European stocks could not hold to gains with all sectors down but oil & gas. Russian position hardened from what we were led to believe post the Alaska meeting. No changes in demand and no agreement with Europe and what security guarantees means, killing hopes for a quick agreement or even a Zelensky Putin meeting.

All eyes on Jackson Hole, although there is little chance to see a pre-commitment as inflation is still expected to pick up while the political pressure increases (more likely to results in pushback rather than submission).

The Fed is already in a fiscally dominated world, but the Administration funding strategy requires lower rates and will lead to greater loss of independence if inflation prevents significant easing. The US debt continue to increase (now $993bn above July 4 level at $37.21tn). Curves will steepen further.

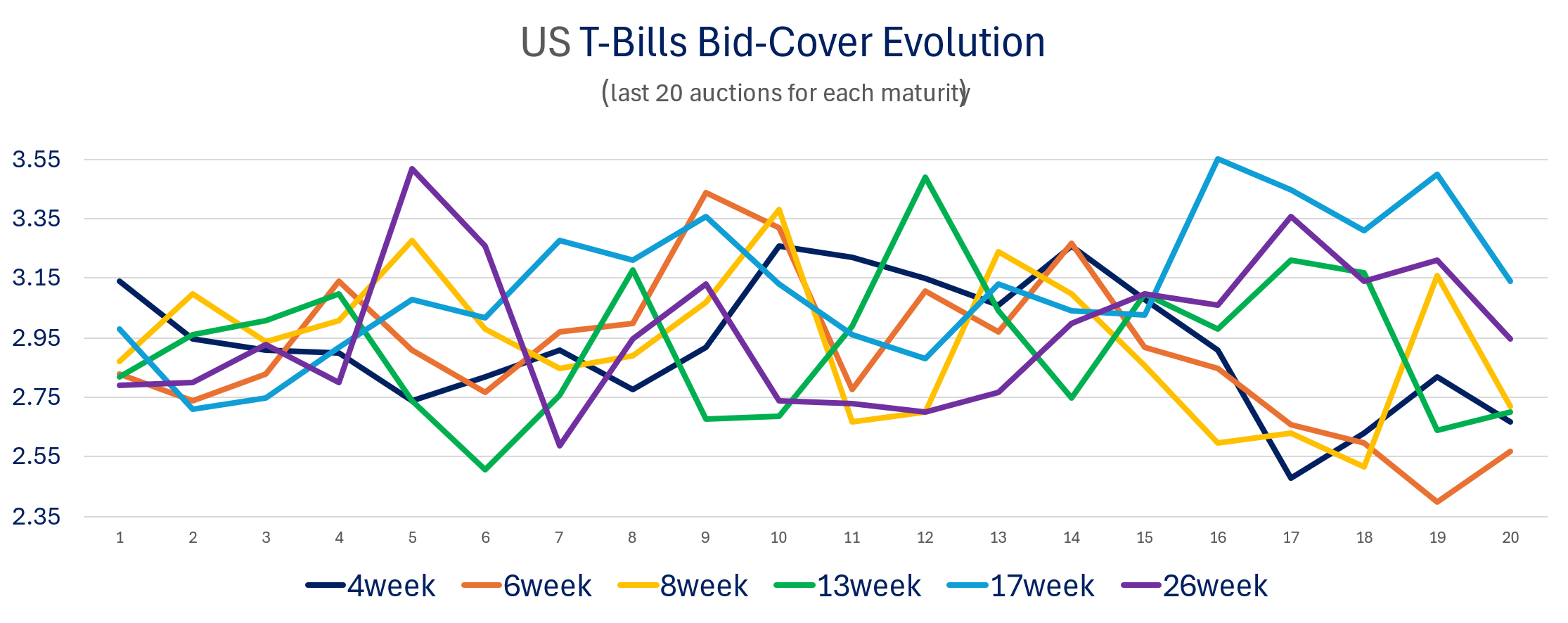

Bond Yield are higher ahead of Powell speech tomorrow after the rather weak 20yr auction yesterday with again lower share of indirect bid. We also not that the bid/cover for T-Bill auction are down.

