Few macro data on the European side but a larger number of companies reporting notably from the Scandinavian region.

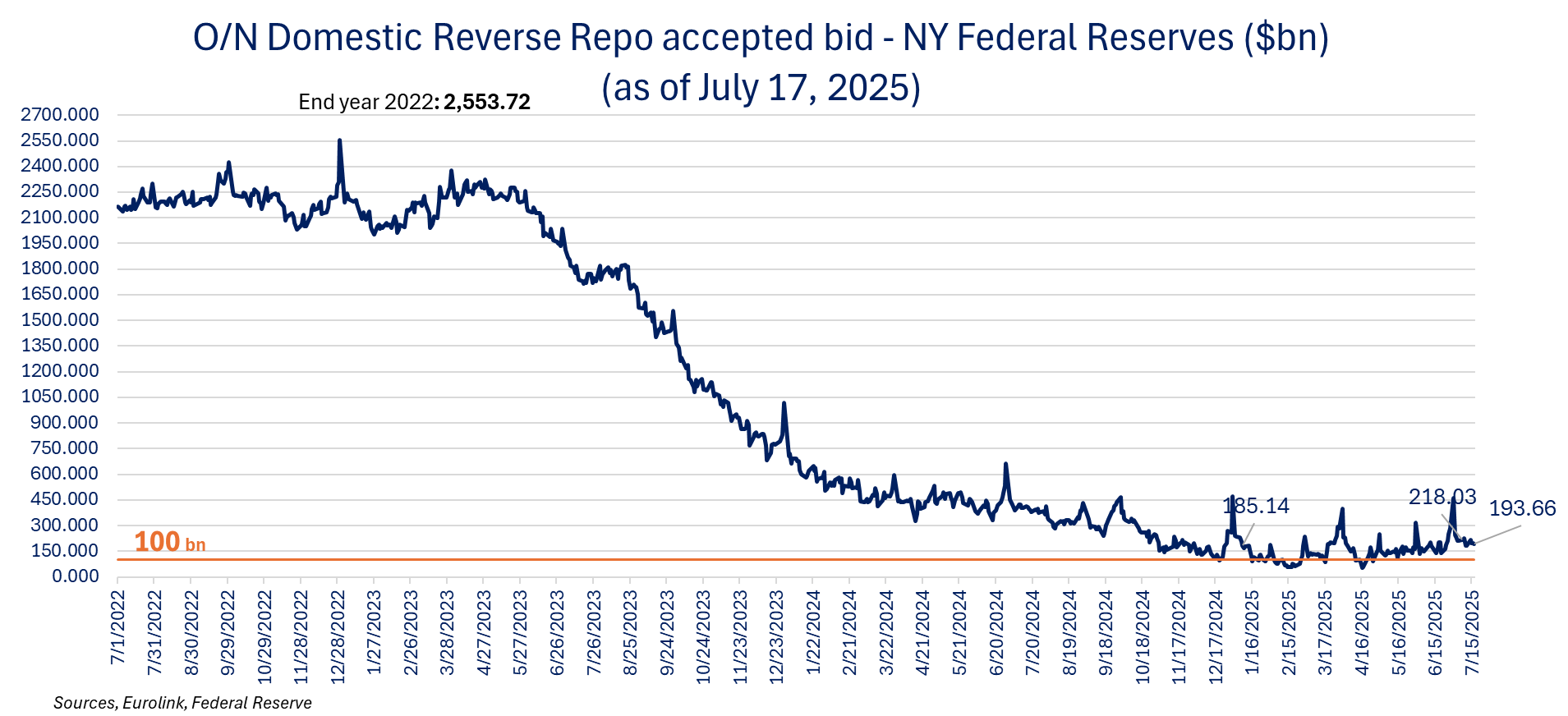

Besides tariffs, The Fed remains in focus after Waller calling again for a cut in July amid concerns about deteriorating job market while not seeing any lasting inflationary effects from tariffs. Last week Waller also made some comments on the Fed balance sheet structure, promoting the view of a much larger proportion of T-bills the Fed balance sheet to match the liabilities as the Fed maintains an “ample reserves” environment. (see comments). Autonomous factors (currency in circulation and The Treasury General Account - TGA) are the main determinants of reserves, along Reverse Repo (RR).

