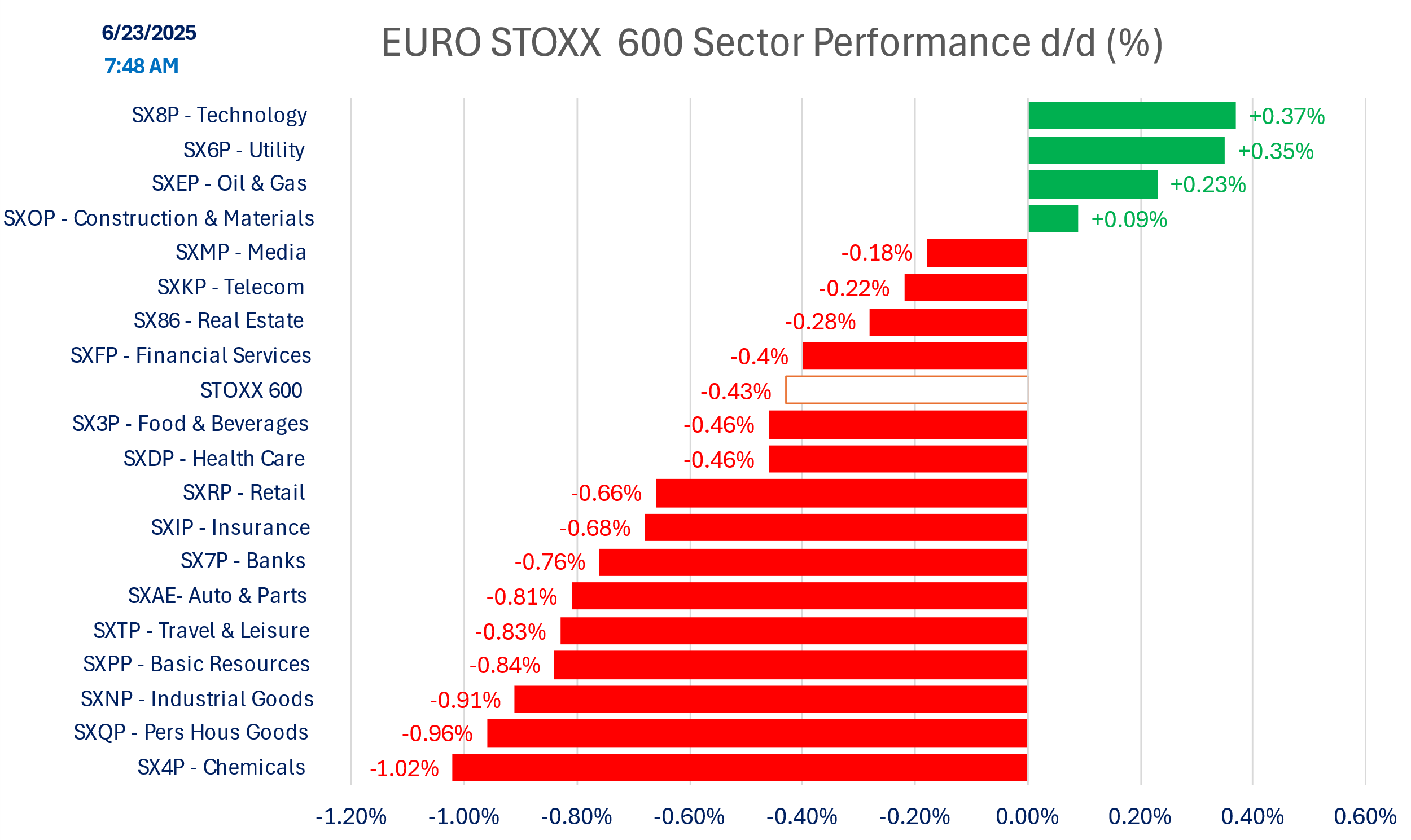

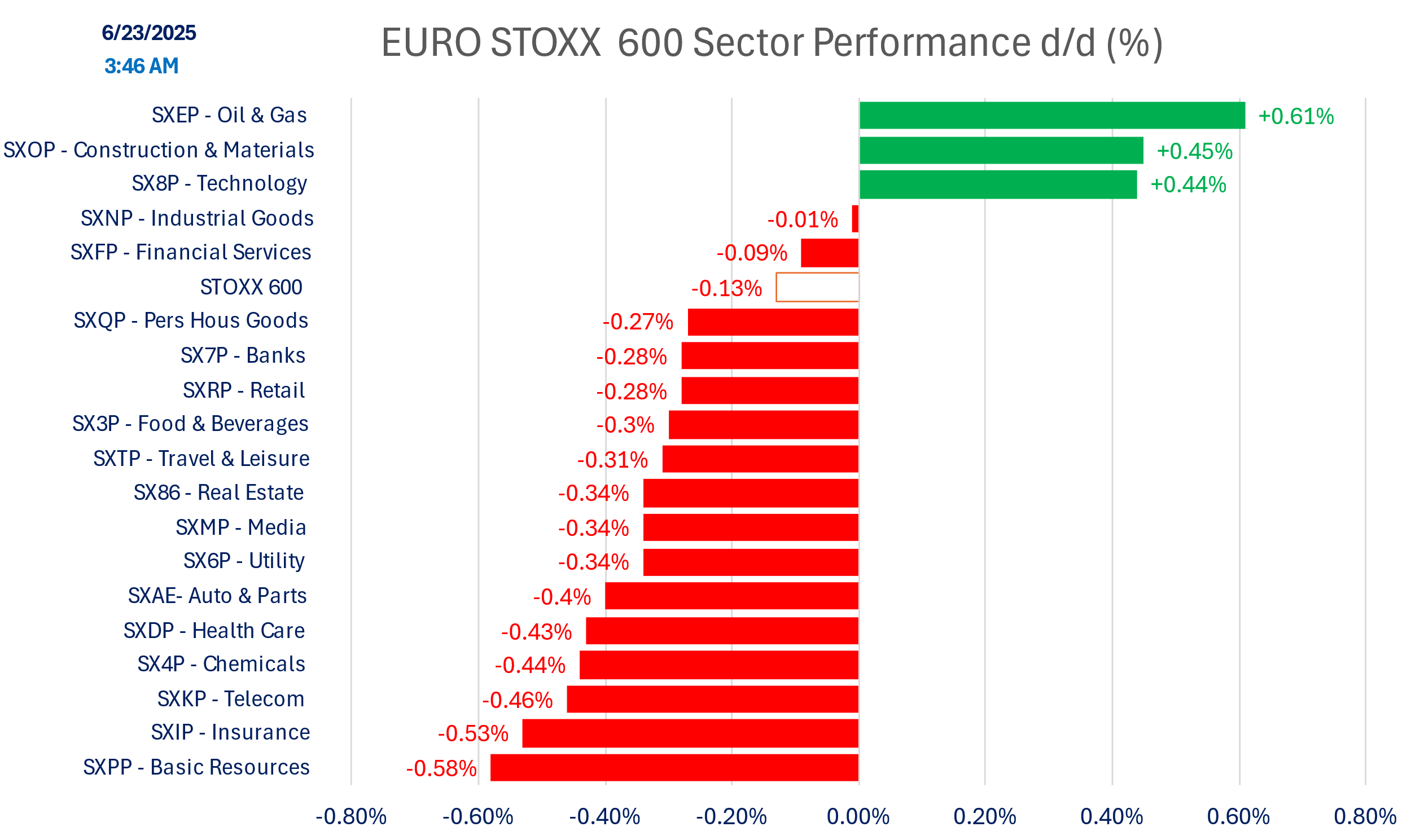

Far more muted market reaction to the US bombing of the Iranian nuclear facilities. As we started to see last week, the $ continued to benefit, apparently reclaiming some safe haven status, but it seems mainly due to one sided negative sentiment (Last week’s ZEW investor $/€ sentiment was the most negative on the $ since December 2006). The DXY is up 0.6% to 99.36, oil is also only up 0.6% to $77.6 (Brent) but is still up more than 20% in the last month. Asian stock markets fell only slightly, and European stocks are only down - 0.4% (only oil & gas, utilities and technology are up). Bond yields are up with slight flatter curves, not as one would have expected. Gold is slightly up, but Bitcoin declined (momentarily below 100k post report of the facilities’ bombing).