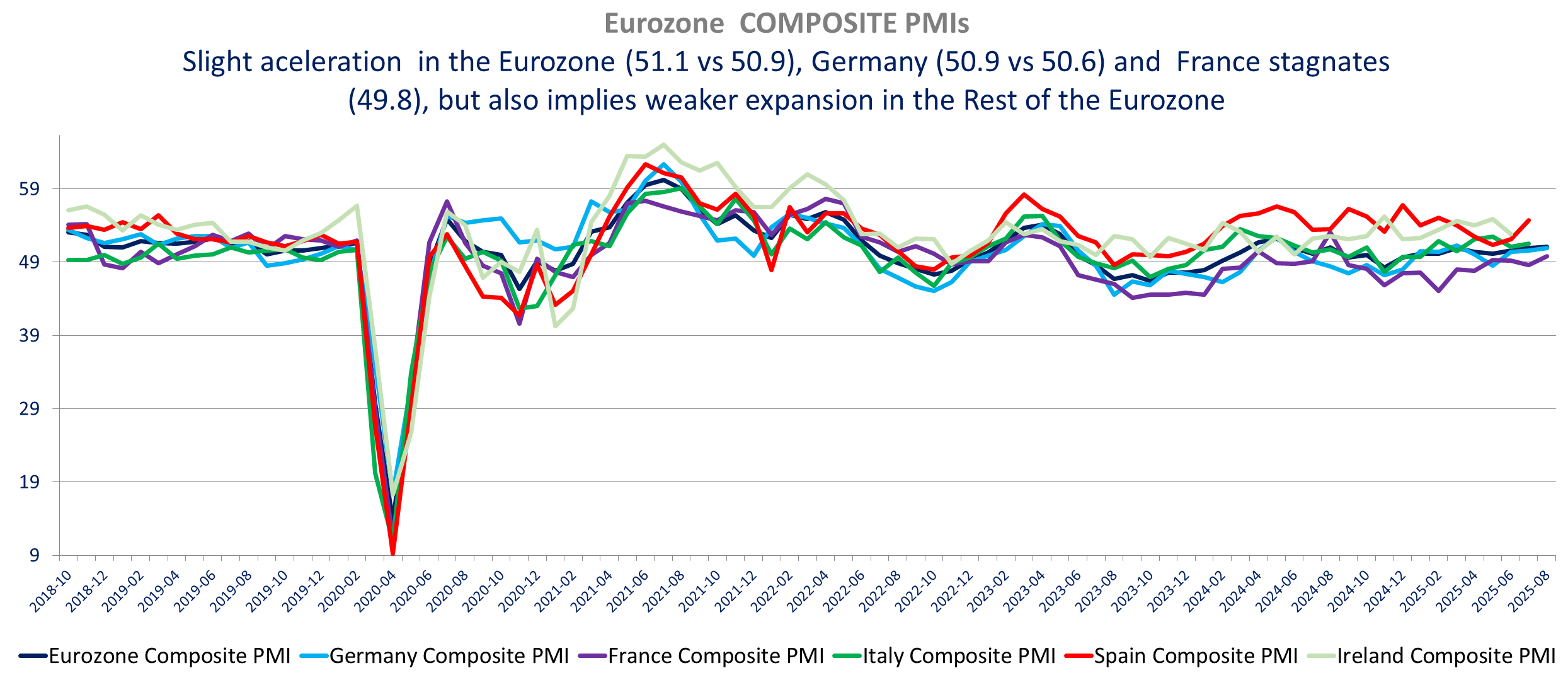

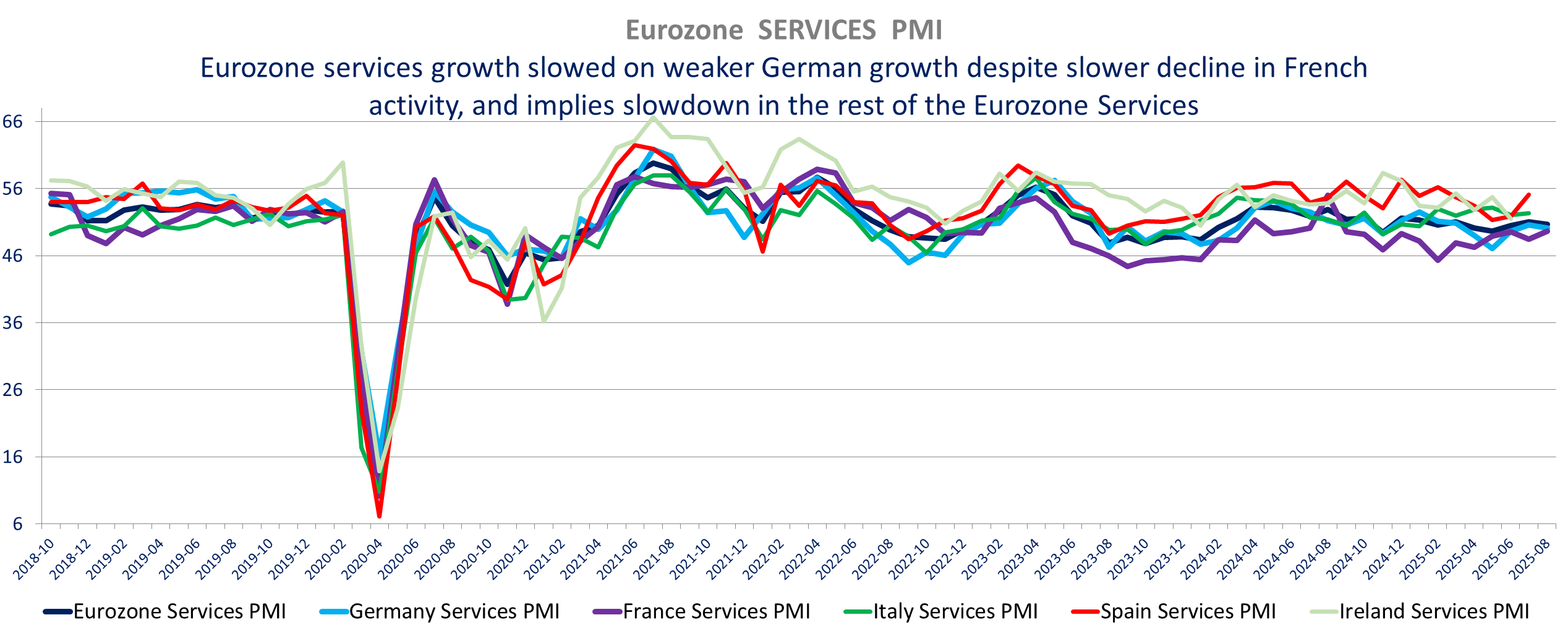

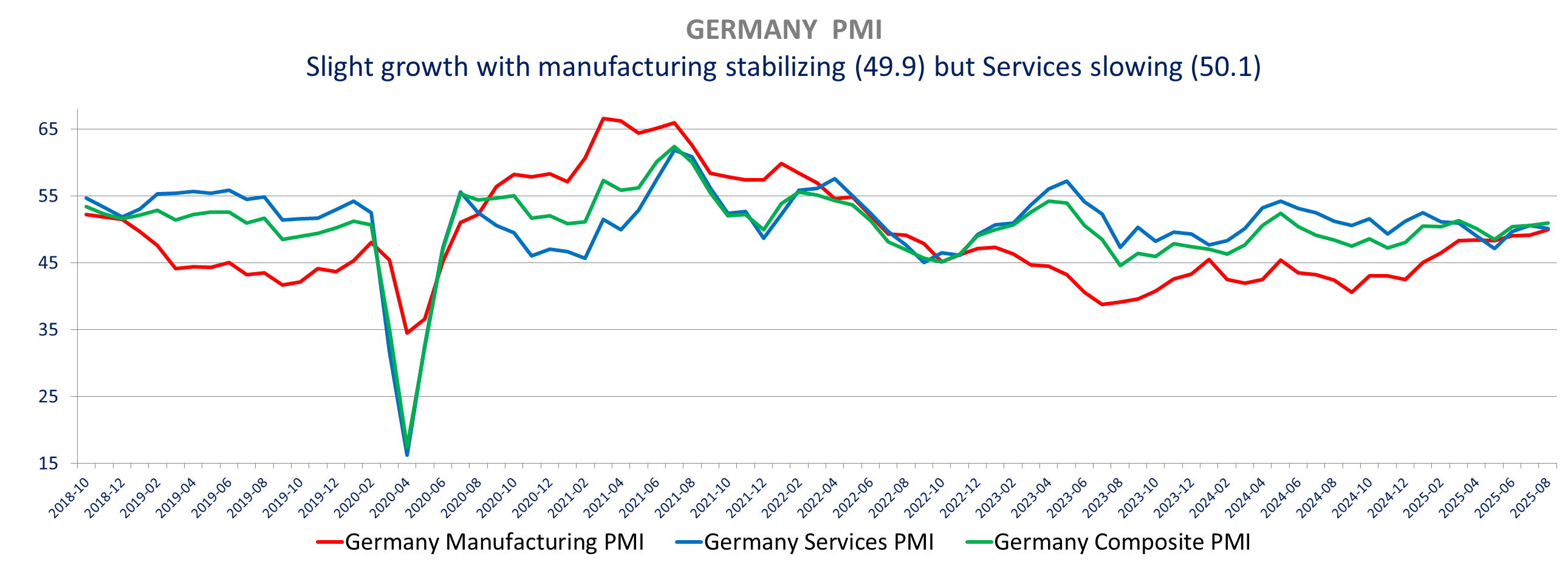

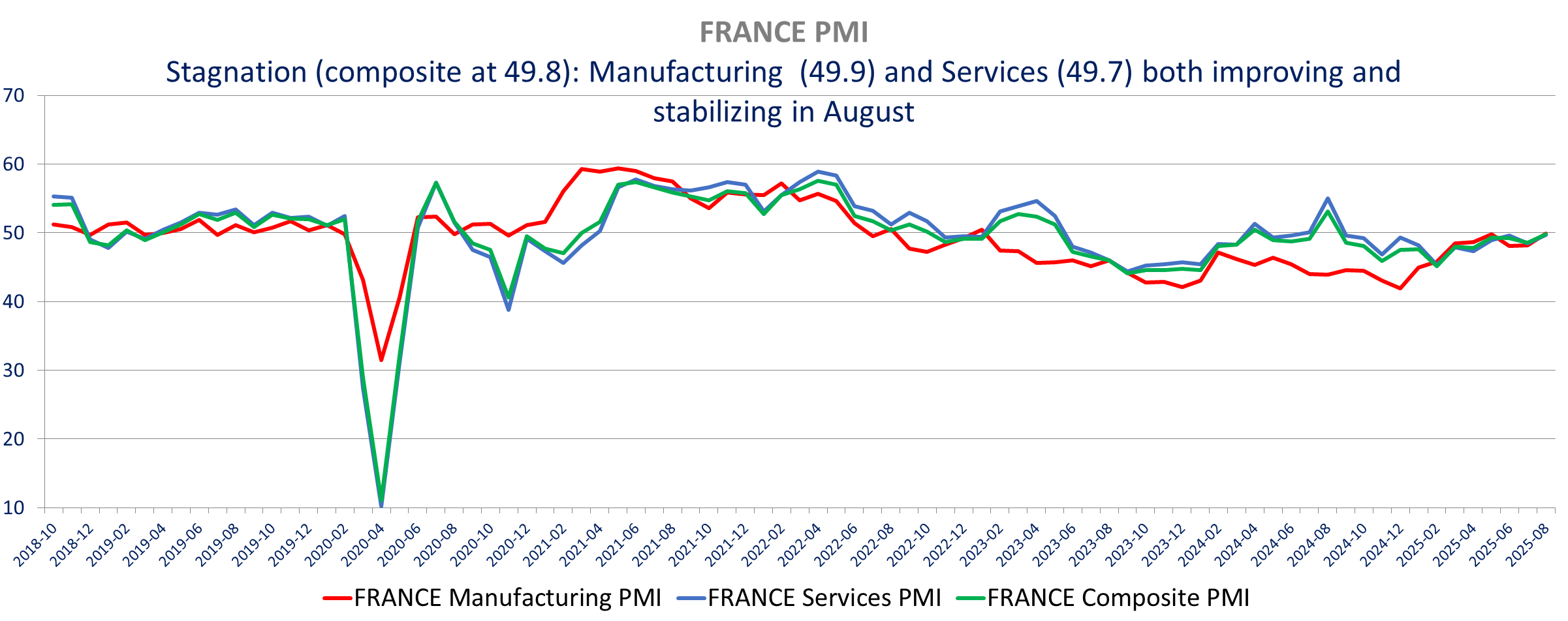

The Eurozone Flash PMI came above expectations as Manufacturing and France improved more than expected. The data implies some slowdown in the rest of the Eurozone. The Eurozone composite PMI improving to a 15-month high of 51.1 from 50.9 in July while economists expected a slight deceleration to 50.7. Eurozone manufacturing swung back to growth in August (50.5 vs 49.5 expected, 38 months high) and services slowed only marginally more than expected with the Services PMI at 50.7 down from 51 and below expectations of 50.8, a 2-month low. France economy stagnated in August improving more than expected in both sectors. In Germany, we also see Manufacturing stabilizing with the Manufacturing PMI improving to 49.9 from 49.2 (38 months high) when economists expected a deeper slowdown at 48.8, while services slowed more than expected to 50.1 vs 50.2 expected down from 50.6 in July , lowest in 2 months.

We see stronger manufacturing production (41month high Output PMI for the Eurozone and Germany, flat production in France) and new orders improved (up for first time Since April 2022 in Manufacturing). Employment increased (still declining for German manufacturing, but