As expected, the BoJ left rates unchanged. As anticipated the Japanese Central Bank also announced a slowdown in the pace reduction of the bond purchased to ¥200bn from ¥400bn per quarter but only in April 2026… Japanese bond yield increased post decision. With the BoJ remaining cautious on rates and inflation remaining elevated, seeking a higher ¥ seems the logical path to follow.

The hope for a quick de-escalation in the Middle East is not materializing. A regime change appears as a target now not pointing to a quick end of hostility. It still does not help the $ to catch a bid. Oil is up, stock down with market more alike Friday’s session.

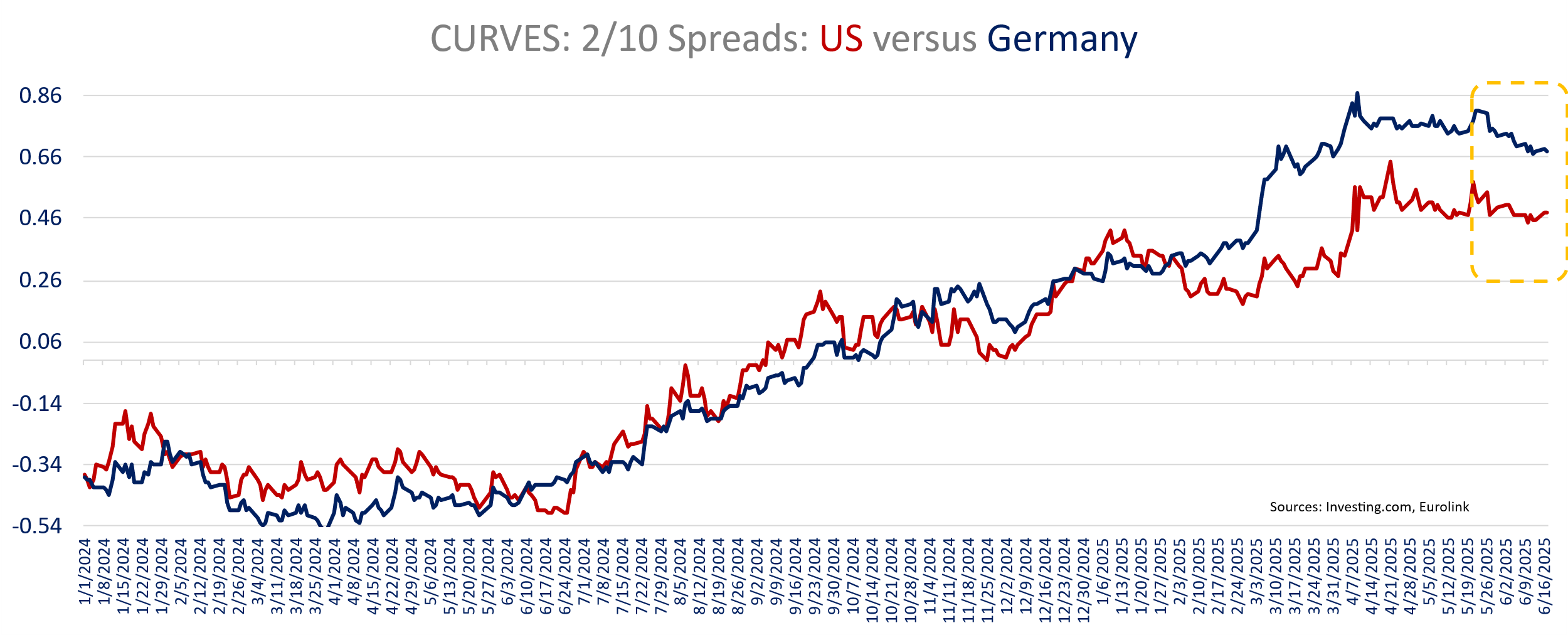

Bond yields are a tad lower though, supported by the solid 20yr auction yesterday. Bund yields open higher but are now lower going into the US retail sales data, but once again, we see some slight widening in European sovereign spreads (Italy 10 yr BTP at +97bp over Bund).

Presidential early departure from the G7, i.e. not meeting with NATO head nor Zelinski, does not help sentiment that the US administration seek further distancing from the global orders it installed post WWII.

The Bill changes in the Senate cast doubts on the ability to pass the bill by Independence Day. The Senate also raised the proposal for the debt ceiling increase to $5tn.