Markets seem to price a status quo rather than escalation from here.

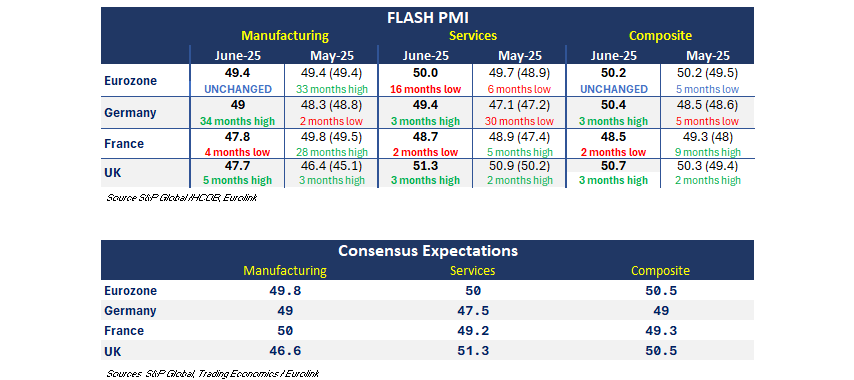

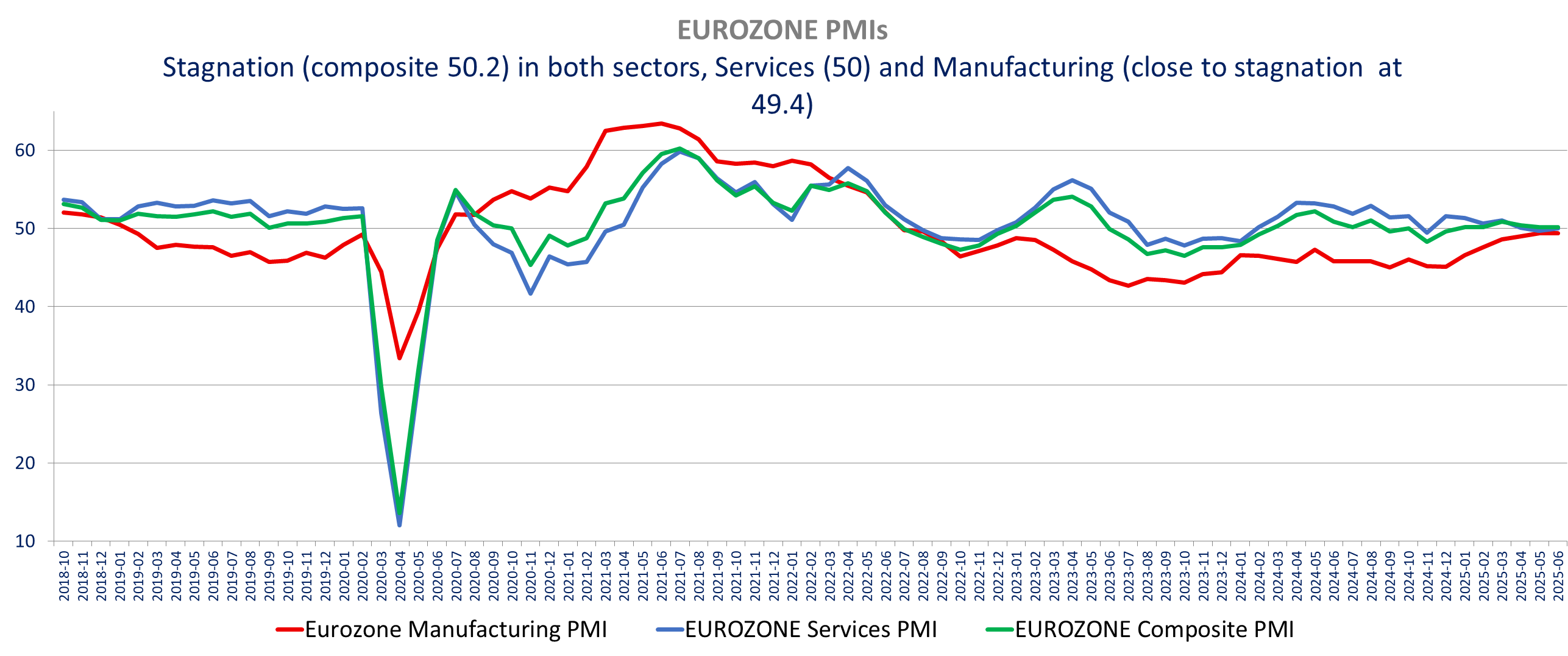

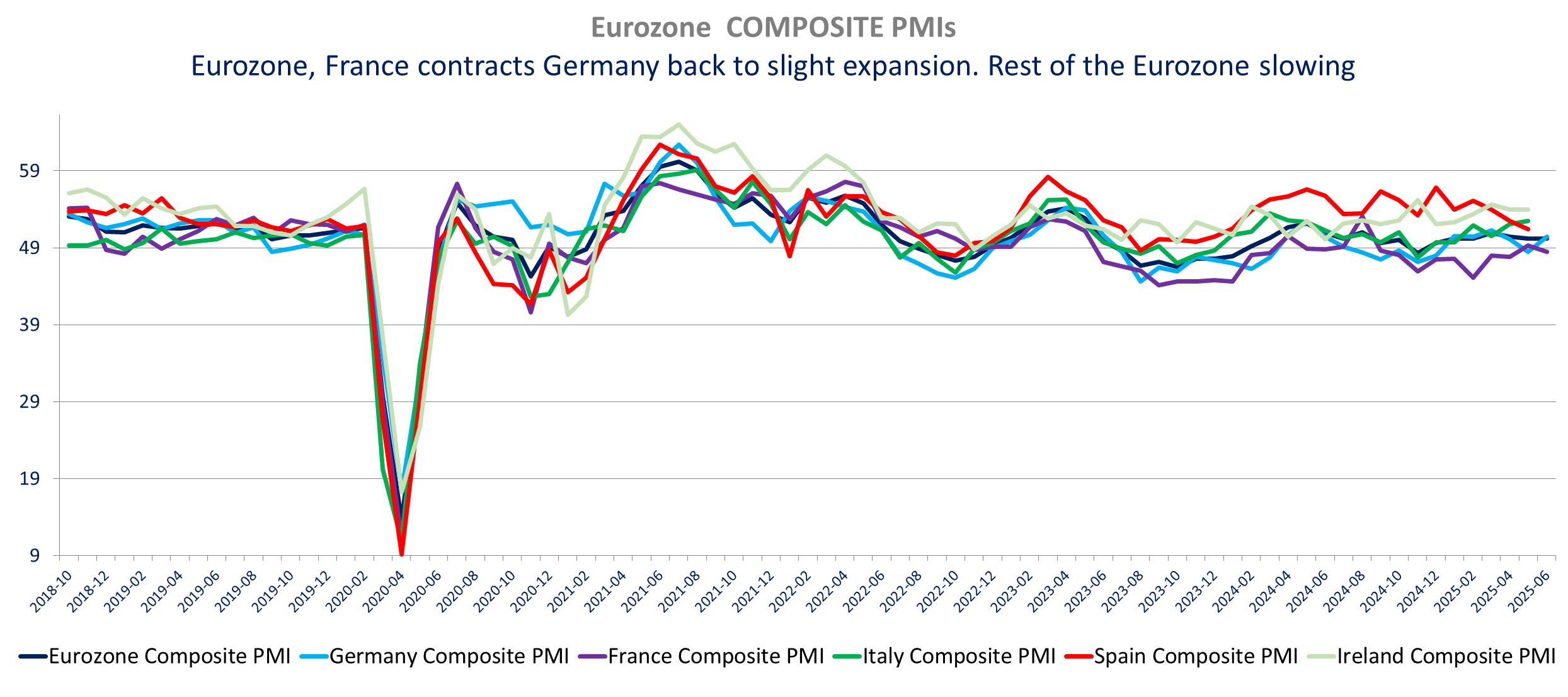

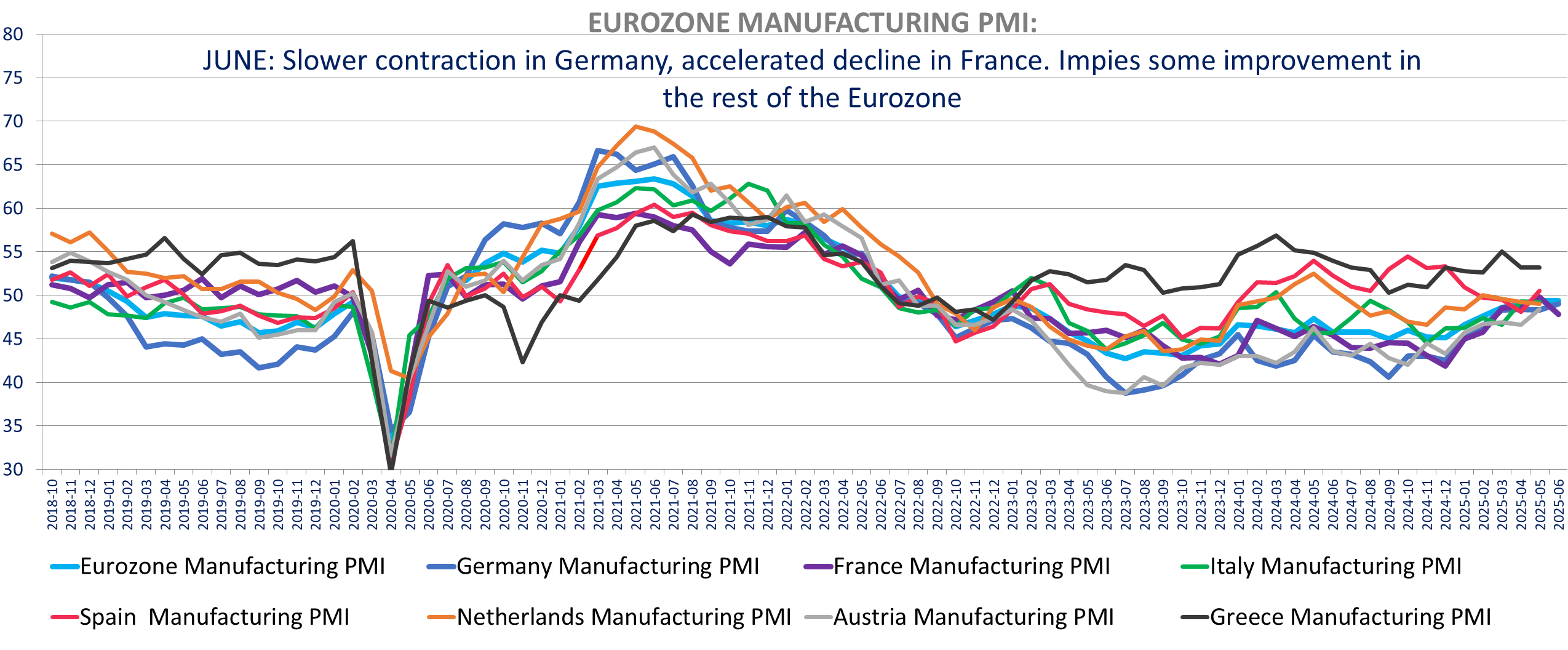

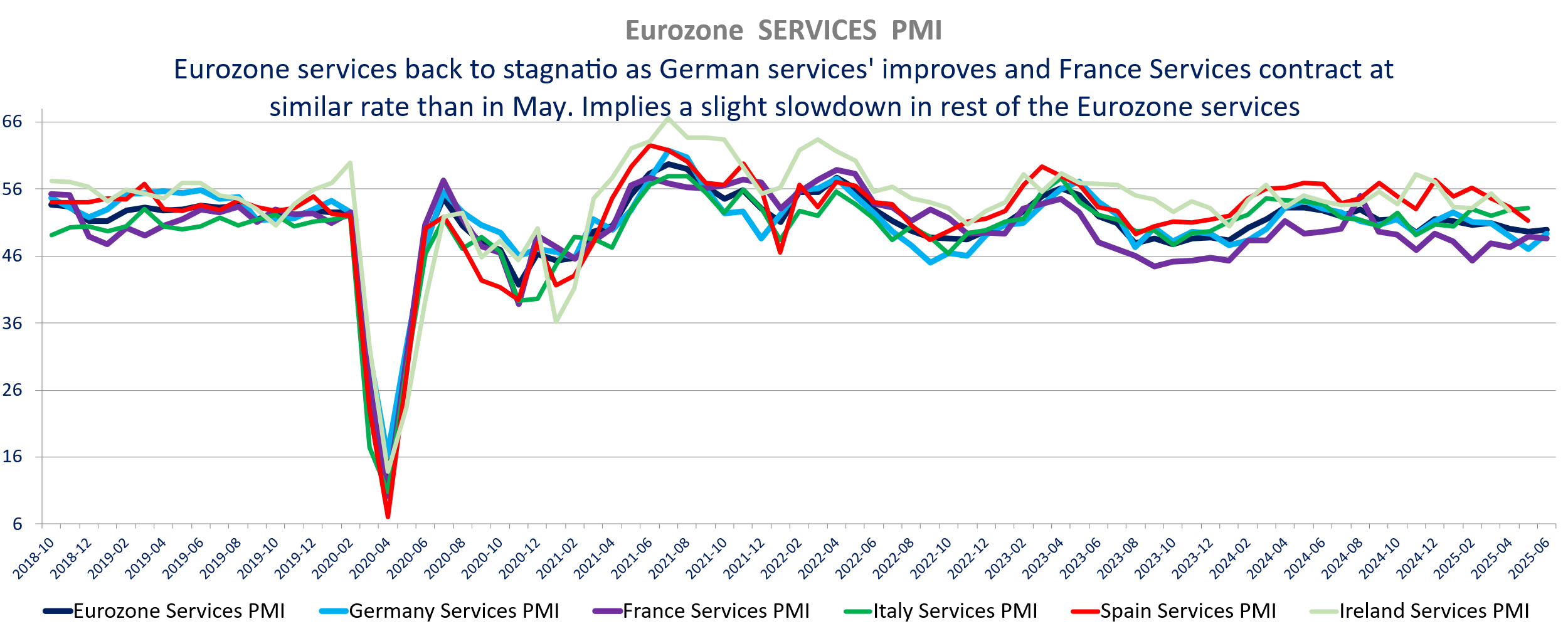

The Eurozone Flash PMI is only slightly below expectation of 50.5, being unchanged in June at 50.2 consistent. The Eurozone Manufacturing PMI is also unchanged from May to 49.4, also slightly below expectations of 49.8, and the services PMI improved slightly to 50 from 49.7 in May in line with expectations.

