With a bare calendar for economic releases focus is on tariffs even if the July 9 deadline has shifted to August 1st. European stocks are taking the renewed tariffs’ threats in stride in hope of better settlement. A deal with the EU is still a long shot especially when digital taxes (or VAT) comes back into the mix. Japanese stocks are also up, the ¥ weaker but bond yields are climbing (10 yr JGB above 1.50% again).

The 50% increase in copper tariffs is clearly more than anticipated, increasing cost for US companies, and creating an increasing gap between exchanges. Large amount of copper was exported to the US ahead of the announcement and it was putting upwards pressure on LME prices. Export will ease post tariff announcement.

More letters will be sent in coming days, and judging from the first 14 letters, the tariffs are no different than the random Liberation Day’s levels. In April, the flawed formula-based Commerce department tariffs shook markets, leading to a quick reversal as Bessent took the lead… Is Lutnick back having the president ear rather than Bessent now as negotiations did not produce the expected deal? Not a positive development.

Regardless of any framework agreement, tariffs remain subject to the US president utterance and market should not be complacent.

The US treasury reiterates that the rebuilding of the TGA towards the $850bn target will be through T-Bills. T-Bill auction size is increased by $25bn per line already and we should expect acceleration in the TGA rebuilding in September adding more pressure on liquidity. Stablecoins are not adding liquidity to the system and the support to the T-bills will come at the expense of other vehicles or other part of the curve. We should see some widening of the T-Bill-OIS spread.

More discussions on a shadow Fed Chair will also contribute to steeper curve. The strategy of front-end loaded issuance and forced rate cuts exposes the US treasury to higher inflation surprise. Higher inflation is more likely now with the flawed Lutnick like tariffs approach rather than fact based negotiated tariffs market wanted to expect, and the overly high “section 232” based tariffs (as shown with copper). Inflation surprise will be preventing Powell from easing first and to higher inflation premia in the longe end when his replacement is announced… also expected in September.

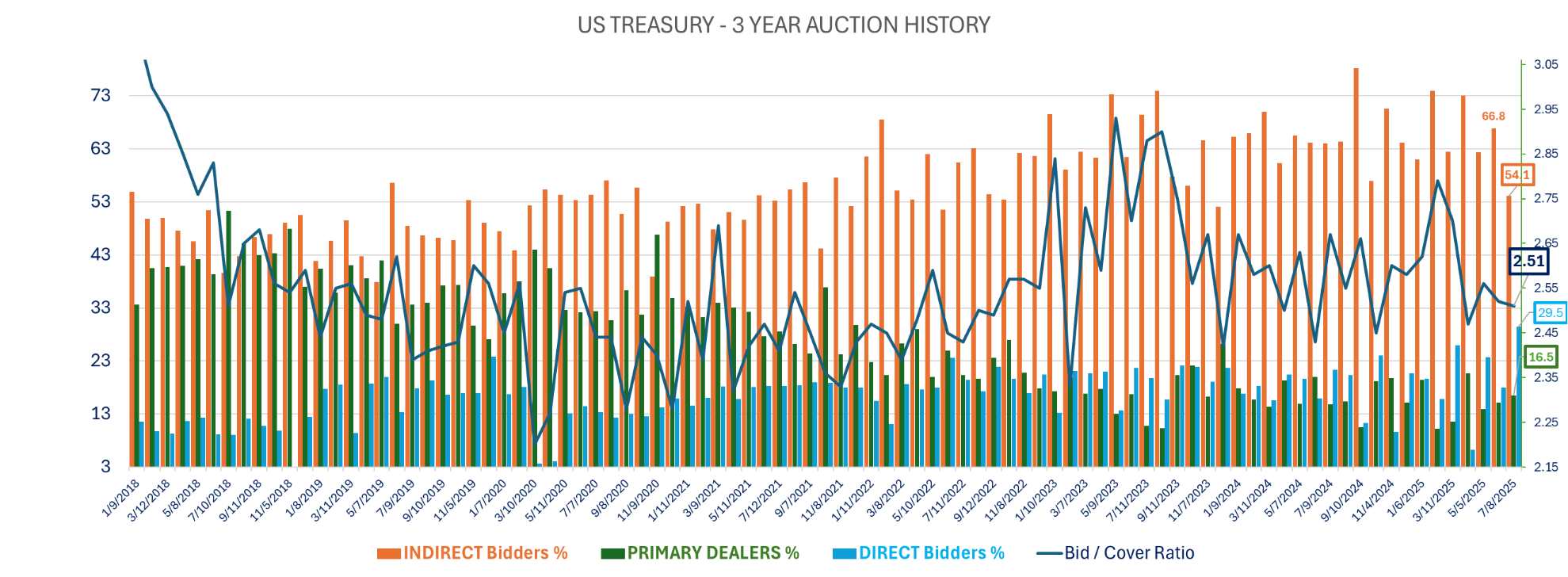

Yesterday US 3-year note auction was rather weak with a small tail but lower demand (bid cover at 2.51, lowest since April 2024), higher dealers’ share (16.5% vs 15.5% average and highest since April) while indirect bid fell to 54.1% weakest since December 2023 (66.5 average over the last 12 auctions).