up in France for both sectors. Inflationary pressure increases though, with manufacturing input costs up for the first time in 5months, and Services input costs increased the most since March, increasing in all Germany, France and the rest of the Eurozone. Price charges are up in both sectors, increasing at a modest but fastest pace in 4 months.

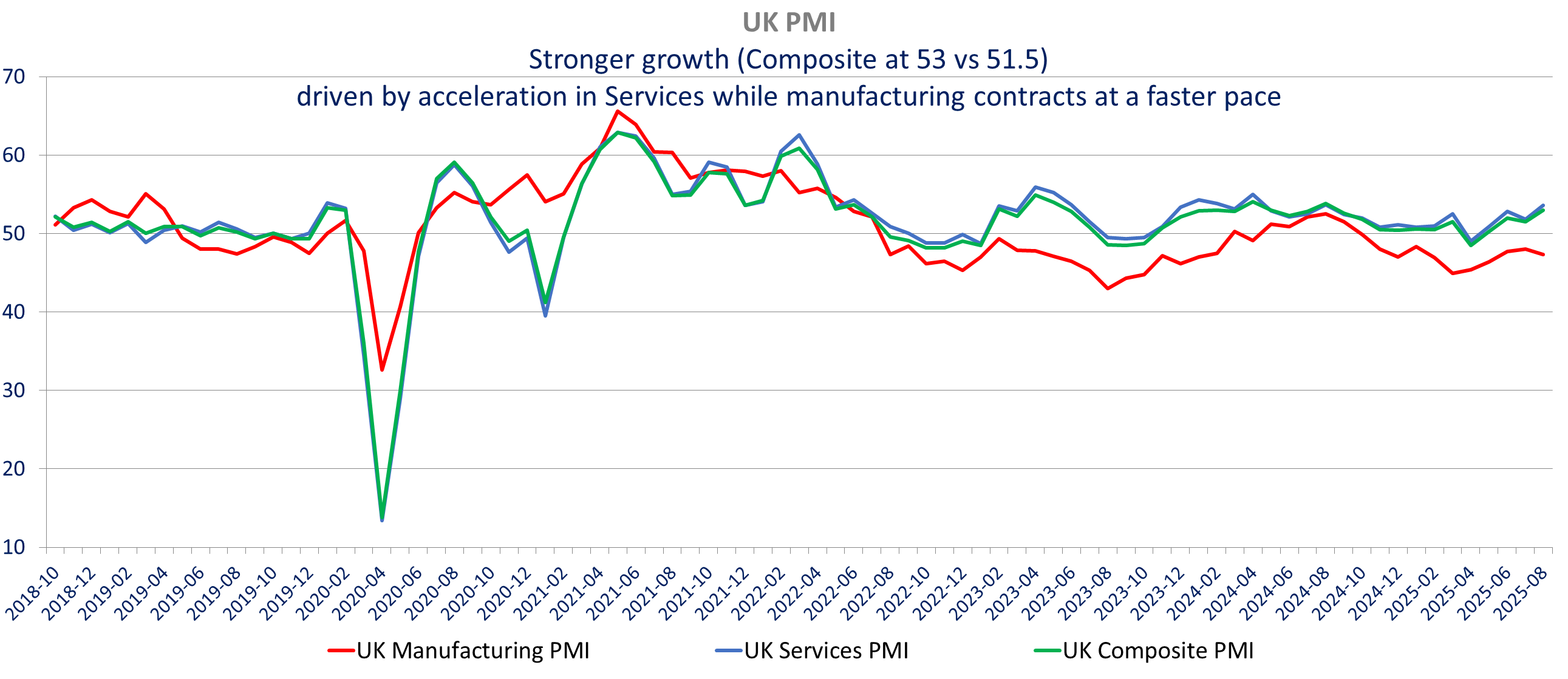

The UK flash PMI shows divergence between manufacturing and services. Inflationary pressure persists driven by services. Disappointing Manufacturing PMI, declining to 47.3 (3 months low) from 48 in July, when expectations were for an improvement to 48.3. On the contrary, services activity accelerated more than anticipated as the services PMI surged to 53.6 from 51.8 far above expectation of 51.8 reaching the highest level in 12 months. The composite PMI is also at a 12-month high at 53 up from 51.5 in July, beating expectations of 51.6. Employment continues to decline in both sectors.

Input costs inflation increased in August to the highest since May, increasing in both sectors. Manufacturers report the sharpest increase in suppliers’ delivery times since December on shipping delays.

Price charged increased at the steepest rate in 3 months for services, but inflation slowed to the lowest level since January in manufacturing.