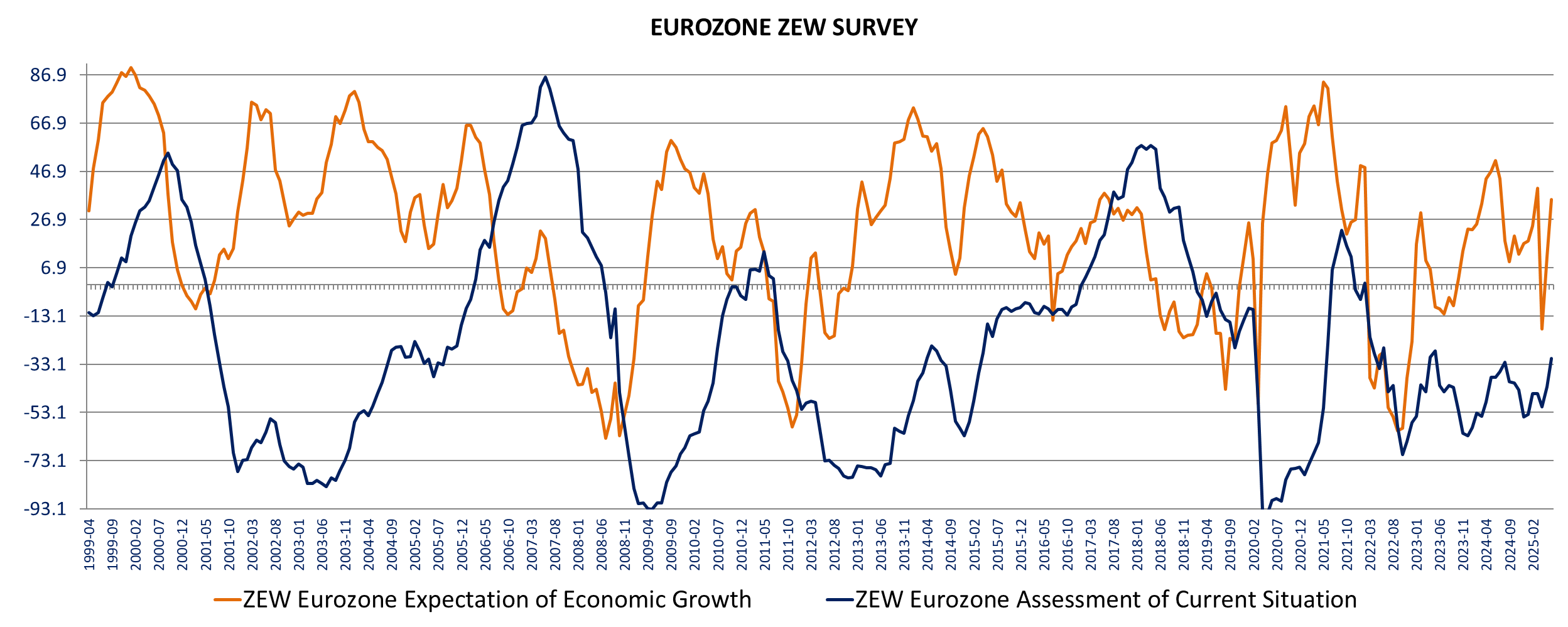

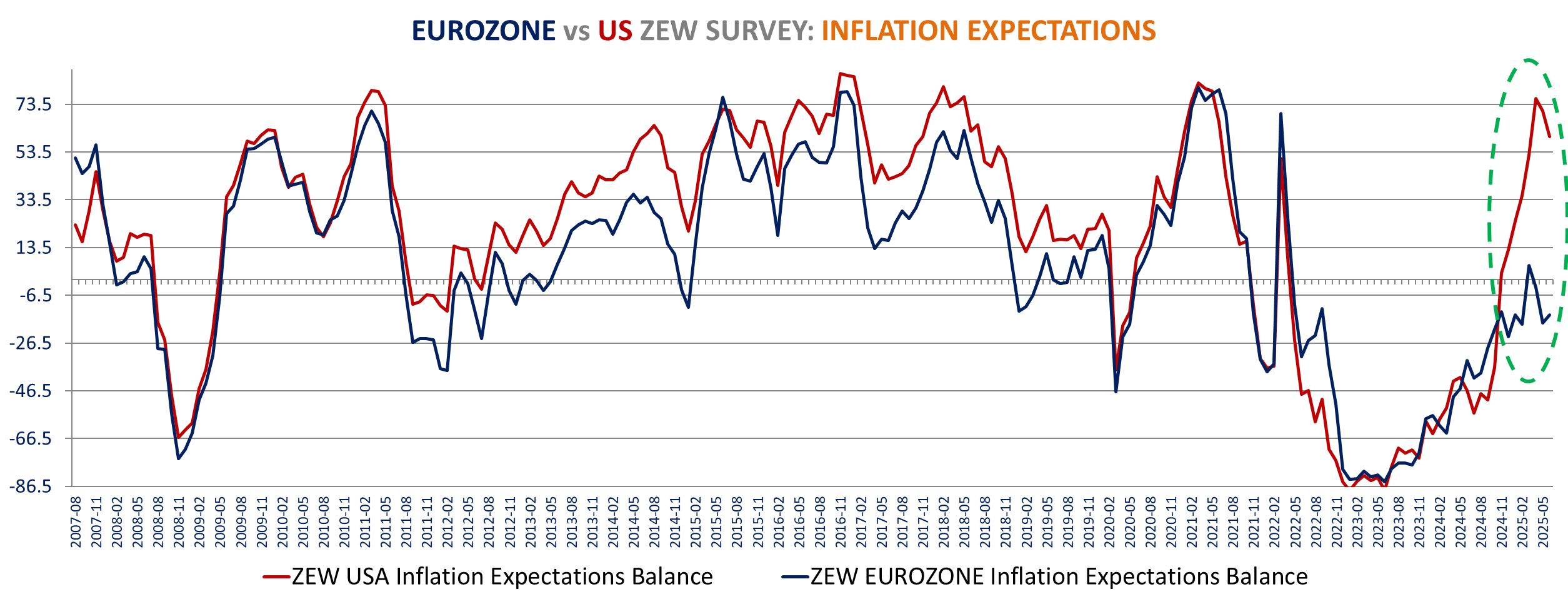

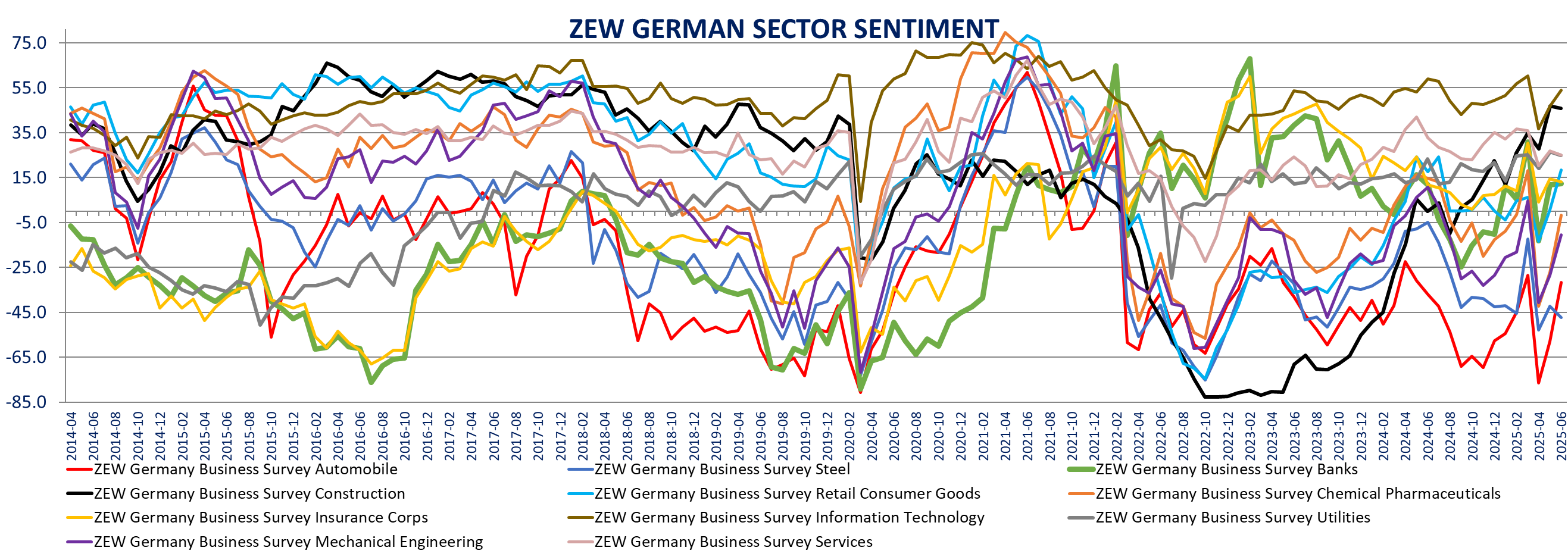

Light day on the data front on the European side. Beside the headlines, the details of ZEW survey of market professionals are interesting:

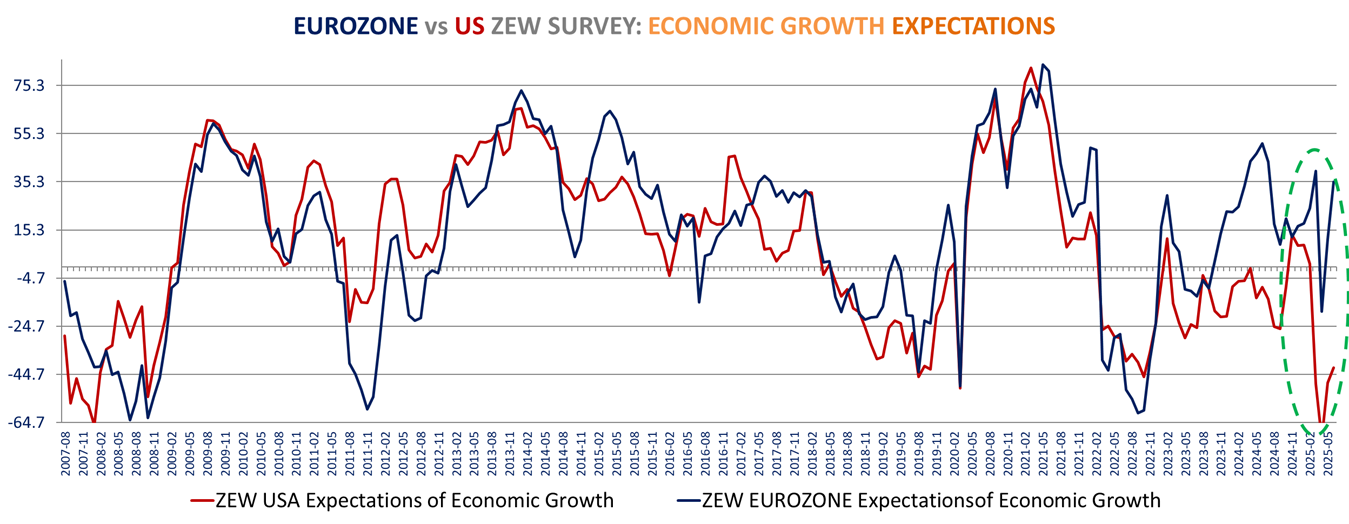

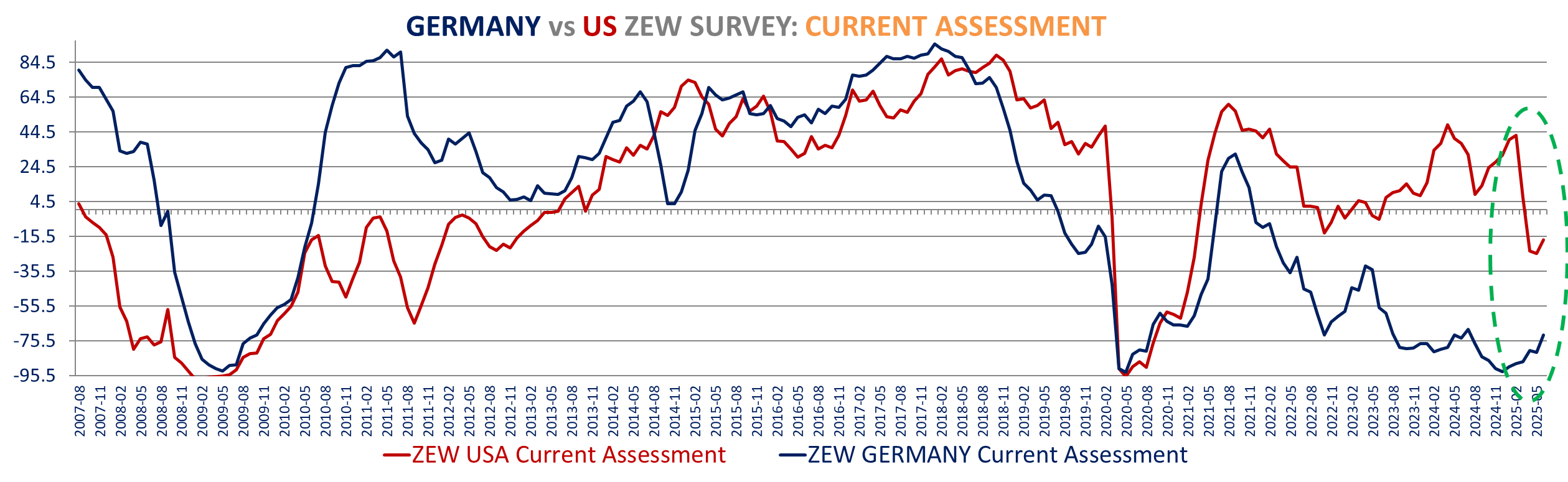

Sentiment for the Eurozone and Germany improved significantly – and more than expectations – in June. The Eurozone current assessment is up +11.7 points to -30.7, the best in more than 2 years (May 2023) and expectations surged +23.7 points to +35.3, almost back to the pre-tariff March level and far above consensus expectations of 23.5. For the US the sentiment also improved but to a lesser extent: current assessment up +8.1 points to -17.3 (highest since March) and expectations up +6.3 points to -41.9, only highest since February.