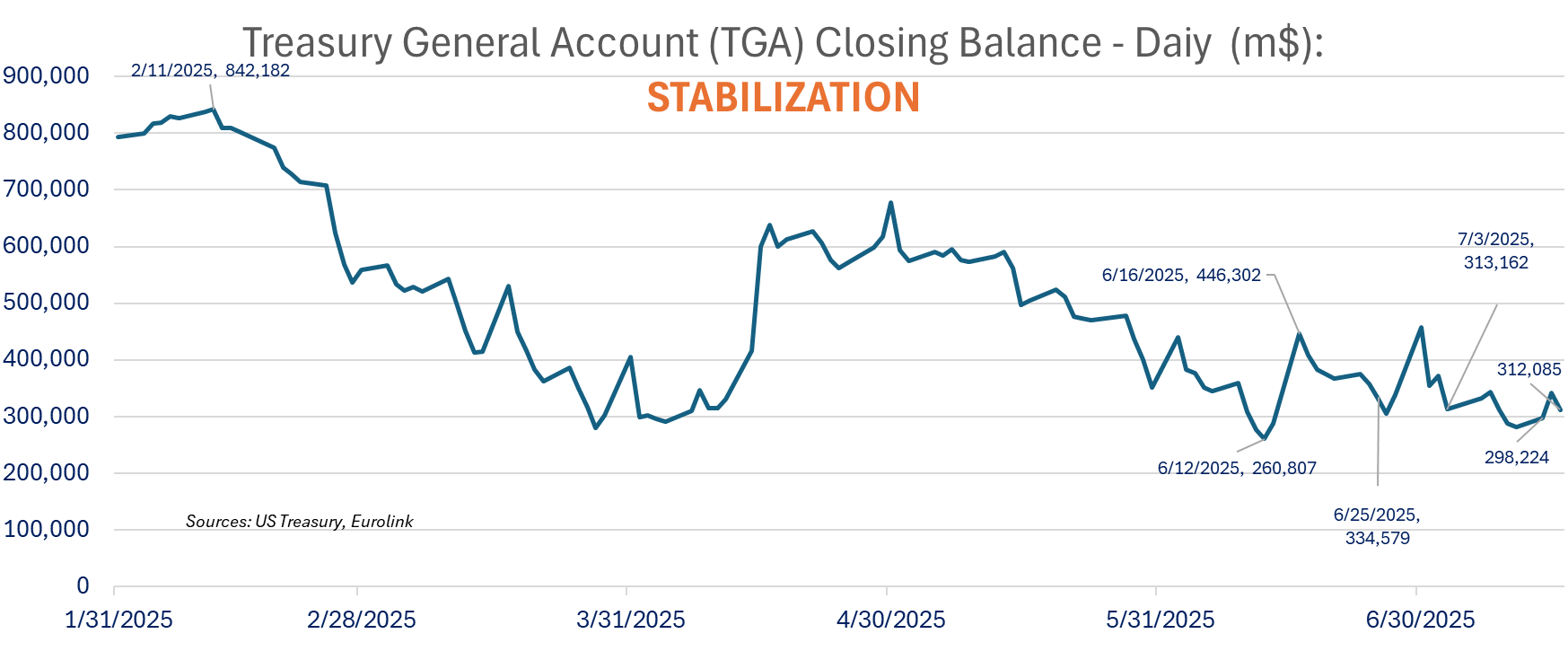

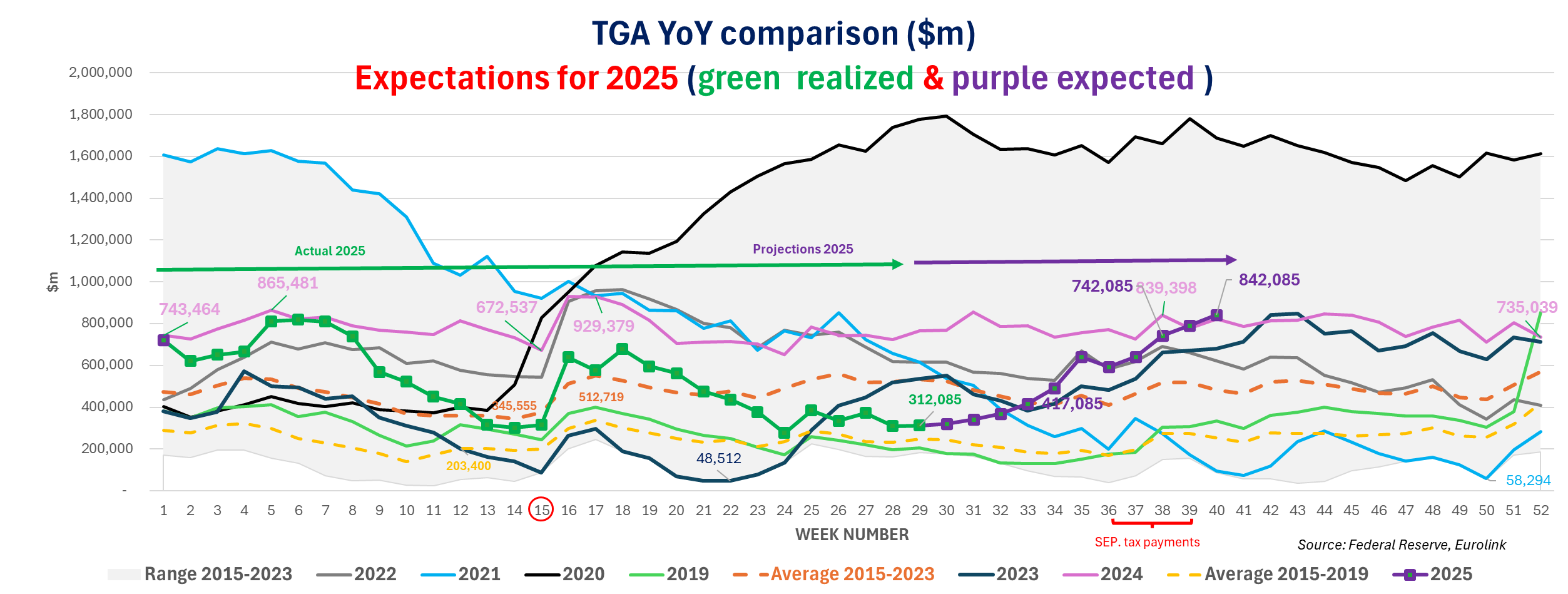

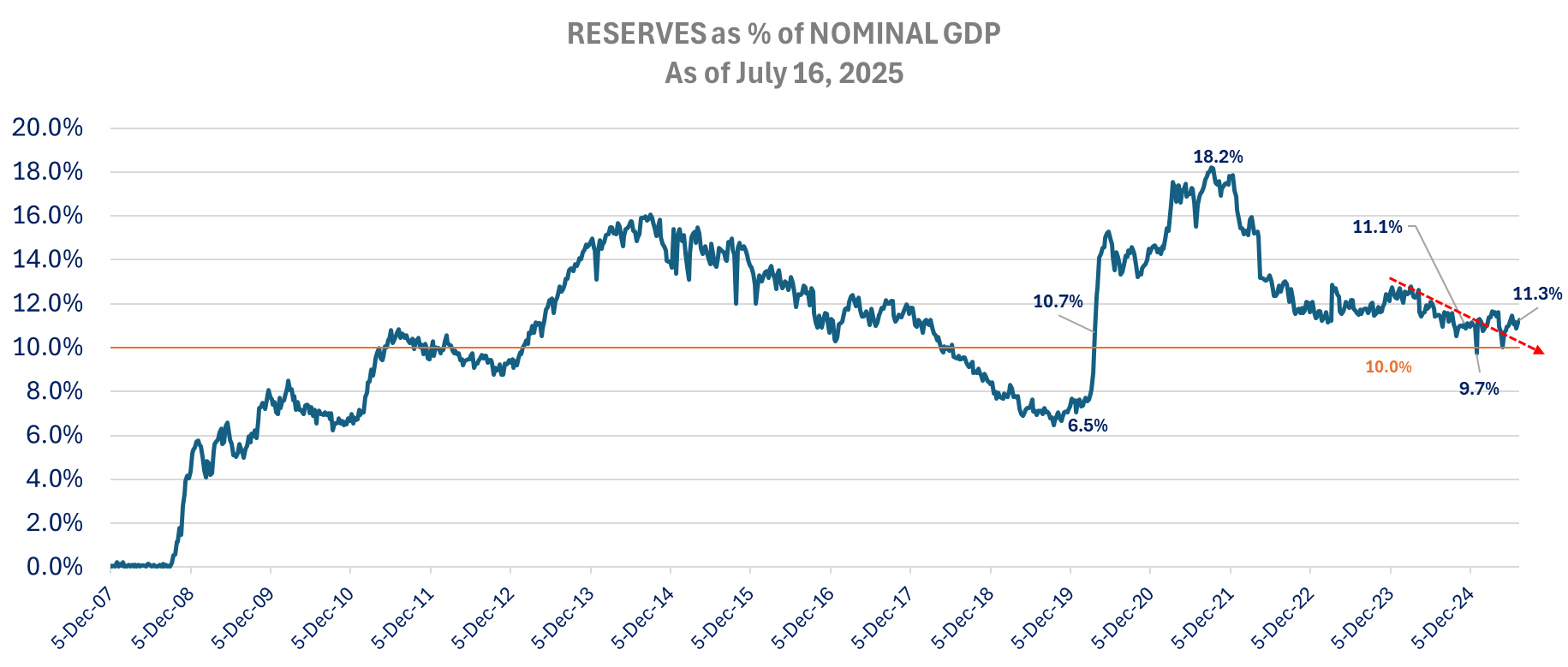

The latest Fed Balance sheet update and the Treasury report show a stabilization of the TGA at $312bn, i.e., not squeezing reserves. The domestic RR declined by -30bn adding to reserves, up +$33.04bn w/w to 11.3% of GDP. The TGA is expected to increase significantly in the coming months to ~ 850bn by the end of September (~+$540bn or ~1.8% of GDP), bringing reserves down to ~ 9.5% of GDP, level at which reserves are not so ample anymore.

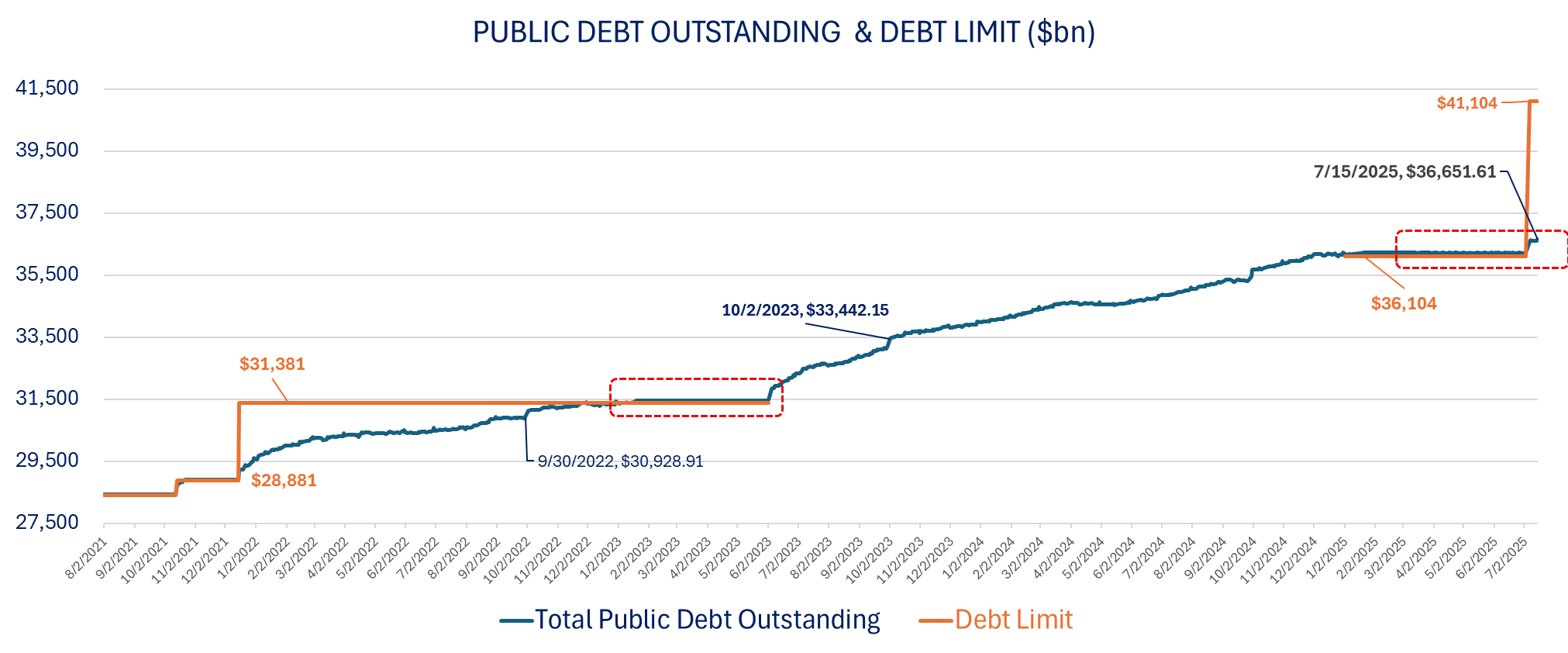

The latest data from the US treasury shows the US public debt outstanding increased by +$435.74bn already since the lifting if the debt ceiling.

Bundesbank Nagel (Reuters) insists that “Independence of central banks is the DNA of central banks” and see the discussion in the US as dangerous. The ECB independence is part of the EU treaty and will be very hard to remove. In the US congress can even if it is unlikely. Nevertheless, the constant bashing erodes the Institution of the Federal Reserve, and it will be less independent in 2026