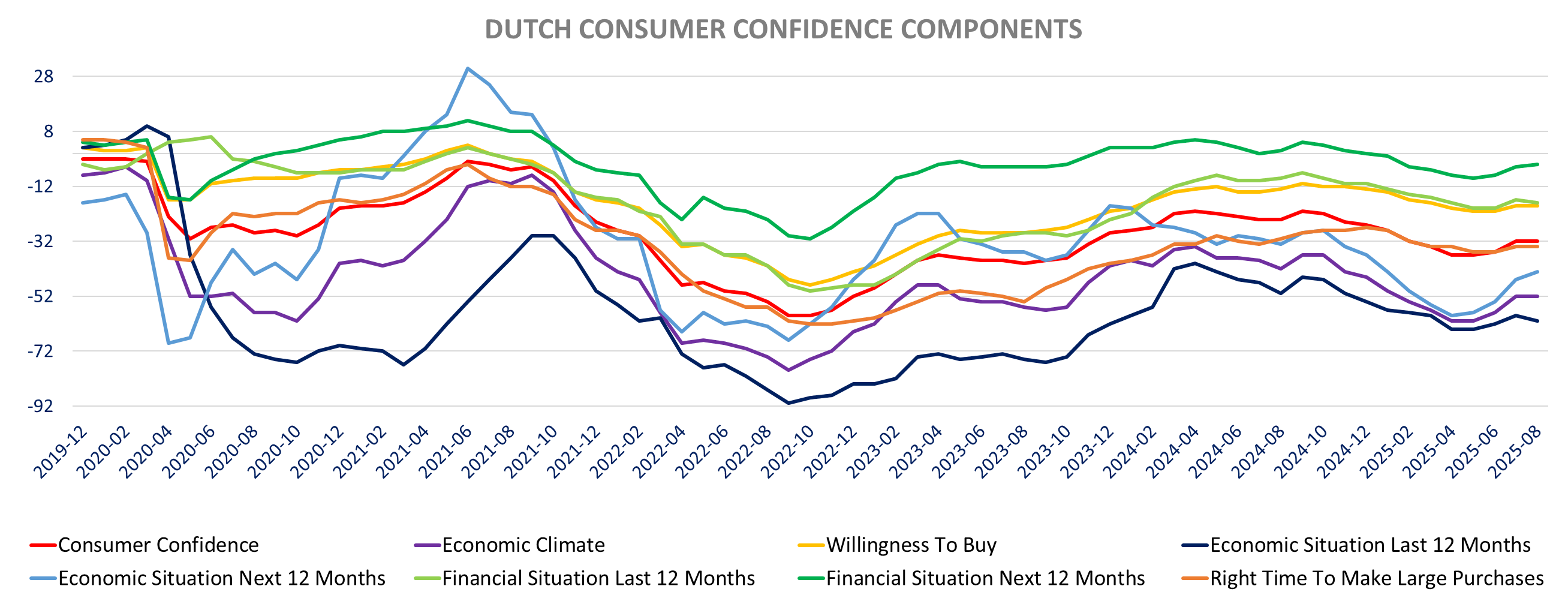

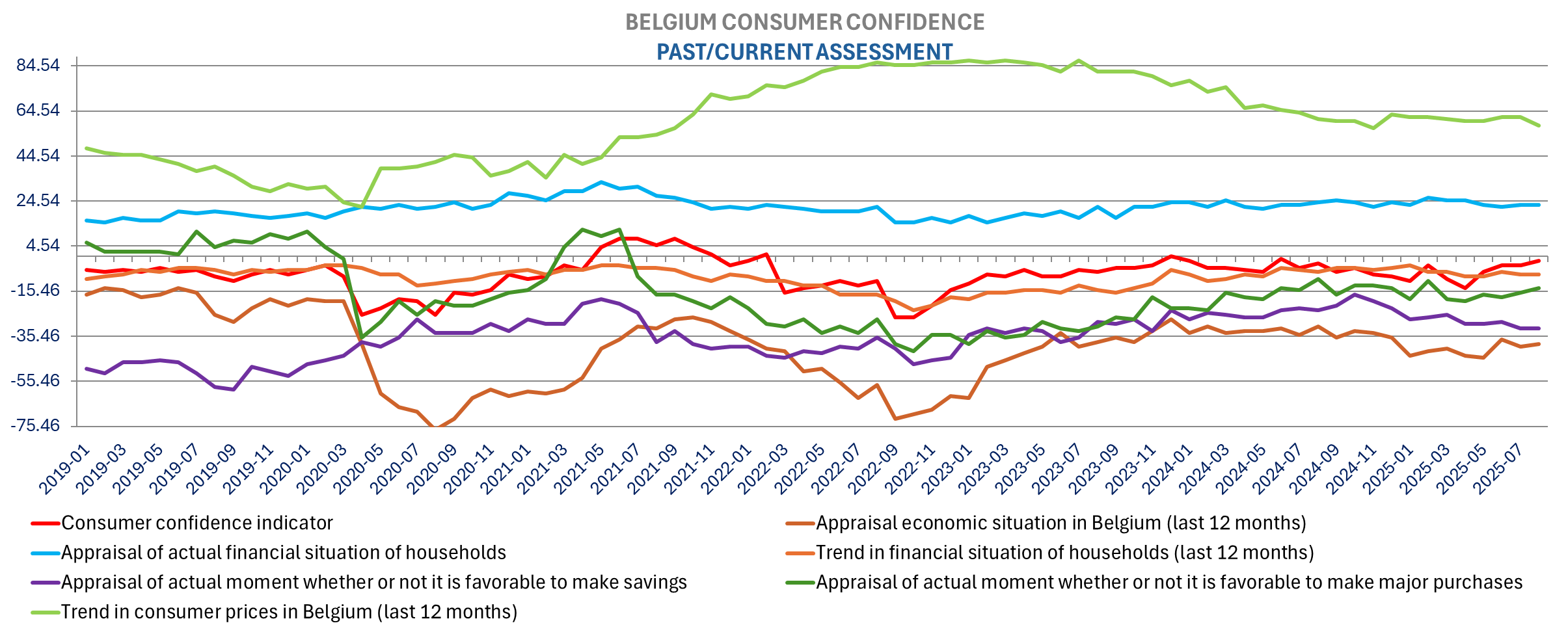

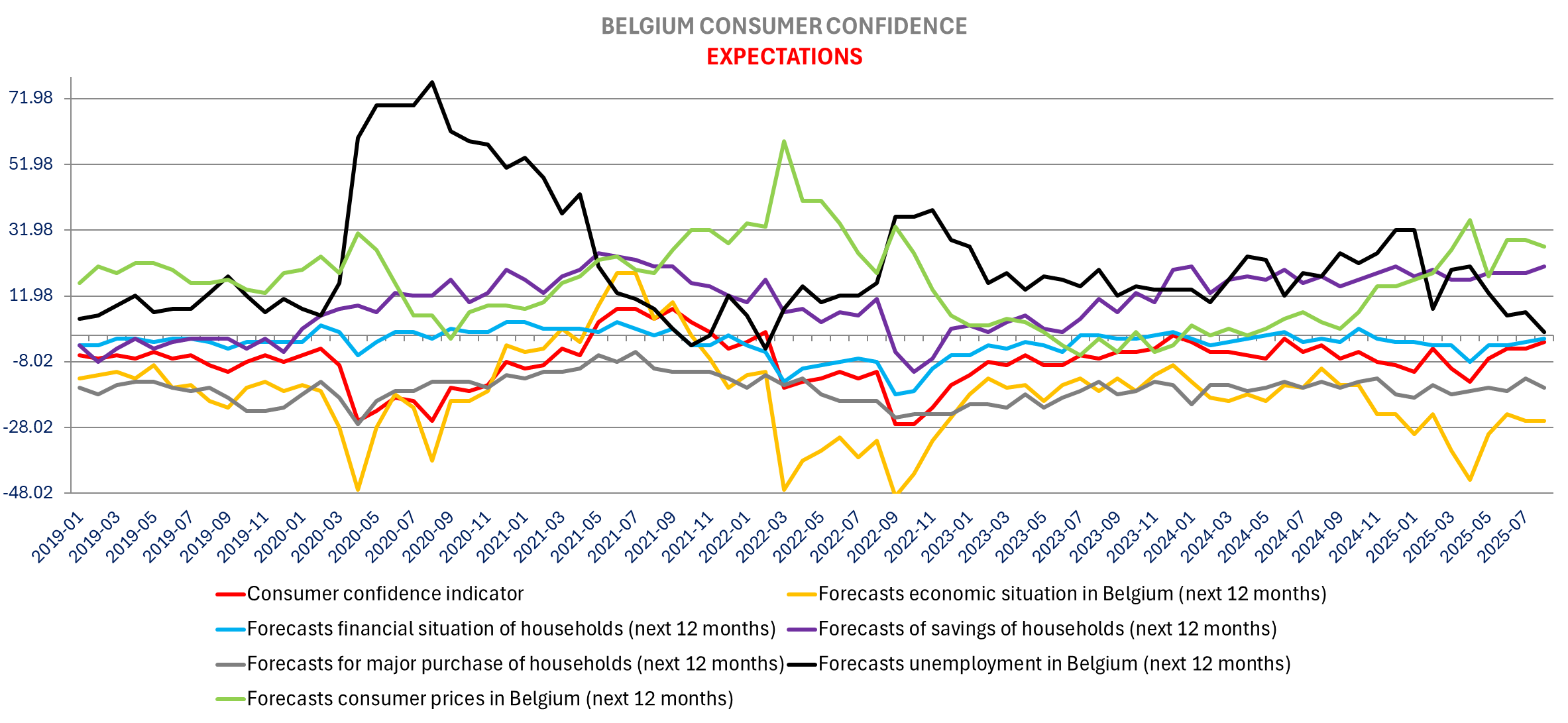

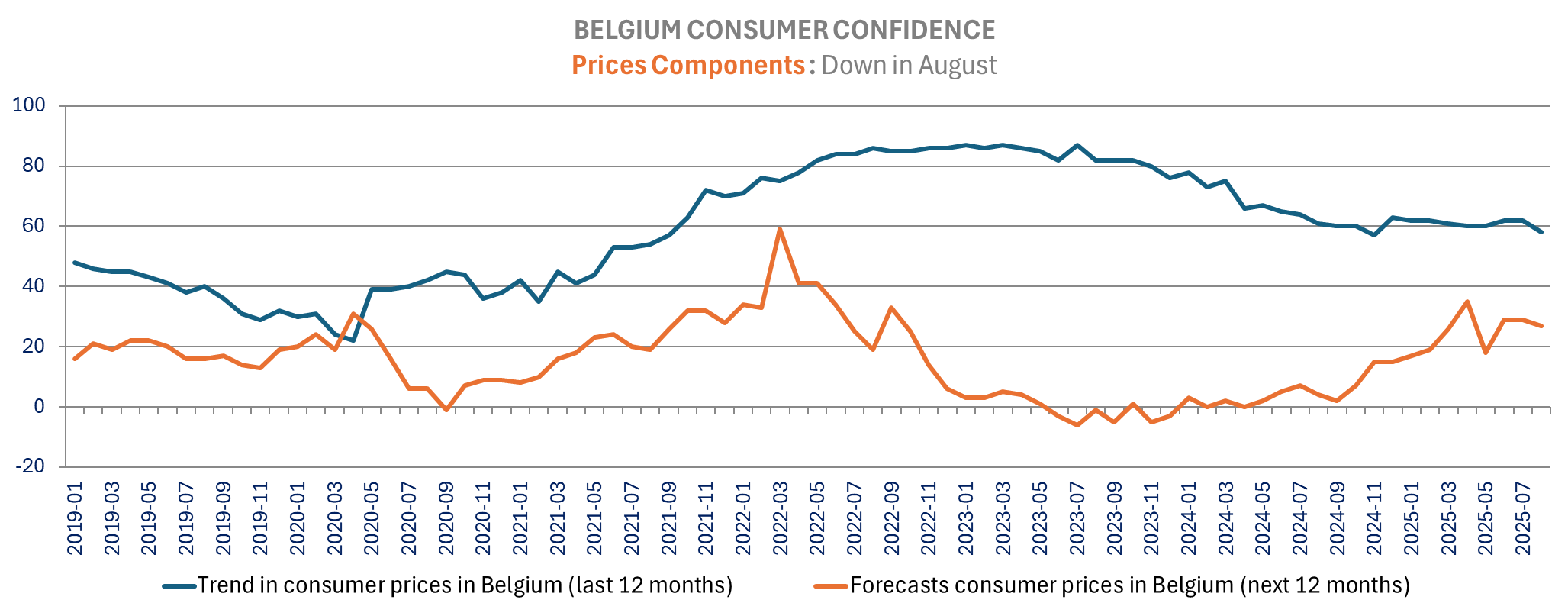

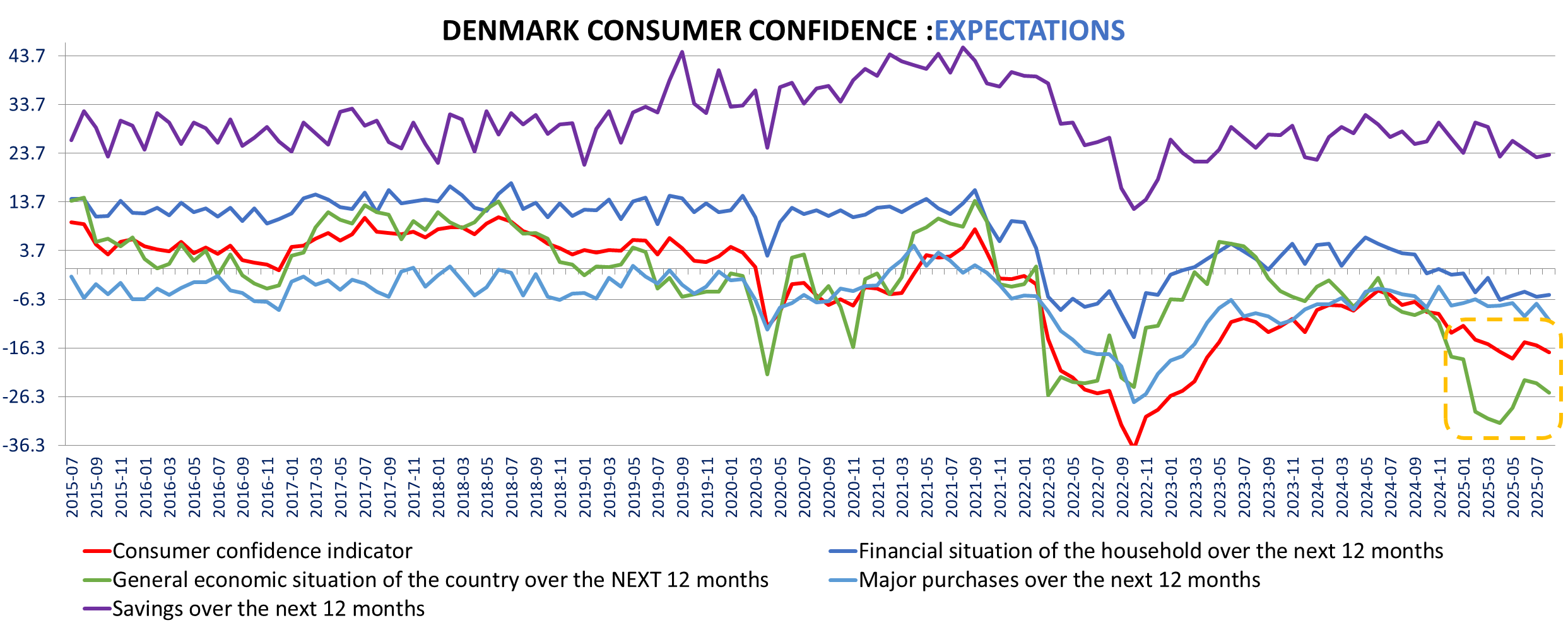

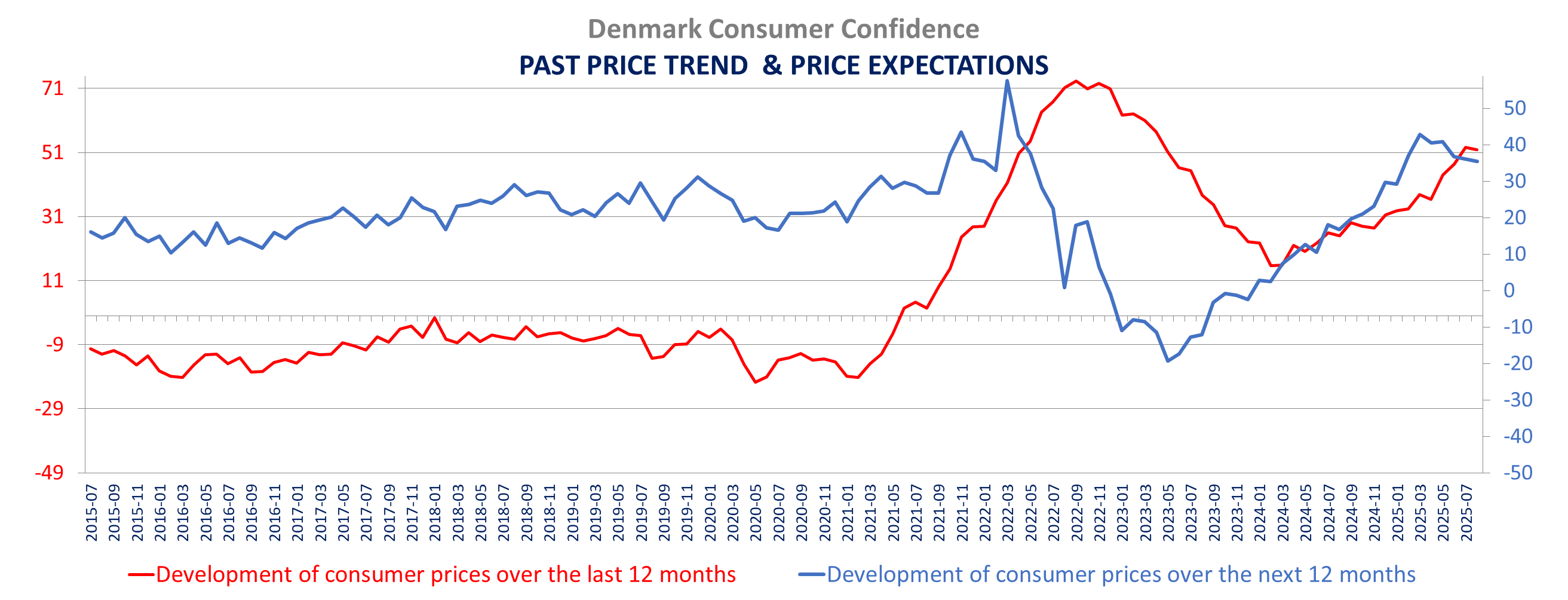

We have the first August consumer confidence data in Europe with Consumer confidence in the Netherlands, Belgium and Denmark. The three countries are consistent is showing consumers’ lower inflation expectations (and past price trend), but we see some divergence with consumer confidence up significantly in Belgium, Unchanged in The Netherlands and down in Denmark. Unemployment fear declined in Belgium is unchanged in Holland and is slightly higher in Denmark.

GN Store Nord’s Q2 2025 revenue fell 8% year-on-year to DKK 4,160 million, missing organic growth expectations but meeting consensus on reported revenue; EBITA surged 46% to DKK 546 million, with margin expansion and strong Hearing division performance offsetting declines in Enterprise and Gaming, while free cash flow nearly tripled on disciplined cost control and restructuring.

Aegon’s H1 2025 results beat expectations, with operating capital generation at €576 million and a significant U.S. contribution; the company doubled its share buyback to €400 million, raised its dividend, and is considering relocating its legal domicile to the U.S., reflecting confidence in its North American-led growth strategy.

SalMar Q2 2025 profits dropped sharply on weaker salmon prices despite higher volumes, with operational EBIT down to NOK 524 million from NOK 1.38 billion; Norway’s segment remained profitable, and the company raised full-year harvest guidance while cautioning about ongoing market volatility and biological challenges.

ALK-Abello: Q2 2025 organic revenue grew 12%, beating forecasts, with EBIT up 41% and margins expanding to 25%; growth was led by strong tablet and anaphylaxis product sales in Europe and North America, and management raised full-year guidance on the back of successful new product launches and cost optimization.

Siegfried Holding’s H1 2025 net profit of CHF 65.7 million missed consensus, pressured by weaker Drug Products sales and FX headwinds; Drug Substances performed in line, and the company-maintained guidance for mid-single-digit revenue growth and an EBITDA margin above 22%, expecting a recovery in H2.

