Markets now fully price the Fed to cut by 25bp next week, with some 10% probability of a 50bp decline. The carry to GC shows the 2 years now at -93bp negative carry versus flat carry for Germany or France and +36bp for Japanese JGB. No action is expected from the ECB this Thursday. The 10yr US note has a -35bp negative carry when Germany is at +70bp and Japan at +110bp. Japanese data were more on the positive side, but we have now higher political uncertainty, but the BoJ hike is expected before year end. Political concerns pushed the ¥ down, yield down except for the very long end (30yr + 5.5bp to 3.29%). The carry for the 30yr JGB is now 282bp (only 33bp for the US). The € is higher even as the French Prime Minister is expected to lose the confidence vote. At this point Macron is expected to seek a new Prime Minister, but he will likely be forced into new parliamentary elections. Budget concerns will increase.

European stocks are higher this morning with the gain stable from the early hours, with il & gas gaining with oil prices up post OPEC production increase announcement and ahead of additional sanction on Russia.

Inflation on Thursday is the next data to watch for the Federal reserve rate cut expectations. Liquidity continues to tighten with the TGA up to $669.27bn as of September 4 and the Domestic Reverse Repo still at rock bottom of $20.997 as of today, going into the September tax payments. The latest Daily Treasury Statement shows the US debt at $37.430bn (+$1,214.3bn since July 4).

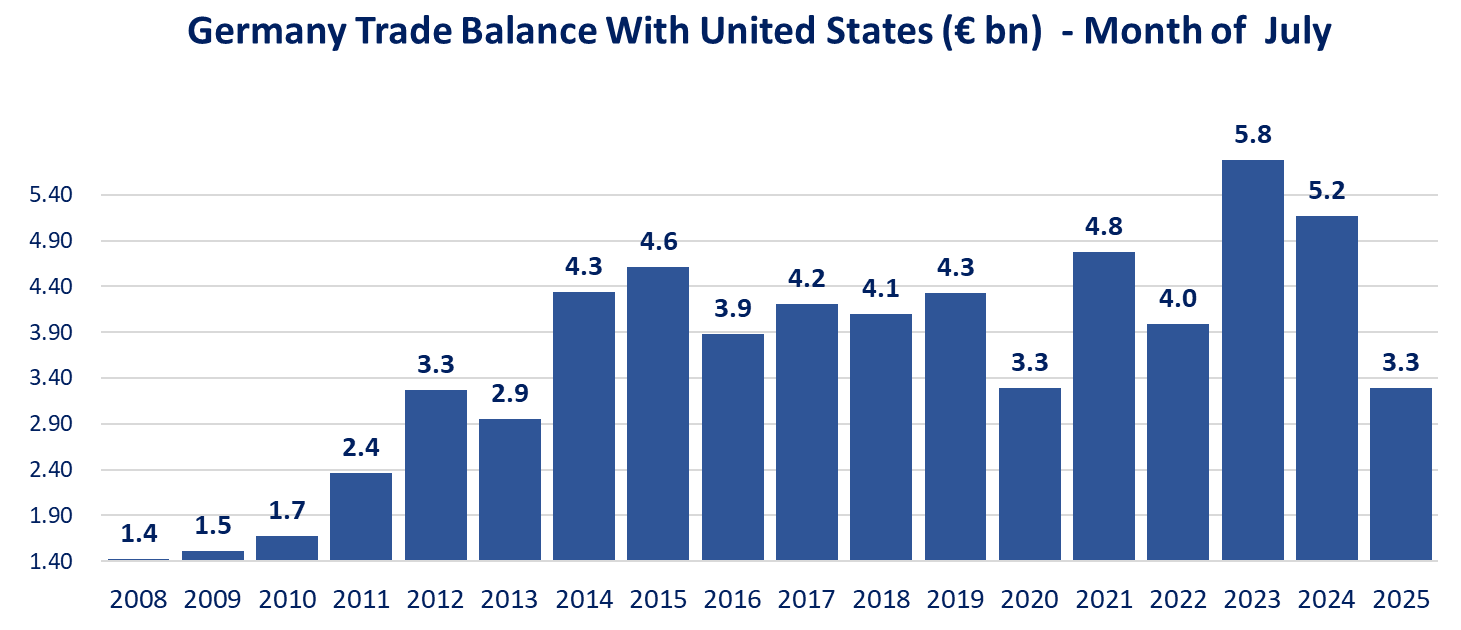

Hassett, Bessent talk Fed independence but both call for changing the Federal Reserve remit. There is little doubt that when push comes to shove, if inflation moves higher, the economy weakens further there will be a clear push for the Fed to cut rates more than the dual mandate commands, favoring growth to inflation containment. Definitely tilted towards more fiscal dominance. Steepening to continue even if tariffs are not judged illegal. The German trade data below shows a weakening in trading with the US in July already... Steepening to continue even if tariffs are not judged illegal. The German trade data below shows a weakening in trading with the US in July already.