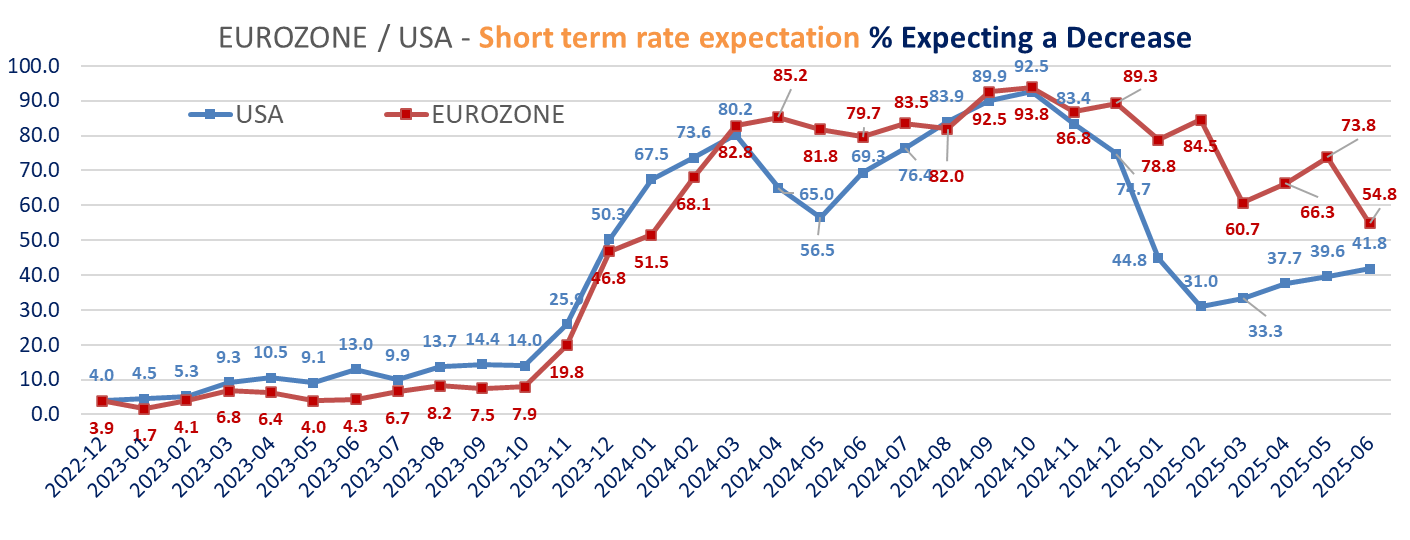

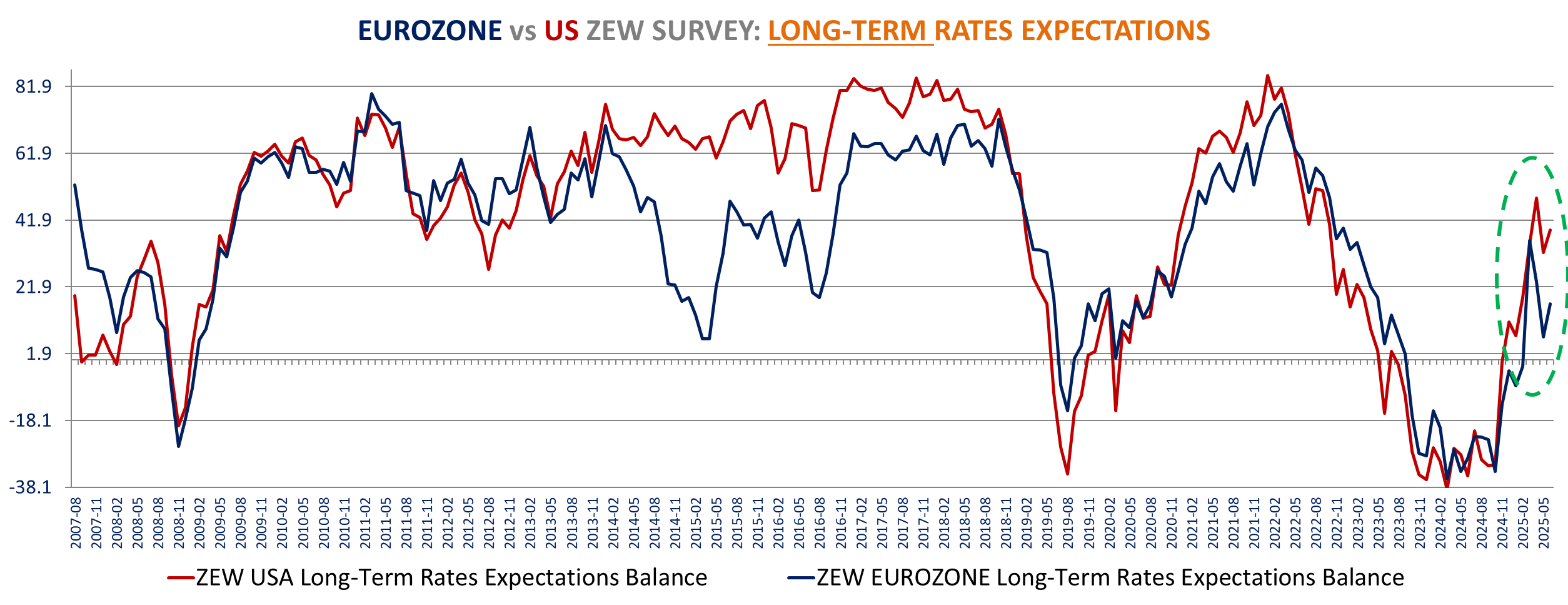

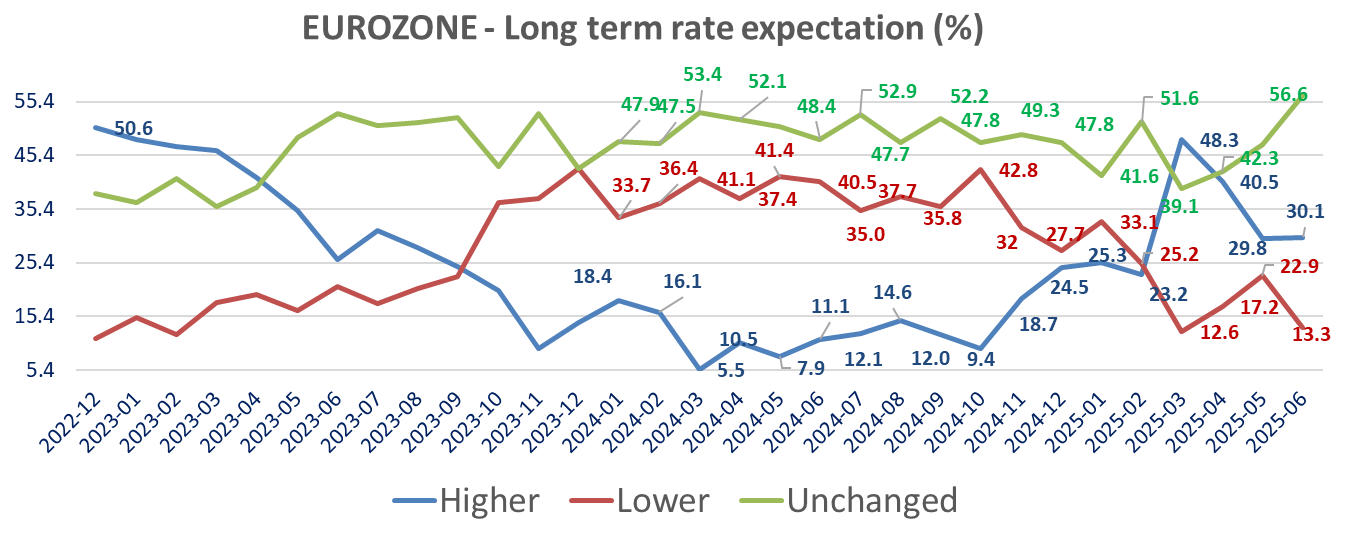

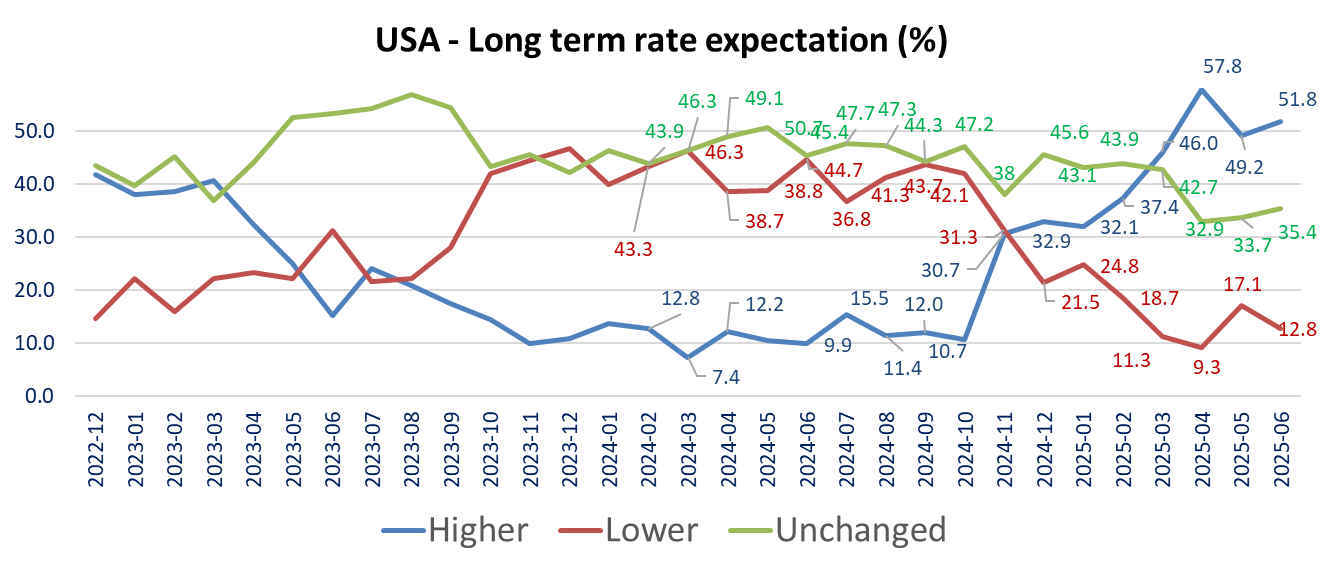

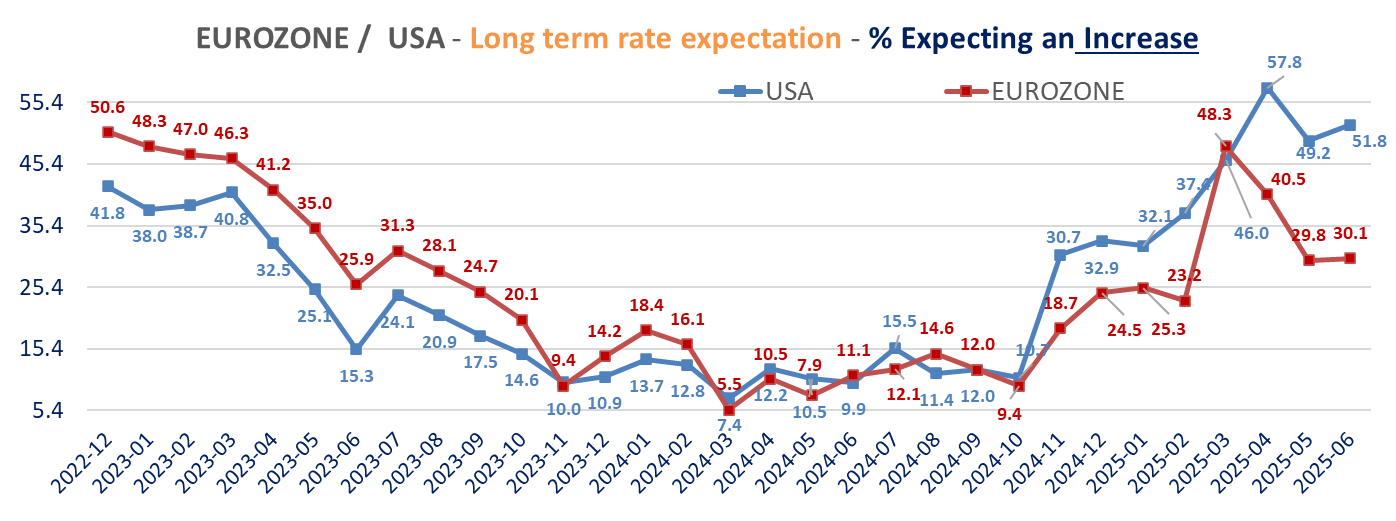

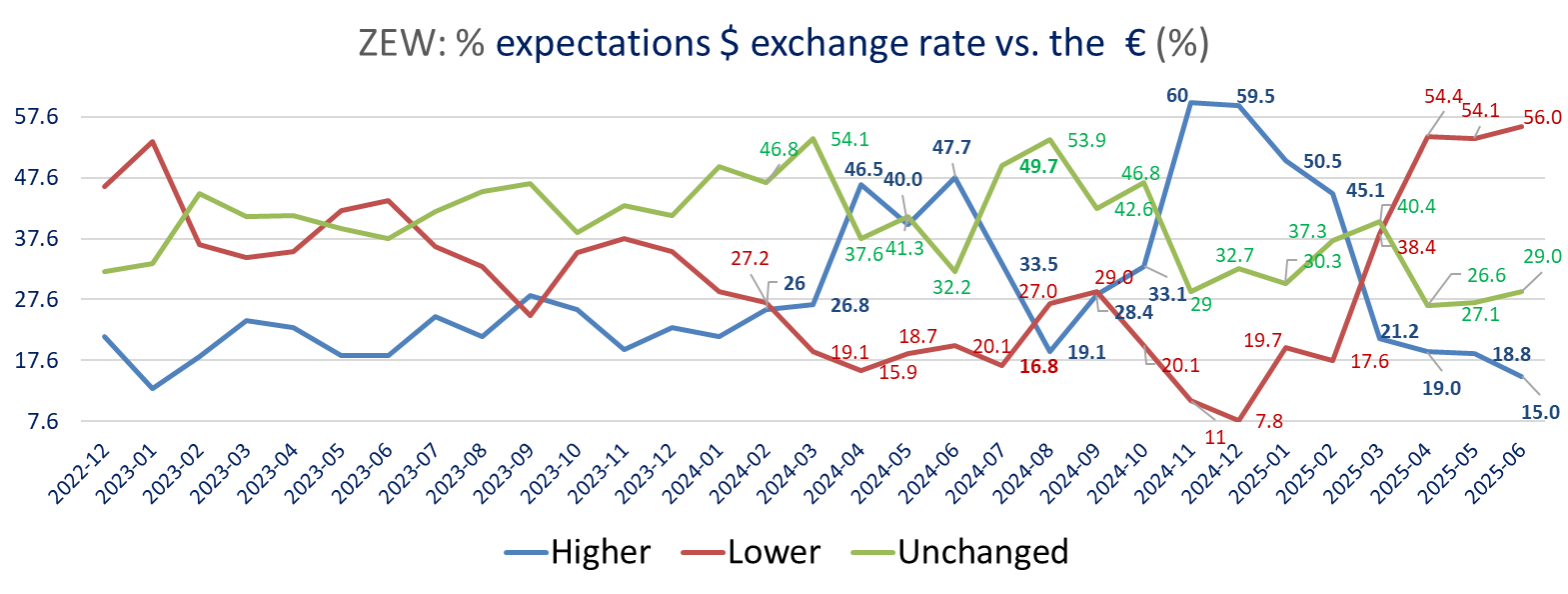

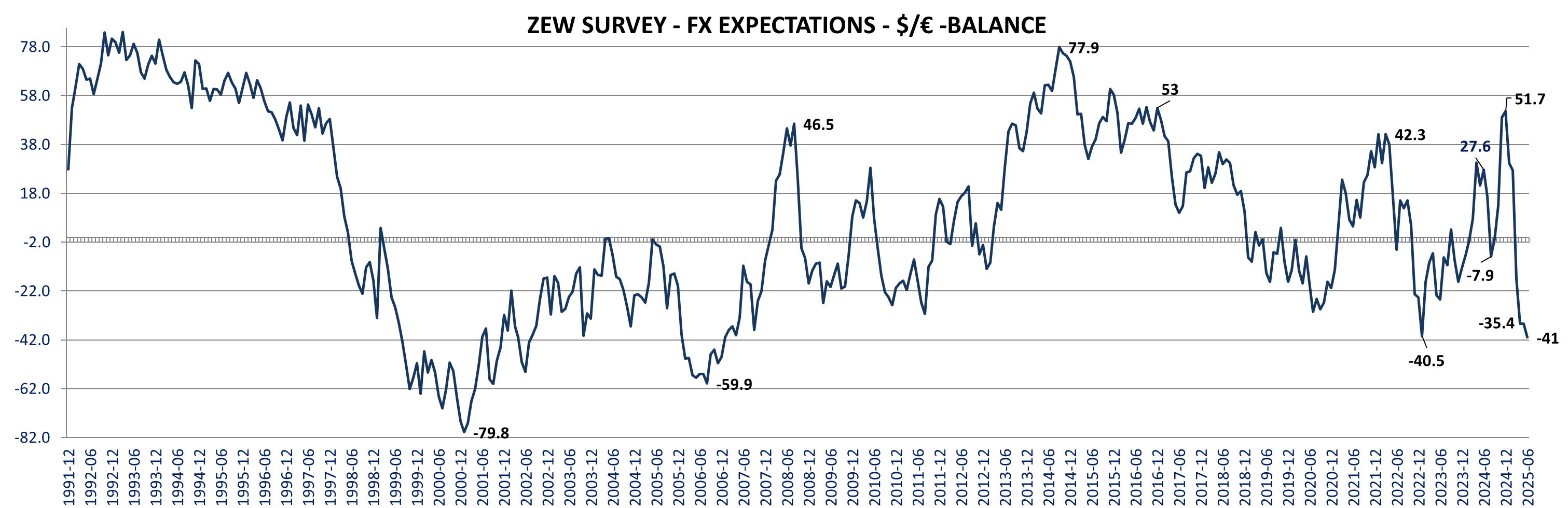

The ZEW survey’s details shows than investors sentiment toward the dollar is the weakest since December 2006 in June (with 56% expect a weaker $ vs. the €, up from 54.1), but it also shows a increase in inflation expectations in Europe, lower in the US, lower rate cuts expectations in Eurozone more investors seeing lower short term rates in the US. Investors’ long-term rates expectations are higher for both regions but with different dynamics between the two regions. More expect higher rates in the US, 51.8% up from 49.2%. For Germany, less expect a decrease (13.3% vs 22.9%) while 30.1% see an increase barely changed from 29.8% in May.