Kojamo Oyj Q2 and H1 2025 revenue growth was modest (up 2.9% and 1.9%, respectively), but profitability was pressured by property valuation losses and higher costs; occupancy improved, and the company is selling non-core assets to strengthen its balance sheet, with stable full-year guidance.

Porr AG H1 2025 revenue and earnings rose, with order intake up 25% and the backlog reaching a record high; Infrastructure International led growth, and the company expects moderate full-year growth with an EBIT margin of 2.8–3.0%, supported by disciplined capital allocation and a strong project pipeline.

BKW SA H1 2025 profits fell sharply (-44%) as energy markets normalized and one-off contributions faded, with segmental declines in Energy Solutions offset by resilience in Power Grid and growth in Infrastructure & Building; guidance is unchanged, with a stronger H2 expected.

CTS Eventim H1 2025 revenue hit a record €1.294 billion (+7.6%), but adjusted EBITDA slipped slightly, with Ticketing performing strongly and Live Entertainment pressured by integration costs; the outlook remains positive as post-acquisition synergies are realized.

WH Smith Issued a major profit warning after discovering a £30 million overstatement in North American trading profit, slashing FY25 pre-tax profit guidance to £110 million and prompting an independent review; the error has shaken analyst confidence in near-term performance.

Stocks table here

Jackson Hole start & Job Market

Elusive deal: hardening position from Russia

20 yr auction on the weak side, y, also posting lower indirect bidders at 60.6% versus 67.55% for the last 12 auction average and 67.4% in July, down to the lowest share since February 2024!

For T-Bills the bid-cover ratios have not been stellar either:

The Eurozone shows a slight acceleration in expansion in August, above expectations. The Eurozone composite PMI improving to a 15-month high of 51.1 from 50.9 in July while market was looking for a slight deceleration to 50.7. The PMI improved for both France and Germany, and with sharper improvement in manufacturing. The Data implies a growth slowdown in the rest of the Eurozone.

Eurozone manufacturing swung back to growth in August (50.5 vs 49.5 expected, 38 months high) and services slowed only marginally more than expected with the Services PMI at 50.7 down from 51 and below expectations of 50.8, a 2-month low.