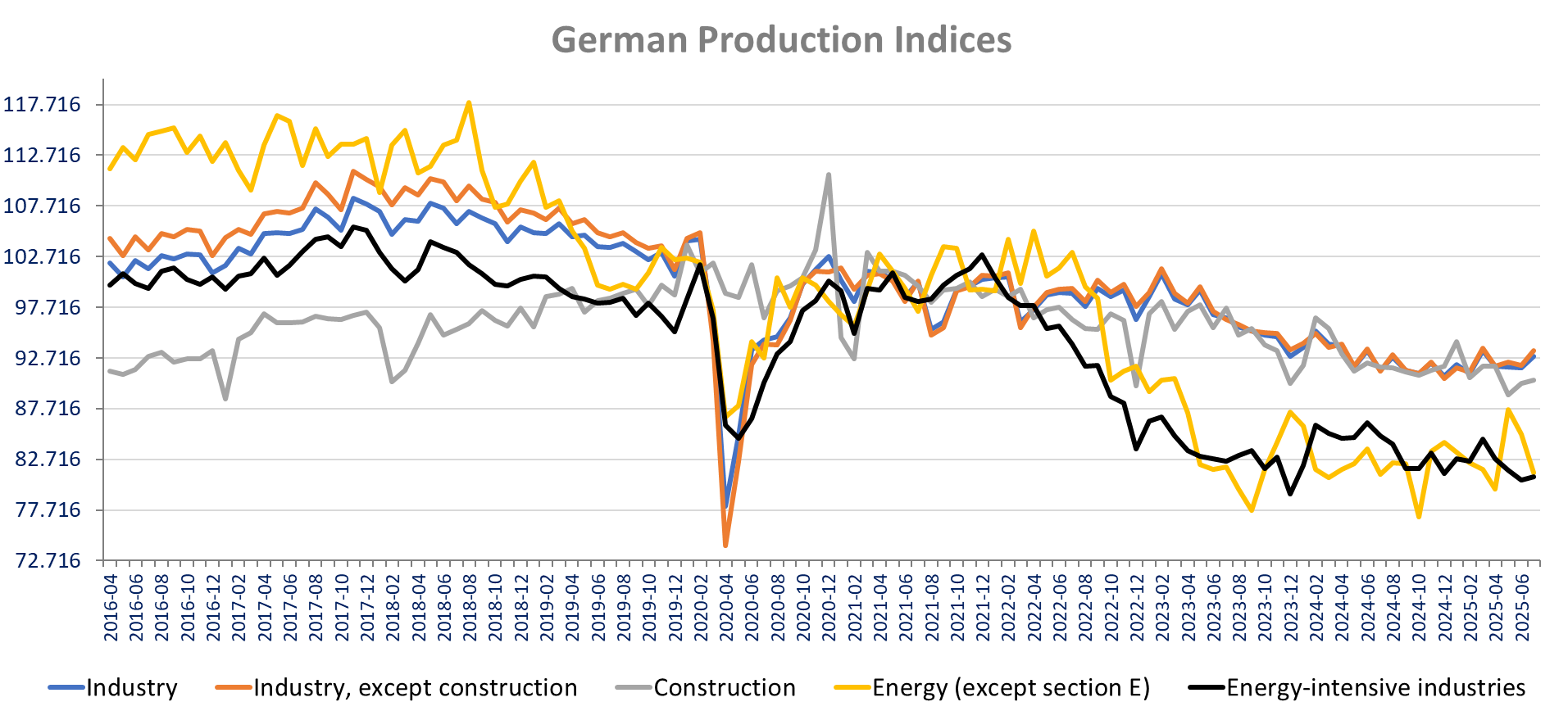

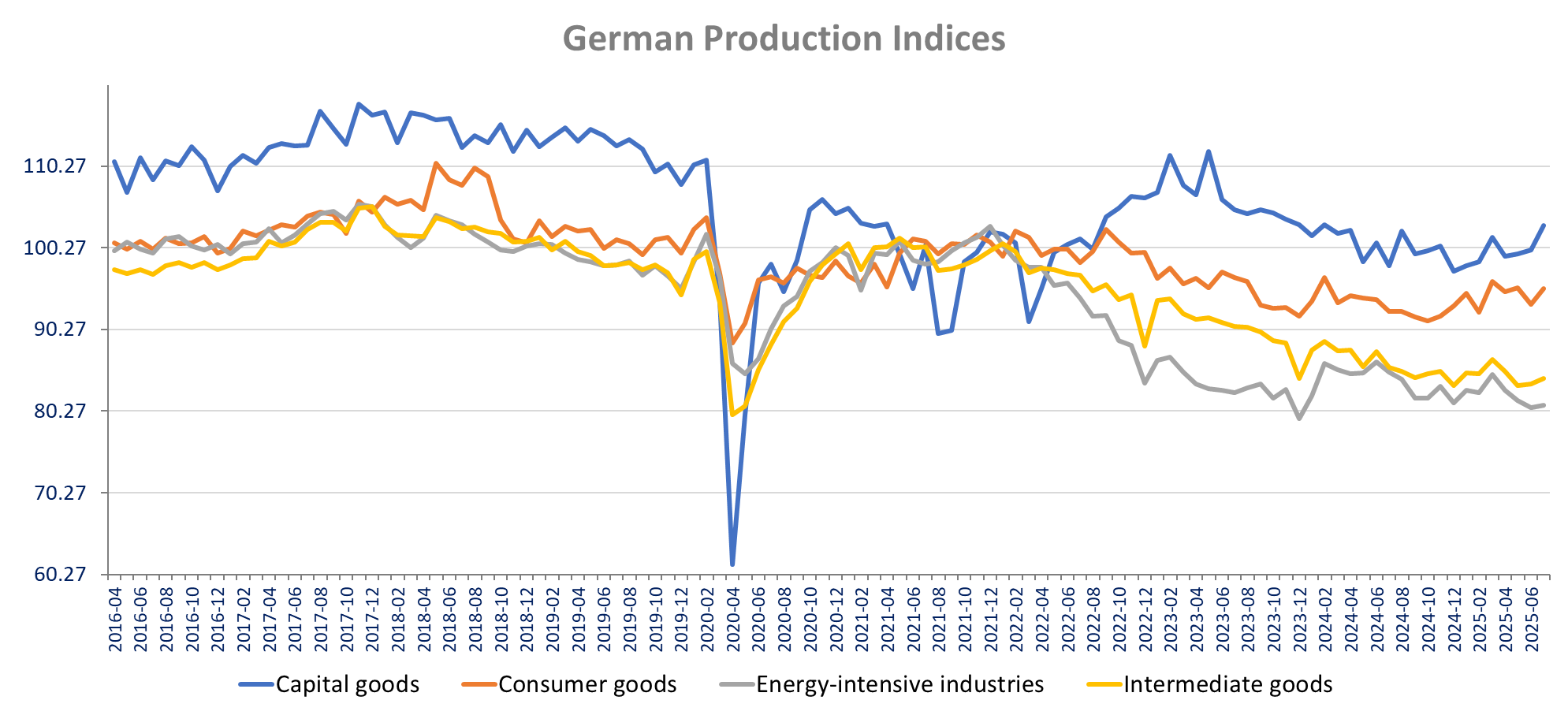

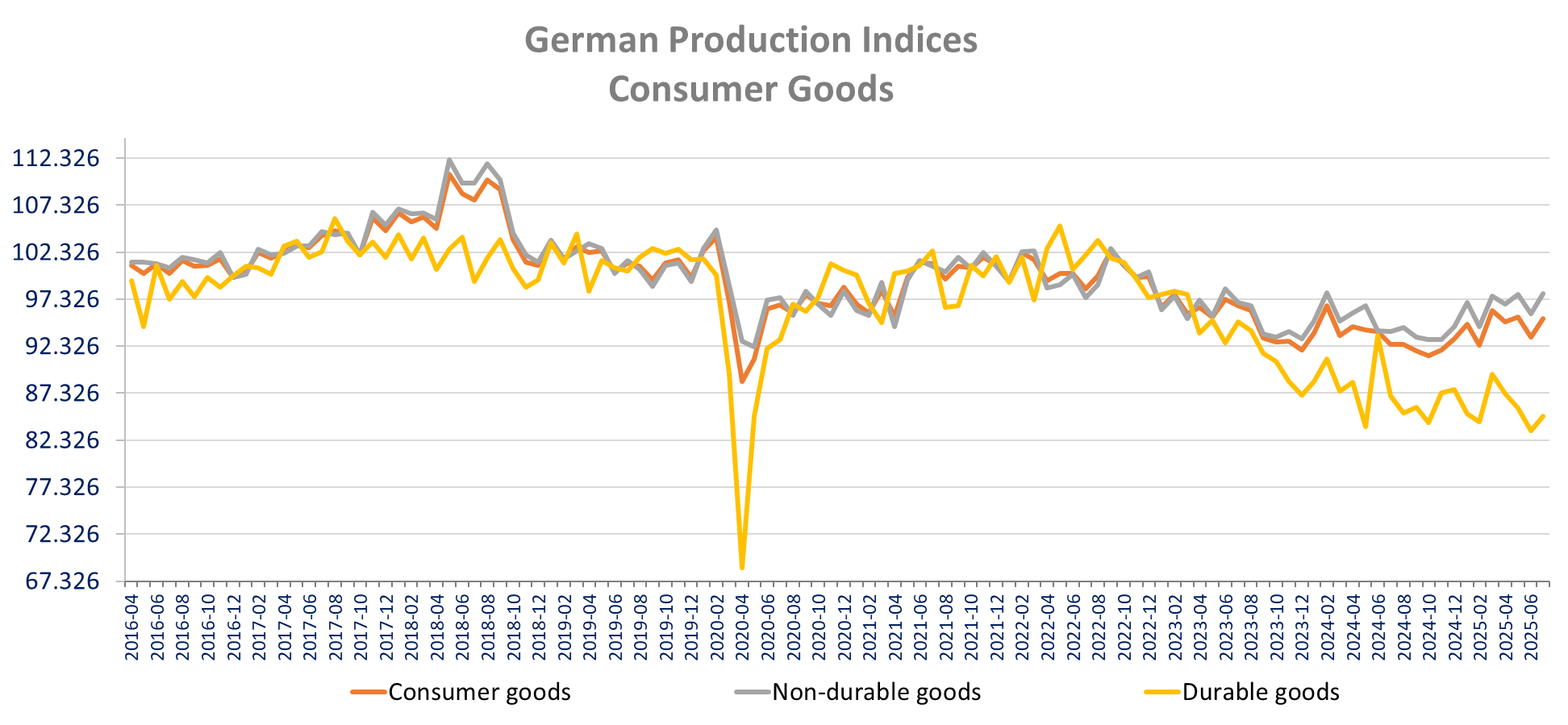

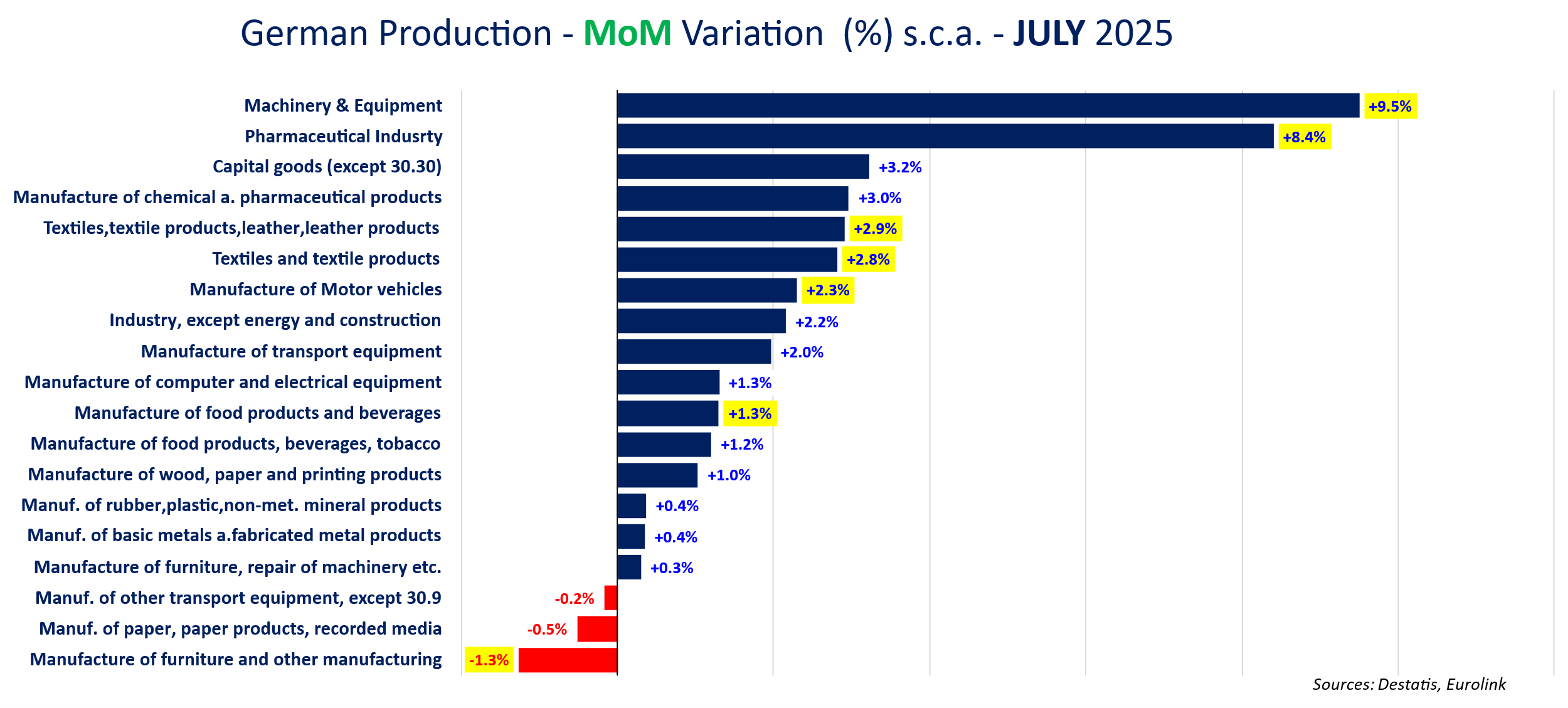

German July industrial production rose more than expected in July, up 1.3% m/m rather than 1% expected, on top of a significant revision upwards for June. As we saw we the German orders last week, there are significant revisions in June, with production now down only -0.1% m/m rather than -1.9% reported initially. When excluding both energy and construction production is up 2.2% m/m after -0.1% m/m in June revised from -2.8% m/m. On a year-on-year basis production is down +1.5% yoy versus -1.8% yoy in June (revised up from -3.6% yoy! Capital goods production increased the most month-over-month, up 3% m/m (after +0.5% m/m in June revised from -3.2%). Non-durable goods production is up 2.2% m/m after -2% m/m in June with a sharp revision from -6.2% m/m! In terms of manufacturing sectors, machinery & equipment production surged +9.5% m/m, pharmaceuticals production increased 8.4% m/m, textiles +2.8% m/m, Motor vehicles +2.3% m/m, Food & beverages +1.3%. On the negative side production declined for furniture (-1.3%), paper product (-0.5%) and other transport equipment (-0.2% m/m).