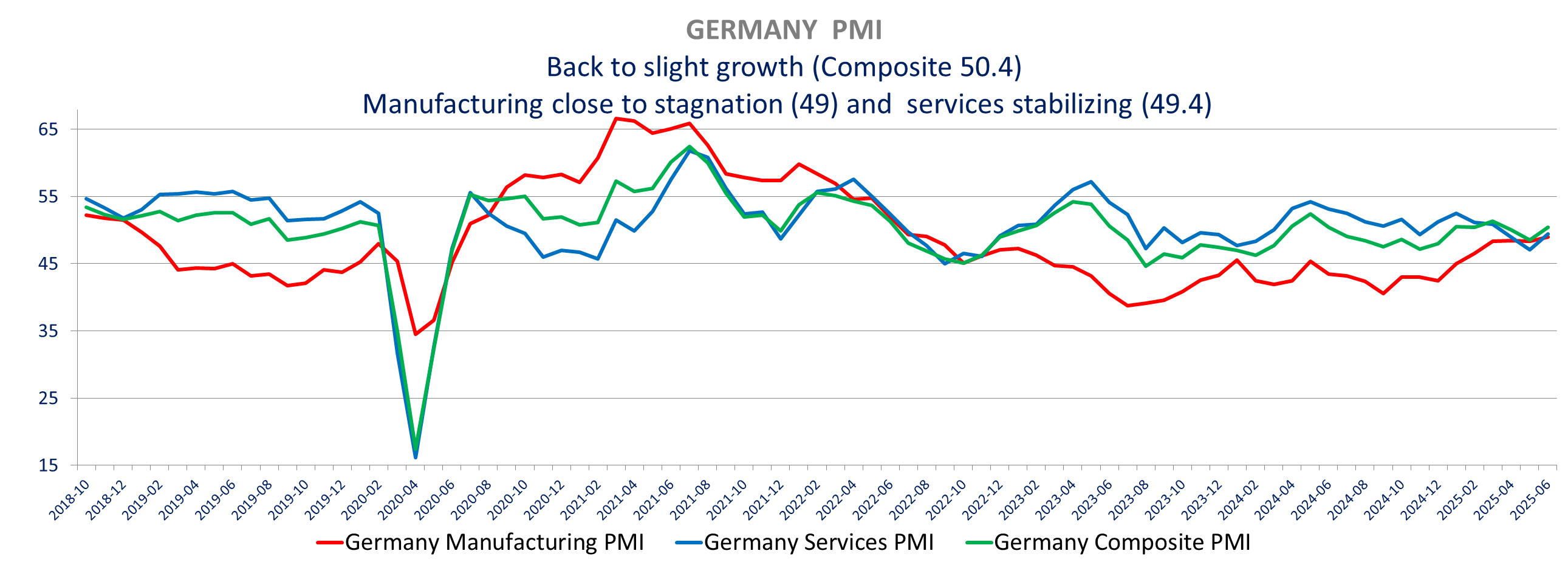

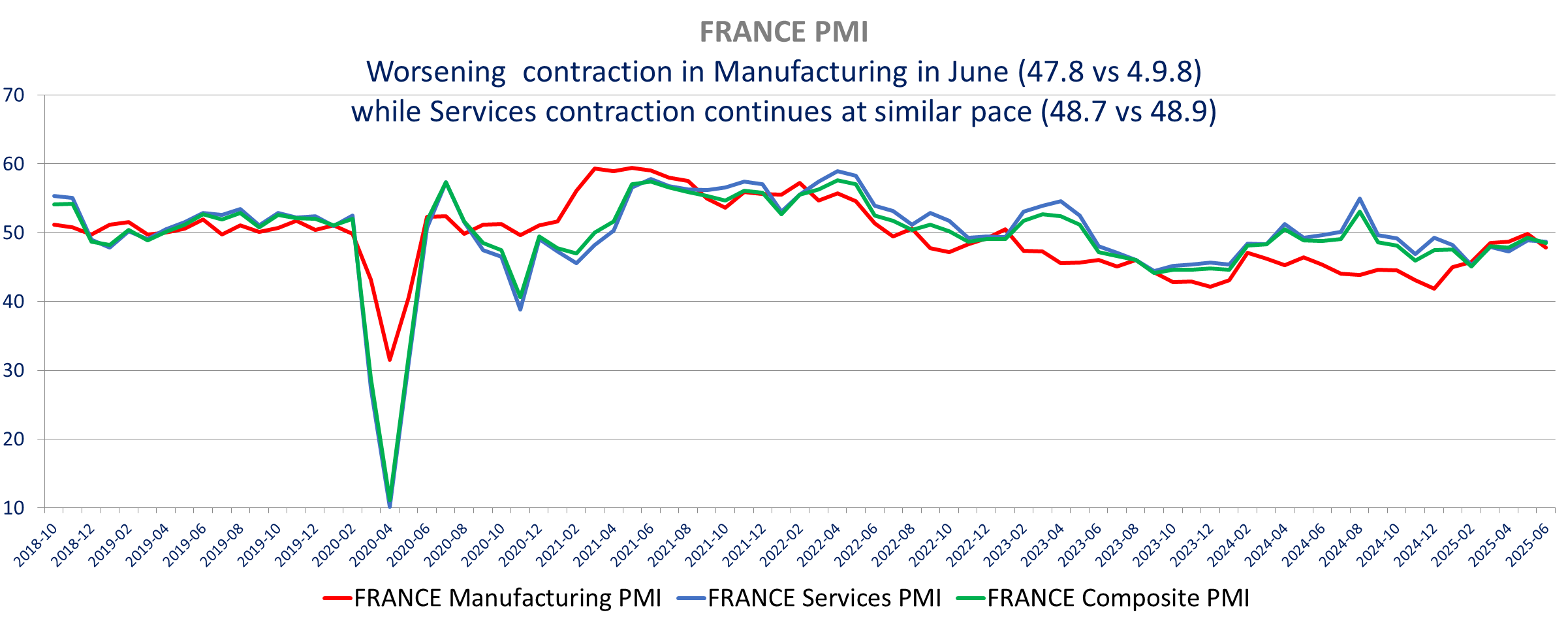

The improvement in Germany was compensated by weakness in France. Germany returned to slight growth with composite at 50.4 up from 48.5 ahead of expectations of 49. France is contracting at a faster rate in June with the composite at 48.5 down from 49.3 in May below expectations of 49.3.