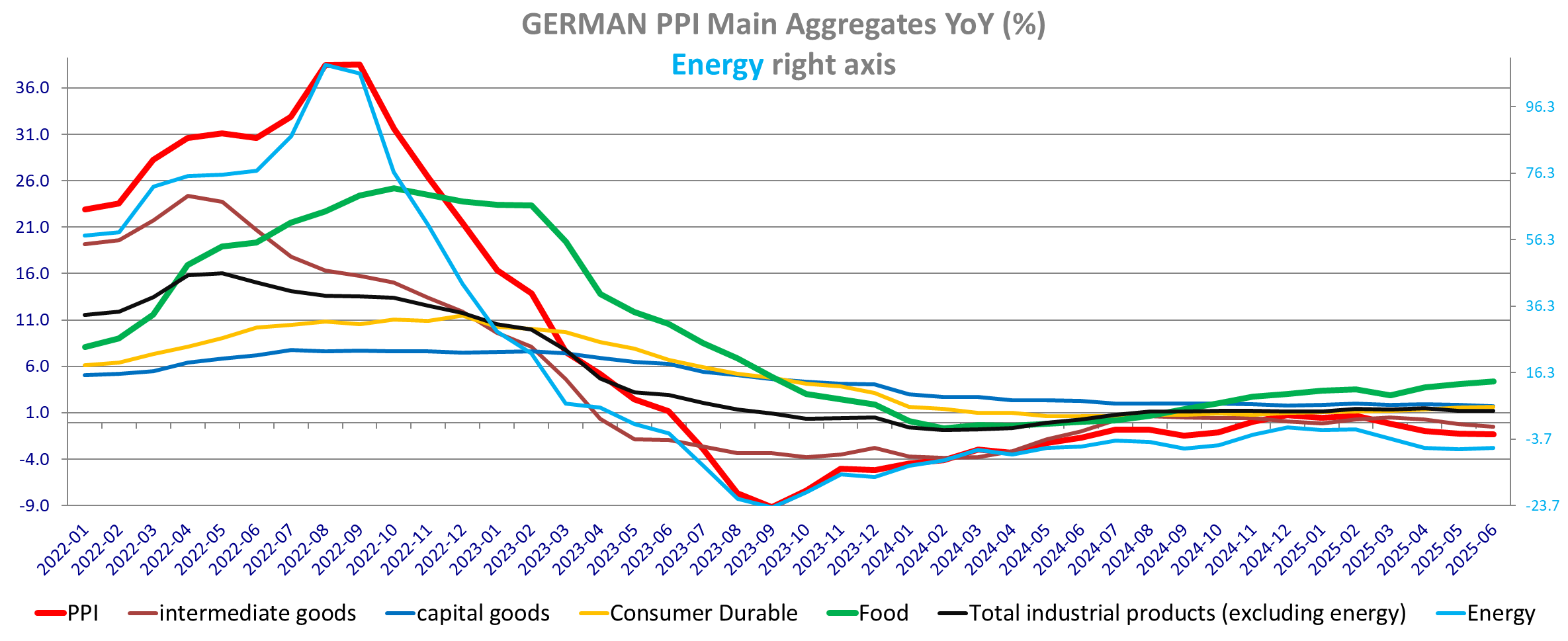

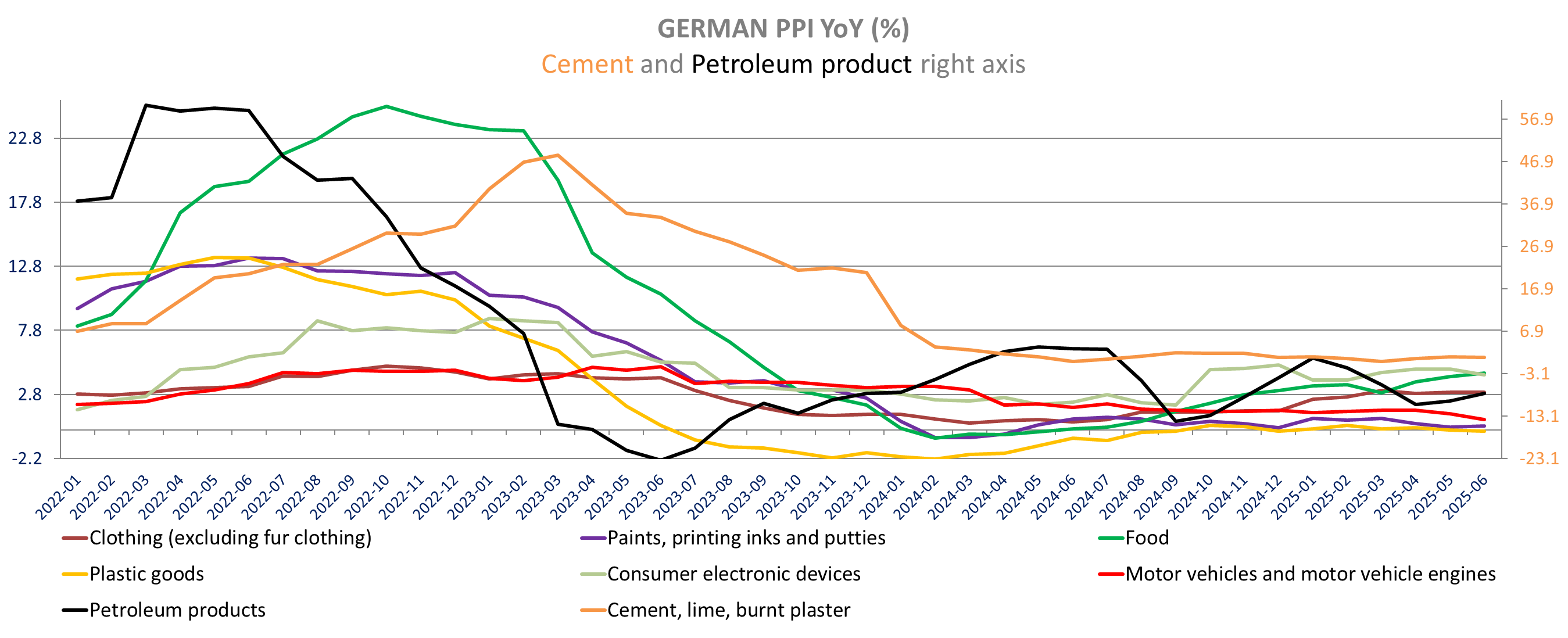

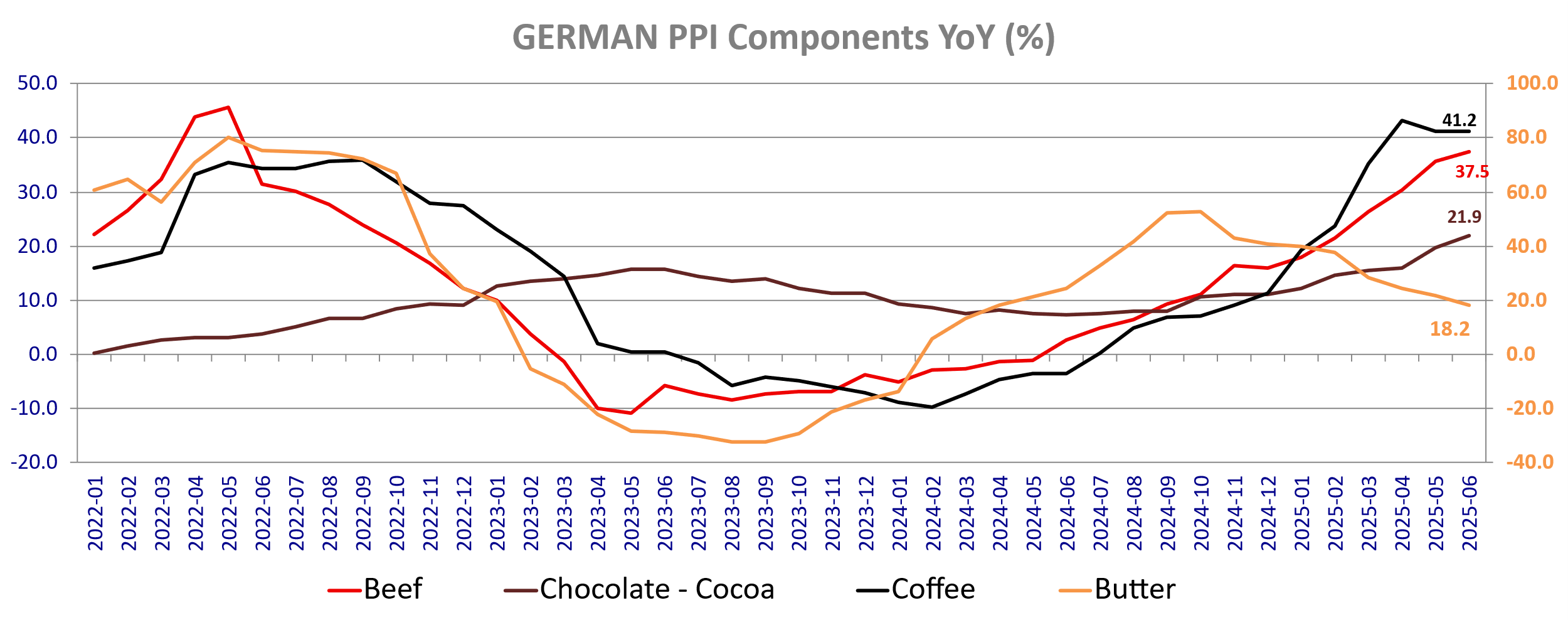

The German June PPI is at -1.3% yoy down from -1.2% yoy in May, in line with expectations and the lowest since September of last year. The decline in mainly due to energy and intermediate goods. The PPI for industrial goods excluding energy is unchanged at +1.3% yoy (+0.1% m/m). We note higher food PPI with as seen in the CPI data, further increase in Beef inflation Chocolate but also for poultry and High coffee, Juice inflation… Capital Goods inflation is lower at 1.7% yoy down from 1.9%.