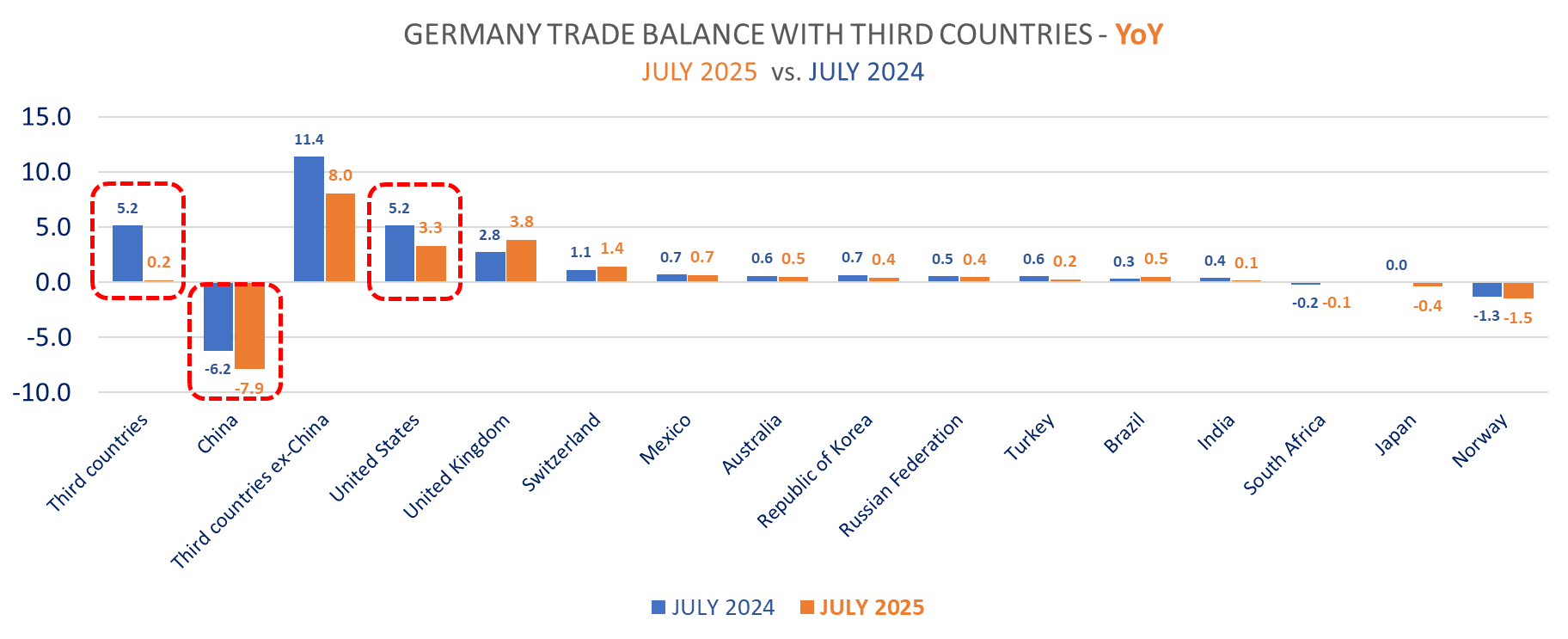

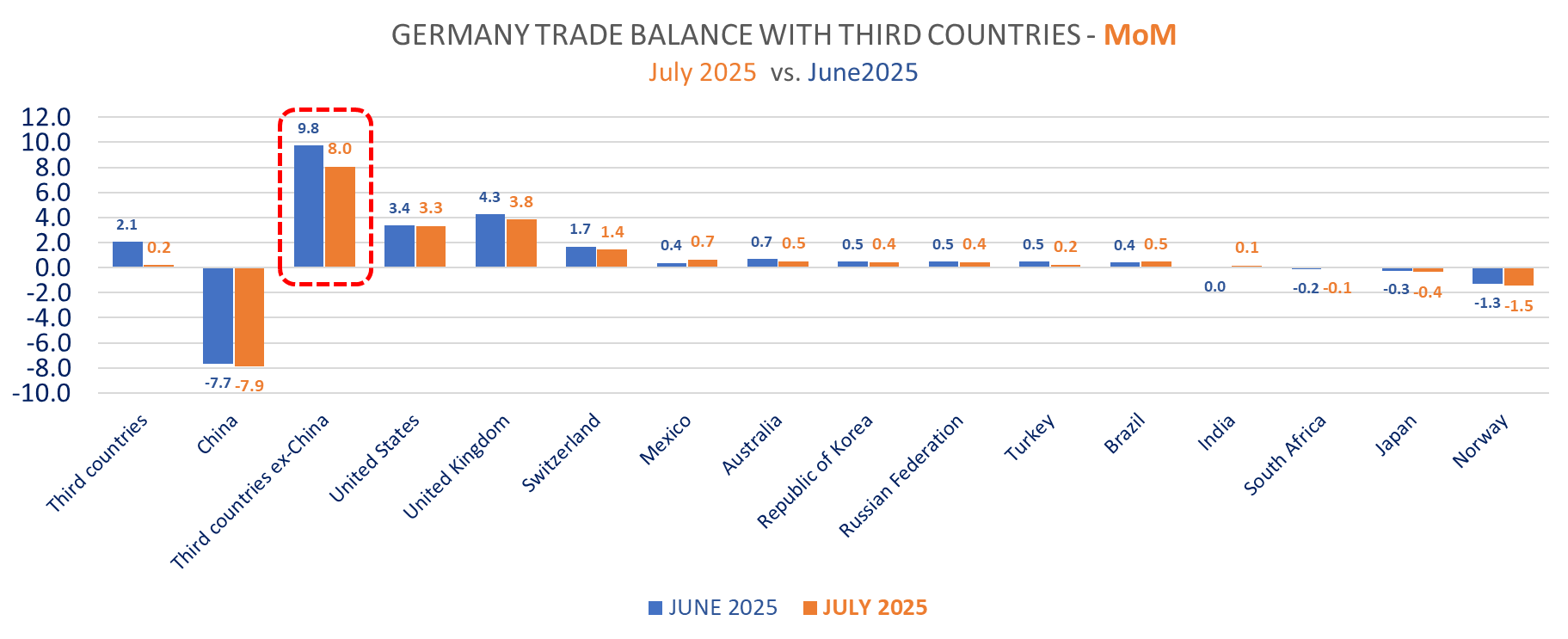

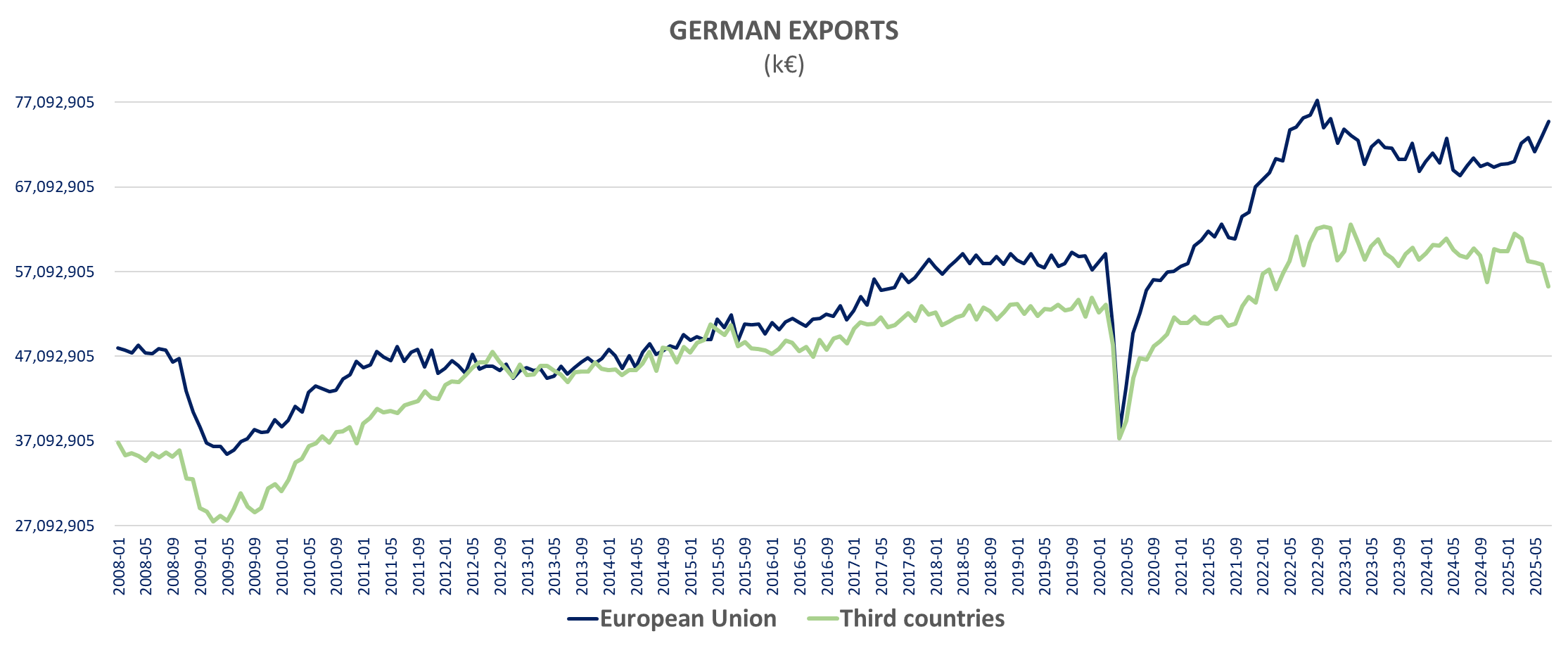

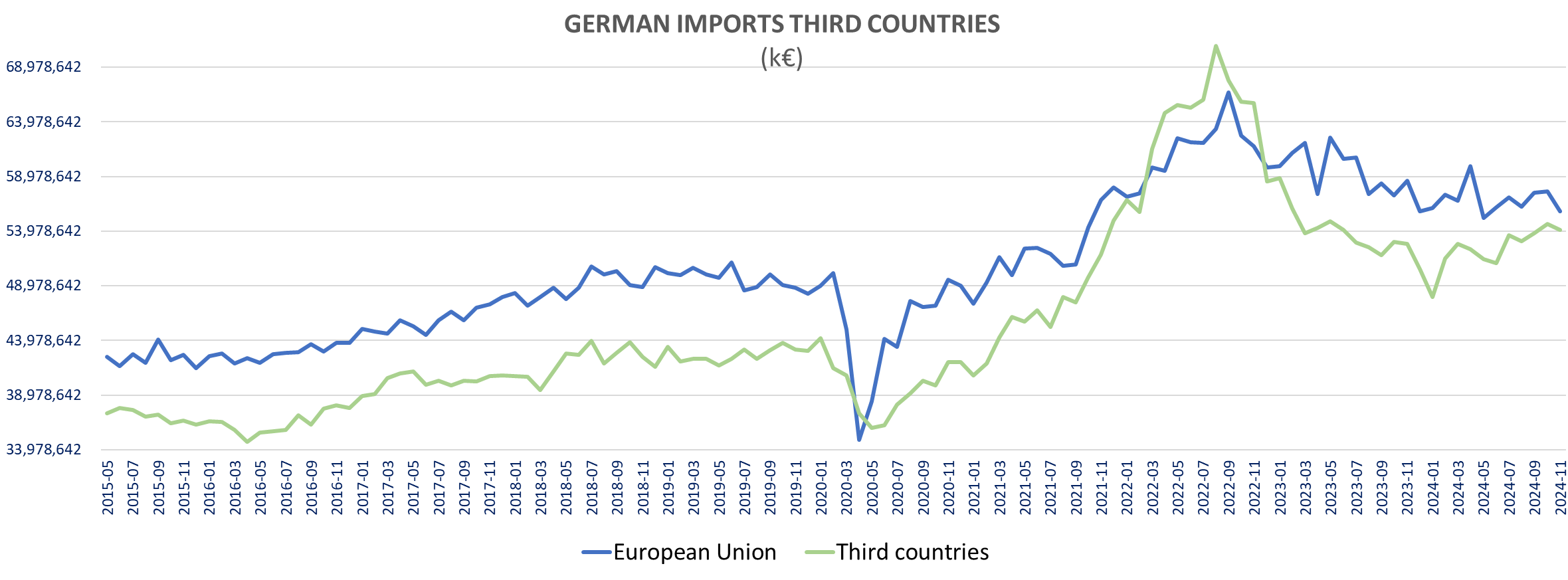

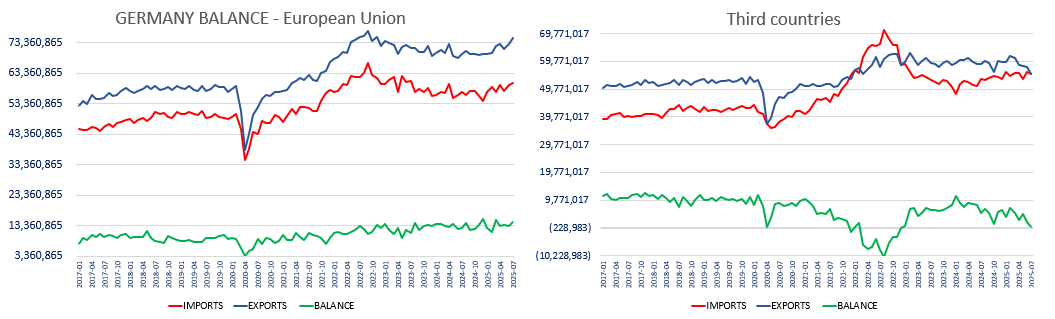

Interesting German trade balance data for July, showing significant decline in trading with third countries (ex-EU) with exports down -4.5% m/m (-5.9% yoy) and imports down -1.3% m/m (+2.8% yoy vs +6.2% in June), compensated by higher intra EU trading.

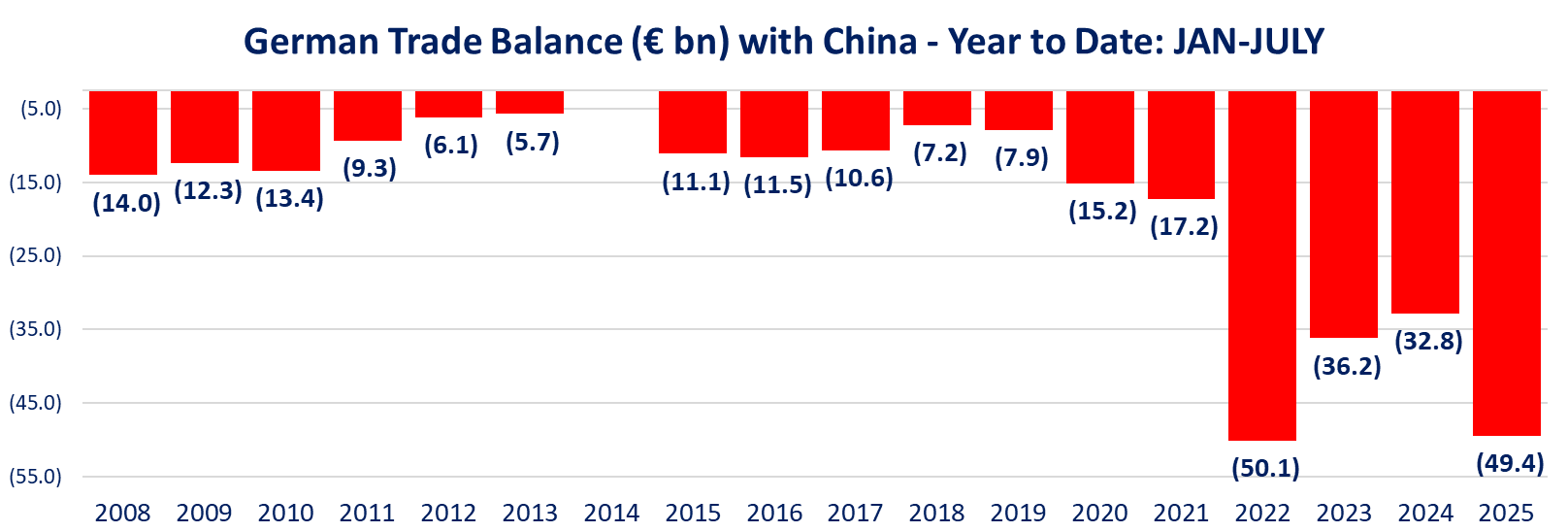

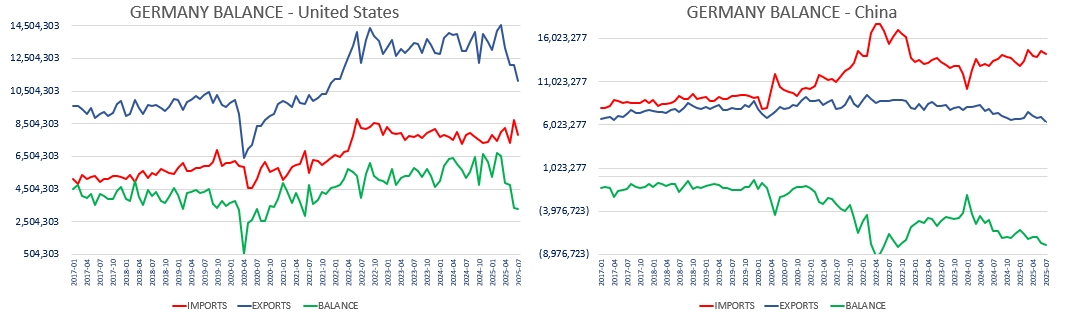

We see a sharp decrease in the surplus with non-EU country to just +€0.2bn in July (-96.2% yoy!) but a surge to a new record for July in the surplus with EU countries. The German trade surplus for July came at €14.7bn out of which €14.5bn with the EU (+16.1% yoy) and €12.2bn (+21.7% yoy) with the Eurozone. Trade with the US declined with German exports to the US down -7.9% m/m (+14.1% yoy) and imports down -10% m/m (and only up 0.6% yoy now). The surplus with the US is down to just +3.3bn in July, weakest July since 2020. The deficit with China reached a record for July at -7.85bn with imports down -2.4% m/m (+6% yoy ) and exports -7.3% m/m (-11.5% yoy), also showing a decline in trading.