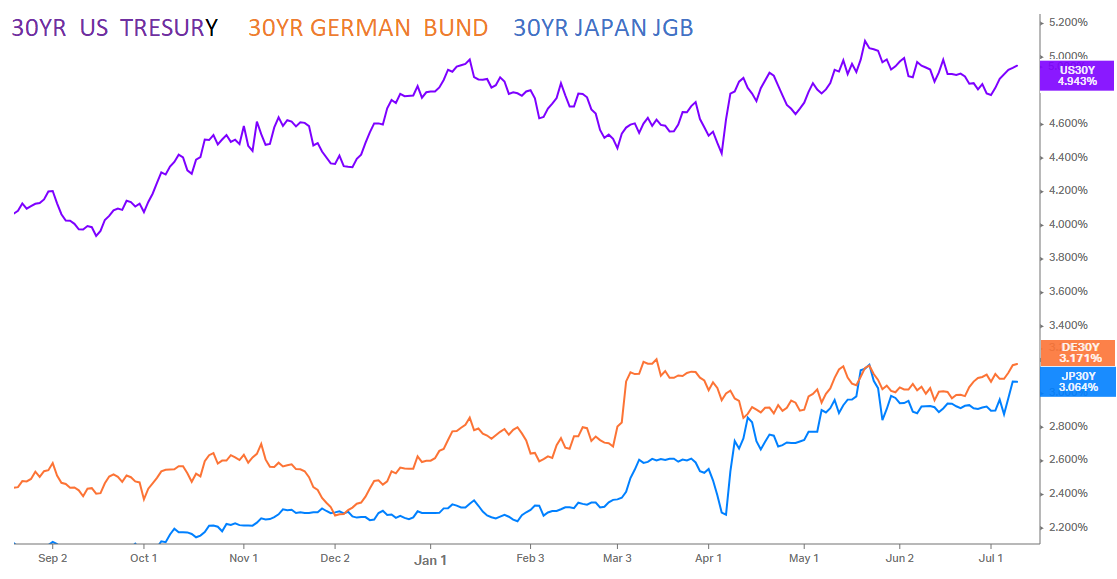

30yr bond yields are only marginally lower after the recent increase ahead of the $39bn 10yr (9yr &10 months) today and $22bn 30 yr (29yr & 10 months) tomorrow. We continue to expect steeper curves. The dollar bounce – flagged due to one-sided bets and Eurozone push back - should also be short lived.

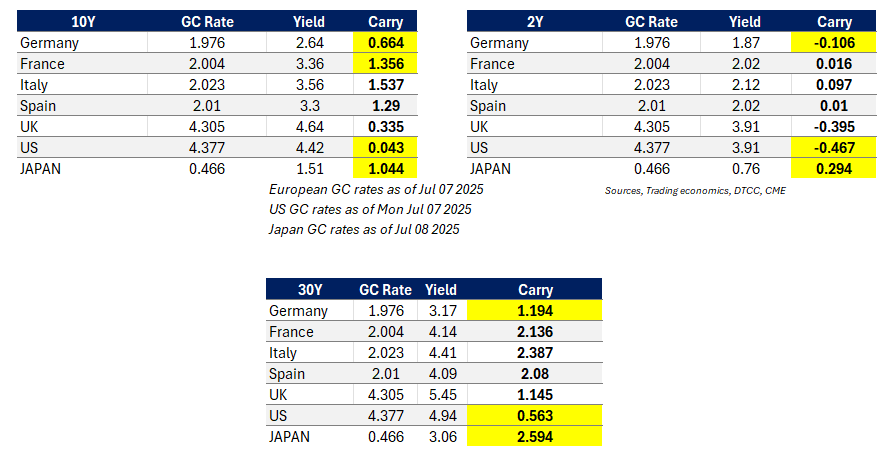

Carry to GC is back to slightly positive for the US 10yr (4bp) but far lower than peers with 104bp for JGB and 66bp for Germany. The US and UK 2yr prices rate cuts. The 30yr JGB carry back to the highest at 259bp vs 56bp for the US! Low incentives to move into US bonds.