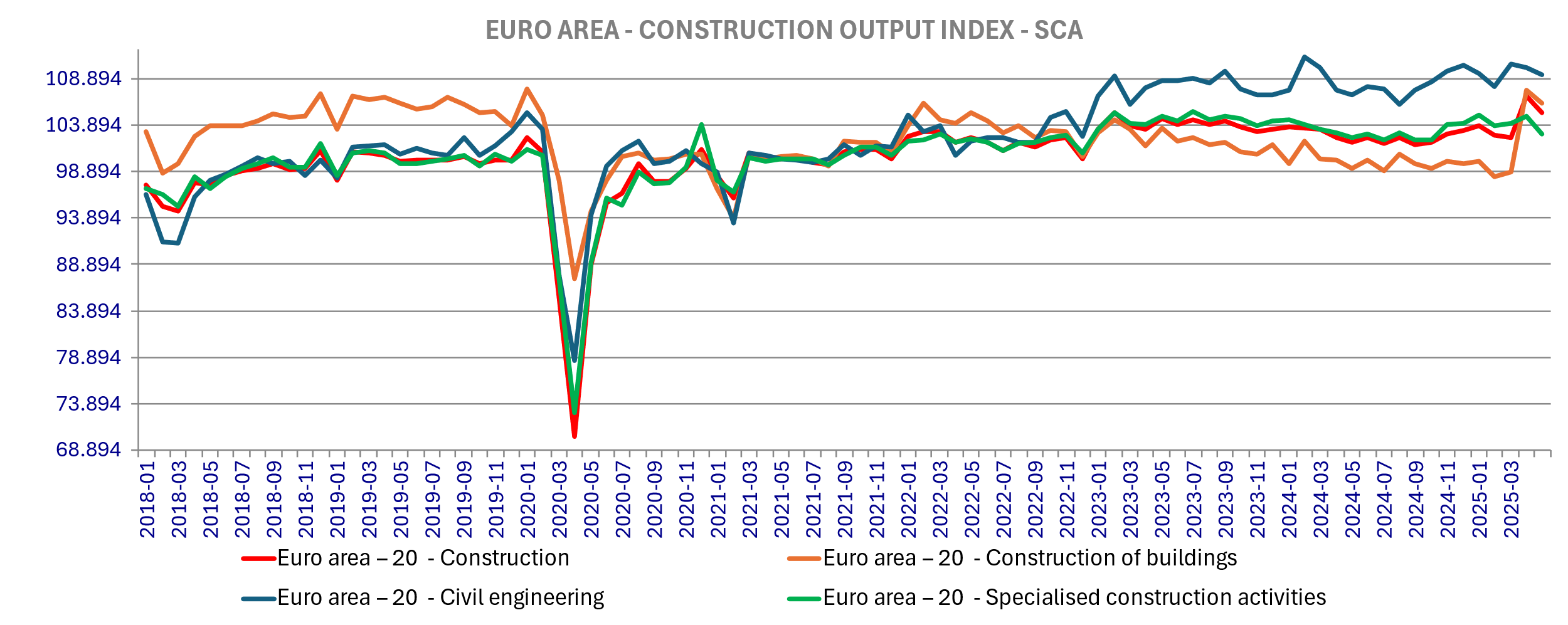

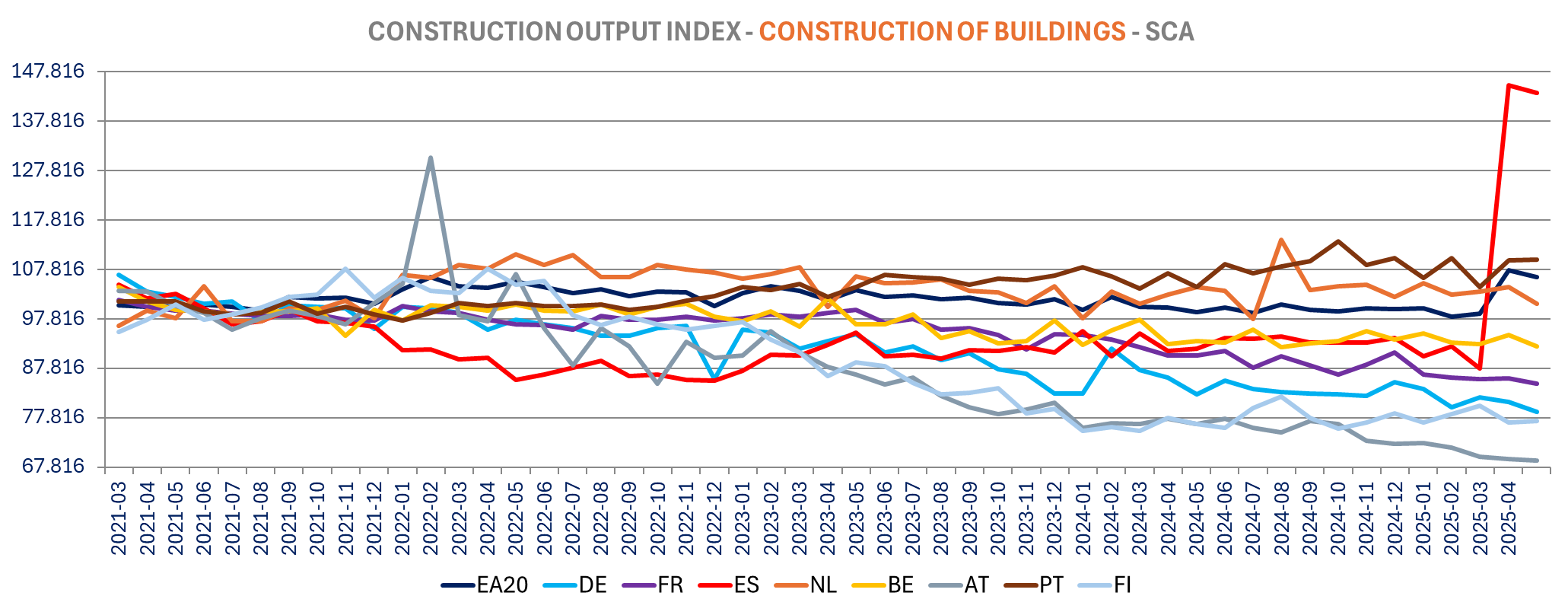

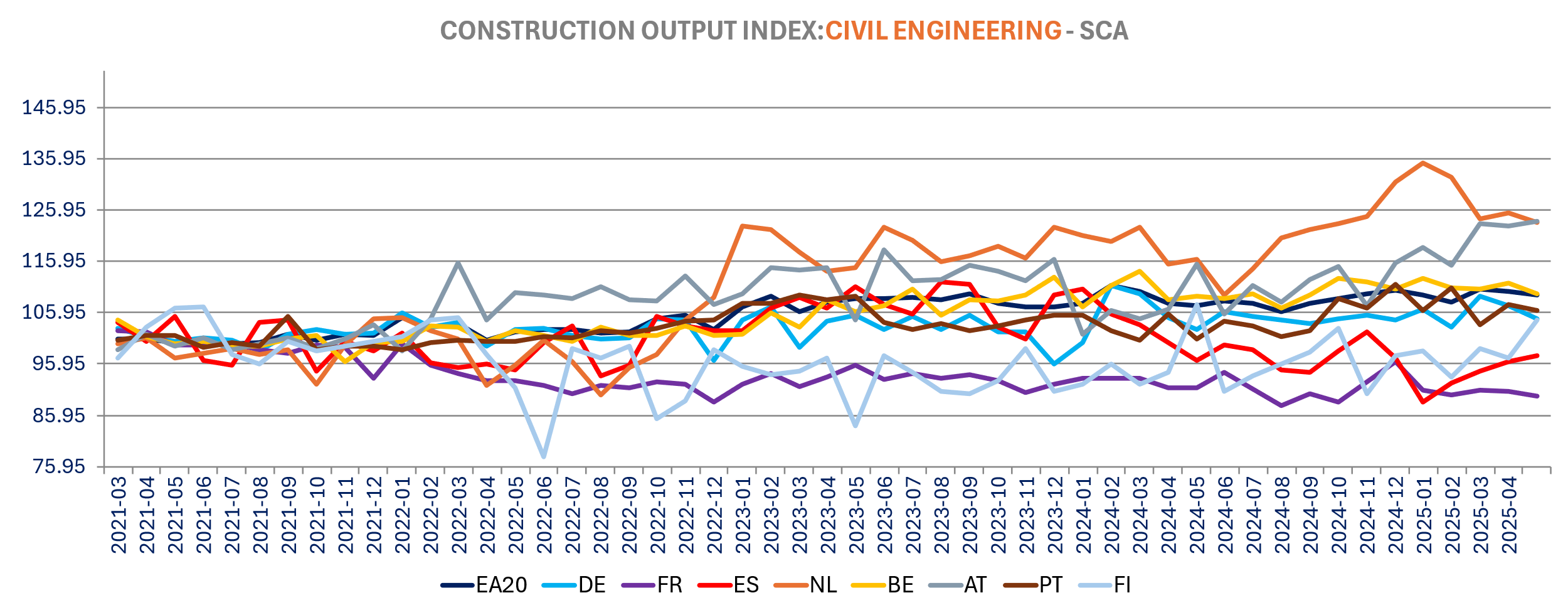

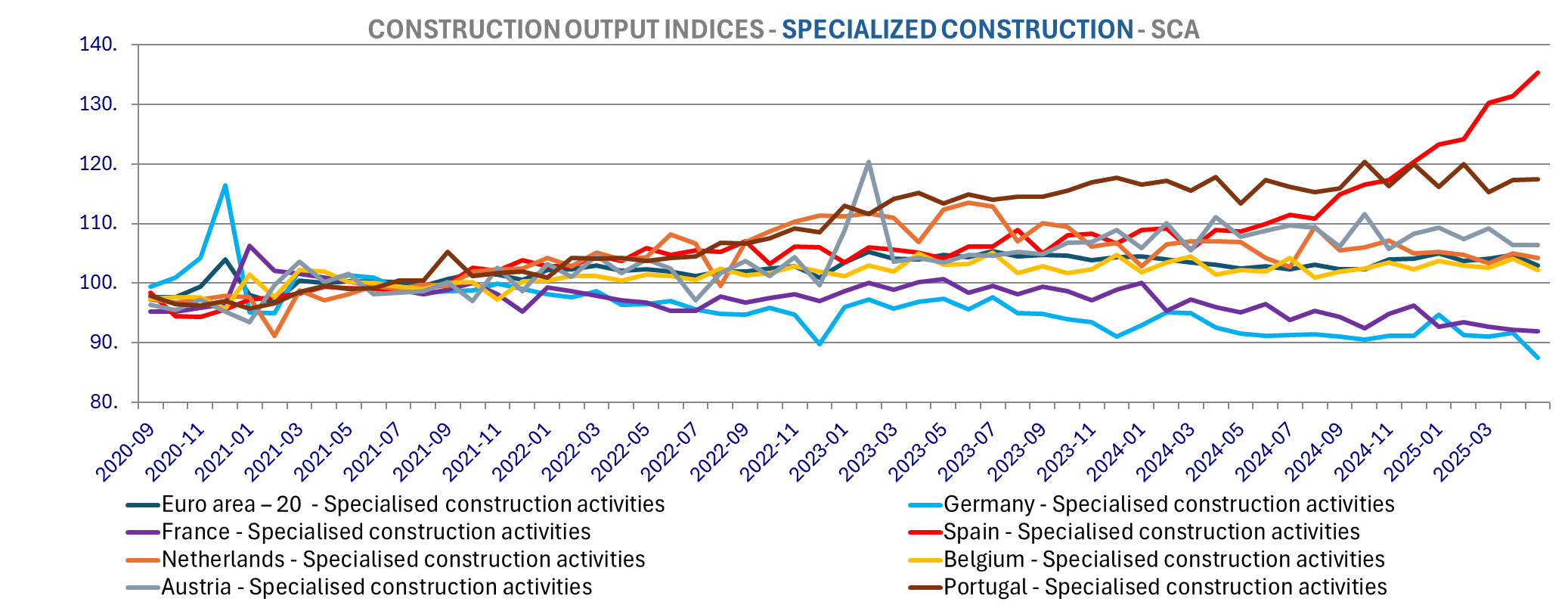

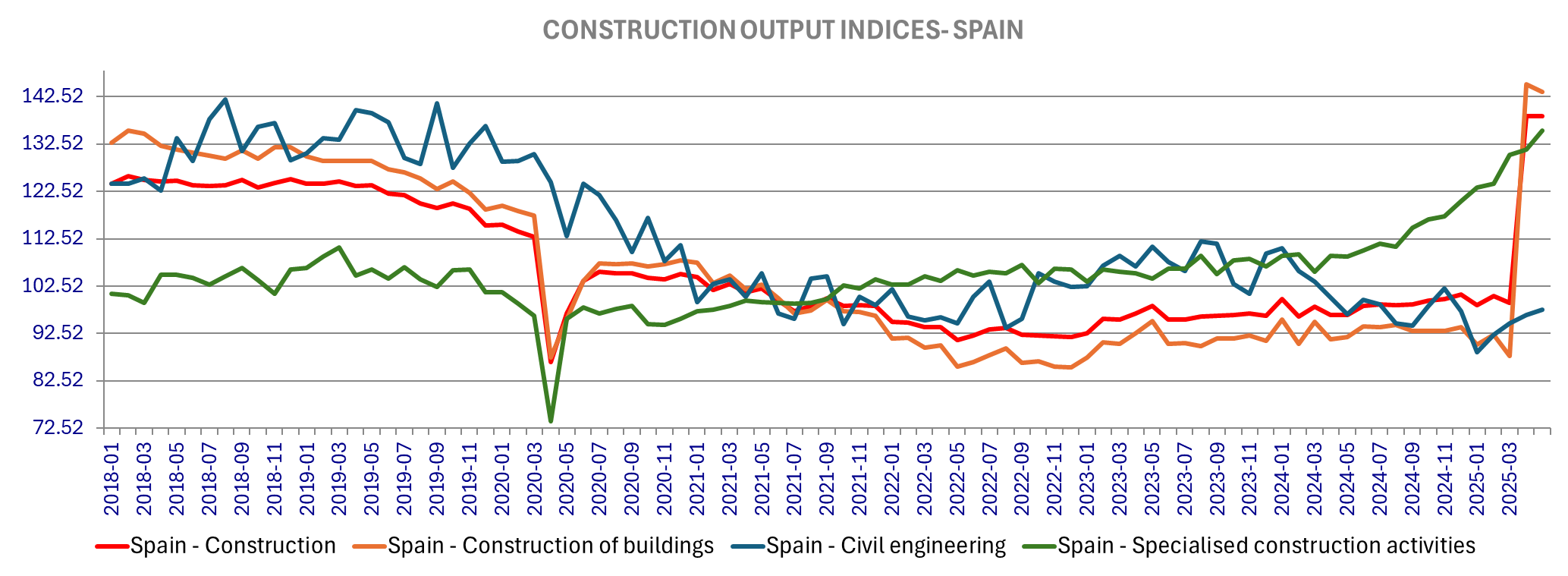

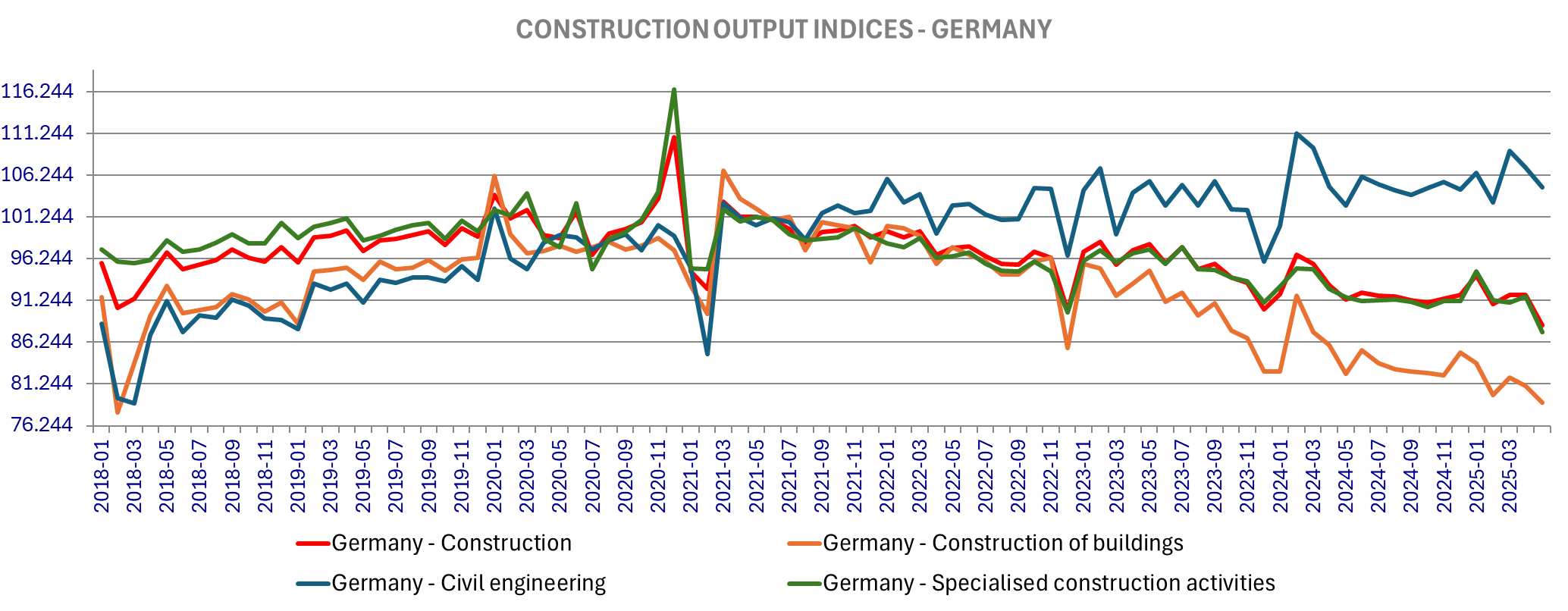

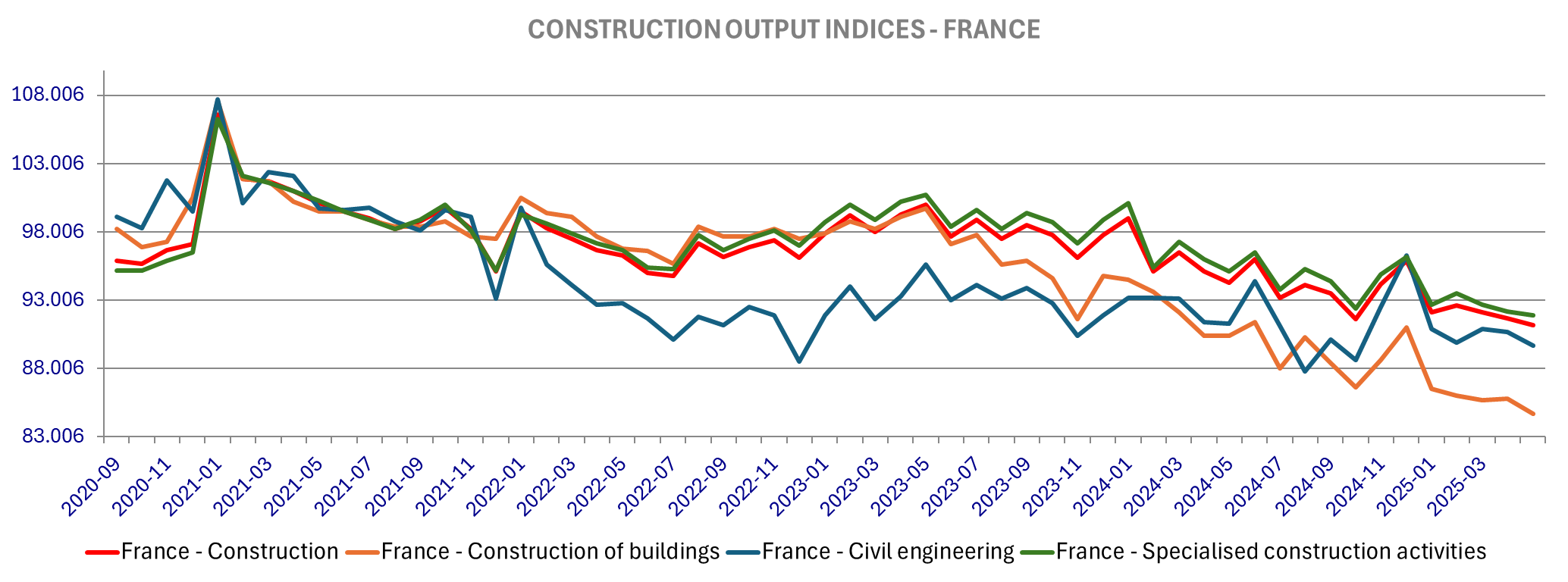

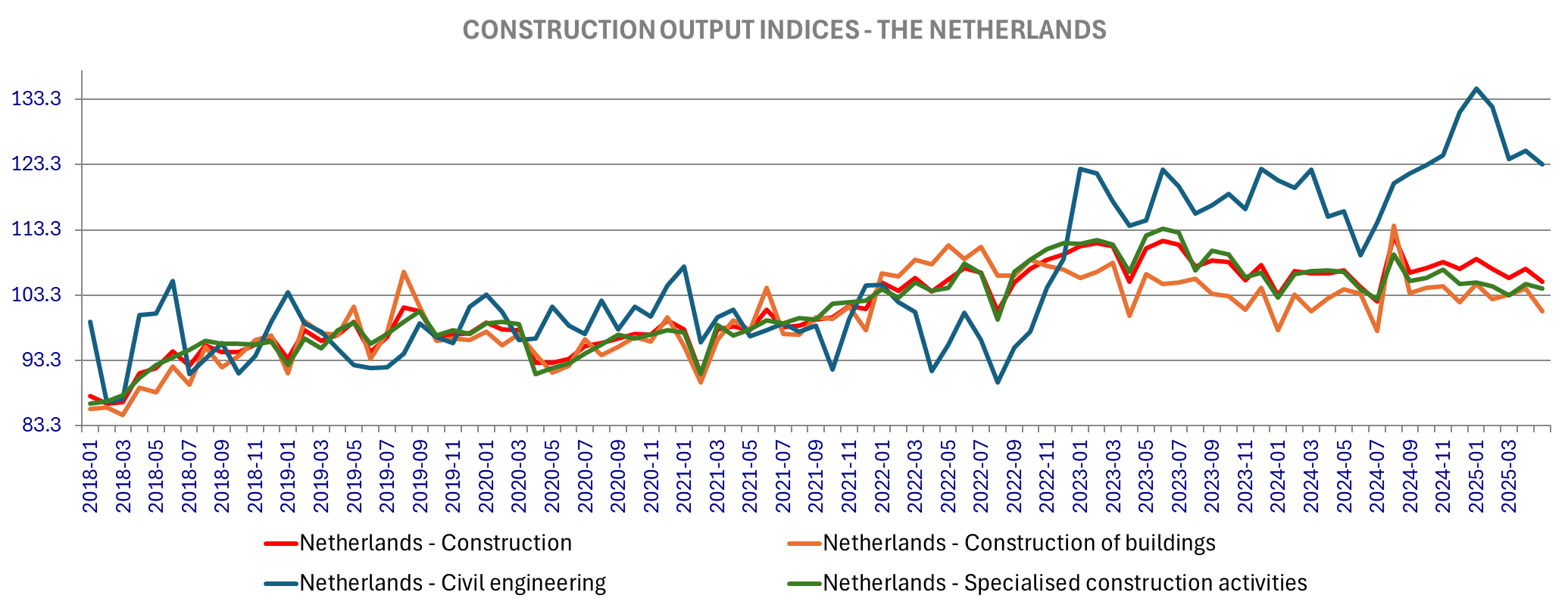

The Eurozone construction Output was down -1.7% m/m in May after +4.3% m/m in April but with massive revision from +1.7% m/m reported for April initially. The revision is mainly from Building construction (8.9% vs 0.9% initially) and principally due to Spain. Spain April output is up 39.8% m/m now revised from 4.3%(!) with Building construction up 65.3% revised from +7.4%(!!)... Eurostat is not giving any more explanation. Year over year construction is up 2.9%yoy down from 4.7% yoy in April (revised from 3%), with Spain up 44.6% (47.6% in April revised from 14.7%!), Portugal up +5.4% yoy (0.4% yoy in April), Italy +3.9% yoy (down from 6.5%) and Finland up 3% (4.4% yoy in April). Germany construction production is down -3.4% yoy, France -3.3% yoy, the worst performing countries.

European Bond Yields bounce back to 3.23% for German 30yr and steeper curves. Yields are lower in Japan (1.53% 10yr) ahead of the elections, after a somewhat better inflation number (3.3% down from 3.5% lowest in 7 months; Core at 3.3% in line with expectations).

On the companies’ front: After reporting strong second quarter results, SAAB raised its full year outlook and expects EBIT to improve faster than sales, citing the persistence of elevated European defense budgets and sustained order flow. Vivendi shares surged as much as 12.5% today after France’s financial regulator, the AMF, mandated that majority shareholder Vincent Bolloré and his holding company launch a public buyout offer for minority shareholders. Despite a drag from tariffs and adverse currencies, Getinge’s margins strengthened by disciplined pricing and productivity gains across divisions. Burberry’s Q1 comparable retail sales fell just 1 % in the three months to June 28— better than the 6 % drop last quarter and ahead of analyst forecasts of a 3 % decline. Telia’s second‑quarter results, published today, delivered