ASML Holding will become Mistral AI’s largest shareholder by leading a €1.7bn Series C with ~€1.3bn invested, valuing the French startup at ~€10bn. The stake would align two European tech leaders and is framed as bolstering Europe’s independence from U.S. and Chinese AI models.

Alstom won a €538m contract from Greater Wellington Regional Council to supply 18 battery-electric commuter trains and provide 35 years of maintenance, New Zealand’s first battery-electric fleet. The trains will replace aging diesel units to enable zero-emission service on non-electrified lines, with production at Alstom’s Savli (India) site.

Getlink’s August traffic showed mixed trends: LeShuttle Freight carried 86,090 trucks (−5% YoY, ~−3% calendar effect), taking YTD trucks to 778,237 (−2%), while passenger vehicles rose 5% to 334,846 and YTD reached 1,588,052 (+3%). The data underscores resilient leisure demand against softer freight flows.

Edenred — Turkey’s Competition Authority opened a full probe into Edenred, Multinet, Pluxee and Setcard over alleged collusion in tenders, customer allocation and information-sharing, a case that could affect pricing and merchant relations in a key market; Edenred had no immediate comment. Separately, a no-confidence vote in France risks further delaying the long-planned meal-voucher reform.

Phoenix Group H1 2025 results were mixed: IFRS operating profit rose 25% YoY to £451m (above £436m consensus) and operating cash generation reached £705m (+9% YoY, ahead of expectations) with a 175% Solvency II ratio, but total cash generation fell 17% YoY to £784m, disappointing the market and nudging shares ~5% lower. Retirement Solutions led growth, while management cited steady progress toward 2026 targets and confirmed a rebrand to Standard Life in March.