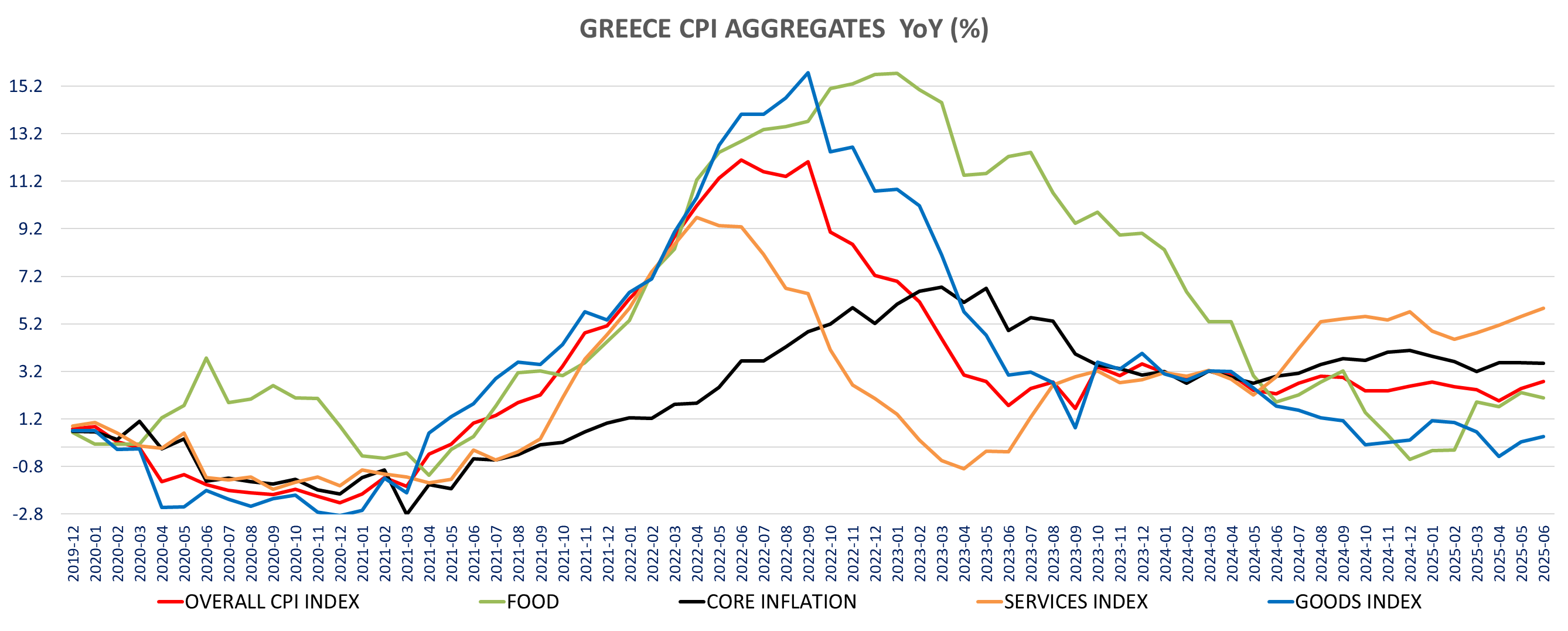

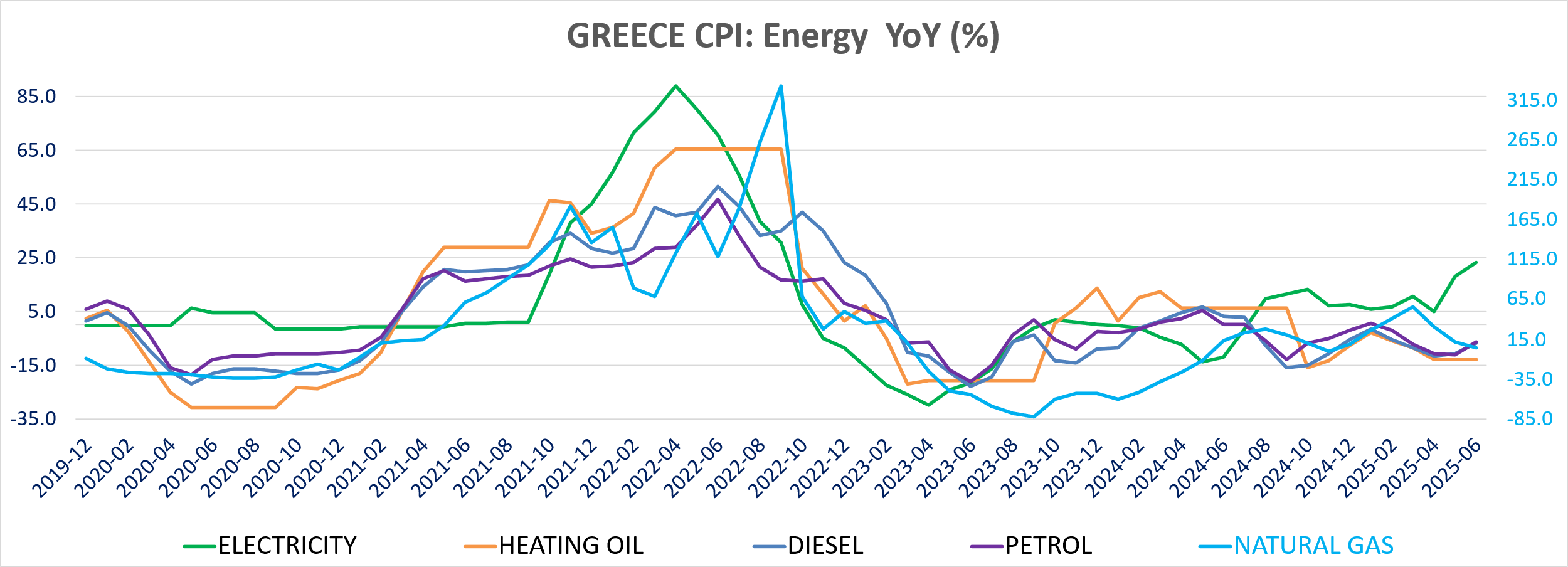

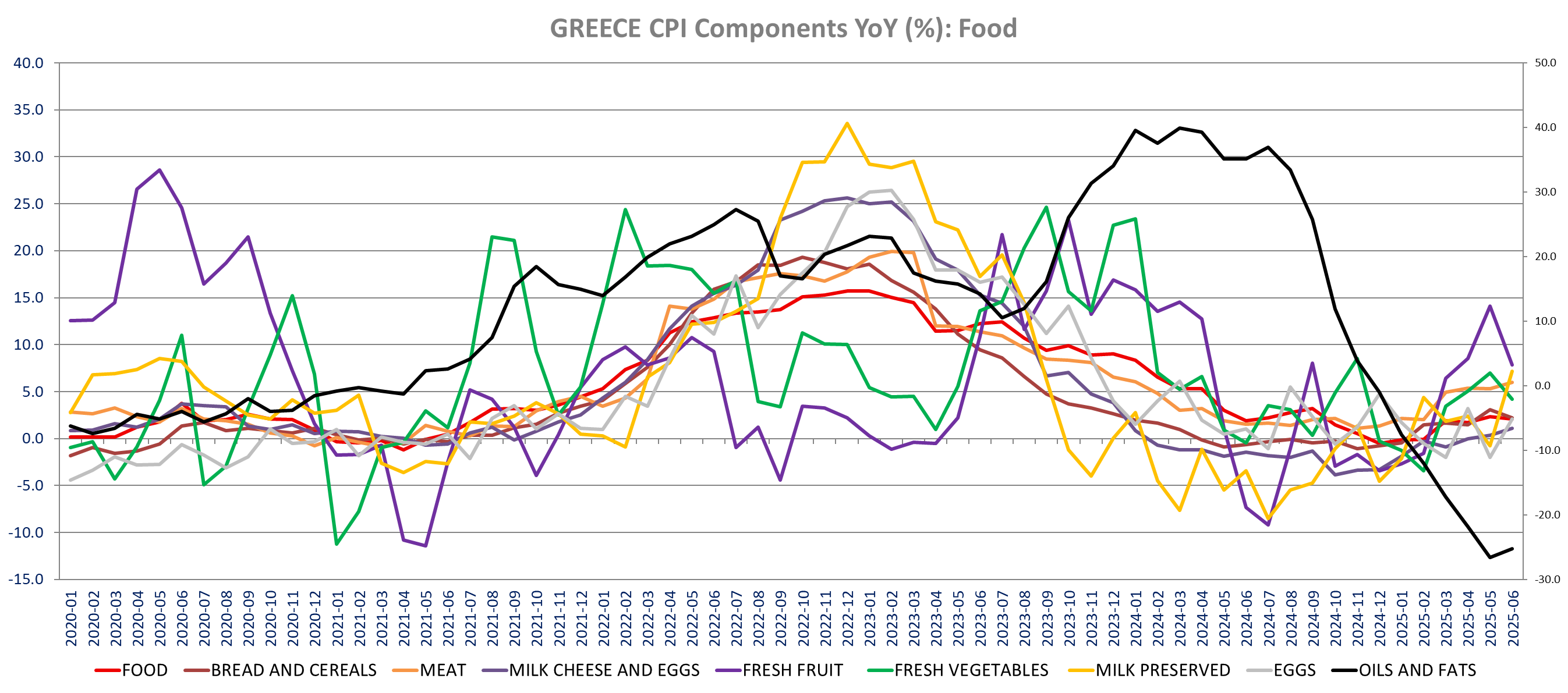

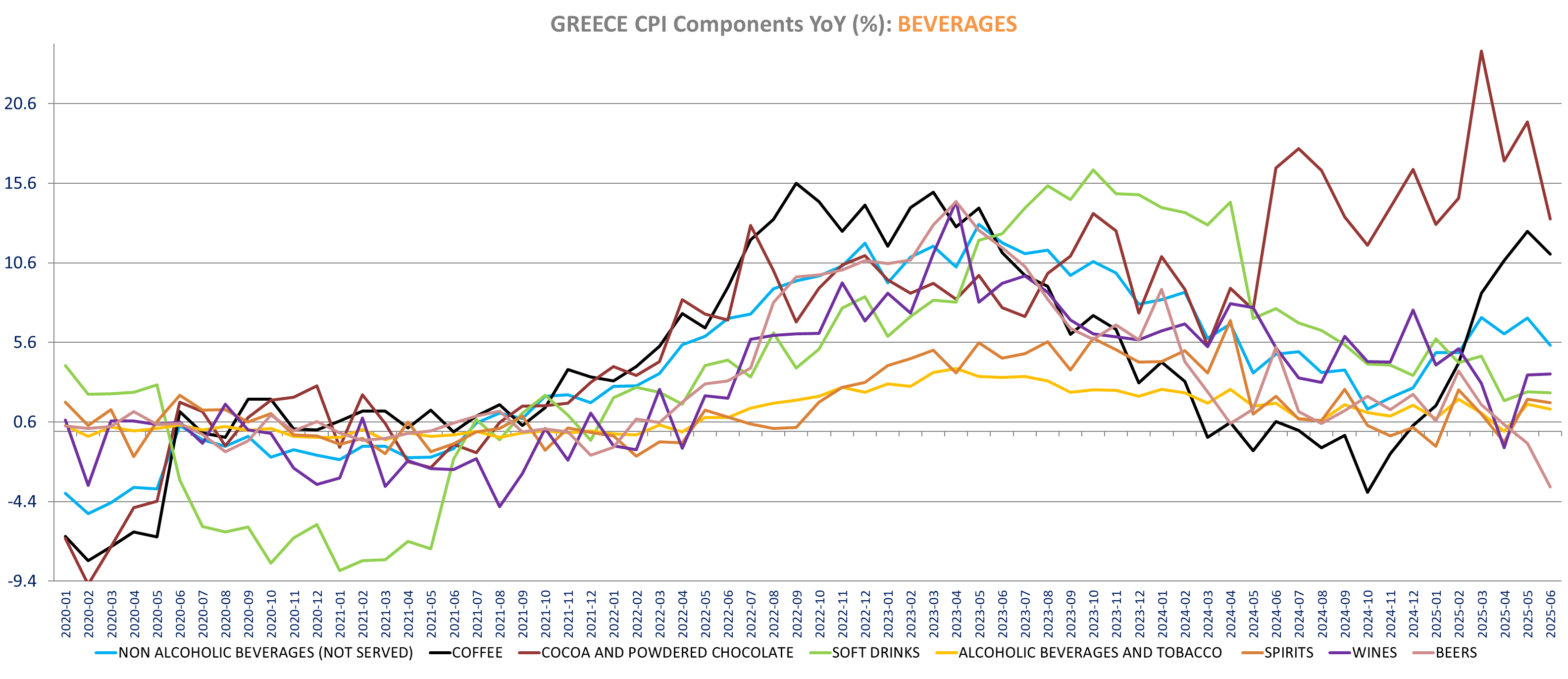

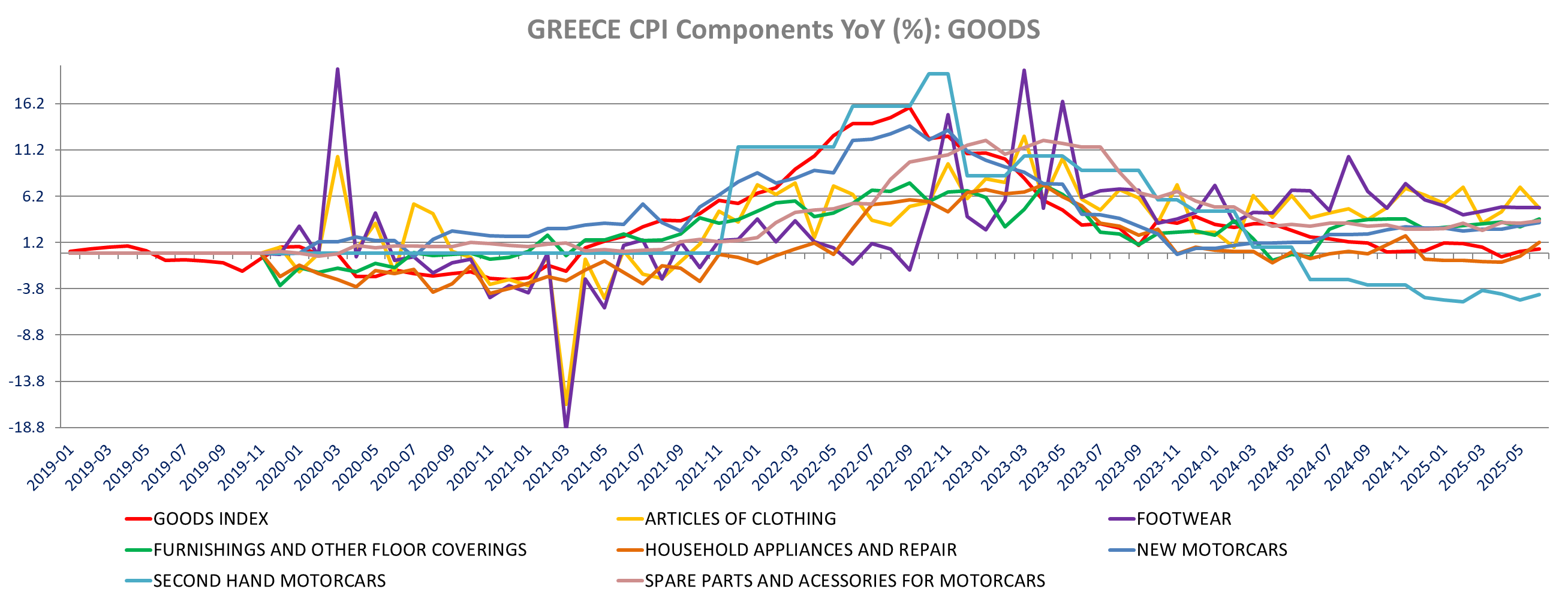

The only economic data on the Eurozone side this morning is the June Greek inflation which came slightly above expectations. The June CPI is up 0.8% m/m to 2.8% yoy (2.5% in May) versus 