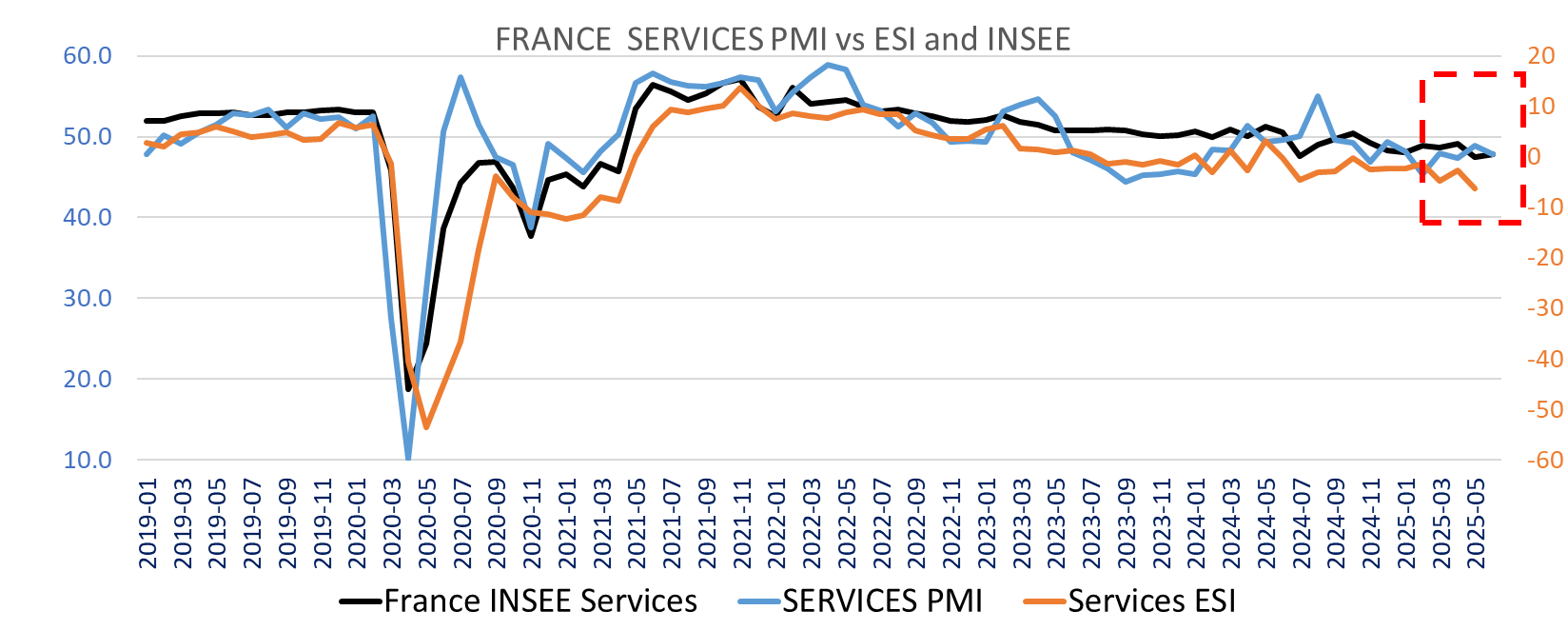

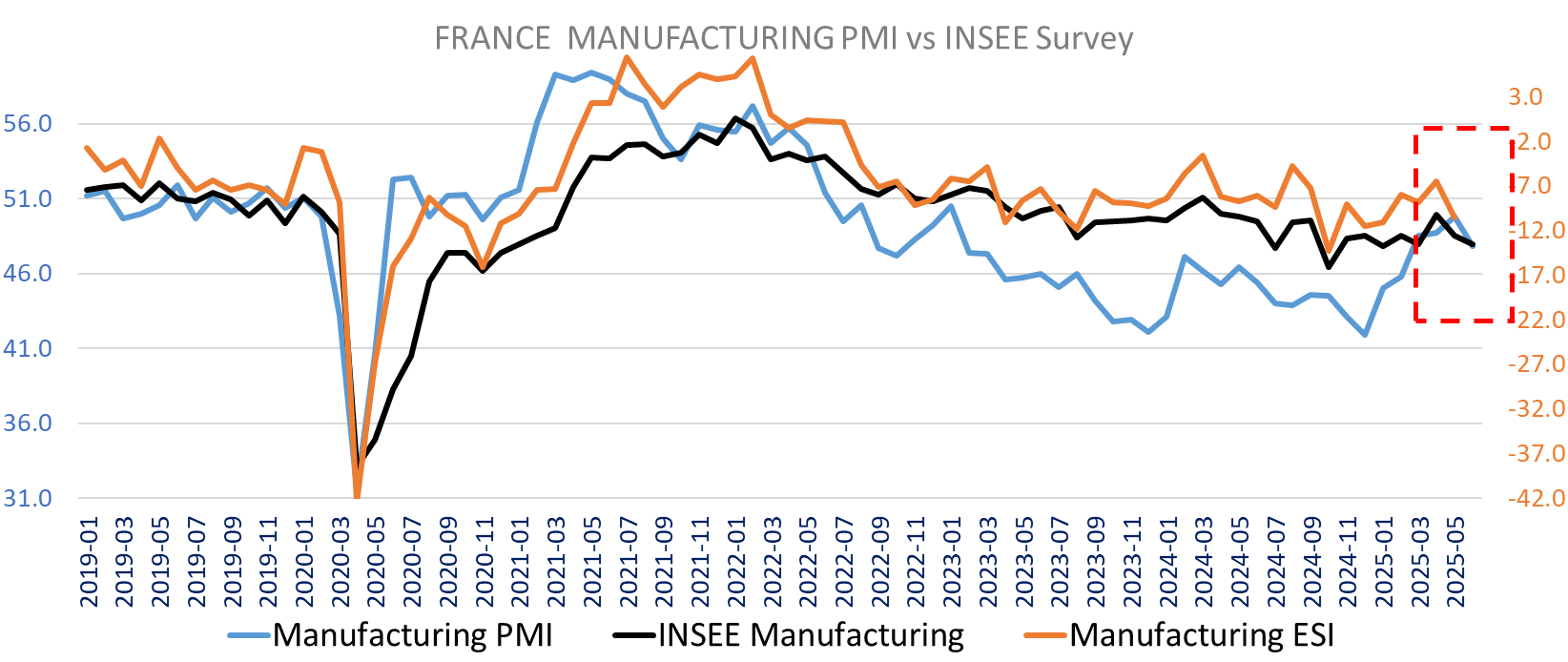

The better-than-expected German composite came from better Services PMI at 49.4 vs 47.1 in May ahead of expectations of 47.5. Manufacturing improved as well but in line with expectations Manufacturing at 49 vs 48.3 in May expectations, highest in 34 months. On the opposite side, France manufacturing deteriorated (as we saw with the INSEE survey) with the Manufacturing PMI down to 4-month low of 47.8 from 49.8 in May, far below expectations for an improvement to 50. The Services PMI is about unchanged at 48.7 vs 48.5 in May, but also below expectations of an increase to 49. The data suggest that the rest of the Eurozone saw slower growth in June: weaker growth in services in the rest of the Eurozone but a slight improvement in Manufacturing.

Employment is down in France and Germany but up in the rest of the Eurozone. The PMI points to increase in delivery times despite weaker orders and only limited increase in production (Eurozone output PMI at is down slightly to 51 from 51.5).

On the price front, we see a resurgence of selling price inflation in services: Services’ prices charged increased at the fastest rate in 3 months. France Services providers renewed increasing price charged in June joining German Services providers (although slightly less inflation than in May) and the rest of Eurozone. Manufacturing output prices declined slightly for the second month, But overall, the survey points to higher inflation.