better than expected profitability even as revenue growth slowed, thanks to operational efficiency. Wartsila reported strong demand, particularly across its Marine and Energy Storage segments driven by a record-setting US datacenter contract and robust thermal power and marine orders, resulting in an all-time high order book. Electrolux missed profitability expectation as the turnaround in North America was offset be a weak demand in Europe. Atlas Copco missed expectations, as the group faced softness in compressors, especially gas and process units, while vacuum orders were broadly flat and service lines showed resilience. Epiroc’s good demand from mining customers was offset by significant currency headwinds and continued weakness in construction. GSK shares fell today after a U.S. FDA advisory panel recommended against re-approving its blood cancer therapy Blenrep. More details on equities here

EU BUDGET TROUBLE

The latest Fed balance sheet update shows only a small decline in total assets, down -$2.64bn week-over week (-$2.07bn w/w decline in securities held outright with a slight increase in T-bills) as of Wednesday July 16.

The larger change were on the liabilities side, with a -$35bn decline in Reverse Repo to $574.7bn (-$4.9bn foreign official to $377.6bn and -$30.2bn to $197.1bn for the domestic side).

Week over week the Treasury General Account (TGA) stabilized at $312.1bn up just +$1.04bn w/w i.e. not yet squeezing reserves. Reserves are up +$33.04bn w/w to 11.3% of GDP. The TGA is expected to rise to ~$850bn in Sep-Oct.

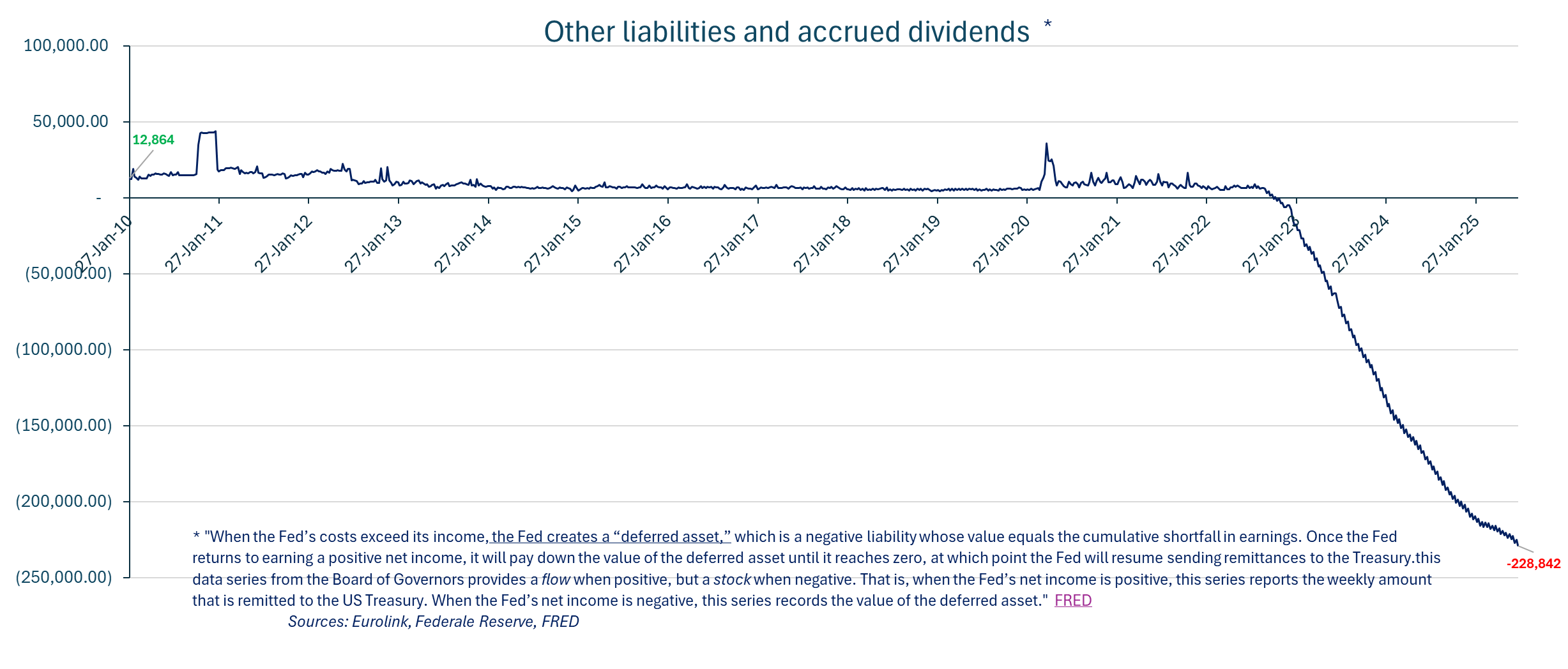

The Federal Reserve loss (negative other liabilities and accrued interest) increased by another $3.78bn to -$228.8bn .

The latest US treasury statement also shows the US total public debt outstanding increased by +$435.74bn already since the lifting if the debt ceiling to $41.1tn from $36.1tn to $36,651.6bn (including debt not subject to the statutory limit)

TGA stabilization before expected to increase sharply

The German June PPI is down to -1.3% yoy down from -1.2% yoy in May, in line with expectations. Producer prices are up 0.1% m/m above the 0% expected, up for the first time in seven months.

