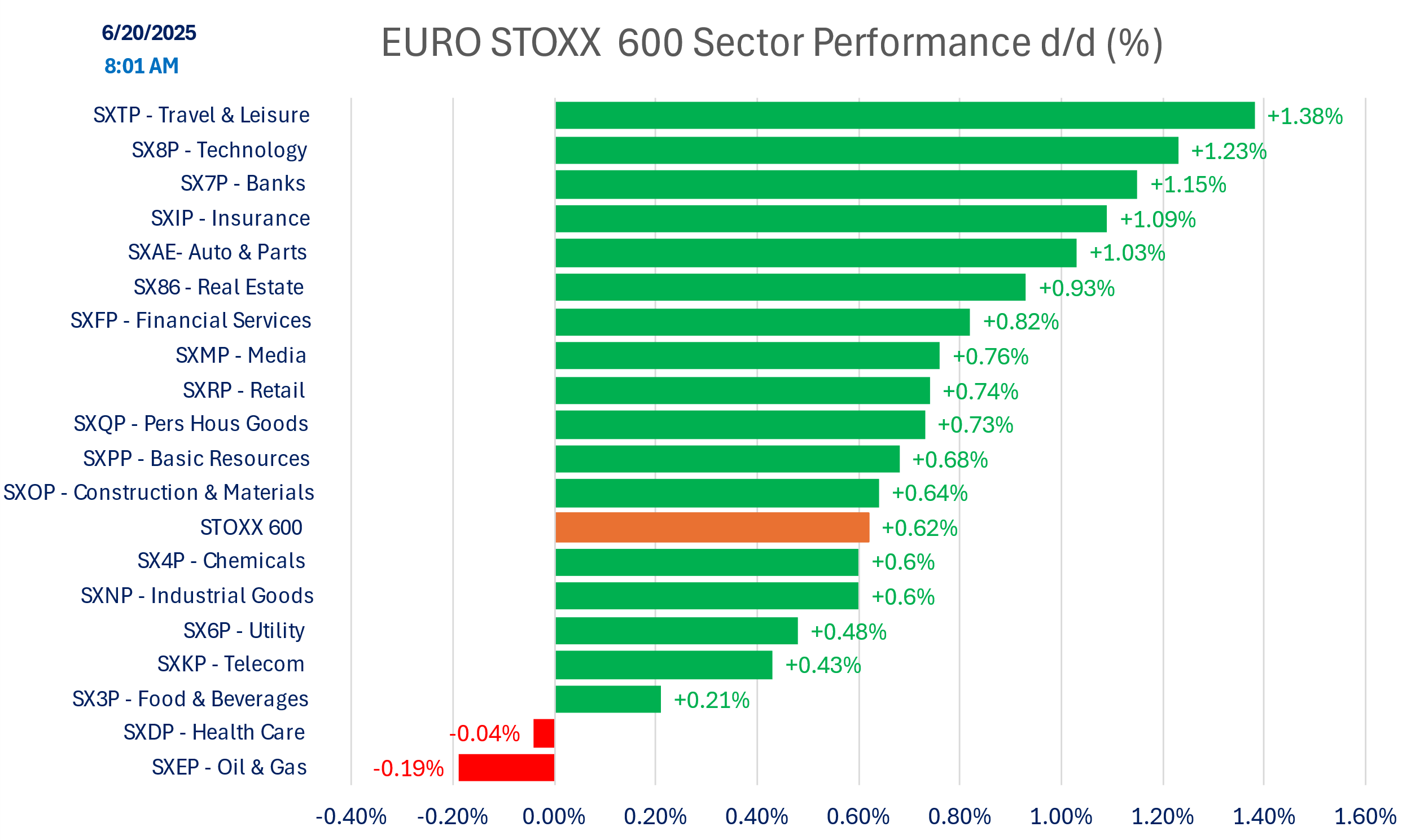

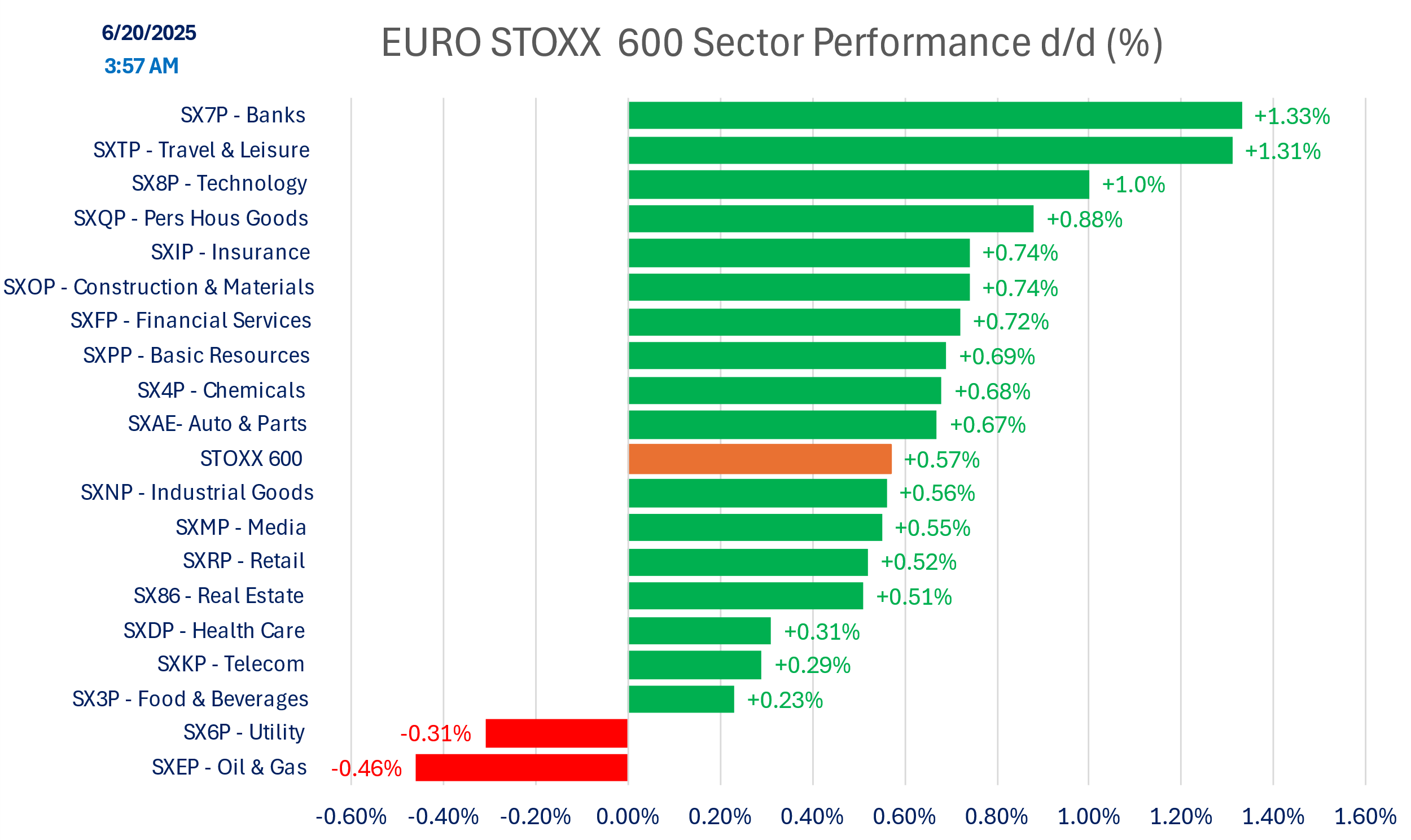

Today’s Performance

Versus early hours:

Indices

Versus early hours

Commodities

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.