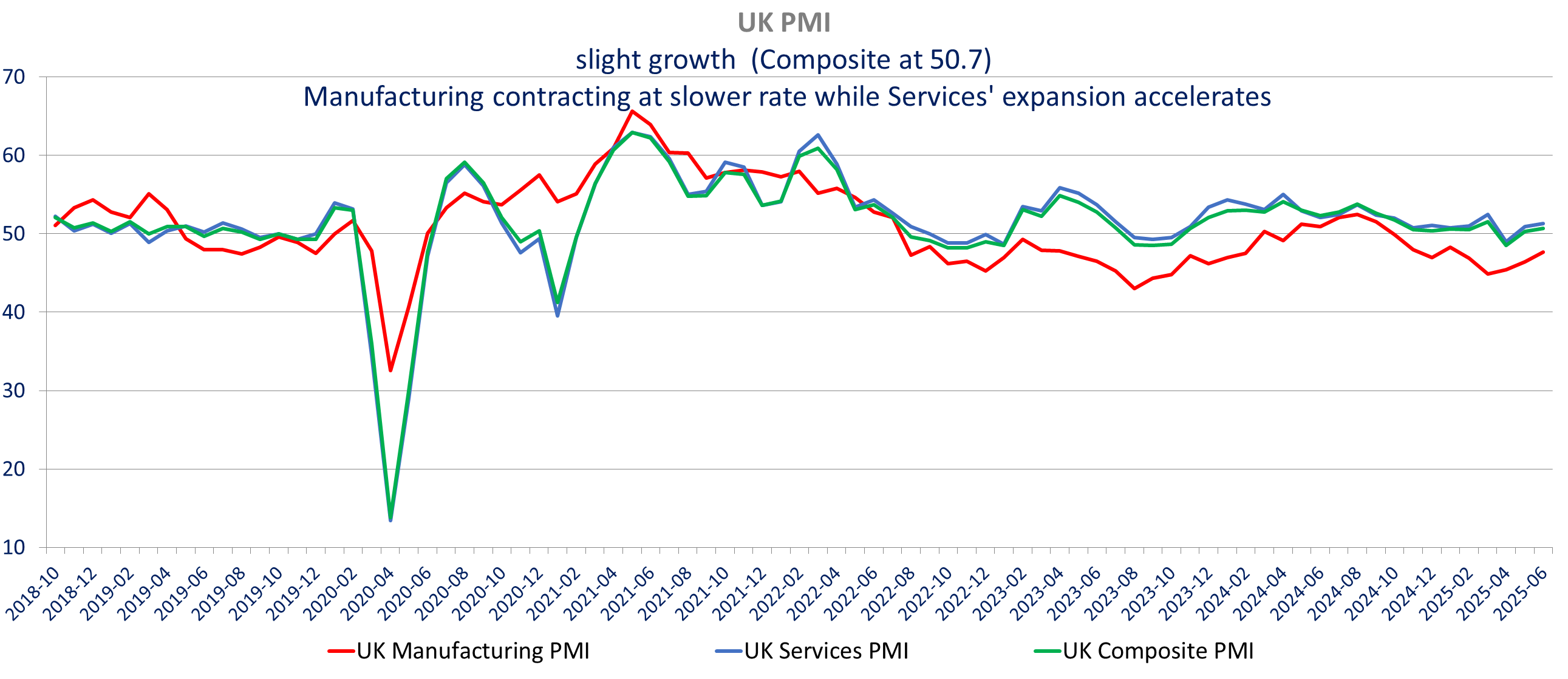

In the UK, the PMI improved in line with expectations in services (51.3 vs 50.9 in May) but the contraction in manufacturing eased more than anticipated: the PMI manufacturing is up to 47.7 from 46.4 vs 46.6 expected. New orders increased for the first time since November, due to an increase in domestic services demand. Manufacturing orders are down, on lower foreign demand. Employment decreased for the 9th consecutive month in June amid. Contrary to the eurozone, UK inflationary pressure continued to ease in June. Input costs inflation is the slowest in 3 months and services providers increased their prices to the slowest degree in over 4 years.

The PMI data supports a BoE rate cut in August and will give more weight for a summer pause for the ECB.

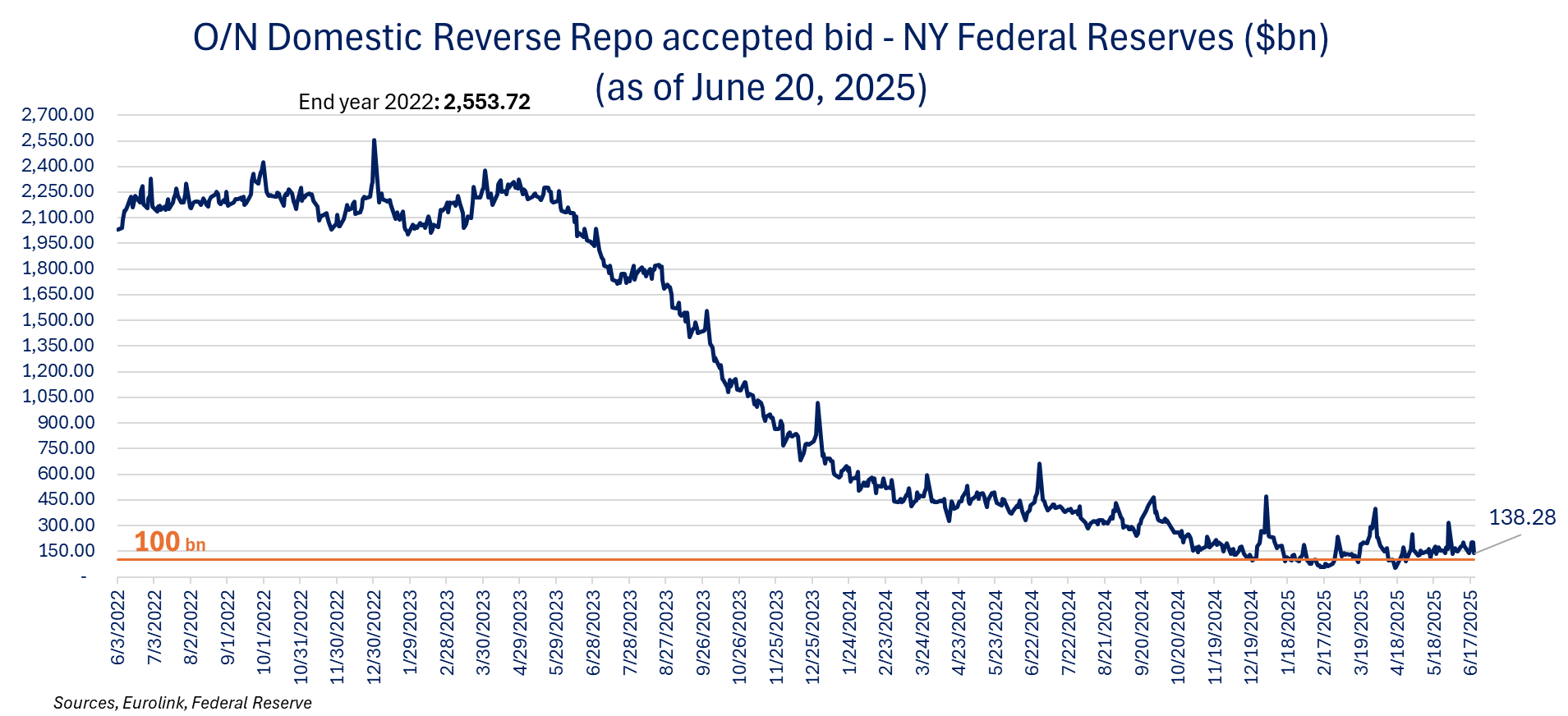

The latest Fed balance sheet update (published Friday after the market closed) showed greater tax receipts than expected. The Treasury General Account increased by +$106.83bn week-over-week to $383.85bn. Reserves are down -$106.68bn and with the increase of +$4.16bn in Federal Reserve’s notes in circulation, base money decreased by -$102.5bn w/w. The better tax receipts will probably give the US Treasury one- or two-weeks reprieve when the X-Date is concerned, but overall, we will still enter the danger zone by the end of July. The debt ceiling needs to be increased before that, but when it happens the rebuilding of the TGA (with no compensation from,) will tighten liquidity. The domestic RR is down to $138.28bn as of Friday.