It is the Lowest annual rate of producer price inflation since September of last year. Destatis Release

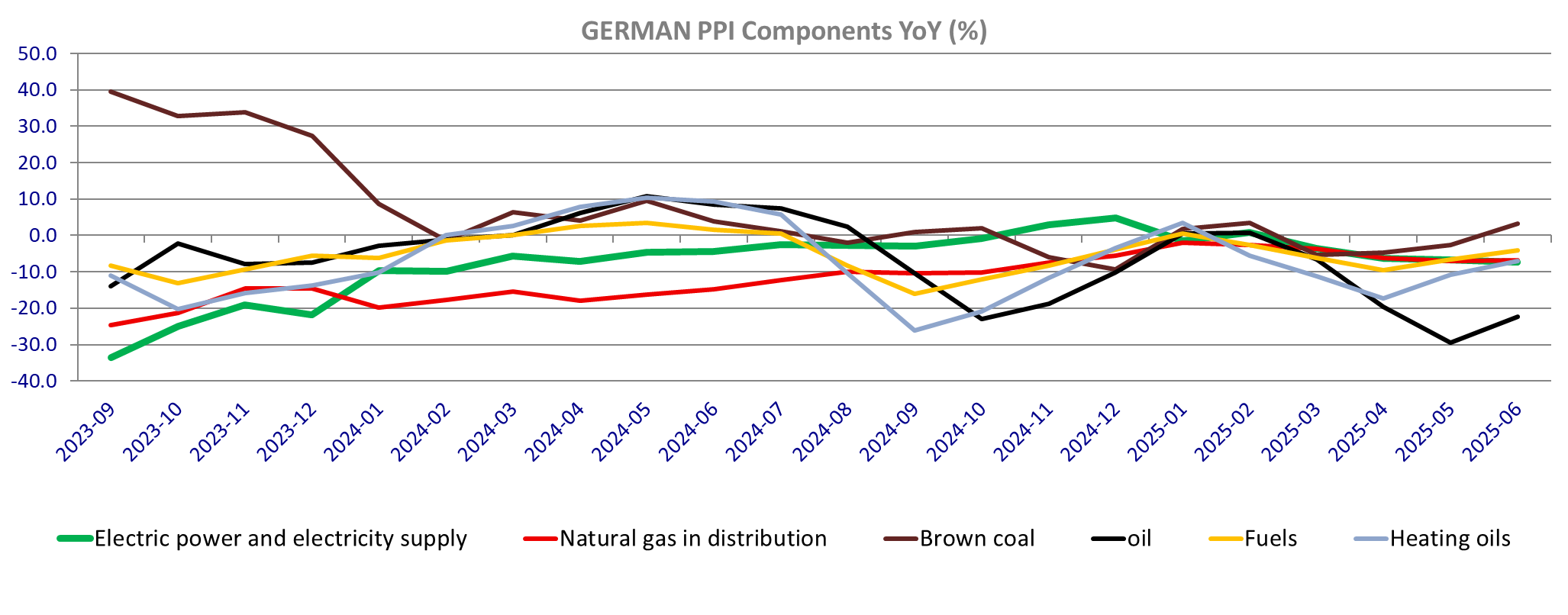

The decline in the PPI is due to lower energy production prices, down -6.4% yoy (a slight improvement from -6.7% yoy in May) and intermediate goods (-0.4% yoy vs -0.2% yoy in May, down -0.2% m/m). Motor fuel PPI inflation is higher in June at -4.2%, yoy from -6.5% yoy in May, up +1.2% m/m. Natural gas (in distribution) inflation is slightly higher as well at -6.9% vs -7.1% yoy in May, but electricity power and supply PPI is lower at -7.3% yoy from -6.8% yoy in May.

The PPI for industrial goods excluding energy is unchanged at +1.3% yoy (+0.1% m/m).

EUROZONE CONSTRUCTION OUTPUT (May)

Eurostat published the May European construction output. The Eurozone construction output is down -1.7% m/m in May after +4.3% m/m in April, revised sharply from +1.7% m/m.

The revision is mainly from Building construction (8.9% vs 0.9% initially) and principally due to Spain. Spain April output is up 39.8% m/m now revised from 4.3%(!) with Building construction up 65.3% revised from +7.4%(!!)... Eurostat is not giving any details.

In May we saw decline in all categories at the Eurozone level -1.7%m/m for specialty construction, -1.3% for construction of building and -0.7% for civil engineering.

Germany (-3.9% m/m after being flat m/m in April), Belgium (-2.2%m/m after +1.6% in April) and the Netherlands (-1.8% following +1.3% in April) posted the largest monthly decline. Construction also declined in France (-0.5% m/m, after -0.4% m/m in April), Italy (-1.4% but following +2.8% m/min April), Portugal (-0.1% after +3.6% in April) and increased only in Finland (+0.9% after -1.1% in April) and Spain (+0.1%).

All three sectors (Building construction, Civil engineering and specialized construction) are down in all countries with just few exceptions: civil engineering up 7.5% m/m in Finland, 1.1% in Spain, 0.7% in Austria, and Specialized construction up 3%m/m in Spain, 0.1% in Spain. Building construction is marginally up only in Portugal (0.1%) and Finland (0.4%).

Year over year construction is up 2.9%yoy down from 4.7% yoy in April (revised from 3%), with Spain up 44.6% (47.6% in April revised from 14.7%), Portugal up +5.4% yoy (0.4% yoy in April), Italy +3.9% yoy (down from 6.5%) and Finland up 3% (4.4% yoy in April). Germany construction production is down -3.4% yoy, France -3.3% yoy, the worst performing countries. %)

|

|

Friday, July 18, 2025 | ||

|

SAAB B | |||

|

SEK |

560.30 |

+16.66% | |

|

SAAB B |

Saab AB reported a surge in second-quarter results that decisively beat market expectations, reflecting robust growth fueled by strong European defense spending. The Swedish defense and security group posted an operating profit of 1.98 billion Swedish kronor (approximately $200 million), representing a 49% year-on-year increase and comfortably surpassing analyst forecasts. Quarterly revenues jumped 30% to SEK 19.8 billion, underpinned by exceptional performance in the Dynamics and Surveillance divisions, which benefited from a spike in deliveries and project activity. Organic sales growth hit 32%, with all business units contributing positively, and net income soared by 53% to SEK 1.54 billion, as earnings per share rose to SEK 2.83 from SEK 1.85 a year ago. Despite operational cash flow remaining negative due to continued investments in capacity expansion, Saab solidified its net liquidity position and raised its full-year outlook, now targeting 16–20% organic sales growth versus a previous 12–16% forecast. The company expects EBIT to improve faster than sales, citing the persistence of elevated European defense budgets and sustained order flow. | ||

|

|

|

|

|

|

VIV | |||

|

EUR |

3.32 |

+12.81% | |

|

VIV |

Vivendi shares surged as much as 12.5% today after France’s financial regulator, the AMF, mandated that majority shareholder Vincent Bolloré and his holding company launch a public buyout offer for minority shareholders. This requirement follows the completion of Vivendi’s breakup into separate listed entities and a Paris Court of Appeal ruling, with the regulator determining Bolloré’s control triggered an obligation to protect minority investors. The AMF’s move compels Bolloré to acquire all remaining outstanding shares, setting the stage for a potential delisting of Vivendi from the stock exchange. | ||

|

|

|

|

|

|

VENDA |

Vend Marketplaces ASA | ||

|

NOK |

398.00 |

+10.43% | |

|

VENDA |

The Nordic marketplace operator reported group revenues of NOK 1,694 million—a 2% drop year-on-year on a constant currency basis—while EBITDA surged by 25% to NOK 583 million (consensus NOK508.5), lifting the margin to 34% (27.2%). The earnings growth reflected both strengthened average revenue per ad and disciplined cost reductions, as Vend accelerated divestments from non-core activities and ventures. Segment performance diverged: the Mobility and Real Estate divisions posted solid revenue growth, propelled by ARPA gains and transactional volume, whereas Jobs and ReCommerce saw revenue declines due to market exits and streamlining measures. Despite persistent pressure on advertising revenue and expectations for continued sluggish volume trends in the near term, Vend maintained its medium-term financial targets and underscored its commitment to shareholder returns, highlighted by a NOK 4.6 billion share buyback and a NOK 500 million special dividend following a notable capital distribution from its Adevinta stake. | ||

|

|

|

|

|

|

GETI B | |||

|

SEK |

203.30 |

+7.34% | |

|

GETI B |

Getinge’s Q2 2025 interim results. Organic net sales rising 4.1 % to SEK 8.24 billion and order intake up 4.4 %, both modestly ahead of analyst expectations; adjusted EBITA of SEK 989 million also exceeded forecasts (~SEK 905 million) despite a SEK 270 million drag from tariffs and adverse currencies, with margins notably strengthened by disciplined pricing and productivity gains across divisions The Surgical Workflows and Digital Health segments delivered particularly margin expansion supported by product mix improvements, while Acute Care Therapies and Life Science continued to benefit from robust demand for ventilators, sterile transfer solutions and the newly integrated Paragonix business, which contributed to EBITA ahead of projections. Free cash flow strengthened to SEK 510 million, reinforcing balance‑sheet resilience, and management maintained full‑year guidance of 2–5 % organic growth while signaling upside to EBITA consensus and affirming long‑term targets amidst geopolitical and FX risks. | ||

|

|

|

|

|

|

ORNBV |

Orion Oyj | ||

|

EUR |

69.20 |

+4.77% | |

|

ORNBV |

H1 net sales rose by 26.9 % to €416.5 million and operating profit by 58.9 % to €104.6 million, well above analyst consensus of around €94 million, driving operating margin to an 25.1 % compared to 20.0 % a year earlier. The growth momentum was fueled primarily by the Innovative Medicines segment—led by blockbuster Nubeqa®—which more than doubled sales to approximately €140 million, lifting segment performance by over 83 % in the quarter.. Operating cash flow per share nearly tripled, highlighting strong cash conversion and operational efficiency. Management reiterated full-year guidance of €1.63–1.73 billion in sales and €400–500 million in operating profit. | ||

|

|

|

|

|

|

BRBY | |||

|

GBp |

1317.00 |

+5.53% | |

|

BRBY |

Burberry’s Q1 comparable retail sales fell just 1 % in the three months to June 28— better than the 6 % drop last quarter and ahead of analyst forecasts of a 3 % decline. Retail revenue slipped 6 % to £433 million, weighed down by a 4 % currency drag, yet core markets such as the Americas (+4 %) and EMEIA (+1 %) showed sequential strength, even as Greater China and Asia Pacific remained subdued. CEO Joshua Schulman cited greater brand desirability and strong reception of the new Autumn 2025 collection as key positives, alongside ongoing traction in core outerwear and scarf categories. Enhanced marketing campaigns, improvements in in-store presentation, and rising online sales for the third consecutive quarter also supported sentiment. | ||

|

|

|

|

|

|

TELIA | |||

|

SEK |

34.80 |

+4.29% |

Telia Company AB release |

|

TELIA |

Telia’s second‑quarter results, published today, delivered better than expected profitability even as revenue growth slowed, thanks to operational efficiency. Service revenue rose roughly 1–1.2 % year‑on‑year to SEK 19.8 billion, just under consensus, while adjusted EBITDA climbed around 6.2 %–6.4 % to approximately SEK 7.97 billion—higher than analyst expectations of SEK 7.84 billion—driving a margin expansion to roughly 40.3 % . Operating income increased to circa SEK 3.35 billion, although net income from continued operations rose to around SEK 2.17 billion (SEK 0.50 per share), down overall due to the prior year’s Danish divestment hangover | ||

|

|

|

|

|

|

SKF B |

SKF Inc | ||

|

SEK |

235.80 |

+4.06% | |

|

SKF B |

SKF reported resilient second-quarter results, achieving an adjusted operating margin of 13.3%—up from 13.0% a year earlier—despite ongoing macroeconomic headwinds and a negative currency impact. Net sales dropped 9.5% year-over-year to SEK 23.2 billion, while organic growth was flat at -0.2%, as strength in the Industrial segment, which posted a 16.6% margin, was offset by persistently weak demand in Automotive except for electric vehicles. Aerospace stood out with 12% annual sales growth and an 8-point margin improvement since 2022. The quarter saw strong cash generation, with net cash flow from operations up 31% to SEK 2.8 billion, fueled by improvements in working capital. The company announced a significant restructuring plan involving 1,700 job cuts, mainly in Europe, targeting SEK 2 billion in annual savings by 2027. Net profit, however, dropped sharply to SEK 583 million from SEK 1.66 billion last year, mainly due to currency headwinds and higher restructuring costs. Management credited pricing actions, cost discipline, and automation investments for the sustained margin performance and anticipates stable organic sales in the coming quarter as end-market conditions remain mixed | ||