France economy stagnated in August improving more than expected in both sectors, both stabilizing: composite at 49.8 up from 48.6, vs 48.5 expected, highest in a year, with the manufacturing PMI at a 31-month high of 49.9 up from 48.2 vs 48.0 expected, and services PMI at 49.7 vs 48.5 beating expectations of 48.5, sitting at the highest level since August of last year.

In Germany, we also see Manufacturing stabilizing with the Manufacturing PMI improving to 49.9 from 49.2 (38 months high( when economist s expected a deeper slowdown at 48.8, while services slowed more than expected to 50.1 vs 50.2 expected down from 50.6 in July , lowest in 2 months. The German composite shows a slight increase in growth for the economy at a 5-month high of 50.9 vs 50.6 in July. above expectations of a slowdown to 50.2.

Disappointing Manufacturing PMI, declining to 47.3 (3 months low) from 48 in July, when expectations were for an improvement to 48.3. On the contrary, services activity accelerated more than anticipated as the services PMI surged to 53.6 from 51.8 far above expectation of 51.8 reaching the highest level in 12 months. The composite PMI is also at a 12-month high at 53 up from 51.5 in July, beating expectations of 51.6.

Dutch consumer confidence is unchanged in August at -32, best since February, with many components unchanged such as willingness to buy, large purchase opportunity and savings intention. When there are changes the past situation is lower and expectations higher.

The Economic climate is also steady at -52 which was the highest since January, but with lower past economy assessment at -61 vs -59 and higher economic expectations at -43 vs -46 in July, best since December 2024.

Consumers past financial situation is down to -18 vs -17 but future financial situation is up to -4 vs -5.

On the price front both past prices assessment and expectations are lower, only 20% see a sharp increase in prices in the next 12 months down from 24%, the lowest since October. 50% expect moderate price increasing up from 48%.

Belgium consumer confidence increased to a 14-mnth high of -2 in August up from -4 in June-July. Contrary to Dutch consumers Belgium households are a little less negative on the past economy. Expectations on the economy and past financial situation are unchanged, but personal financial situation expectations improved (-1 vs -2).

Unemployment fear declined significantly in August to +1 vs +7 (was 77 at the peak of covid) the lowest since February 2022.

Consumer are less negative in making large purchases now but more negative over the next 12 months.