On the companies’ front:. Holcim today completed its 100% spin-off of Amrize who focuses on building materials business in North America., through a dividend-in-kind distribution of one Amrize share for every outstanding Holcim share owned as of the close of business on 20 June 2025. Prosus reported FY25 results showing Ecommerce revenue growth of 21% and EBIT ahead of the pre-close guidance at $443m (435m pre-close) vs $38m a year ago. Spectris has agreed to be acquired by MI Metron UK Bidco, an indirect subsidiary of funds managed by private equity firm Advent International, in a deal that values the company’s equity at £3.8 billion and its enterprise value, including debt, at £4.4 billion. Under the proposed terms, Spectris shareholders will receive £37.63 per share in cash, comprising £37.35 per share in cash consideration and an interim dividend of 28 pence. Dassault Aviation signed a letter of intent to explore potential partnerships with the European Space Agency. Dassault Aviation interest in automated LEO platforms suitable for commercial and institutional markets, led them to develop a vehicle concept called “Véhicule Orbital Réutilisable de Transport et d’Exploration (VORTEX)”, designed for research in space, transport of cargo to and from space stations, and a range of in-orbit services More details on equities here

RECAP TABLE EUROPEAN FALSH PMI

Better tax receipts in June, leading to a larger increase in the TGA than expected last week. The Treasury General Account increased by $106.83bn Week over week to $383.85bn while the domestic reverse Repo was stable (+$425m w/w) at $205.05. (The Domestic RR fell to $138.38bn as of Friday and will re-increase at the end of the month / quarter).

The total assets were up only marginally (+$3.9bn w/w) with no change in securities holdings, slight increase in primary credit (+$1.4bn) and other assets up $3.15bn

Bottom line, Reserves are down -$106.68bn and with the increase of +$4.16bn in Federal Reserve’s notes in circulation, base money decreased by -$102.5bn w/w.

The Better tax receipts will probably give the US Treasury one- or two-weeks reprieve when the X-Date is concerned, but overall, we will enter the danger zone by the end of July.

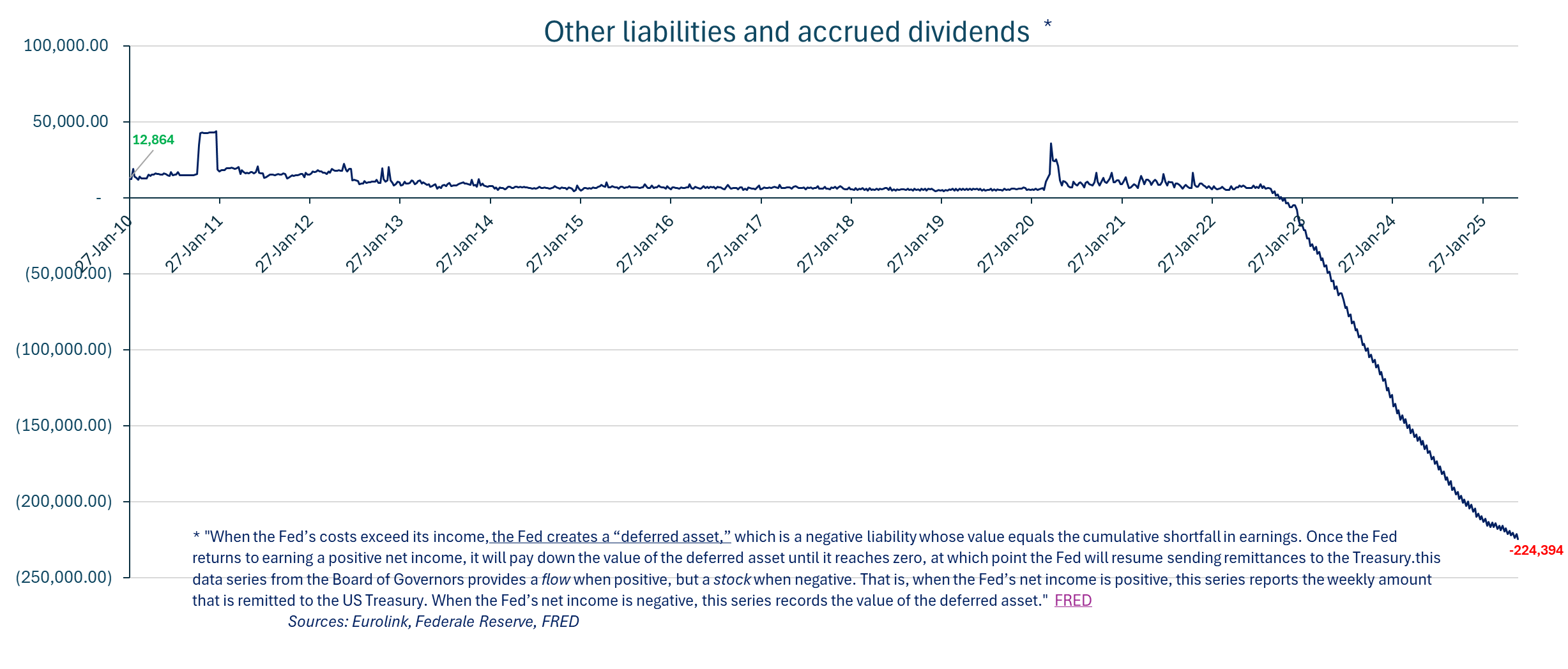

The Fed losses continue to increase, reaching -$224.39bn as of last Wednesday.

The Eurozone composite PMI is slightly below expectation of 50.5, unchanged in June at 50.2, consistent with stagnation. The Eurozone Manufacturing PMI is also unchanged from May to 49.4, slightly below expectations of 49.8, and the services PMI improved slightly to 50 from 49.7 in May in line with expectations.

The improvement in Germany was compensated by weakness in France (aligned with last week’s INSEE survey).

Germany returned to slight growth with composite at 50.4 up from 48.5 ahead of expectations of 49. The better-than-expected composite came from better Services PMI at 49.4 vs 47.1 in May ahead of expectations of 47.5. Manufacturing improved as well but in line with expectations Manufacturing at 49 vs 48.3 in May expectations, highest in 34 months.

On the opposite side, France manufacturing deteriorated (as we saw with the INSEE survey) with the Manufacturing PMI down to 4-month low of 47.8 from 49.8 in May, far below expectations for an improvement to 50. The Services PMI is about unchanged at 48.7 vs 48.5 in May, but also below expectations of an increase to 49.2. France is therefore contracting at a faster rate in June with the composite at 48.5 down from 49.3 in May below expectations of 49.3.

The rest of the Eurozone continues to grow but HCOB says “the rate of growth eased to the slowest since last November”, The data suggest weaker growth in services in the rest of the Eurozone but a slight improvement in Manufacturing.