|

|

|

|

|

|

WRT1V | |||

|

EUR |

22.25 |

+3.06% | |

|

WRT1V |

Wärtsilä reported a standout second quarter, surpassing market expectations with adjusted operating profit of €207 million—up 18% year-on-year and 8% above analyst estimates—and an adjusted operating margin reaching 12.0%, its highest in recent years. Net sales rose 10.5% to €1,719 million, with organic growth accelerating to 13%, underscoring strong demand, particularly across its Marine and Energy Storage segments. Order intake soared 18% to €2,190 million—20% above consensus—driven by a record-setting US datacenter contract and robust thermal power and marine orders, resulting in an all-time high order book. Services also performed well, with service agreement order intake up 48% and net sales up 9%. Profit before tax and net profit registered solid gains, while earnings per share climbed 15% to €0.23. Cash flow from operating activities nearly doubled year-on-year to €416 million. Looking forward, management remains optimistic about demand in Marine and Energy Storage over the next year but has moderated its outlook for the Energy segment to stable levels, citing geopolitical and tariff risks as potential headwinds. | ||

|

|

|

|

|

|

TELo |

Telenor ASA | ||

|

NOK |

162.60 |

+1.63% | |

|

TELo |

Telenor delivered good second-quarter results, prompting an upward revision to its 2025 earnings guidance after robust Nordic performance and continued momentum in key markets. The company reported service revenues of NOK 16.5 billion and adjusted EBITDA of NOK 9.3 billion, with organic service revenue up 2.9% and adjusted EBITDA increasing 8.3% year-on-year, outpacing expectations. A standout contribution came from Norway, which recorded 3.7% growth in service revenues and a 16.1% jump in adjusted EBITDA, supported by successful network partnerships and expanded fiber operations. Across the Nordics, service revenue rose by 3.7%, reflecting resilience in core offerings like network coverage, security, and cloud connectivity. Telenor also recorded a robust 15% service revenue growth in Pakistan and stable performance in Bangladesh via Grameenphone. The operator raised its full-year group EBITDA growth outlook to a mid-single-digit range and now targets high-single-digit EBITDA growth in the Nordics, up from earlier forecasts. Free cash flow before M&A reached NOK 1.6 billion for the quarter, supporting future capital deployment. | ||

|

|

|

|

|

|

BEIJ B |

Beijer Ref AB (publ) | ||

|

SEK |

160.40 |

+1.58% | |

|

BEIJ B |

Beijer Ref reported a highest-ever EBITA margin at 12.2%, with EBITA rising 7.9% year-on-year to SEK 1,238 million and beating market consensus by 4%. Revenues grew 5.2% to SEK 10,181 million, in line with expectations, while organic sales growth reached 2.0%. Regional highlights included robust performance in EMEA, where sales climbed 12.6% and margins improved, while North America and APAC managed steady or slightly positive organic growth despite year-on-year sales declines in those areas. The company also cited double-digit growth in digital sales and further expansion of its e-commerce platform in the US. Good operating cash flow, up from SEK 350 million last year to SEK 614 million, underlined tight working capital management and seasonal demand. CEO Christopher Norbye attributed the strong showing to strategic initiatives and positive foreign exchange effects, noting Beijer Ref’s continued growth trajectory despite currency headwinds and a challenging market backdrop. | ||

|

|

|

|

|

|

HUSQ B |

Husqvarna AB | ||

|

SEK |

53.32 |

+0.68% | |

|

HUSQ B |

Husqvarna reported good underlying performance in the second quarter of 2025, with organic sales growing 5% year-on-year despite headline net sales slipping 1% to SEK 15,277 million due to significant currency headwinds, which reduced sales by 6%. Operating profit rose by 8.6% to SEK 2.06 billion, beating analyst expectations, as cost-saving initiatives and operational efficiencies lifted the operating margin to 13.5% from 12.3% a year ago. The strong quarter was driven by robust demand for robotic lawnmowers—which saw a 15 % increase in sales—and garden irrigation products across Europe, bolstered by favorable spring weather, although North America remained softer. Margin expansion was underpinned by cost efficiencies, greater volumes, and a strategic pivot toward higher‑margin offerings. Management also disclosed a proactive supply‐chain overhaul in response to rising U.S. tariffs, including shifting production from China to Europe and rerouting Canada‐bound freight to mitigate inflationary pressures. | ||

|

|

|

|

|

|

SKA B |

Skanska AB | ||

|

SEK |

228.60 |

+0.26% | |

|

SKA B |

Skanska’s Q2 2025 revenue dipped 6 % to SEK 44.6 billion—just shy of market expectations—while adjusted operating profit reached SEK 1.81 billion, topping consensus of SEK 1.75 billion despite remaining 30 % below last year’s level. Order intake also beat forecasts at SEK 56.7 billion, though it declined around 6–7 % year‑on‑year—buoyed by strong activity in residential and infrastructure projects, particularly in the Nordics, Europe and North America . Skanska’s construction margin expanded to 3.9 %, exceeding the 3.6 % consensus, thanks to disciplined bidding and cost control across its core operations. The company reported good operating cash flow of SEK 1.3 billion, up from SEK 0.3 billion a year ago. | ||

|

|

|

|

|

|

BOL |

Boliden AB | ||

|

SEK |

300.90 |

-0.73% | |

|

BOL |

Boliden reported operating profit of SEK 1.09 billion, missing the SEK 1.48 billion consensus and down sharply from SEK 4.81 billion a year ago, primarily due to a weaker U.S. dollar which shaved around SEK 600 million off earnings, and scheduled smelter maintenance that cost roughly SEK 400 million. Revenues held steady at about SEK 22.29 billion, matching expectations. The company maintained its full-year capex guidance of SEK 15.5 billion and reaffirmed investment plans, noting integration of Somincor and Zinkgruvan mines and record production at the Aitik mine. CEO Mikael Staffas described the performance as “stable despite challenging market conditions” and highlighted long-term benefits from underinvestment in mining, which could support elevated metal prices. | ||

|

|

|

|

|

|

DANSKE |

Danske Bank A/S | ||

|

DKK |

253.40 |

-0.28% | |

|

DANSKE |

Danske Bank posted second-quarter net profit of DKK 5.45 billion, modestly below last year’s DKK 5.84 billion but in line with analyst estimates around DKK 5.50 billion, as strong customer activity and stable credit quality underpinned a resilient performance amid macro uncertainty. Net interest income reached DKK 9.06 billion, exceeding forecasts of DKK 8.98 billion, thanks to increased lending volumes and hedging gains. Pre‑provision profit also edged slightly above consensus at DKK 7.61 billion, supported by disciplined cost management and sustained fee income. Loan impairment charges remained low at DKK 69 million. CET1 at 18.7%, liquidity coverage ratio at 160%, and cost/income ratio improving to 45.4%. Management reaffirmed full‑year net profit guidance of DKK 21–23 billion and flagged expectations of improved capital markets activity in H2. | ||

|

|

|

|

|

|

SCHN |

SCHINDLER | ||

|

CHF |

288.00 |

-1.37% |

Schindler Holding Ltd. release |

|

SCHN |

Schindler’s Q2 2025 Revenue declined 5.7 % in Swiss francs to CHF 2.75 billion—largely due to a stronger franc—but rose 0.4 % in local currencies, surpassing analyst expectations of CHF 2.65 billion. Adjusted EBIT climbed to CHF 372 million—5.7 % ahead of consensus—lifting the adjusted EBIT margin to 13.5 % (compared to 11.6 % a year earlier), while operating profit reached CHF 346 million and net profit rose 4.6 % to CHF 274 million. Strong performance in the modernization division—up over 10 % across all regions—helped offset a weak new-installation market, particularly in China, and bolstered order intake, which rose 4.6 % in local currencies. Operating cash flow was slightly softer at CHF 163 million. Schindler reaffirmed its full-year guidance, targeting low single-digit revenue growth in local currencies and a reported EBIT margin around 12 %. | ||

|

|

|

|

|

|

YAR |

Yara International ASA | ||

|

NOK |

378.80 |

-1.79% | |

|

YAR |

Yara International reported Q2 adjusted EBITDA rising 27% year‑on‑year to USD 652 million (vs. USD 513 million in Q2 2024), underpinned by record-high production, strong commercial execution and tightening nitrogen market fundamentals, still missing analyst's expectations of $668m.. Management flagged rising gas input costs—an additional USD 60 million in Q3 and USD 10 million in Q4—but reaffirmed belief that ongoing cost‑capex reductions, currently ahead of schedule, will deliver annual savings of around USD 180 million by year‑end. The company also announced plans to invest in U.S. ammonia projects to strengthen its portfolio and enhance shareholder returns. | ||

|

|

|

|

|

|

KNEBV |

KONE Corporation | ||

|

EUR |

54.32 |

-3.41% | |

|

KNEBV |

Kone Q2 sales rose by 1.8% year-on-year to €2.85 billion, edging past analyst expectations, while adjusted EBIT increased 3.7% to €347 million, driving the margin up to 12.2% from 11.9% a year earlier. Net profit jumped 6.1% to €277 million, and earnings per share rose to €0.53, also exceeding consensus. Despite stable order intake at €2.32 billion, Kone reported effective margin management as growth in service and modernization offset persistent weakness in China’s new equipment market, which continues to exert pressure on overall order trends and profitability. The business mix shift, supported by operational efficiency and procurement initiatives, was credited for the margin improvement, with management stating these efforts should yield even stronger financial benefits next year. Cash flow from operations improved to €364 million, reflecting disciplined working capital management. Looking forward, Kone narrowed its full-year revenue growth outlook to 2–5% from 1-6% and reaffirmed its adjusted EBIT margin guidance of 11.8–12.4%, underscoring confidence in the service and modernization businesses as key growth drivers for the remainder of 2025, while cautioning that China’s market will remain a drag in the near term. | ||

|

|

|

|

|

|

LAGR B |

Lagercrantz Group AB | ||

|

SEK |

233.80 |

-4.57% | |

|

LAGR B |

Lagercrantz Group reported Q1 net revenue of SEK 2,473 million—up 9.8% year-on-year and slightly ahead of consensus—while EBITA came in 2.9% above expectations at SEK 432 million, producing an EBITA margin of 17.5%. Organic sales growth was moderate at 3%, with acquisitions continuing to underpin broader expansion, as four deals were completed in the period, adding an annualized SEK 560 million in sales. Net profit rose 18.5% from the previous year to SEK 263 million, with earnings per share increasing 17.6% to SEK 1.27. Operating and cash flow metrics also improved. CEO Jörgen Wigh noted generally stable market conditions across most business areas, with positive organic and acquisition-driven growth and healthy cash generation despite lingering geopolitical and sector-specific uncertainties. | ||

|

|

|

|

|

|

GSK | |||

|

GBp |

1347.50 |

-4.64% | |

|

GSK |

GSK shares fell today after a U.S. FDA advisory panel recommended against re-approving its blood cancer therapy Blenrep—a key part of its growth strategy—citing concerns over ocular toxicity and inadequate U.S. trial representation; the panel voted 5–3 and 7–1 against the drug in proposed combinations with bortezomib and pomalidomide respectively, stoking doubts that the FDA will approve the treatment next week. | ||

|

|

|

|

|

|

SAVE |

Nordnet AB (publ) | ||

|

SEK |

265.00 |

-5.29% | |

|

SAVE |

Nordnet’s Q2 operating profit slipped slightly to SEK 893 million from SEK 904 million a year ago, missing consensus by roughly 1 % mainly due to a 6 % dip in commission income—yet was partially offset by net interest income of SEK 601 million and disciplined cost control, which kept expenses 2 % below expectations. The firm reaffirmed robust full‑year guidance, projecting net interest income of about SEK 2.3 billion. Returning capital to shareholders remained a priority: an SEK 8.10 dividend was paid and a SEK 500 million share buyback program launched, with SEK 250 million set to run July–November. | ||