BAYROU…

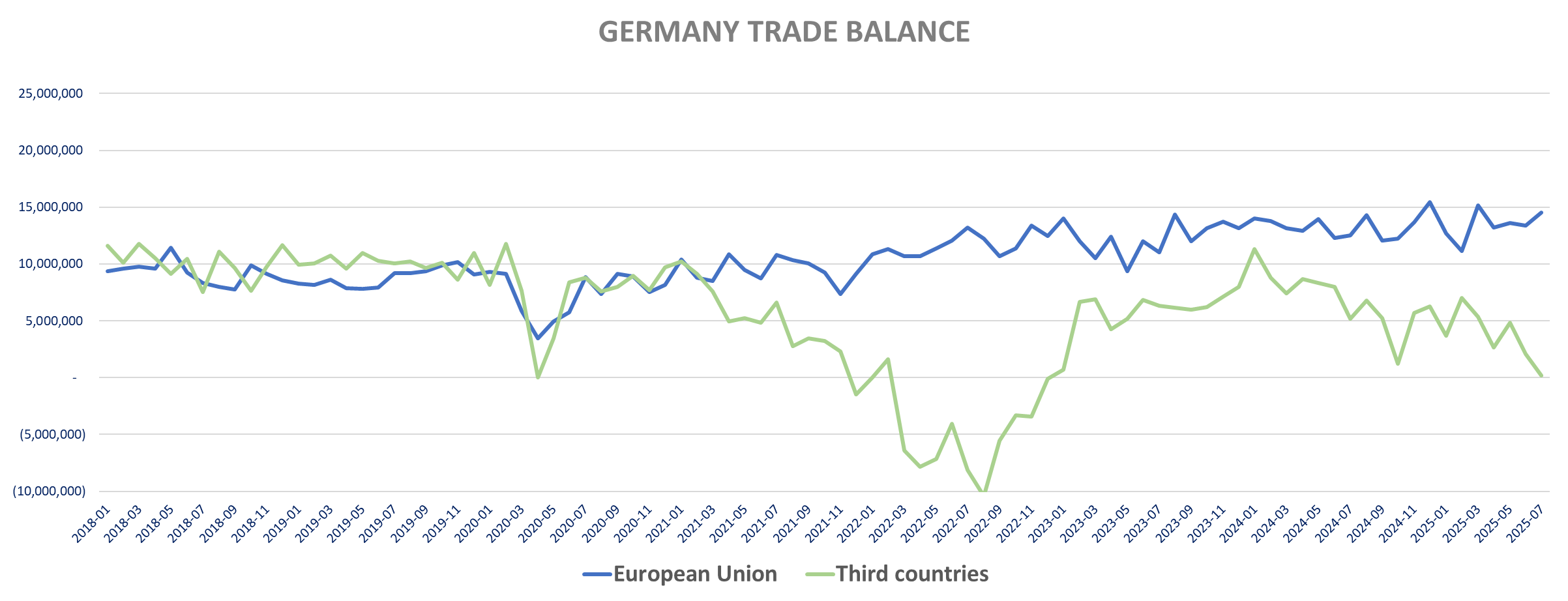

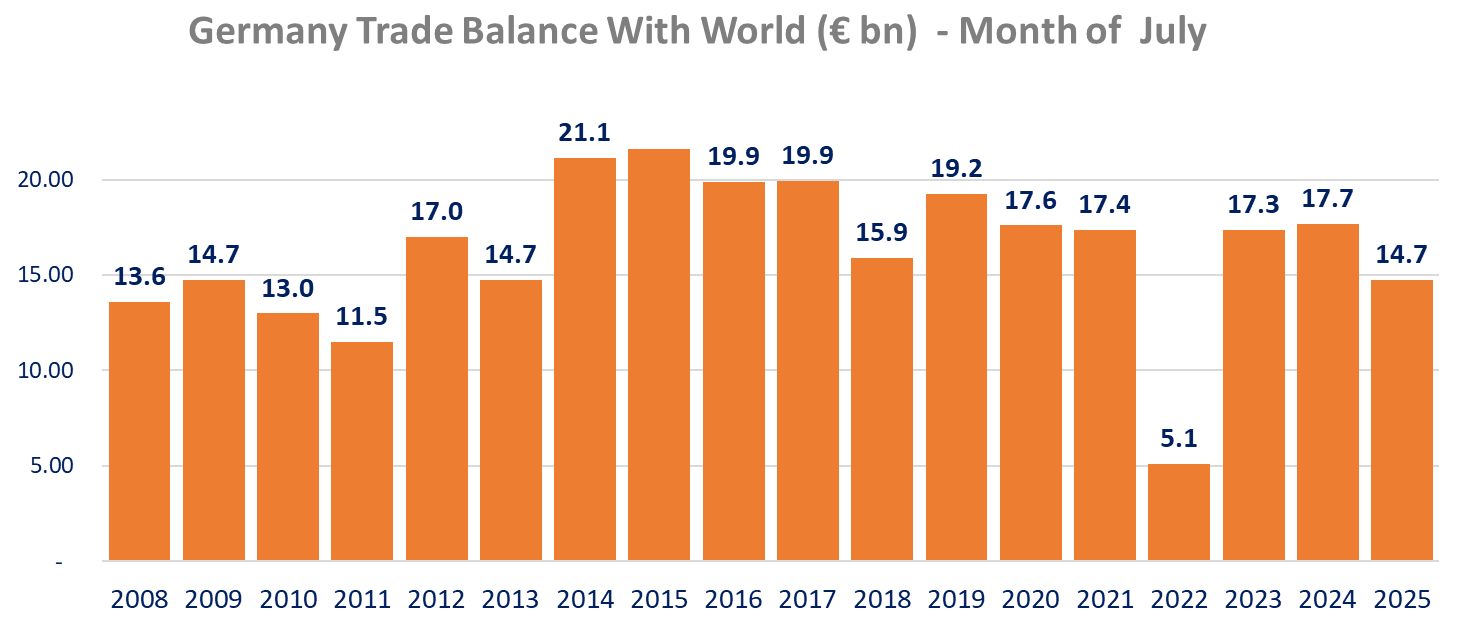

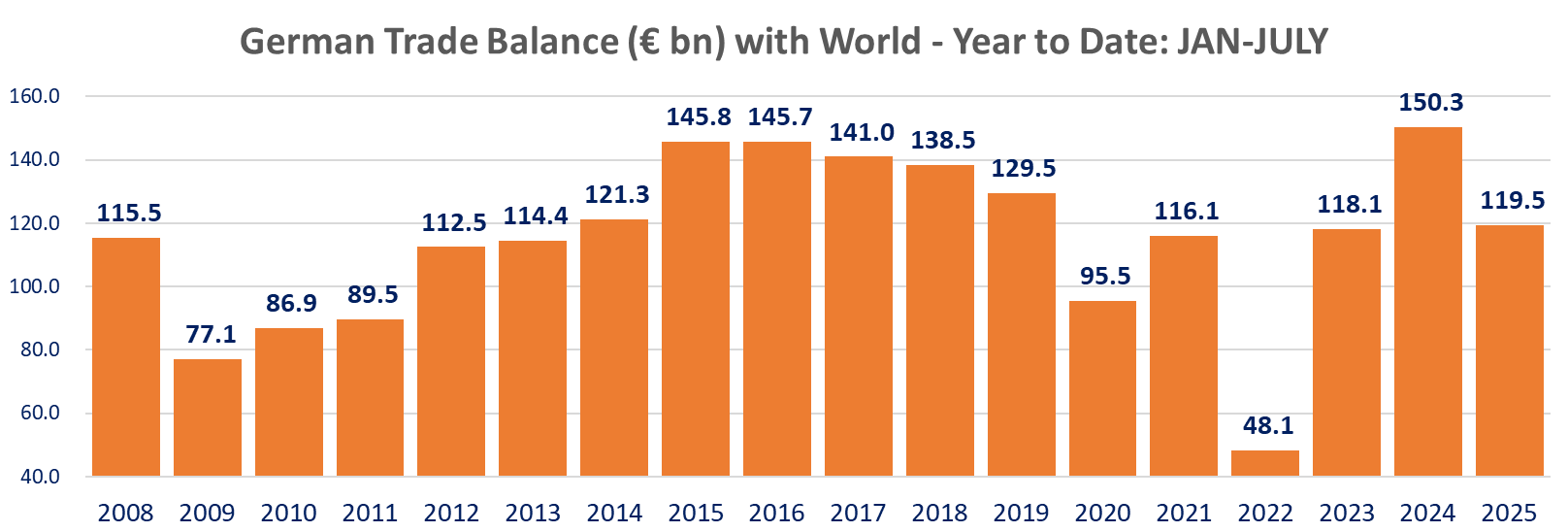

German July trade balance declined -4.3% m/m, -16.7% yoy to €14.7bn (€17.7bn in July 20240, below expectations of €15.4bn. Exports decreased -0.6% m/m (+1.4% yoy) to €130.2bn and imports declined -0.1% m/m (0% yoy) but are up 4.9% yoy to €115.4bn. Year to Date the surplus is to down -20.5% yoy to 119.5bn from €150.3bn for the same period of 2024. It is still above the same period for 2023. Ytd exports up 0.7% yoy to €916.1bn, imports up 4.9% to €796.6bn.

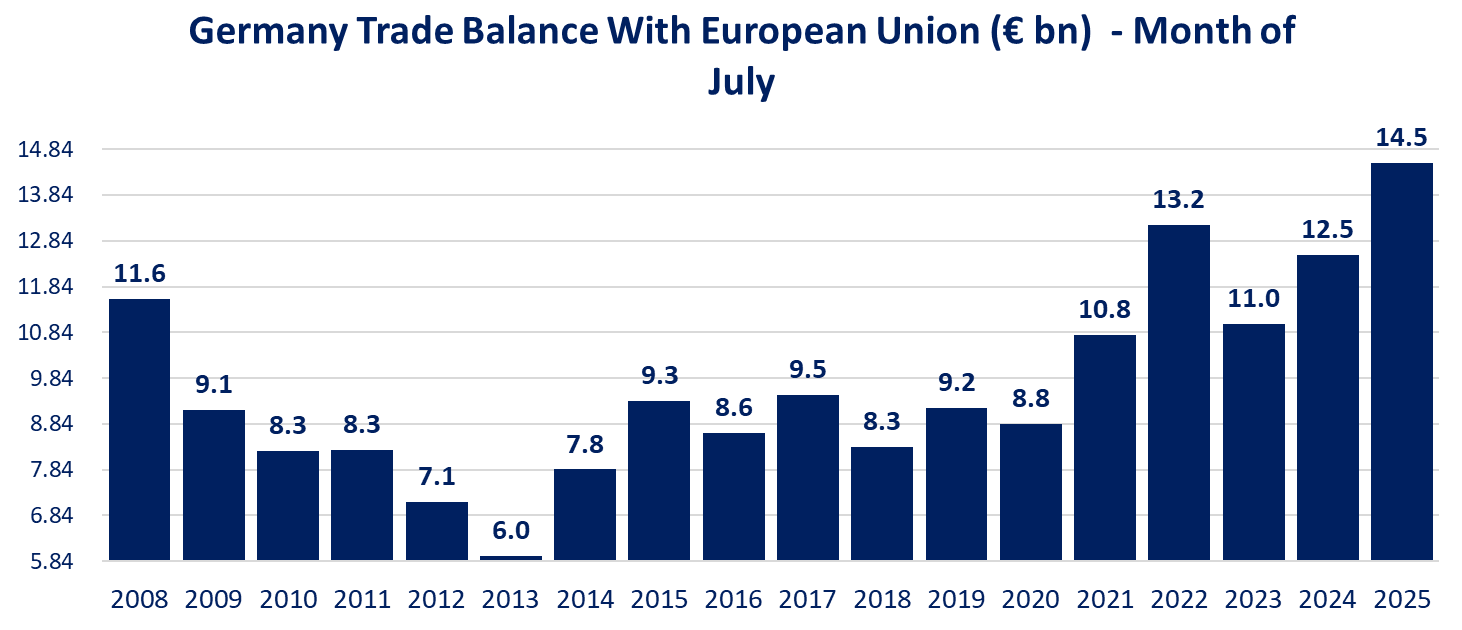

Trading with the EU increased, with exports to the EU up 2.5% m/m (+7.4% yoy) to €74.8bn and imports up 1.1% m/m (5.6% yoy) to €60.3bn, resulting in a surplus of 14.5bn in July (o/w 12.2bn with the Eurozone), i.e. all of the trade surplus registered with the world last month . It is a record for July and the trade surplus ytd with the EU is now at €93.7bn, also largest on record for the month of July.

The Trade balance with third countries (ex-EU) shrunk to just 0.2bn! Exports to third countries are down -4.5% m/m (-5.9% yoy) to €55.3bn and imports are down -1.3% m/m (+2.8% yoy) to €55.1bn.