2.7% expected. The HICP increased 1.2% m/m to 3.6% yoy up from 3.3% yoy in May. The core CPI is marginally lower at 3.5 (3.53%) down from 3.6% (3.56%) in May. Energy inflation increased to 6.9% yoy from 4.8% in May (2% m/m) on higher electricity and liquid fuel inflation.

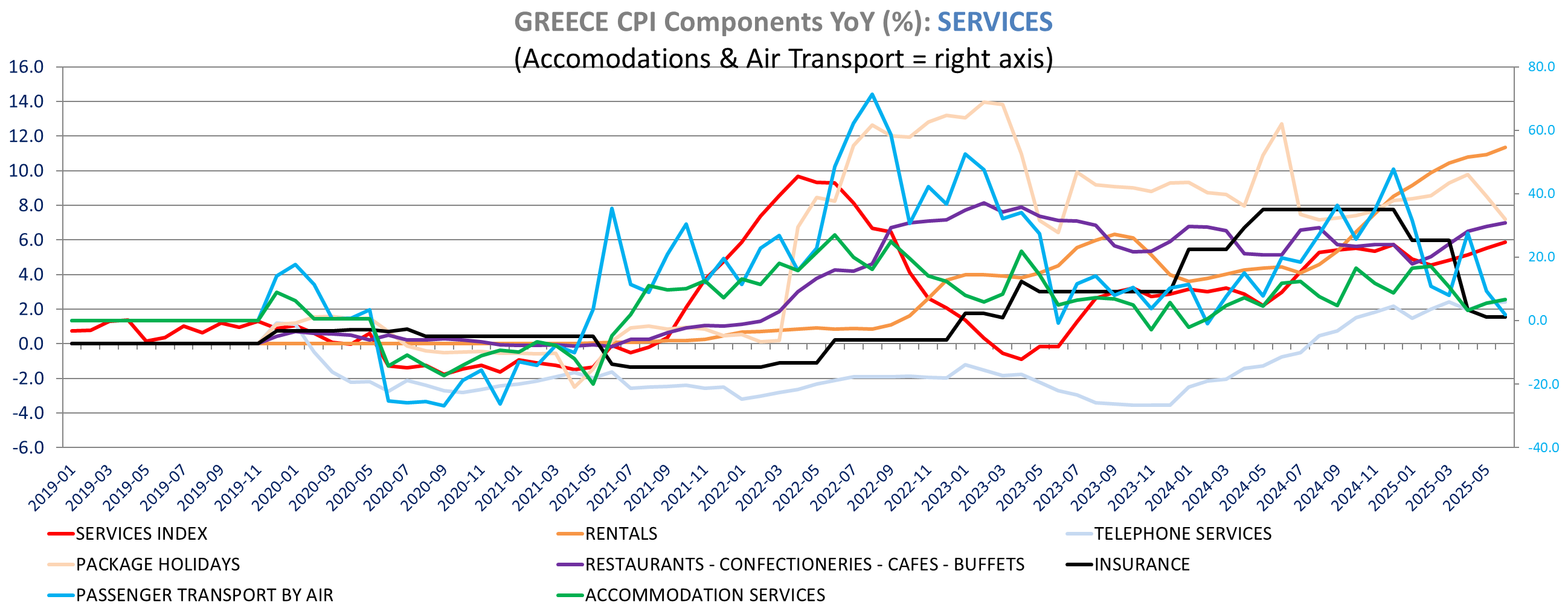

Services’ inflation increased to 5.9% yoy from 5.5%, up 1.1% m/m amid higher inflation for rentals, accommodation, restaurants, health services and social protection. Air transport and package holidays inflation is down in June. At the core inflation level, the increase in services was compensated by lower inflation for processed food, non-alcoholic beverages (5.4% yoy vs. 7.1% yoy, -0.6% m/m) and alcoholic beverages (1.35% vs 2%), and some other goods such as clothing (4.9 vs 7.1%).