|

|

|

|

|

|

EPI B |

Epiroc AB | ||

|

SEK |

179.20 |

-7.63% |

Epiroc AB release |

|

EPI B |

Good demand from mining customers was offset by significant currency headwinds and continued weakness in construction. Orders received fell 7% year-on-year to SEK 15,276 million, with a negative 9% currency effect, though organic growth was up 2%. Revenues declined 8% to SEK 15,130 million, also hindered by currency, but managed 1% organic growth. Both orders and revenue landed below analyst’s expectations. Operating profit was SEK 2,831 million, down 3% year-on-year and missing forecasts, but the operating margin improved to 18.7% from 17.7%. Adjusted operating profit reached SEK 2,984 million, corresponding to a 19.7% margin. The company highlighted robust mining customer activity, including a record SEK 2.2 billion order from Fortescue in Australia for autonomous and electric equipment. Epiroc reaffirmed its outlook for continued strength in mining demand but expects construction to remain subdued. | ||

|

|

|

|

|

|

ATCO B | |||

|

SEK |

130.70 |

-8.05% | |

|

ATCO B |

Atlas Copco delivered a mixed set of second-quarter results, with both orders received and revenues falling 8% year-on-year to SEK 40.1 billion and SEK 41.2 billion respectively, due largely to significant currency headwinds and uneven demand across business segments. On an organic basis, orders declined by just 1% and revenues by 2%, as the group faced particular softness in compressors—especially gas and process units—while vacuum orders were broadly flat and service lines showed resilience. Operating profit dropped 10% to SEK 8.5 billion, translating to a margin of 20.6%, and the adjusted operating profit of SEK 8.4 billion was below market expectations. The company expects customer activity to remain stable in the coming quarters but flagged ongoing currency challenges and an uncertain macroeconomic outlook. | ||

|

|

|

|

|

|

ELUX B | |||

|

SEK |

60.56 |

-15.77% | |

|

ELUX B |

Electrolux reported a return to profit in the second quarter of 2025, with operating income rising sharply to SEK 797 million from SEK 419 million a year ago and an improved operating margin of 2.5%, driven largely by a positive turnaround in North America where the company posted a profit despite weak market demand. Without a SEK 180 million gain from the divestment of the Kelvinator trademark in India, Electrolux missed analysts' expectation. Net sales fell to SEK 31.3 billion from SEK 33.8 billion, though organic sales growth was a modestly positive 1.8% as gains in North and Latin America offset a slight decrease in Europe, Asia-Pacific, Middle East, and Africa. CEO Yannick Fierling highlighted that price increases helped mitigate higher costs from newly implemented U.S. tariffs, particularly in North America, even as Europe faced tough competition and a shift toward lower price points. Despite the profit improvement, Electrolux saw operating cash flow after investments swing to a negative SEK 741 million, reflecting increased working capital needs and a large antitrust fine payment. The company maintained its market outlook for the rest of the year, emphasizing ongoing consumer uncertainty but reaffirming its commitment to transformation, cost control, and price actions to counter continued external pressures. | ||

Versus early hours

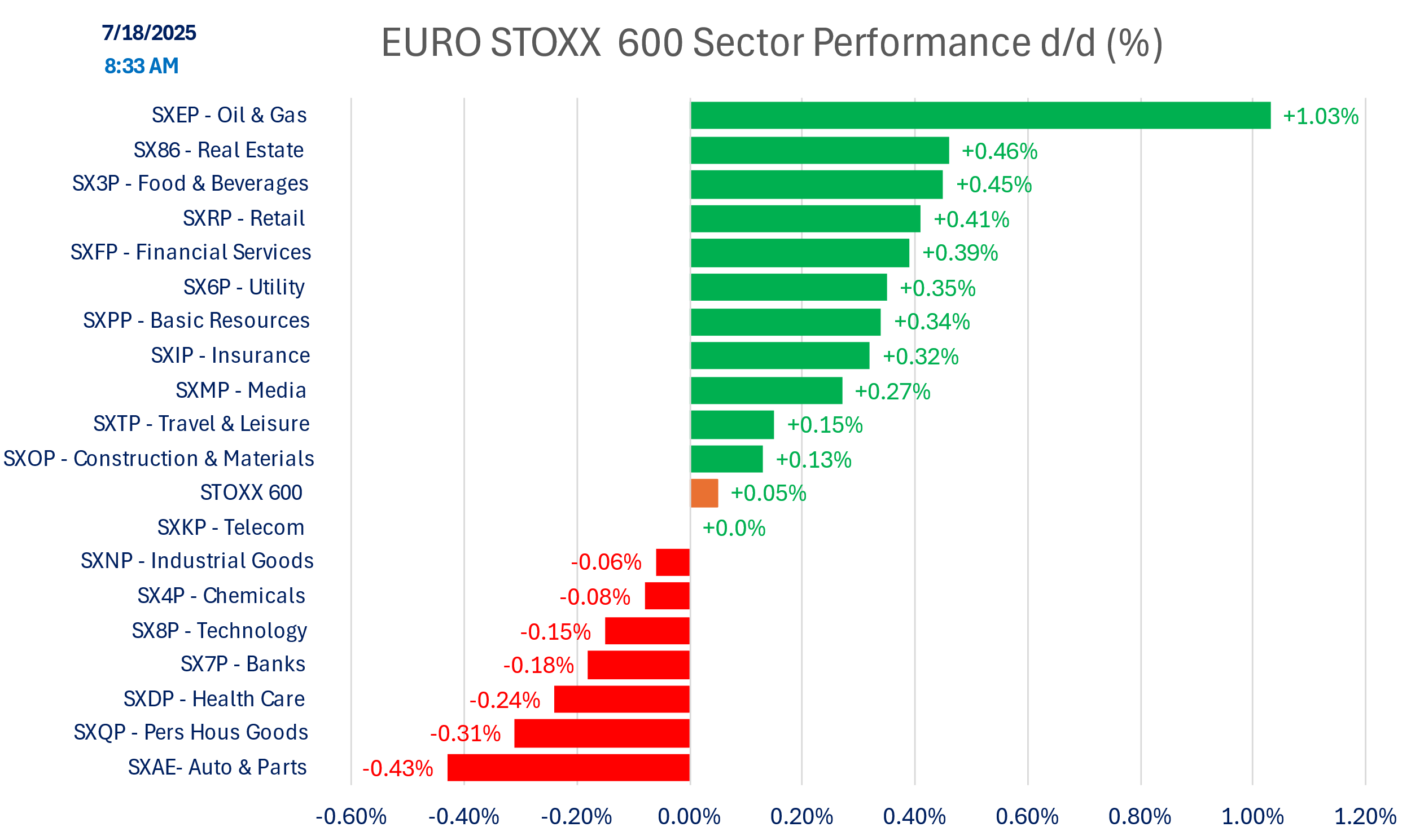

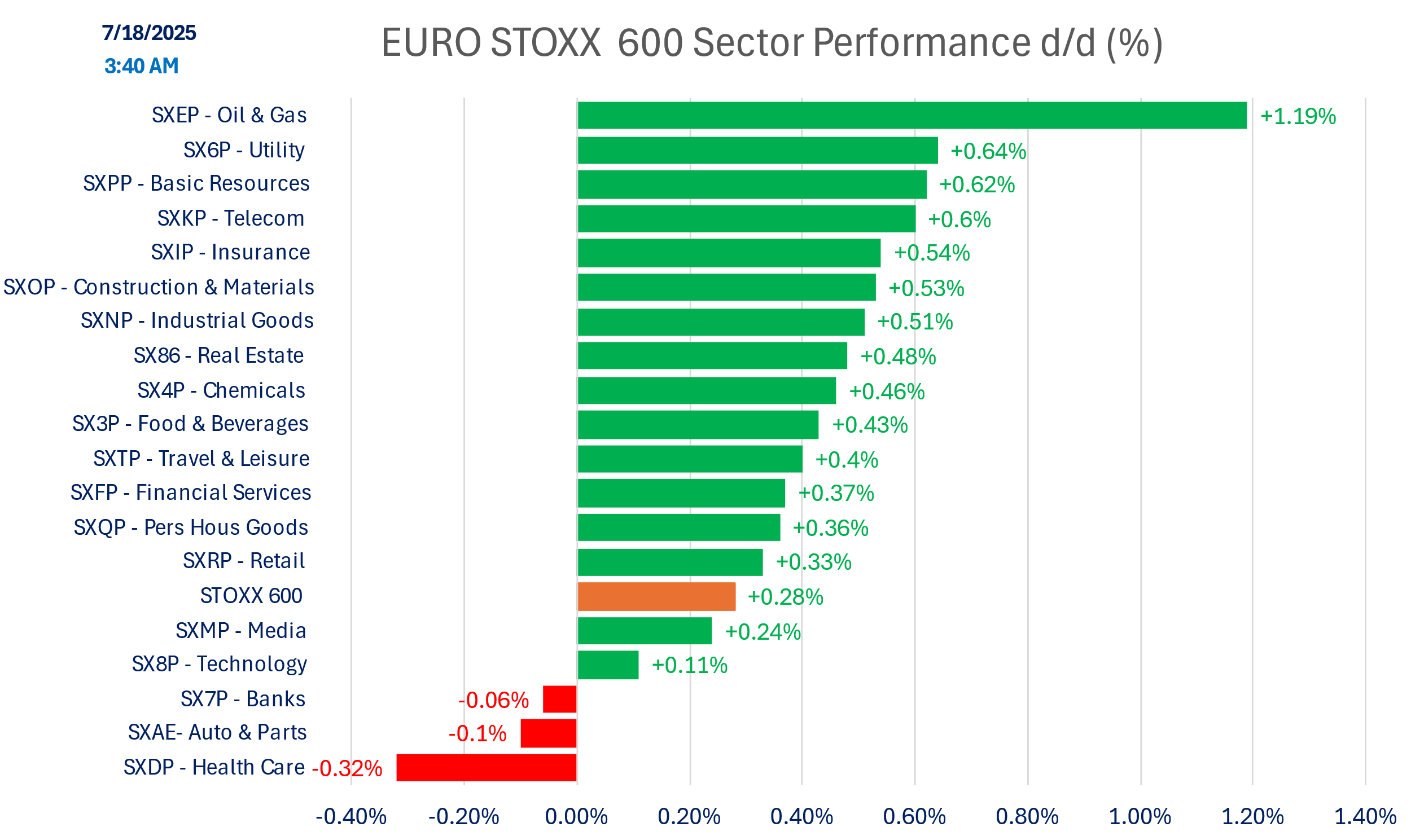

SECTOR PERFORMANCE

Versus early hours:

Indices

Versus early hours

DISCLAIMER

This material is provided by Eurolink Securities L.L.C. for information purposes only and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. The opinions, forecasts, facts, and recommendations contained here are based upon the information available as of the date of the report. The analysts are basing their opinions upon information they have received from sources they believe to be accurate and reliable. The report is directed exclusively at Institutional Investors who make their own decisions regardless of the present publication or opinions reflected within the report. This material is not a complete analysis of all material facts respecting any issuer, industry, or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. A guarantee of completeness and accuracy of the information in this report is not assumed by Eurolink Securities LLC and any liability arising from the use of this report is excluded and disclaimed. The information contained herein is as of the date and time referenced above. Opinions and recommendations are subject to change without notice. Eurolink Securities L.L.C. has any obligation to update such information. Past performance is not indicative of future results. The investments discussed may fluctuate in price or value. Changes in rates of exchange may have an adverse effect on the value of investments. Transactions involving the financial instruments mentioned herein may not be suitable for all investors. Eurolink Securities L.L.C. has no obligation to continue to provide this research product and no such obligation is implied or guaranteed. The distribution rights of this report belong solely to Eurolink Securities L.L.C. It is prohibited to publish or to give this report or parts to third parties. No parts of it may be reproduced, resold, stored, or transmitted in any printed, electronic, or other form, or used for generating or marketing any printed or electronic publication, service, or product without Eurolink Securities LLC’s previous approval.