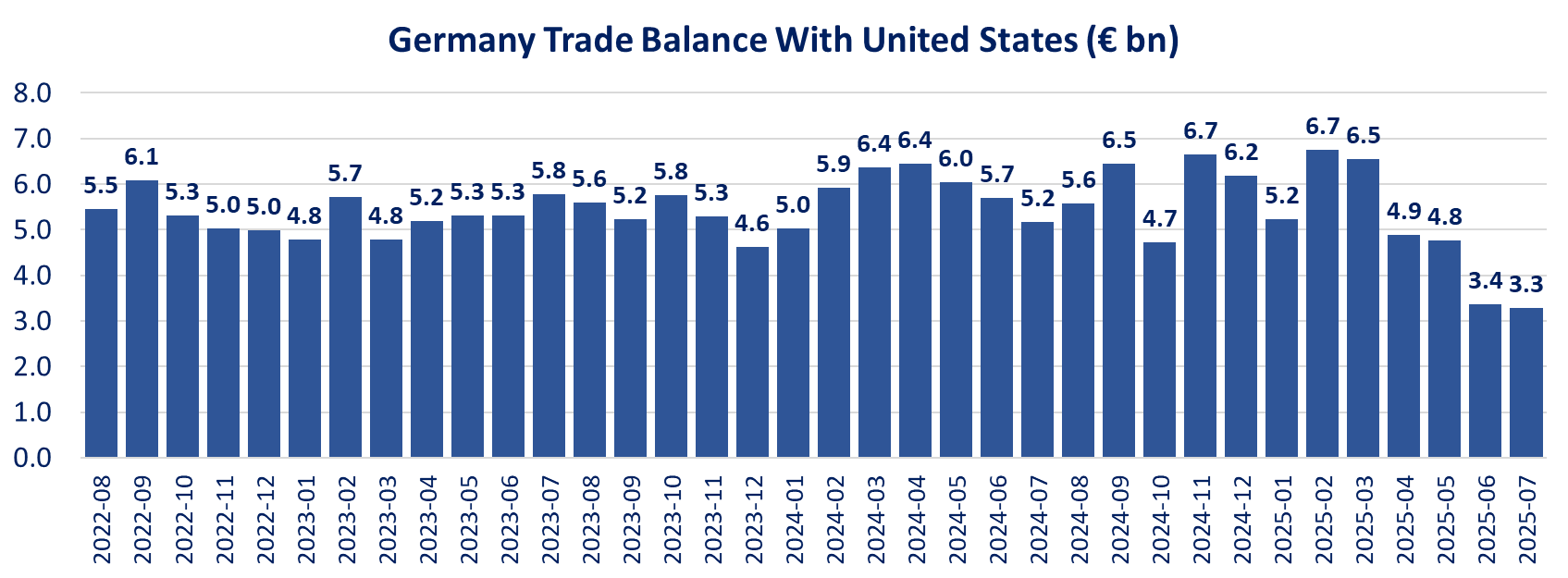

Trading with the US fell with exports falling -7.9% m/m (-14.1% yoy) to €11.1bn and imports down -10% m/m (+0.6% yoy) to €7.8bn. The surplus is down to just +3.3bn in July (-36.3% yoy), the weakest July since 2020. Year to date, the surplus is down -14.3% yoy to €34.8bn: exports -4.4% yoy ytd to €90.3bn and imports up 3.1% yoy ytd to €55.4bn

The deficit with China increased 2% m/m (+32.8% yoy) to -€7.9bn in July (-€6.2 in July 2024) with exports falling -7.3% m/m (-11.5% yoy) to €6.4bn while imports declined -2.4% m/m (but up 6% yoy) to €14.3bn. It is the worst deficit on record for the month of July. The deficit ytd is at -€49.4bn just shy of the 2022 July record of -€50.1bn.

The trade balance increased with the UK year-over-year to +3.8bn from 2.8b in July 2024 with exports up 8.2% yoy (to €7bn) and imports down -14.5% (€3.2bn).

See full tables for details by country (balance, exports, imports)

German industrial production rose more than expected in July, up 1.3% m/m rather than 1% expected, on top of a significant revision upwards for June. As we saw we the German orders last week, there are significant revisions in June, with production now down only-0.1% m/m rather than -1.9% reported initially. Destatis mentions the same reason as for the orders revision “due to corrected data that were subsequently reported by a large enterprise in the automotive industry, and to additional data that were provided”.

Construction production is up 0.3% m/m (civil engineering +1% m/m) and energy production was down -4.5% m/m. When excluding construction production is up 1.5% and when excluding both energy and construction production is up 2.2% m/m after -0.1% m/m in June revised from -2.8% m/m.

On a year-on-year basis production is down +1.5% yoy versus -1.8% yoy in June (revised up from -3.6% yoy!). Ex-construction production is up 2.1% yoy and excluding energy & construction, production is up +2.3% yoy after -2% yoy in June revised from -4.7% yoy reported initially.

Capital goods production increased the most month-over-month, up 3% m/m (after +0.5% m/m in June revised from -3.2%!), Intermediate goods production is up 0.8% after 0.2% m/m in June (revised from -0.6%) and consumer goods production is up 2.1% after -2.2% in June, revised from -5.6% m/m. Durable goods production is up 1.9% after -2.8% in June (revised marginally form -2.6%m/m). Non-durable goods production is up 2.2% m/m after -2% in June with a sharp revision from -6.2% m/m!

In terms of manufacturing sectors, machinery & equipment production surged +9.5% m/m, pharmaceuticals production increased 8.4% m/m, textiles +2.8% m/m, Motor vehicles +2.3% m/m, Food & beverages +1.3%. On the negative side production declined for furniture (-1.3%), paper product (-0.5%) and other transport equipment (-0.2% m/m).

|

|

Monday, September 8, 2025 | ||

|

ASML | |||

|

EUR |

667.80 |

+1.15% | |

|

ASML |

ASML is set to become Mistral AI’s largest shareholder, leading a €1.7bn Series C with about €1.3bn invested, valuing the French startup at ~€10bn. Reuters sources said that a stake in Mistral would tie together two European technology leaders, and the cash from ASML could help Mistral make Europe less reliant on U.S. and Chinese AI models. | ||

|

|

|

|

|

|

ALO | |||

|

EUR |

20.31 |

+1.40% | |

|

ALO |

Alstom announced on September 8 it has won a €538 million contract from the Greater Wellington Regional Council in New Zealand to supply 18 battery-electric trains and 35 years of maintenance—the country’s first-ever battery-electric commuter fleet. The trains will replace aging diesel units, enabling zero-emission operations on non-electrified segments of Wellington’s rail network, with construction at Alstom’s Indian facility. | ||

|

|

|

|

|

|

GET | |||

|

EUR |

15.76 |

+0.51% | |

|

GET |

Getlink August traffic data. LeShuttle Freight carried 86,090 trucks (−5% YoY, including ~−3% calendar effect), taking YTD trucks to 778,237 (−2%); passenger vehicles rose 5% YoY to 334,846, with YTD at 1,588,052 (+3%). The release flags continued resilience in leisure traffic alongside softer freight flows | ||

|

|

|

|

|

|

EDEN | |||

|

EUR |

22.83 |

-4.12% | |

|

EDEN |

Turkey’s Competition Authority opened a probe into four meal-voucher providers—Edenred, Multinet, Pluxee and Setcard—over alleged collusion in tenders, customer allocation and information-sharing. The watchdog said preliminary findings warranted a full investigation; Edenred had no immediate public comment at time of writing. The case could affect pricing dynamics and merchant relations in a key EM market for employee-benefits issuers. Additionally, a vote of non-confidence today in the French Parliament would threatens to delay the adoption of the meal voucher reform presented at the end of June. This project, which has been in the works for two years now, has already been postponed several times due to changes in government. | ||

|

|

|

|

|

|

PHNX | |||

|

GBp |

626.50 |

-6.49% |

Phoenix Group Holding release |

|

PHNX |

Phoenix Group released its 2025 interim results on September 7, delivering IFRS operating profit up 25% YoY to £451 million (consensus £436m), with operating cash generation of £705 million (+9% YoY, +2% vs. consensus) and a Solvency II ratio of 175%, 6pp ahead of market forecast. However, total cash generation was £784 million, down 17% YoY and below market expectations, causing a 5% drop in shares. Segment strength was led by Retirement Solutions (+19%), supported by annuity asset trading and cost efficiencies, offset by weaker European performance. Return on equity and balance sheet metrics improved due to debt reduction and robust capital actions. CEO Andy Briggs emphasized “a strong first half and steady progress toward 2026 objectives,” including upcoming rebranding to Standard Life in March | ||

Vs. Early Hours

Versus early hours:

Indices

Versus early hours

Versus early hours

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.