Germany manufacturing output PMI rose to 52.6 in June (51.4 in May) the highest level in 39 months. The German manufacturing PMI is at the highest in 34 months at 49 in line with expectations, but the Services PMI is higher than expected at 49.4 (47.5 expected) up from 47.1 in May. The June IFO survey will be released tomorrow,

In contrast with Germany, France manufacturing production contacted in June: the output PMI declined to 47.2 from 51.0 in May. This is aligned with the INSEE Survey (production -1.3 in June vs +2.9 in May). The Manufacturing PMI is down, to 47.8 from 49.8, while an increase to 50.0 was expected by economists. Services contracted at a steady pace (48.7 vs 48.9 in May) while expectations were for a slower rate of contraction (49.2).

The UK economy accelerated slightly more than expected in June with the composite PMI at 50.7 up from 50.3 in May, better than 50.5 anticipated by economists. The Services PMI is in line with expectations at 51.3% showing an acceleration from 50.9 in May. The manufacturing PMI beat expectations at 47.7 (5-month high), up from 46.4 while forecasts were 46.6.

Manufacturing output continued to decline but less than in May (47.1 vs 46.5).

|

|

Monday, June 23, 2025 | ||

|

SXS | |||

|

GBp |

3792.00 |

+15.54% | |

|

SXS |

Spectris has agreed to be acquired by MI Metron UK Bidco, an indirect subsidiary of funds managed by private equity firm Advent International, in a deal that values the company’s equity at £3.8 billion and its enterprise value, including debt, at £4.4 billion. Under the proposed terms, Spectris shareholders will receive £37.63 per share in cash, comprising £37.35 per share in cash consideration and an interim dividend of 28 pence. | ||

|

|

|

|

|

|

HOLN | |||

|

CHF |

54.32 |

+14.12% | |

|

HOLN |

Holcim today completed its 100% spin-off of Amrize who focuses on building materials business in North America., through a dividend-in-kind distribution of one Amrize share for every outstanding Holcim share owned as of the close of business on 20 June 2025. | ||

|

|

|

|

|

|

PRX | |||

|

EUR |

47.60 |

+3.19% | |

|

PRX |

Prosus reported FY25 results showing Ecommerce revenue growth of 21% and EBIT ahead of the pre-close guidance at $443m (435m pre-close) vs $38m a year ago. Food Delivery EBIT reached £218m vs $38m a year ago on 30% revenue growth. Classified revenues went up18% and EBIT +61% to $373m. Payments & Fintech revenues +34% and EBIT $-11m vs $-31m. "We expect this momentum to continue, and to add at least the same level of incremental aEBIT in FY26. FY2025 marks the first year that Prosus is free cash flow positive, excluding the Tencent dividend, with a free cash flow improvement of US$513m." We completed the acquisition of Despegar in May 2025 and are already integrating its products into iFood’s Clube membership. We are making good progress with the purchase of Just Eat Takeaway.com, which will create a new AI-powered tech champion in Europe." | ||

|

|

|

|

|

|

AM | |||

|

0 |

301.80 |

-1.05% | |

|

AM |

Dassault Aviation signed a letter of intent to explore potential partnerships with the European Space Agency. ESA, with its ambitious strategy for space exploration, Explore2040, is seeking innovative solutions for capabilities development to reach and return from Low Earth Orbit (LEO), Moon and Mars, and supports the advancement of selected critical enabling technologies to be used and demonstrated in particular in LEO, such as hypervelocity re-entry. Dassault Aviation interest in automated LEO platforms suitable for commercial and institutional markets, led them to develop a vehicle concept called “Véhicule Orbital Réutilisable de Transport et d’Exploration (VORTEX)”, designed for research in space, transport of cargo to and from space stations, and a range of in-orbit services. | ||

Versus early hours:

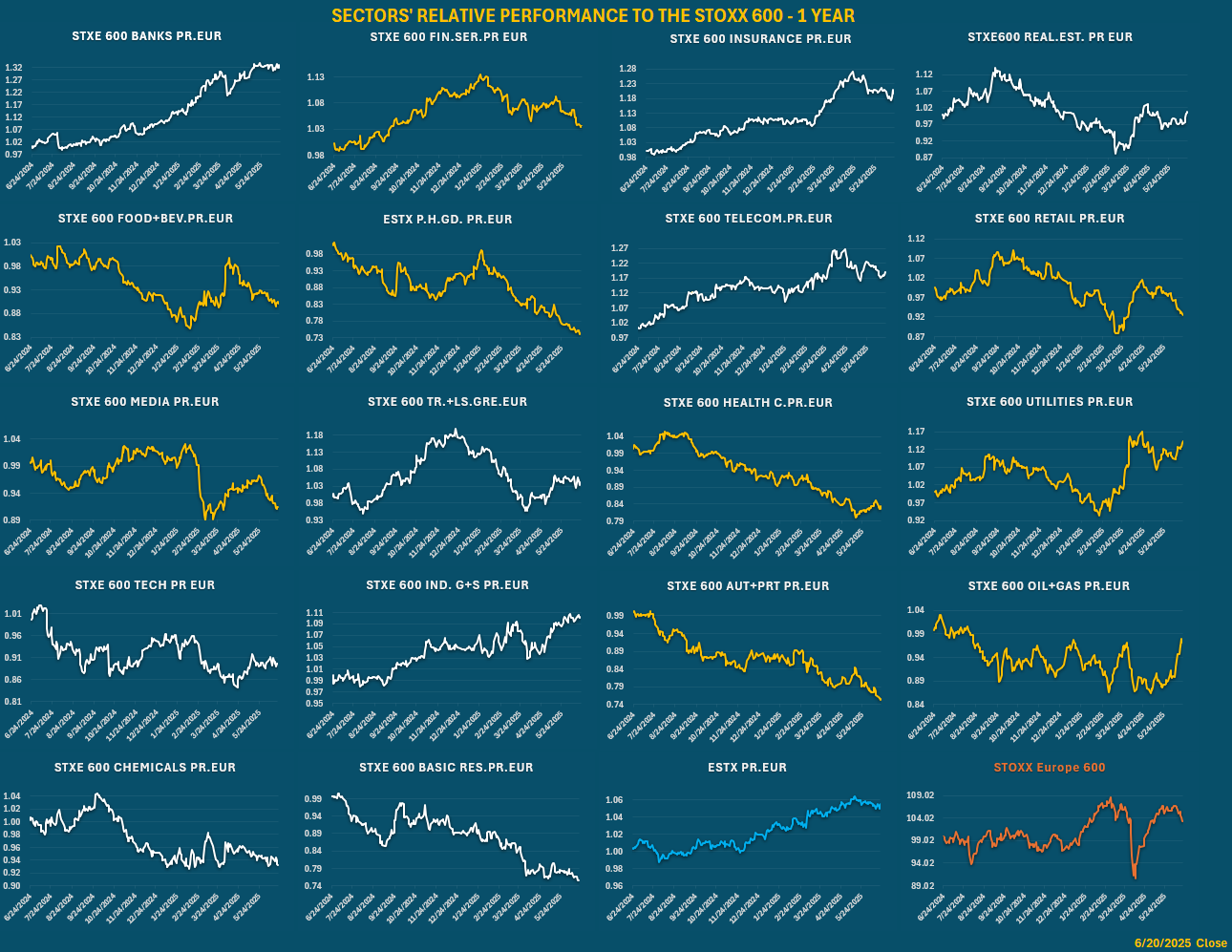

SECTOR PERFORMANCE

Relative performance to STOXX 600

Today’s Performance

Versus early hours:

Indices

Versus early hours

Commodities

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.