On the companies’ front: WPP lowered it FY guidance of LFL revenue less pass-through costs growth to -3% to -5% (from flat to -2%) with a year-on-year decline in headline operating profit margin of 50 to 175 bps (vs. around flat previously). Chief Executive Mark Read said clients had become more cautious, both about the economy and their own prospects. The defense group Kongsberg Q2 sales were slightly below expectations while the operating profit was above. Growth was primarily driven by increased deliveries of missiles and air defense systems from the defense segment, solutions for the newbuild market in the maritime sector, as well as high activity related to deliveries of underwater technology. Crédit Agricole Assurances announces successful sale of its whole stake in FDJ United. Sale of about 3.3% of share capital of FDJ United, for €30 per share. Despite the German government opposition, UniCredit announced that it has converted c.10% of its current synthetic position in Commerzbank, taking its physical share ownership and effective voting rights to around 20%. UniCredit intends to convert the remaining circa 9% synthetic position into physical shares in due course reaching around 29% of Commerzbank voting rights. Meta took a 3% stake in EssilorLuxottica. Last year both EssilorLuxottica and Meta confirmed they discussed a potential investment by Meta in the company, after the Wall Street Journal reported the U.S. group was in talks to buy a 5% stake. In line with its optimization strategy, St Gobain has signed a definitive agreement with the German group Köster for the sale of Brüggemann, a specialist in the production and installation of prefabricated solutions. More details on equities here

The EU will probably not avoid the letter much longer...

Lower demand (bid cover at 2.51, lowest since April 2024), higher dealers’ share (16.5% vs 15.5% average and highest since April) while indirect bid fell to 54.1% weakest since December 2023 (66.5 average over the last 12 auctions) …

Carry to GC is back to slightly positive for the US 10yr (4bp) but far lower than peers with 104bp for JGB and 66bp for Germany. The US and UK 2yr prices rate cuts. The 30yr JGB carry back to the highest at 259bp vs 56bp for the US! Low incentives to move into US bonds.

GREECE INFLATION (June)

The June Greek inflation is up slightly more than expected, with the CPI up 0.8% m/m to 2.8% yoy (2.5% in May) above expectations of 2.7%. The HICP increased 1.2% m/m to 3.6% yoy up from 3.3% yoy in May. The core CPI is marginally lower at 3.5 (3.53%) down from 3.6% (3.56%) in May.

Energy inflation increased to 6.9% yoy from 4.8% in May (2% m/m) on higher electricity and liquid fuel inflation.

Services’ inflation increased to 5.9% yoy from 5.5%, up 1.1% m/m amid higher inflation for rentals, accommodation, restaurants, health services and social protection. Air transport and package holidays inflation is down in June.

At the core inflation level, the increase in services was compensated by lower inflation for processed food, non-alcoholic beverages (5.4% yoy vs. 7.1% yoy, -0.6% m/m) and alcoholic beverages (1.35% vs 2%), and some other goods such as clothing (4.9 vs 7.1%).

Energy inflation increased to 6.9% from 4.8% with electricity prices up 23.1% yoy in June (18% in May), increasing 3.6% m/m and liquid fuel & lubricants inflation increased to -5.95% toy from -10.2% yoy in May. Diesel prices are down -6.9% yoy in June versus -10.9% yoy in May (+2.6% m/m) and gasoline prices inflation is up to -6.6% yoy from -11% (+1.55% m/m). gas inflation eases to 3.9% from9.6% (-0.1% m/m and high comparison from 2024, +5.4% m/m).

Food inflation declined to 2.1% from 2.3% yoy in May dragged down by lower fresh fruit inflation (7.9% yoy vs +14.1% yoy, up 11.6% m/m but with high comparison level of +18%m/m in June 2024) and fresh vegetables (4.2% yoy down from 6.95% yoy in May, falling -5.5% m/m in June). As seen in other countries we continue to see higher meat prices (6% yoy up from 5.3%) and in particular higher beef inflation with prices up 15.1% yoy in June increasing from13.7%, (up 1.3 % m/m). Fresh Fish inflation is also up at 9.7% from 8.4%, Milk up to 3.4% vs 3% and eggs inflation to +2.1% from -2% (+3.6% m/m). oil & fats inflation is also less negative (+1.7% m/m). Cheese, Bread & cereals inflation eased in June.

Greece, non-alcoholic beverages inflation fell in June to 5.4% yoy from 7.1% yoy in May as cocoa based drinks inflation feel sharply to 13.4% from 19.45% yoy in May (+1.75% m/m but high comparison of 7.2% m/m in June 2024). Coffee prices inflation also eased to 11.2% from 12.6% (-0.3% m/m). Soft drinks, mineral water and tea inflation also decreased Fruit Juice inflation also fell significantly (0% vs 4.8% yoy, -3.45% m/m).

For alcoholic beverages, the decline of inflation to 1.35% yoy from 2% is mainly due to lower beer prices inflation (-3.5% yoy vs.-0.75% yoy in May on high comparison from last year). Tobacco inflation is stable at 1.35% yoy.

Alcoholic beverages inflation is down to -0.6% yoy vs 1.1% in May.