Investors are more positive on European stock markets but more negative for the Dow.

On the companies’ front: Keing announced the appointment of Luca de Meo as Chief Executive Officer of the Group. As part of a renewed governance structure, the role of Chairman of the Board of Directors, held by François-Henri Pinault, will be separated from that of Chief Executive Officer. Luca de Meo will take office on September 15, 2025. For FY2026 Ashtead sees rental revenues up 0 to 4% compared to the 4% reported today in FY2025. Capex is expected around $1.8 to $2.2bn vs $2.4bn in FY25, consequently the FCF is guided around $2-2.3bn vs $1.8bn in FY25. "While completions continue to outpace starts in local non-residential construction, mega project activity continues to be robust, particularly in the data center, semiconductor and LNG space”. Legal & General confirms its 2025 guidance and expects that 70-75% of Asset Management earnings will be fee-related, and cost income ratio will reduce to below 70% by 2028. Fresenius Medical Care presented its new Reignite strategy. The Company also introduced the 5008X dialysis machine and unveils launch plans in the USMore details on equities here

Debt Ceiling : Senate raise the proposal to an increse of $5tn from $4tn..

`

Sharp improvement in the Eurozone ZEW survey in June: Current assessment is up +11.7 points to -30.7 the best in more than 2 years (May 2023) and expectations surged +23.7 points to +35.3, almost back to the pre-tariff March level and far above consensus expectations of 23.5 (Trading economics).

Germany current assessments are up 10 points to -72 best since July 2024 and expectations increase +22.3 points to +47.5 also best since March also above expectations of 35. ZEW Release, ZEW table.

For the US the sentiment also improved but to a lesser extent: current assessment up +8.1 points to -17.3 (highest since March) and expectations up +6.3 points to -41.9 only highest since February.

INTEREST RATES

|

|

Tuesday, June 17, 2025 | ||

|

AHT |

ASHTEAD GROUP PUBLIC LIMITED COMPANY | ||

|

GBp |

4391.00 |

+0.21% | |

|

AHT |

For FY2026 Ashtead sees rental revenues up 0 to 4% compared to the 4% reported today in FY2025. Capex is expected to be around $1.8 to $2.2bn vs $2.4bn in FY25, consequently the FCF guided around $2-2.3bn vs $1.8bn in FY25. During FY2025, Ashtead delivered Group rental revenue up 4% while revenue was down 1%, impacted by lower sales of used equipment. Adjusted profit before taxation of $2,128m (2024: $2,230m. | ||

|

|

|

|

|

|

DG |

Vinci SA | ||

|

EUR |

124.60 |

-0.52% |

|

|

DG |

May traffic after market close | ||

|

|

|

|

|

|

ADP |

Aeroports de Paris SA | ||

|

EUR |

108.30 |

-1.01% | |

|

ADP |

May 2025 traffic: Group traffic: 32.4 million passengers, up +2.7%; – Paris Aéroport's traffic: 9.4 million passengers, up +3.3%. | ||

|

|

|

|

|

|

LGEN |

LEGAL & GENERAL GROUP PLC | ||

|

GBp |

254.20 |

-0.86% | |

|

LGEN |

Analyst day. "Today's presentation will set out why our Asset Management business is well-positioned for profitable, sustainable growth, and our strategy and plans to address this opportunity." Demand for retirement solutions is growing globally. As a market leader in UK Defined Benefit (DB) and Defined Contribution (DC), and the UK's largest asset manager with a growing international presence, we are well-positioned to capitalize on this opportunity." 2028 targets: will deliver £500-600m operating profit (6-10% CAGR 2024-28) through a combination of fee earnings growth (9-15% CAGR 2024-28) and cost discipline. By 2028, 70-75% of Asset Management earnings will be fee-related, and the cost income ratio will reduce to below 70%. Current Outlook: "We have made a good start to 2025 and are on track to deliver results in line with our 3-year targets, therefore we expect growth in 2025 Group core operating EPS of between 6-9%." | ||

|

|

|

|

|

|

KER |

Kering SA | ||

|

EUR |

187.08 |

-3.01% | |

|

KER |

Keing announced the appointment of Luca de Meo as Chief Executive Officer of the Group. As part of a renewed governance structure, the role of Chairman of the Board of Directors, held by François-Henri Pinault, will be separated from that of Chief Executive Officer. Luca de Meo will take office on September 15, 2025. | ||

|

|

|

|

|

|

FME |

Fresenius Medical Care AG | ||

|

EUR |

48.26 |

-1.91% | |

|

FME |

CMD: today Fresenius unveiled its new FME Reignite strategy at its Capital Markets Day in London. FME Reignite centers on value creation, based on three strategic elements: Reignite the core, Reignite growth and innovation and Reignite our culture. In the global market the average annual growth for the number of dialysis patients is projected to be between 4 and 5 percent between 2025 and 2035. This includes an average annual patient number growth of 2 plus percent in the U.S. in the same timeframe. The number of people on maintenance dialysis is expected to grow by 90 percent globally to 7 million people by 2035. The Company also introduced the 5008X dialysis machine and unveils launch plans in the US. Under this plan, the company savings target expanded by €300m to €1.05bn by 2027. Profitability aspirations set for 2030 to advance to mid-teens percent industry-leading operating income margins. optimization of capital structure with lowered net leverage ratio target band of 2.5x to 3.0x. Commitment to return excess capital to shareholders: 30-40 percent dividend ppayout plusinitial share buyback program of €1 billion | ||

Bonds:

Versus early hours:

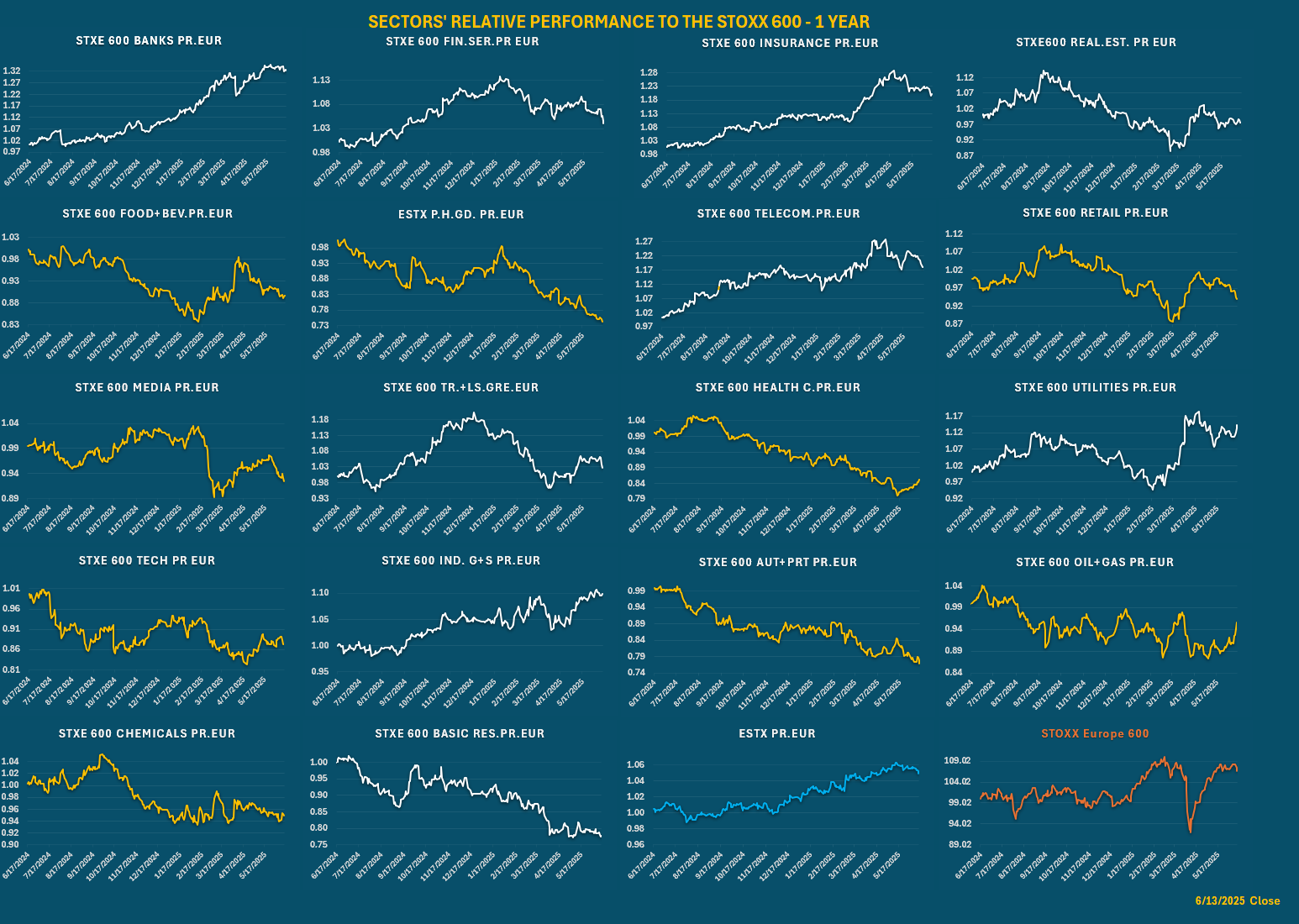

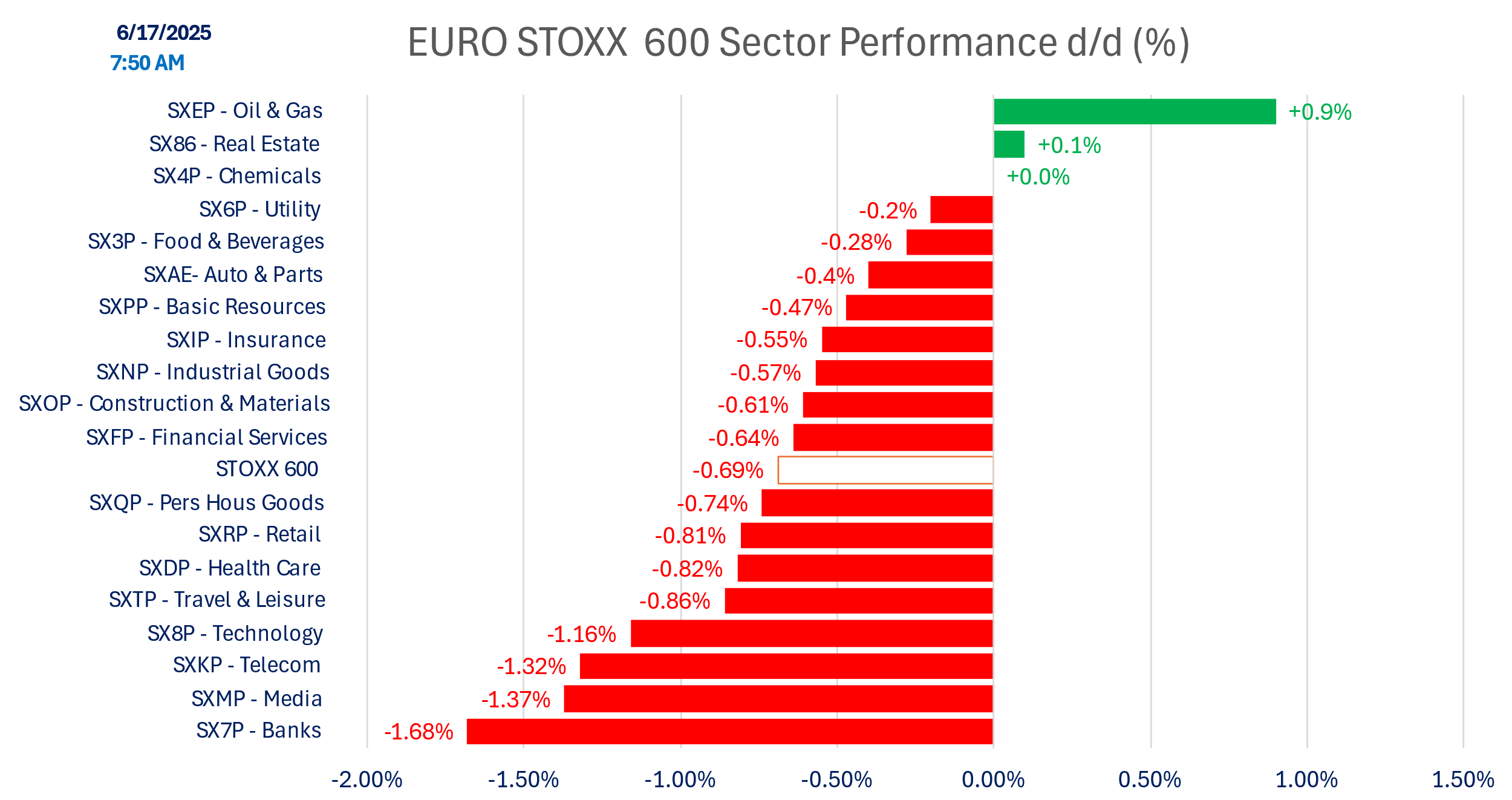

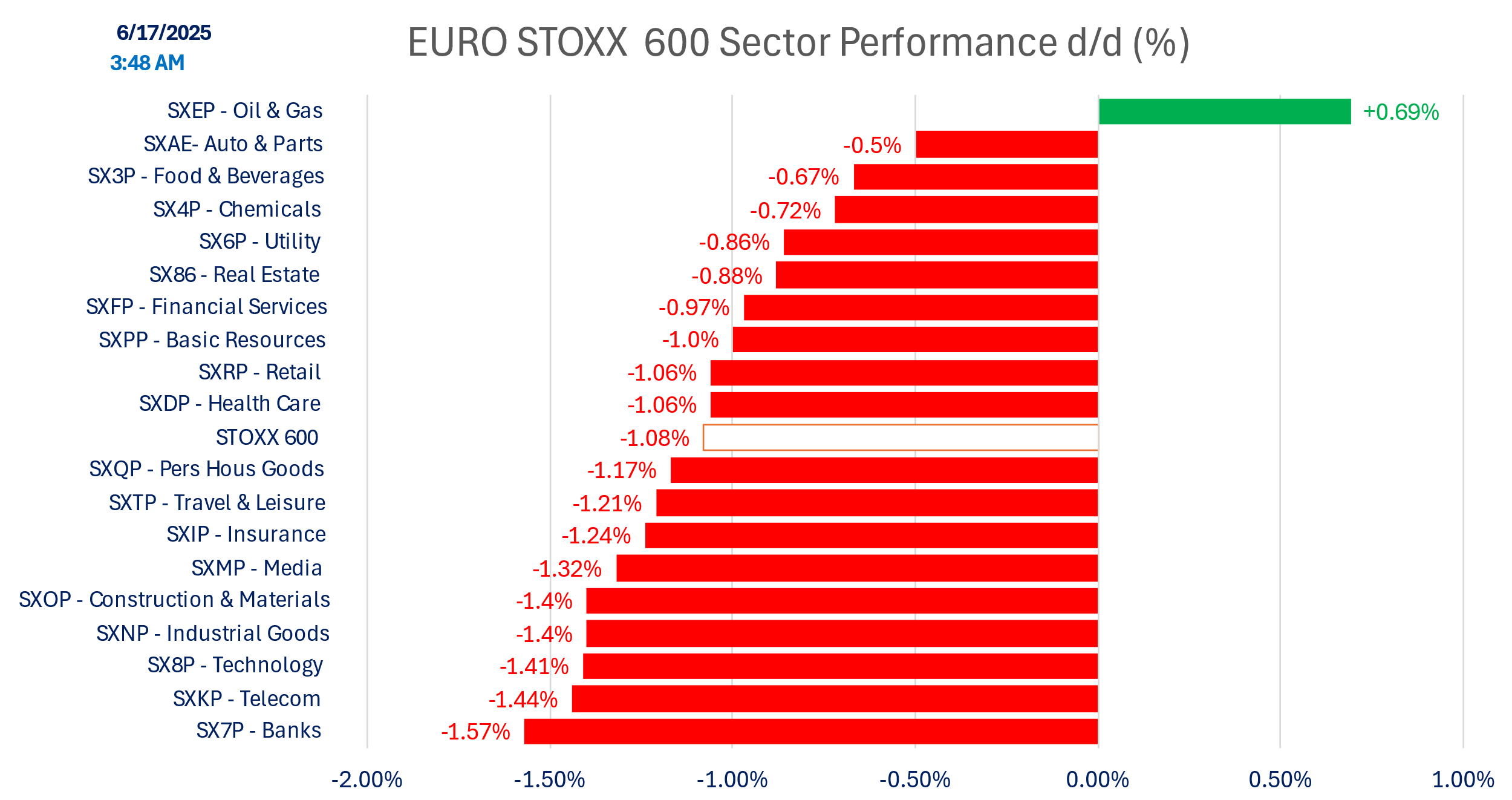

SECTOR PERFORMANCE

Relative performance to STOXX 600