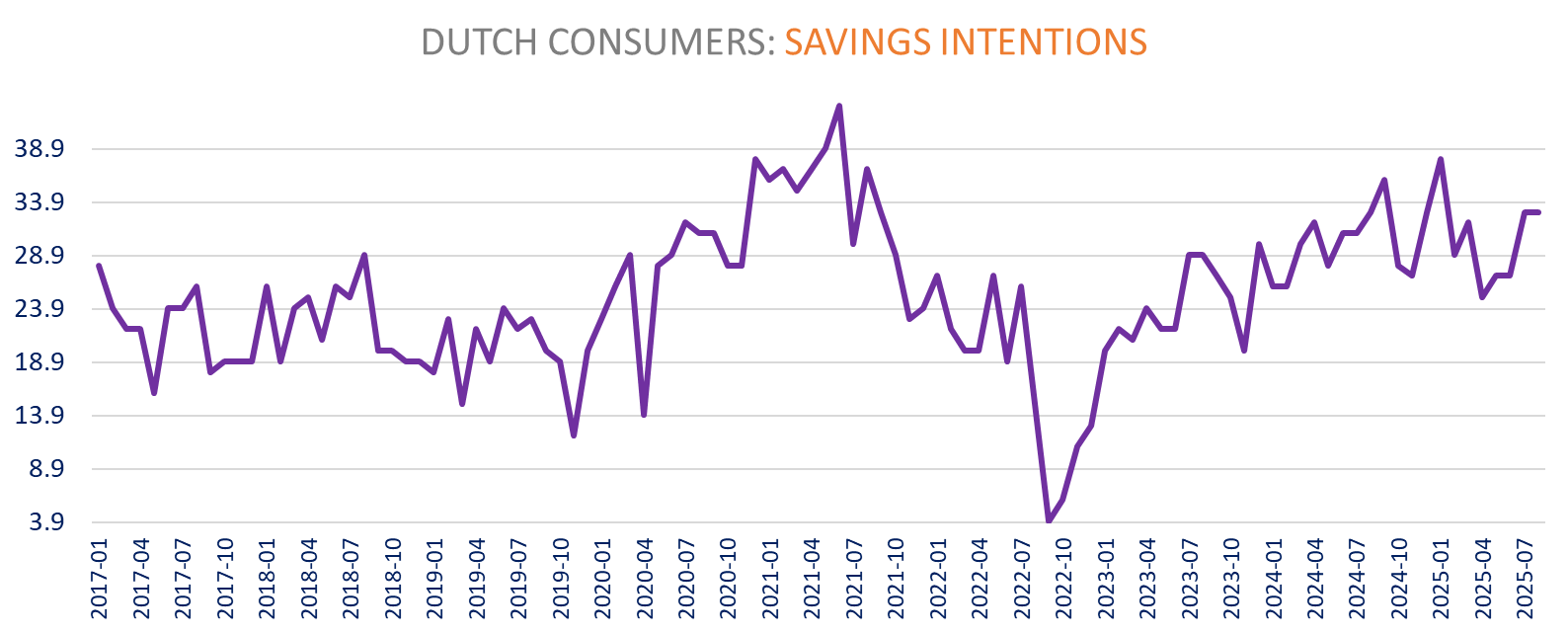

Savings intention rose further to the highest since July 2021 (21 vs 19 in July)

Past price assessment and price expectations are down.

Denmark consumer confidence deteriorated in August down to -17.2 from -15.7, lowest since May with - as for Dutch consumers - deterioration in past assessment of the economy (-26.3 vs -21.9) and past financial situation (-13 vs -11.1) Danish consumers are also more negative on the economic expectations (-25.5 vs -23.5) but slightly less pessimistic on their future financial situation (-5.4 v s-5.8).

Unemployment fear worsened slightly in August to 11.9 vs 11 in July (12.9 in June).

Households are as negative as in July about making large purchases now (-16) and are the most negative about making large purchases in the next 12 months since November 2023 at -10.5 down from -7.2 in July.

Savings intentions re-increased in August to 23.5 after a dip to 22.9 in July (24.6 in June).

On the price front, both past price assessment (51.8 vs 52.6) and price expectations (35.4 vs 36.1, lowest since January) are lower.

|

|

Thursday, August 21, 2025 | ||

|

GN | |||

|

DKK |

117.35 |

+14.71% | |

|

GN |

GN Store Nord reported second-quarter 2025 revenues of DKK 4,160 million, down 8% year-on-year (from DKK 4,499 million in Q2 2024) and organic revenue growth of -5%, missing consensus estimates for organic growth and just meeting expectations for reported revenue (analyst consensus was around DKK 4,100 million). The company’s EBITA, however, outpaced expectations, surging 46% to DKK 546 million (up from DKK 374 million), with the EBITA margin expanding sharply by 480 basis points to 13.1%. EBITDA margin also rose to 15.4% (from 10.5%), well above forecasts. Segments diverged: the Hearing division delivered 8% organic growth and 4% reported growth (DKK 1,858 million vs. DKK 1,792 million), while the Enterprise division reported a 9% decline (DKK 1,713 million vs. DKK 1,873 million) and Gaming, excluding consumer assets now wound down, saw a 4% fall (DKK 589 million vs. DKK 611 million). Gross profit was marginally down at DKK 2,313 million (from DKK 2,334 million), but gross margin improved significantly to 55.6%, up 370 bps, reflecting strong price management and cost control. Free cash flow, excluding M&A, nearly tripled to DKK 353 million (from DKK 155 million), reflecting disciplined working capital management and restructuring initiatives. Management underscored strong execution in Hearing, especially around the ReSound Vivia and Savi launches, driving global market share gains, while Enterprise and Gaming divisions benefited from supply chain diversification and price adjustments in the U.S. to offset tariff impacts, which are now expected to dent the 2025 EBITA margin by about 1% in total. CEO Peter Karlstromer highlighted continued progress through macroeconomic challenges, reiterating confidence in medium-term market opportunities. Guidance for 2025 was confirmed for an EBITA margin of 11–13% and free cash flow (excluding M&A) of around DKK 800 million, with organic revenue growth expectations narrowed to -2% to +2% | ||

|

|

|

|

|

|

AGN | |||

|

EUR |

6.86 |

+6.62% | |

|

AGN |

Aegon exceeded expectations in its H1 2025 results, delivering stronger-than-anticipated operating capital generation and reinforcing shareholder value. Operating capital generation stood at €576 million, narrowly beating consensus estimates and with the U.S. business contributing €371 million—highlighting the continued strength of its Transamerica operations. The company also doubled its share buyback program to €400 million (to be completed by end‑2025) and raised its interim dividend by nearly 20%, underscoring strong cash flow and return-of-capital focus. At the same time, Aegon announced it is studying a possible relocation of its legal domicile and headquarters to the U.S., citing that over 65% of earnings derive from its U.S. operations. A decision is expected by its Capital Markets Day in December. | ||

|

|

|

|

|

|

SALM | |||

|

NOK |

489.80 |

+3.60% | |

|

SALM |

SalMar’s Q2 2025 results missed expectations, as weaker salmon prices—despite higher harvest volumes—caused a steep profit decline. Operational EBIT per kg fell to NOK 8.1 from NOK 30.7 a year earlier, with group operational EBIT dropping to NOK 524 million from NOK 1.38 billion. Revenue rose to NOK 6.18 billion (from NOK 5.84 billion) on harvest volumes of 64,500 tons (up from 44,800 tons), but profit before tax sank to NOK 190 million from NOK 1.48 billion, and net profit fell to NOK 146 million from NOK 900 million. EPS was NOK 1.9 versus NOK 6.3 a year ago. Performance by segment: Norway saw operational EBIT of NOK 696 million on a harvest of 54,500 tons (operational EBIT/kg: NOK 12.8). SalMar raised 2025 harvest guidance to 298,200 tons, highlighting progress in Iceland, Scotland, and offshore farming, while noting biological conditions remain challenging. The outlook was lifted based on anticipated price recovery, but immediate profitability remains pressured by oversupply and market volatility. | ||

|

|

|

|

|

|

4AJ0 | |||

|

EUR |

24.88 |

-0.48% | |

|

4AJ0 |

ALK-Abello’s Q2 2025 results materially exceeded analyst expectations, with reported organic revenue growth of 12% (DKK 1,527 million vs. DKK 1,374 million), primarily propelled by a 16% jump in tablet sales and a 56% surge in anaphylaxis (Jext®) revenue. Operating profit (EBIT) leapt 41% to DKK 375 million (from DKK 264 million), lifting the EBIT margin to 25% (from 19%) and free cash flow increased to DKK 216 million (from DKK 161 million). Growth was broad-based across Europe and North America, with international sales held back by temporary shipment phasing. Management noted excellent progress on strategic launches, including the house dust mite and tree pollen tablets for children, as well as the neffy® adrenaline nasal spray in Germany, with further launches planned.