Goods inflation increased to 0.5% yoy from 0.2% (0.5% m/m). For non-food, non-energy goods we saw a significant decline in clothing inflation (4.9% vs 7.1%), lower inflation for medical products (2.1% vs 3.3%), but most of the other aggregates are posting higher inflation. Inflation increased for furniture, appliances, tools, pharmaceutical products, autos and car parts. New car inflation rose to 3.3% yoy from 3%, Used cars inflation to -4.45% from -5%.

Services’ inflation picked up in June to 5.9% from 5.5% with prices up 1.1% m/m. Comparison level will be much higher in July (1.4% m/m in July 2024). The increase in services inflation is relatively broad-based and is noticeably higher for rent (11.4% vs 10.9%yoy, 0.9% m/m), accommodation (6.7% yoy vs 5.5% yoy, up 9.75% m/m), restaurants (7% vs 6.8%), Social protection services (7.7% vs 6.8%), domestic services (5.1% vs 4.7%), dental services (1.8% vs 1.3%), paramedical services (2.5% vs 2%), sporting & leisure services (4.6% vs 4.4%)… On the other hand, we see lower inflation for more volatile items: package holiday (7.2% vs 8.5%), air transport (1.9% vs 9.3%), specifically for international flights (-4.3% vs 9.7% on high comps pf +23.6% m/m in June 2024). Domestic flight inflation is higher than in May (9.4% vs 7.5%). Cultural services inflation is also lower at 6.1% vs 7.1% yoy.

Detailed table

|

|

Wednesday, July 9, 2025 | ||

|

EL | |||

|

0 |

253.10 |

+5.72% | |

|

EL |

Meta took a 3% stake in EssilorLuxottica. Last year both EssilorLuxottica and Meta confirmed they discussed a potential investment by Meta in the company, after the Wall Street Journal reported the U.S. group was in talks to buy a 5% stake. | ||

|

|

|

|

|

|

UCG | |||

|

EUR |

60.32 |

+3.22% | |

|

UCG |

Having received all necessary legal and regulatory approvals - including ECB, German Antitrust and FED, underscoring the appropriateness of our actions and approach - UniCredit today announces that it has converted c.10% of its current synthetic position in Commerzbank, taking its physical share ownership and effective voting rights to around 20%. | ||

|

|

|

|

|

|

SGO | |||

|

EUR |

100.50 |

+1.97% | |

|

SGO |

Saint-Gobain has signed a definitive agreement with the German group Köster for the sale of Brüggemann, a specialist in the production and installation of prefabricated solutions. | ||

|

|

|

|

|

|

FDJU | |||

|

EUR |

30.46 |

-3.97% | |

|

FDJU |

Crédit Agricole Assurances announces successful sale of its whole stake in FDJ United. Sale of about 3.3% of share capital of FDJ United, for €30 per share. | ||

|

|

|

|

|

|

KOG | |||

|

NOK |

328.05 |

-11.15% | |

|

KOG |

Q2 Revenue rose by 19.9% percent to NOK 13,899 million (Consensus 13,969). "Operations during the second quarter were stable. All business areas increased their operating income compared to Q2 2024. Growth was primarily driven by increased deliveries of missiles and air defense systems from the defense segment, solutions for the newbuild market in the maritime sector, as well as high activity related to deliveries of underwater technology," commented CEO Geir Håøy. Order intake in Q2 was MNOK 18,184, compared to MNOK 17,278 in the same quarter last year. Book to Bill in the Defense division stood at 1.6 and 1.18 in the Maritime division.