Today’s Performance

Versus early hours:

Indices

Versus early hours

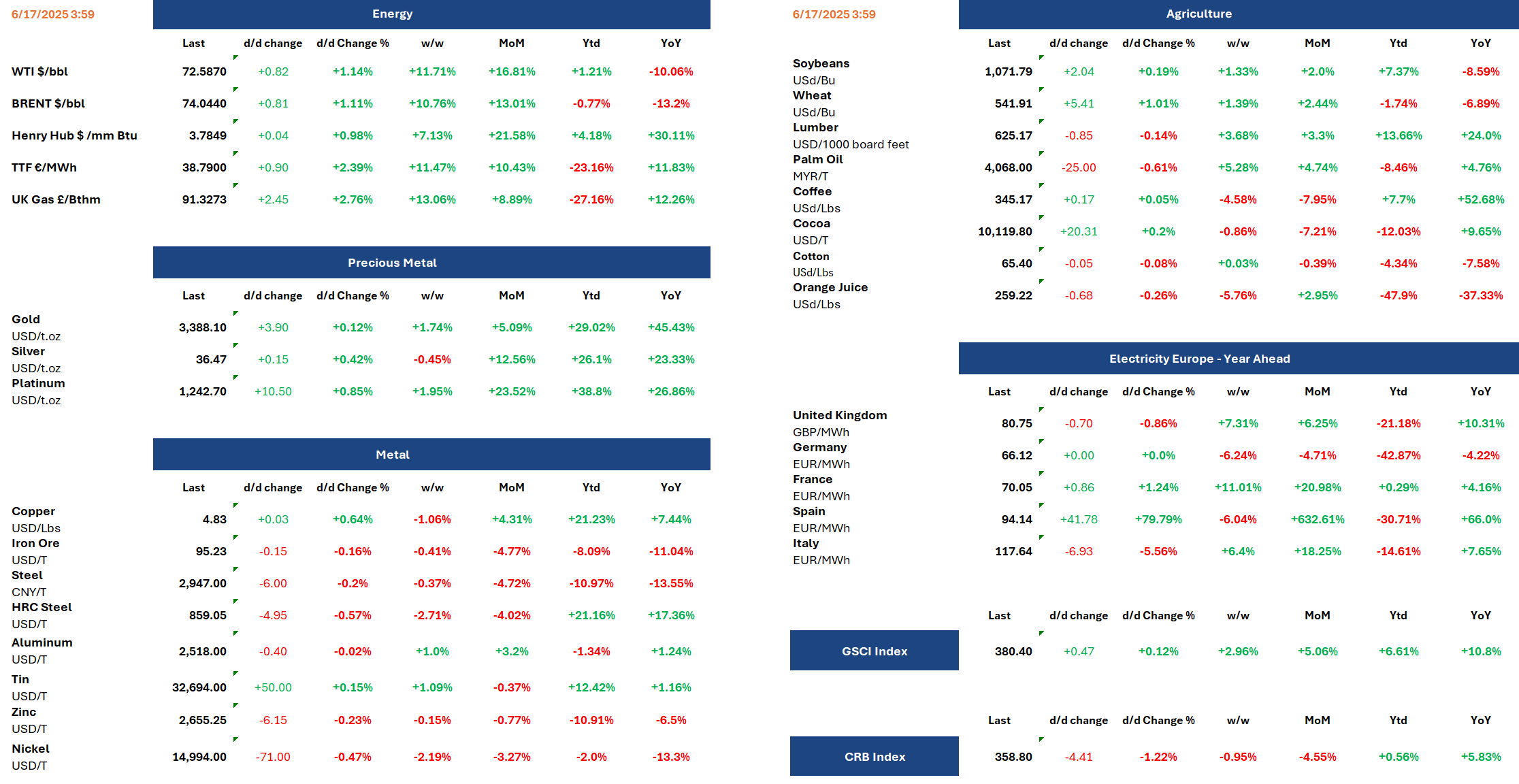

Commodities

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.