The company raised full-year 2025 guidance, now expecting 12–14% revenue growth (up from 9–13%) and reiterating EBIT margin improvement of 5 percentage points to about 25%. CEO Peter Halling emphasized the early but promising contributions from new product launches and the U.S. pediatric sales force, underpinning confidence in sustained, profitable growth. The robust quarter was further supported by improved gross margins and ongoing cost optimization | ||

|

|

|

|

|

|

SFZN | |||

|

CHF |

86.90 |

-3.55% | |

|

SFZN |

Siegfried’s H1 2025 results came in below expectations, with net profit at CHF 65.7 million, missing consensus of CHF 72 million. Revenue was just below forecast at CHF 620 million (up 1.6% at constant rates), as Drug Products sales of CHF 206 million (consensus: CHF 212 million) weighed on both top-line and margins. Drug Substances performed in line at CHF 414 million. Adjusted EBITDA reached CHF 134 million, matching consensus, but the margin (21.6%) was flat. Net profit declined due to FX headwinds and CHF 10 million of destocking. The company maintained full-year guidance for mid-single-digit revenue growth (constant rates) and EBITDA margin above 22%, with medium-term targets unchanged. Management cited temporary weakness in Drug Products and currency effects but expects a recovery in H2 as inventory normalization and new launches support growth. | ||

|

|

|

|

|

|

KOJAMO | |||

|

EUR |

10.36 |

-4.34% | |

|

KOJAMO |

Kojamo’s Q2 2025 and H1 results showed resilient revenue but continued pressure on profitability. Q2 total revenue rose 2.9% to €115.6 million (€112.3 million), while net rental income edged up 0.9% to €82.8 million. However, pre-tax profit was €-12.7 million (€-104.3 million in Q2 2024), reflecting a €-48.0 million fair value loss on investment properties (€-33.8 million on non-yielding assets). FFO fell 9.3% to €38.8 million due to higher financial, maintenance, and repair costs. H1 revenue grew 1.9% to €229.9 million, with net rental income up 2.0% to €145.6 million. FFO for H1 was down 9.0% to €62.0 million. The financial occupancy rate improved to 93.6% (H1 2024: 91.7%), but like-for-like rental income growth remained negative (€-0.4%). In June, Kojamo agreed to sell 44 properties (1,944 apartments), to be completed after the period, with proceeds earmarked for debt reduction and buybacks. The balance sheet remains strong, with LTV at 45.7% and equity ratio at 44.3%. 2025 guidance was reiterated: revenue growth of 0–2% and FFO of €135–141 million. CEO Reima Rytsölä noted robust operational progress but a challenging rental market, especially in Helsinki, with new supply stagnation as construction remains subdued. | ||

|

|

|

|

|

|

POS | |||

|

EUR |

29.20 |

-7.45% | |

|

POS |

Porr's revenue rose 1.8% to EUR 2,959 million (H1 2024: EUR 2,908 million), EBITDA grew 3.6% to EUR 153 million, and EBIT jumped 15.5% to EUR 49 million, with the EBIT margin improving 0.2 percentage points to 1.6% - all metrics reflecting both operational leverage and disciplined cost management. Profit for the period increased 7.0% to EUR 29 million, and earnings per share climbed 17.8% to EUR 0.53. Production output edged up 1.8% to EUR 3,171 million as PORR focused on its in-house value chain, reducing external service purchases by EUR 26 million. Order intake surged 25% to EUR 4,049 million, propelling the order backlog to a record EUR 9,421 million (+10%)—a historically strong position that provides high visibility into H2 and 2026. Segmentally, Infrastructure International led growth with a 19.6% rise in production output, driven by major contracts in Romania and Poland, while building construction rebounded, especially in residential and industrial sectors. Civil engineering remains the backbone, accounting for over 60% of the order backlog. Germany saw notable gains after the reclassification of industrial and design-build activities. Outlook is unchanged: management expects moderate growth in output and revenue for 2025, with an EBIT margin target of 2.8–3.0% and is targeting 3.5–4.0% by 2030. Disciplined capital allocation and strong order momentum support confidence in continued performance | ||

|

|

|

|

|

|

BKW | |||

|

CHF |

168.70 |

-6.59% |

BKW SA release |

|

BKW |

BKW SA reported mixed first-half 2025 results, with net profit falling 44% year-on-year to CHF 203.3 million (H1 2024: CHF 361.4 million) and revenues declining 3.4% to CHF 2.25 billion—a performance below both 2024’s highs and analyst expectations, reflecting a return to more normalized energy market conditions after prior year volatility. EBIT dropped 29% to CHF 310.7 million, and the EBIT margin contracted about 500 basis points, as the company negotiated the absence of one-off Mühleberg nuclear decommissioning contributions and weaker hydro and wind generation due to unfavorable weather. Segmentally, Energy Solutions’ revenue fell 6.3% to CHF 992 million, pressured by lower electricity production, while Power Grid remained resilient (CHF 319.3 million), supported by the rollout of over 70,000 smart meters. Infrastructure & Building posted a 1% revenue gain to CHF 957.5 million, with EBIT up 26% to CHF 30.8 million on robust construction demand. Sequentially, most key metrics are down sharply from 2024, but the company expects a stronger H2 as seasonal factors in Energy Solutions and Infrastructure & Building come into play. BKW reiterated 2025 guidance for EBIT of CHF 650–750 million, forecasting stability in Power Grid and growth in infrastructure. | ||

|

|

|

|

|

|

EVD | |||

|

EUR |

82.05 |

-16.78% | |

|

EVD |

CTS Eventim’s H1 2025 revenue reached a record €1.294 billion (+7.6% year-over-year), but adjusted EBITDA slipped 0.8% to €200.5 million, broadly in line with the previous year and slightly below consensus. The adjusted EBITDA margin was 15.5% (H1 2024: 16.8%). Q2 revenue rose 0.3% to €795.6 million, with adjusted EBITDA down 8.9% to €100.2 million (margin: 12.6%). The Ticketing segment delivered robust growth, with H1 revenue up 16.1% to €415.7 million and adjusted EBITDA up 6.6% to €166.8 million (margin: 40.1%). Q2 Ticketing revenue rose 15.4% to €202.1 million, with adjusted EBITDA up 6.5% to €78.1 million (margin: 38.6%). The Live Entertainment segment grew H1 revenue 3.3% to €894.4 million, but adjusted EBITDA fell 26.1% to €33.7 million (margin: 3.8%), pressured by higher costs and integration expenses for recent acquisitions (U-Live, See Tickets). Q2 Live Entertainment revenue declined 4.5% to €602.5 million, with adjusted EBITDA down 39.7% to €22.1 million (margin: 3.7%). The company maintained its outlook, expecting continued growth and margin recovery post-integration. Management highlighted strong demand for live events, successful festivals (“Rock am Ring/Rock im Park”), and ongoing tech investments, but acknowledged cost pressures in the live segment and temporary drag from M&A | ||

|

|

|

|

|

|

SMWH | |||

|

GBp |

667.11 |

-39.90% | |

|

SMWH |

WH Smith issued a sharp profit downgrade for the fiscal year ending 31 August 2025 following an accounting error in its North American division. The company revised the North America trading profit to £25 million, down from a prior estimate of £55 million, due to premature recognition of supplier income—an overstatement totaling £30 million. As a result, group pre‑tax profit guidance has been cut to approximately £110 million, well short of analysts’ expectations around £157–183 million. The company has commissioned an independent review by Deloitte | ||

Vs. Early Hours

Versus early hours:

Indices

Versus early hours

Versus early hours

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.