| ||

|

|

|

|

|

|

WPP | |||

|

GBp |

443.70 |

-15.90% | |

|

WPP |

WPP is updating the market today on H1 trading and the FY 2025 outlook. | ||

Versus early hours

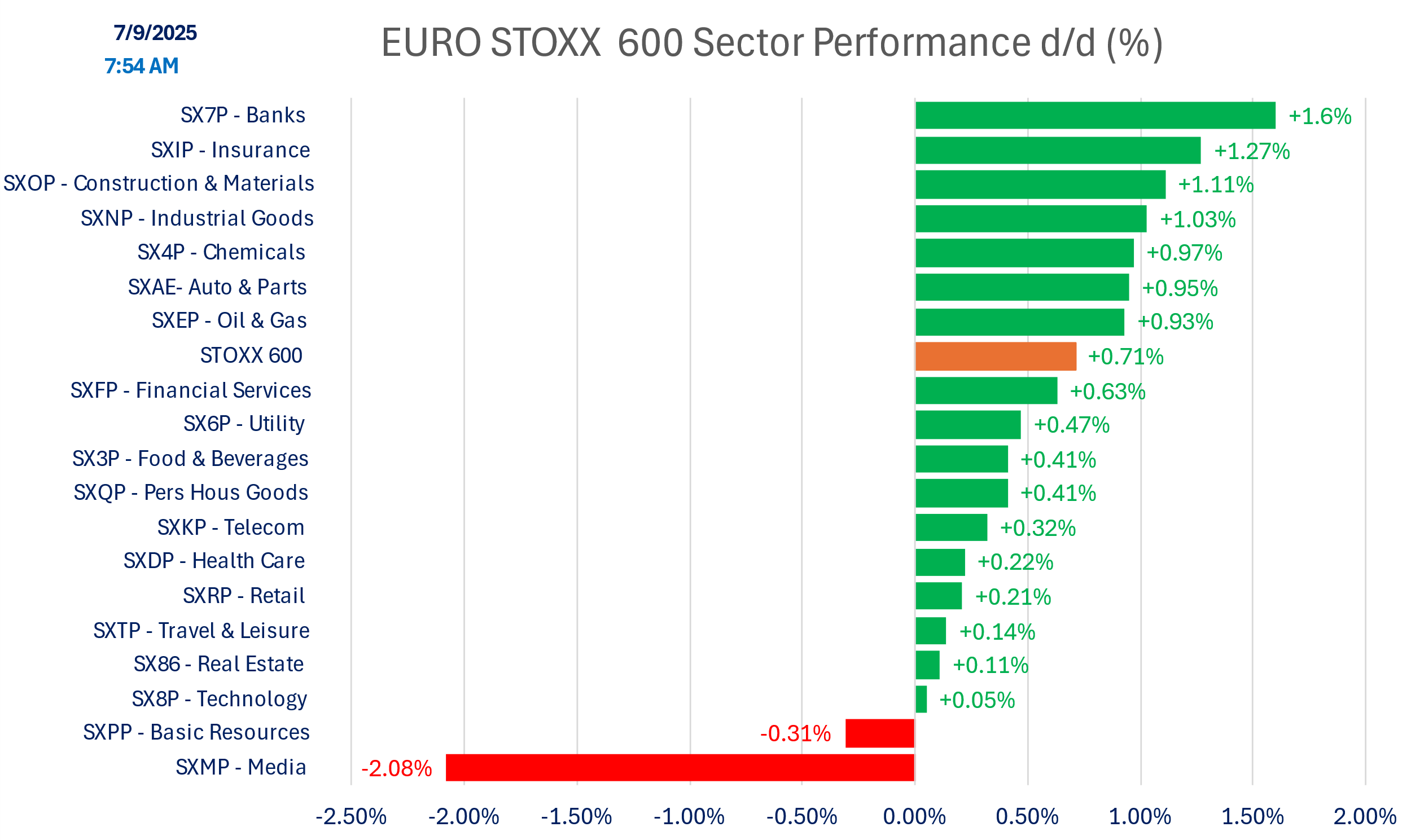

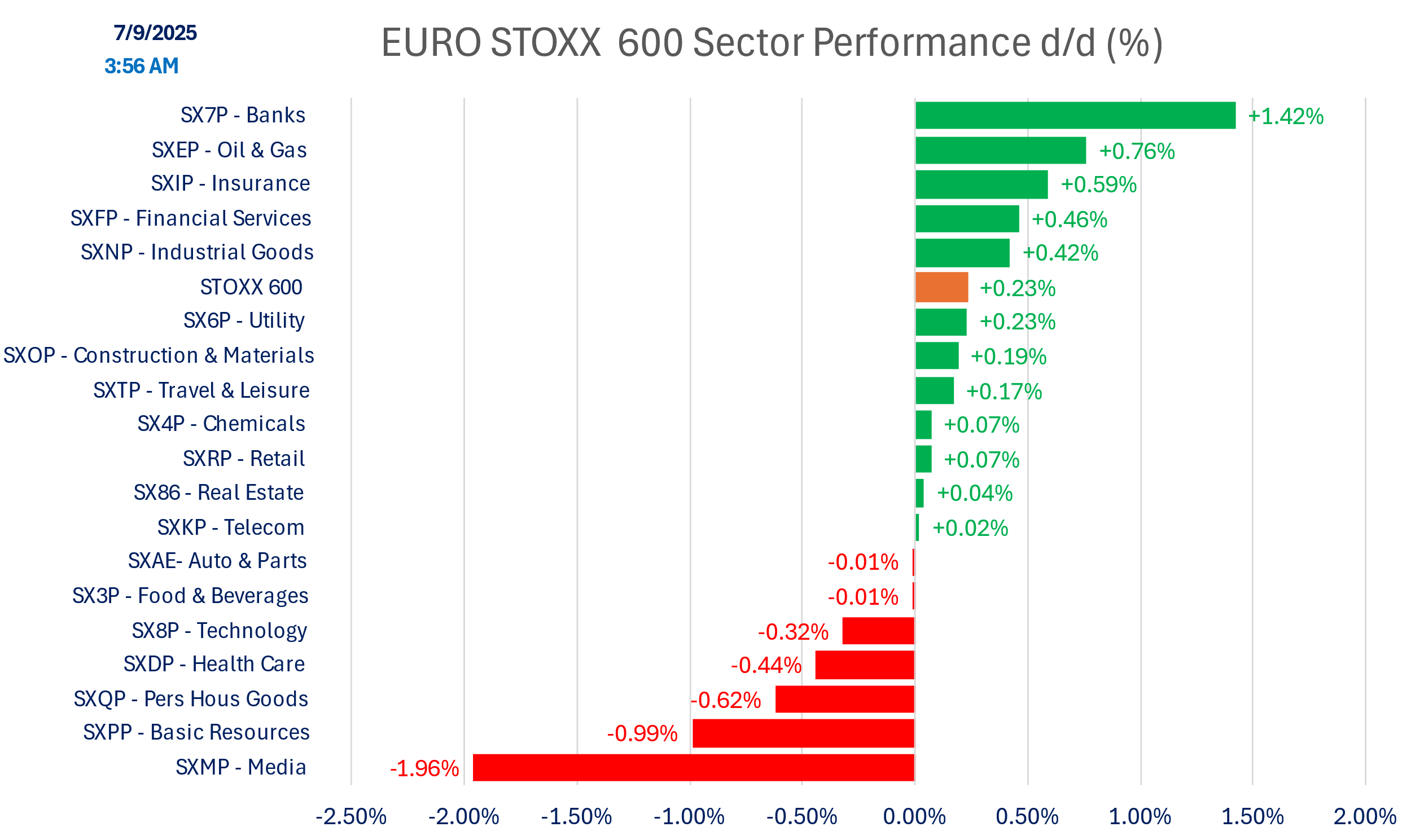

SECTOR PERFORMANCE

Today’s Performance

Versus early hours:

Indices

Versus early hours

Commodities

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.